Reports

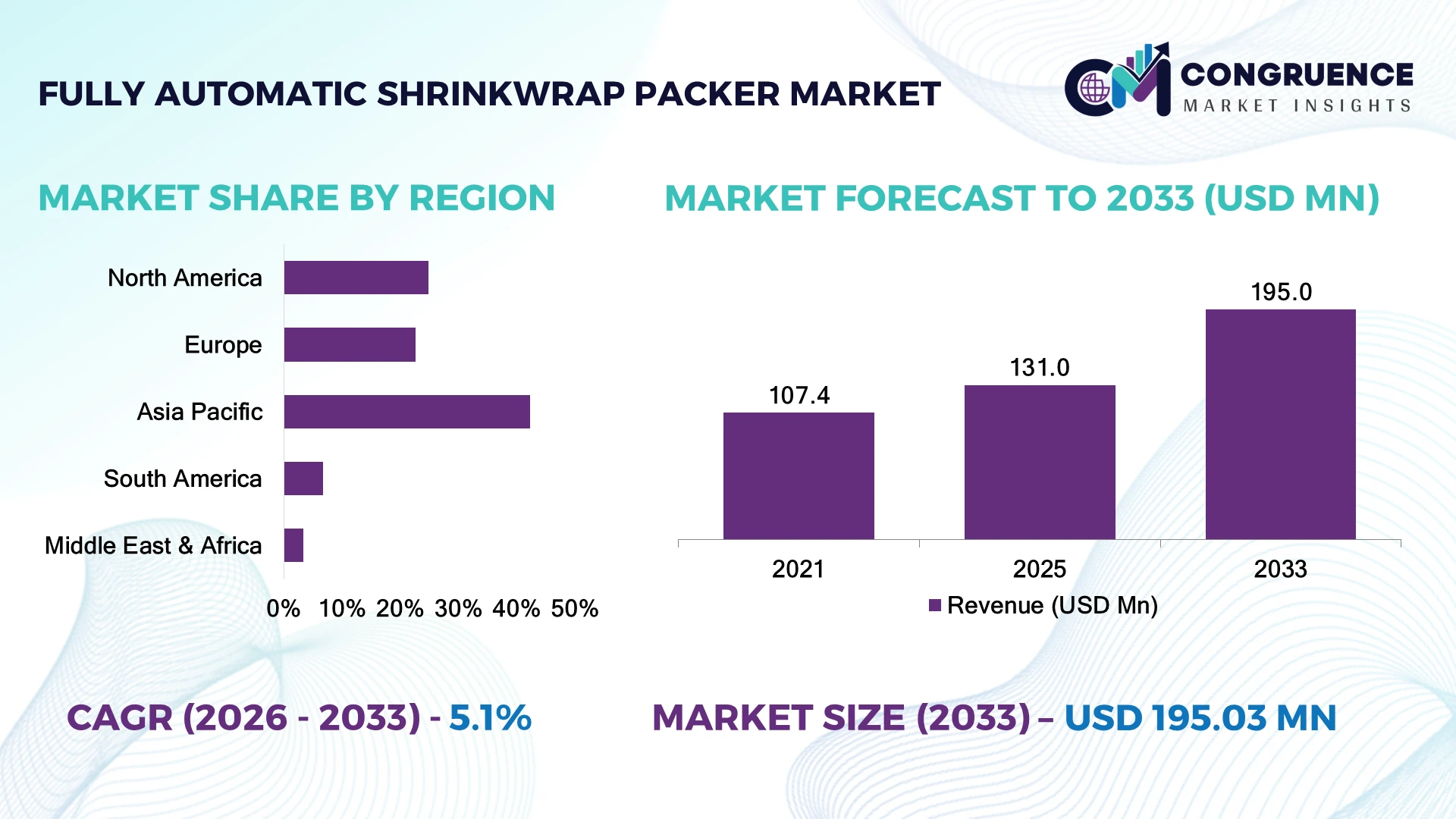

The Global Fully Automatic Shrinkwrap Packer Market was valued at USD 131.0 Million in 2025 and is anticipated to reach a value of USD 195.0 Million by 2033 expanding at a CAGR of 5.1% between 2026 and 2033. Growth is driven by rapid automation across food, beverage, pharmaceutical, and consumer goods packaging lines, supported by high-speed production upgrades and energy-efficient shrink packaging technologies.

