Reports