China leads the global market with approximately 34% of manufacturing capacity, supported by extensive packaging machinery production, export-oriented manufacturing, and large-scale food processing investments. Germany accounts for nearly 12% of advanced packaging equipment output, emphasizing precision automation and Industry 4.0 integration, while China's industrial packaging installations exceed Germany by more than 2.5 times. Expanding manufacturing localization and resilient supply-chain strategies continue strengthening regional competitiveness.

Manufacturers prioritizing intelligent automation, production flexibility, and localized equipment deployment will secure stronger competitive positioning across high-volume packaging operations.

Market Size & Growth: USD 131.0 Million in 2025, projected to reach USD 195.0 Million by 2033 at 5.1% CAGR, supported by factory automation and high-speed packaging modernization.

Top Growth Drivers: Food packaging automation (+28%), pharmaceutical packaging expansion (+22%), and e-commerce fulfillment demand (+19%) accelerate equipment adoption.

Short-Term Forecast: By 2028, packaging line efficiency is expected to improve by over 16% while material waste declines by approximately 11%.

Emerging Technologies: AI-enabled inspection, servo-driven automation, and digital monitoring systems improve packaging accuracy and operational uptime.

Regional Leaders: Asia-Pacific approaches USD 78 Million, Europe exceeds USD 49 Million, and North America reaches nearly USD 41 Million, driven by smart factory adoption and regional manufacturing expansion.

Consumer/End-User Trends: More than 63% of large packaging facilities prioritize fully automatic systems to reduce labor dependency and improve consistency.

Pilot/Case Example: In 2024, an automated beverage packaging upgrade improved packaging throughput by approximately 24% while reducing unplanned downtime by 15%.

Competitive Landscape: Leading manufacturers collectively account for nearly 42% market share, with Krones AG, Syntegon, SMI Group, OCME, and Douglas Machine serving major global industries.

Regulatory & ESG Impact: Sustainable packaging initiatives reduce packaging film consumption by up to 14% while supporting energy-efficient production operations.

Investment & Funding: More than USD 450 Million has been directed toward packaging automation expansion, strategic partnerships, and advanced manufacturing upgrades worldwide.

Innovation & Future Outlook: Intelligent predictive maintenance, robotic integration, and digital production analytics continue reshaping next-generation packaging operations.

Fully Automatic Shrinkwrap Packer systems are witnessing stronger deployment across food processing, pharmaceuticals, beverages, and logistics where high-speed, reliable secondary packaging is essential. Smart sensors, vision-guided inspection, and predictive maintenance capabilities are improving equipment utilization, with automated packaging accuracy exceeding 98% in modern production environments. Ongoing supply-chain diversification and sustainable packaging initiatives are further accelerating adoption, setting the foundation for broader strategic transformation.

Fully Automatic Shrinkwrap Packer systems have become strategically important as manufacturers pursue greater production efficiency, operational consistency, and lower dependence on manual labor. Increasing supply-chain restructuring and factory modernization programs are encouraging companies to replace conventional packaging lines with intelligent automated equipment capable of supporting high-volume production while maintaining product quality and traceability.

Modern servo-controlled shrinkwrap packers process up to 25% more packs per hour than conventional pneumatic systems while reducing energy consumption by approximately 15%, delivering measurable operating advantages. Asia-Pacific continues expanding manufacturing capacity and equipment deployment at a larger scale, whereas Europe remains focused on precision engineering, digital automation, and sustainable production standards. During the next two to three years, integrated machine monitoring and predictive maintenance adoption is expected to exceed 40% across newly installed automated packaging lines.

Global manufacturers are increasingly deploying fully automated shrinkwrap systems in beverage and consumer goods facilities to minimize production interruptions and improve packaging consistency. Companies are expanding regional manufacturing partnerships, strengthening localized service networks, and investing in modular automation platforms that simplify future upgrades. These strategic priorities are reinforcing competitive differentiation, improving operational resilience, and establishing long-term advantages across increasingly automated industrial packaging ecosystems.

Manufacturers are rapidly replacing semi-automatic packaging operations with fully automated shrinkwrap systems to improve throughput, consistency, and labor efficiency. More than 62% of large food and beverage production facilities now prioritize automated end-of-line packaging, while servo-driven equipment improves packaging speed by nearly 25% and reduces product rejection by approximately 18%. China's industrial modernization initiatives and expanding consumer goods manufacturing continue accelerating equipment deployment across high-volume factories. This operational shift enables continuous production with minimal manual intervention, reducing downtime and packaging variability. Equipment suppliers are responding through modular machine platforms, AI-enabled inspection technologies, localized manufacturing expansion, and strategic partnerships with system integrators. A key competitive advantage increasingly lies in delivering flexible equipment capable of supporting multiple packaging formats without major production interruptions.

High initial investment requirements and dependence on specialized automation components continue limiting wider deployment among small and medium-sized manufacturers. Imported motion controllers, servo motors, and industrial sensors account for nearly 38% of total equipment cost, while lead times for selected electronic components remain 20–30% longer than pre-disruption levels in several manufacturing markets. Germany and Japan continue supplying critical automation technologies, creating procurement exposure during supply-chain disruptions. These structural constraints delay production expansion, increase installation costs, and extend commissioning schedules. Manufacturers are reducing risk by localizing component sourcing, establishing long-term supplier agreements, and redesigning equipment with standardized control architectures that improve component interchangeability and procurement flexibility.

The integration of smart manufacturing technologies with sustainable packaging operations is creating new commercial opportunities beyond conventional production efficiency. More than 45% of newly commissioned packaging facilities are incorporating Industrial IoT connectivity, while intelligent monitoring systems reduce maintenance interventions by approximately 20% and improve equipment utilization by nearly 15%. India's expanding packaged food industry and government-backed manufacturing initiatives are encouraging investment in digitally connected packaging infrastructure. Equipment manufacturers are developing cloud-enabled diagnostics, digital twin capabilities, and recyclable film-compatible systems while expanding technology partnerships with software providers. A significant strategic opportunity lies in offering data-driven packaging optimization services that generate recurring customer value alongside equipment sales.

Successful deployment increasingly depends on integrating packaging equipment with enterprise automation platforms, warehouse systems, and digital production environments. Nearly 41% of industrial facilities identify skilled automation personnel shortages as a major implementation constraint, while software integration activities can represent almost 18% of total project deployment time. The United States continues facing increasing demand for multidisciplinary automation engineers capable of managing robotics, machine vision, and industrial networking simultaneously. Inconsistent interoperability between legacy equipment and modern digital control platforms affects operational stability and long-term scalability. Leading manufacturers are addressing these challenges through standardized communication protocols, expanded technical training programs, digital commissioning tools, and collaborative partnerships with automation solution providers to ensure reliable large-scale deployment.

AI-Driven Packaging Intelligence Intelligent machine vision and AI-enabled inspection are becoming standard across high-speed packaging lines, with defect detection accuracy improving by nearly 30% and unplanned downtime declining by approximately 18%. Labor shortages across Germany and the United States are accelerating automated quality control deployment. Equipment manufacturers are integrating predictive analytics, remote diagnostics, and centralized production monitoring to improve operational continuity while reducing manual inspection requirements.

Sustainable Film Optimization Packaging producers are redesigning shrinkwrap systems to process thinner recyclable films, reducing material consumption by 12–15% without compromising seal integrity. New environmental packaging regulations across the European Union are encouraging equipment upgrades that minimize energy use and packaging waste. Machinery suppliers are responding with servo-controlled sealing technology, precision temperature management, and retrofit solutions that allow manufacturers to meet sustainability targets with limited production disruption.

Flexible Multi-Format Production Consumer product diversification is increasing demand for packaging equipment capable of handling multiple product dimensions on a single production line. Modern automatic changeover systems reduce product transition time by nearly 40%, while overall equipment utilization improves by approximately 20%. Chinese manufacturing facilities are increasingly adopting modular machine architectures, enabling companies to expand production capacity without replacing complete packaging systems.

Connected Manufacturing Expansion Industrial facilities are linking shrinkwrap packers with Manufacturing Execution Systems and Industrial IoT platforms, increasing production visibility by over 35% and reducing maintenance response times by nearly 22%. Global supply-chain restructuring is encouraging localized manufacturing supported by digitally connected packaging operations. Leading equipment suppliers are expanding software partnerships and cloud-enabled service platforms to deliver continuous performance optimization and lifecycle support.

Inline Fully Automatic Shrinkwrap Packers represent the largest market segment, accounting for approximately 36% of total installations due to their continuous production capability, high throughput, and compatibility with integrated packaging lines. Food and beverage manufacturers particularly favor inline systems because they simplify synchronization with filling, labeling, and palletizing operations while reducing operator intervention. Rotary systems continue serving high-volume beverage applications, whereas Side-Seal and L-Bar equipment remain preferred for medium-volume operations requiring packaging flexibility and compact installation footprints. Wrap-Around Fully Automatic Shrinkwrap Packers are emerging as the fastest-growing segment as manufacturers seek lower film consumption and stronger package stability during transportation. Nearly 27% of newly commissioned consumer goods packaging lines now incorporate wrap-around technology to improve logistics efficiency. Equipment manufacturers are expanding modular product portfolios, investing in faster changeover capabilities, and developing intelligent control systems that support multiple packaging formats. These evolving investment priorities are shifting demand toward adaptable equipment platforms capable of supporting increasingly diversified production environments.

Food & Beverages remain the dominant application, contributing nearly 48% of equipment demand because of high production volumes, strict hygiene standards, and continuous packaging requirements. Automated shrinkwrap systems improve packaging consistency, reduce manual handling, and support rapid distribution across retail supply chains. Pharmaceuticals continue requiring precision packaging for secondary packaging operations, while Consumer Goods and Personal Care manufacturers increasingly automate packaging lines to improve throughput and packaging quality. Electronics represents the fastest-growing application as manufacturers require protective transit packaging for increasingly complex electronic products. Approximately 23% of newly automated electronics packaging facilities now deploy fully automatic shrinkwrap systems integrated with vision inspection and traceability solutions. Industrial Products and other specialty manufacturing applications continue adopting customized packaging configurations to improve logistics efficiency. Equipment suppliers are responding through sector-specific machine designs, software integration, and flexible automation solutions tailored to evolving production requirements.

Food & Beverage Manufacturers represent the largest end-user segment, accounting for approximately 44% of global installations due to continuous production schedules, stringent packaging standards, and expanding packaged food consumption. Large manufacturing facilities increasingly deploy fully automatic shrinkwrap systems to improve line balancing, reduce labor dependency, and achieve consistent packaging quality. Consumer Goods Manufacturers remain significant buyers because diversified product portfolios require flexible and reliable secondary packaging operations. Logistics & E-commerce Fulfillment Centers are emerging as the fastest-growing end-user segment as higher parcel volumes demand faster packaging workflows and standardized shipment preparation. Nearly 29% of newly established automated fulfillment facilities now incorporate high-speed shrink packaging systems for bundled products and promotional packaging. Contract Packaging Companies continue investing in modular equipment to accommodate multiple customer requirements, while Pharmaceutical Companies prioritize validated automation and packaging traceability. Equipment suppliers are strengthening competitiveness through customized machine configurations, lifecycle service agreements, and localized technical support.

Asia-Pacific accounted for the largest market share at 42.3% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America represents approximately 24.8% of the global Fully Automatic Shrinkwrap Packer Market, supported by extensive deployment across food processing, pharmaceuticals, beverages, and consumer goods manufacturing. High labor costs and increasing automation priorities continue encouraging manufacturers to replace conventional packaging systems with intelligent shrinkwrap solutions. More than 58% of newly installed end-of-line packaging equipment incorporates digital monitoring and predictive maintenance capabilities. Investments in smart manufacturing facilities and warehouse automation are strengthening equipment demand, while packaging machinery suppliers continue expanding regional service capabilities, aftermarket support, and software-enabled performance optimization to improve production efficiency and equipment availability.

United States Market Outlook: The United States remains the largest market in North America due to its extensive food processing industry, advanced pharmaceutical manufacturing, and mature automation ecosystem. Large manufacturers increasingly deploy fully automatic shrinkwrap systems integrated with robotics and manufacturing execution systems to improve packaging consistency and production throughput. Nearly 65% of large-scale packaging facilities are investing in digital production technologies, reinforcing the country's leadership in intelligent packaging automation.

Europe contributes approximately 22.7% of the global market through strong industrial automation capabilities, precision engineering, and sustainability-focused manufacturing investments. Environmental packaging regulations continue accelerating equipment upgrades that support recyclable films, lower energy consumption, and improved packaging efficiency. Around 54% of newly commissioned packaging equipment incorporates energy-efficient servo technologies and digital machine diagnostics. Packaging equipment manufacturers are expanding modular machine platforms while strengthening partnerships with automation specialists to improve production flexibility across food, beverage, and pharmaceutical manufacturing operations.

Germany Market Outlook: Germany leads the European market through its globally recognized packaging machinery manufacturing sector and advanced Industry 4.0 adoption. Domestic manufacturers continue investing in intelligent production systems capable of supporting flexible manufacturing and high-speed packaging operations. Approximately 60% of newly deployed industrial packaging systems include integrated digital monitoring functions, enabling higher productivity and improved operational reliability across export-oriented manufacturing facilities.

Asia-Pacific dominates the global market with a 42.3% share, supported by extensive manufacturing capacity, expanding packaged food production, and growing industrial automation investments. China, India, Japan, and Southeast Asian manufacturing hubs continue increasing deployment of high-speed packaging equipment to improve production efficiency and export competitiveness. Nearly 46% of new packaging machinery installations within the region feature intelligent automation and remote operational monitoring. Equipment suppliers are expanding localized production, engineering support, and component sourcing to strengthen supply-chain resilience while reducing equipment delivery timelines.

China Market Outlook: China represents the largest national market owing to its massive consumer goods manufacturing base and leadership in packaging machinery production. Food, beverage, household products, and logistics industries continue investing in automated packaging systems to improve throughput and product consistency. The country accounts for approximately 34% of global packaging machinery manufacturing capacity, providing strong operational advantages through localized production, competitive supply chains, and continuous industrial modernization.

South America is experiencing increasing demand for fully automatic shrinkwrap systems as food processing, beverage production, and consumer goods manufacturing expand across key industrial economies. The region accounts for approximately 6.8% of global market activity, while modernization of production facilities continues improving equipment deployment. Automated packaging installations have increased by nearly 19% over the past three years as manufacturers focus on improving operational efficiency and reducing packaging waste. Companies are strengthening regional distribution partnerships and technical service capabilities to support growing industrial automation requirements despite infrastructure and logistics challenges.

Brazil Market Outlook: Brazil leads the regional market through its large food processing, beverage, and consumer packaged goods industries. Domestic manufacturers continue modernizing packaging operations to improve productivity and export competitiveness while expanding investments in automated production lines. More than half of newly established high-volume food manufacturing facilities are adopting integrated packaging automation solutions to improve packaging quality and operational efficiency.

The Middle East & Africa market continues expanding through industrial diversification, food manufacturing investments, and modernization of packaging infrastructure. The region contributes approximately 3.4% of global demand while governments continue supporting domestic manufacturing and industrial development initiatives. Nearly 27% of recently commissioned industrial production facilities incorporate automated packaging technologies to improve operational performance and product consistency. Equipment suppliers are increasing local partnerships, technical support capabilities, and training programs to accelerate deployment across emerging manufacturing sectors.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically important market in the region due to ongoing industrial diversification initiatives, expanding food manufacturing capacity, and advanced logistics infrastructure. Manufacturers are increasingly investing in automated packaging systems that improve production efficiency and reduce dependence on manual operations. Industrial modernization programs have accelerated adoption of digitally controlled packaging equipment across large manufacturing facilities, strengthening the country's position as a regional packaging automation hub.

Competition is led by Krones AG, Syntegon, OCME, SMI Group, and Douglas Machine, while regional machinery manufacturers compete aggressively on pricing and localized customization. Global technology leaders primarily compete on automation performance, digital integration, and lifecycle services, whereas regional suppliers focus on faster delivery and lower capital costs. The top five companies collectively account for approximately 46% of the global market. More than 60% of customer evaluations prioritize production speed and equipment reliability, while over 55% emphasize rapid format changeovers and digital diagnostics during procurement. Companies are strengthening competitiveness through manufacturing expansion, software-enabled predictive maintenance, strategic distributor partnerships, and vertically integrated packaging solutions. Competition is increasingly shifting toward intelligent automation, sustainable packaging compatibility, and remote machine monitoring instead of conventional mechanical performance alone. High engineering expertise, established service networks, and application-specific customization create significant barriers for new entrants. Winning requires scalable automation platforms, superior aftersales support, continuous innovation, and localized customer engagement.

Syntegon Technology GmbH

SMI S.p.A.

OCME S.r.l.

Douglas Machine Inc.

Polypack Inc.

Aetna Group S.p.A.

SMIPACK S.p.A.

Pacteon Group

Massman Automation Designs LLC

Clearpack Group

Fuji Machinery Co., Ltd.

Fully automatic shrinkwrap packers are rapidly evolving through servo-driven motion control, AI-enabled machine vision, and Industrial IoT connectivity. Servo-controlled systems improve positioning accuracy while reducing energy consumption by approximately 15%, and AI-based inspection lowers packaging defects by nearly 25%. More than 58% of newly installed premium packaging lines now incorporate remote diagnostics and predictive maintenance capabilities, allowing manufacturers to minimize downtime and improve overall equipment effectiveness.

Legacy pneumatic machines are steadily being replaced by intelligent automation platforms capable of delivering around 20% higher throughput and significantly faster product changeovers. Digital twin technology, cloud-based machine analytics, and integrated manufacturing execution connectivity are becoming standard among leading equipment suppliers. Global manufacturers with diversified product portfolios benefit most because these technologies enable flexible production scheduling, simplified maintenance planning, and improved packaging consistency across multiple production sites.

Between 2026 and 2028, collaborative robotics, machine learning optimization, and adaptive sealing technologies will reshape packaging operations. Companies investing early in intelligent automation, modular machine architecture, and connected service platforms will strengthen operational resilience, accelerate deployment, reduce lifecycle costs, and establish stronger competitive differentiation across increasingly automated packaging environments.

April 2025 – Syntegon launched the Pack 103 flow wrapping platform delivering output of up to 175 packs per minute, providing a cost-effective automation solution for food, medical, and non-food manufacturers while improving production flexibility for small and medium enterprises. Source: www.syntegon.com

September 2025 – Krones announced the reorganization of its Compact Class business, integrating development activities across product lines to strengthen competitiveness and accelerate innovation for low- and medium-output packaging systems. The initiative improves engineering collaboration across multiple equipment families. Source: www.krones.com

May 2026 – Krones introduced a redesigned Variopac Pro shrink tunnel capable of reducing energy consumption by at least 20% while improving shrink-wrap quality through optimized airflow and heating technology, lowering operating costs for beverage packaging lines. Source: www.krones.com

2026 – OCME expanded its secondary packaging portfolio with high-speed automatic shrink-wrap and combined packaging systems capable of processing up to 450 packs per minute, strengthening operational flexibility for beverage and consumer goods manufacturers.

This report provides comprehensive analysis of the Fully Automatic Shrinkwrap Packer Market across major equipment types, applications, end-user industries, and regional markets between 2026 and 2033. It evaluates inline, rotary, wrap-around, side-seal, L-bar, and other equipment configurations while assessing deployment across food and beverages, pharmaceuticals, consumer goods, electronics, industrial products, and additional manufacturing sectors. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, together representing virtually all global industrial packaging demand.

The report examines technology adoption, automation deployment, digital manufacturing integration, sustainability initiatives, and competitive positioning across leading equipment manufacturers. More than 60% of the analysis focuses on operational trends, enterprise adoption, and packaging modernization strategies. It delivers actionable intelligence supporting investment planning, product development, manufacturing expansion, supplier evaluation, competitive benchmarking, market entry decisions, and long-term strategic positioning across established and emerging packaging automation segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 131.0 Million |

| Market Revenue (2033) | USD 195.0 Million |

| CAGR (2026–2033) | 5.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Krones AG; Syntegon Technology GmbH; SMI S.p.A.; OCME S.r.l.; Douglas Machine Inc.; Polypack Inc.; Aetna Group S.p.A.; SMIPACK S.p.A.; Pacteon Group; Massman Automation Designs LLC; Clearpack Group; Fuji Machinery Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |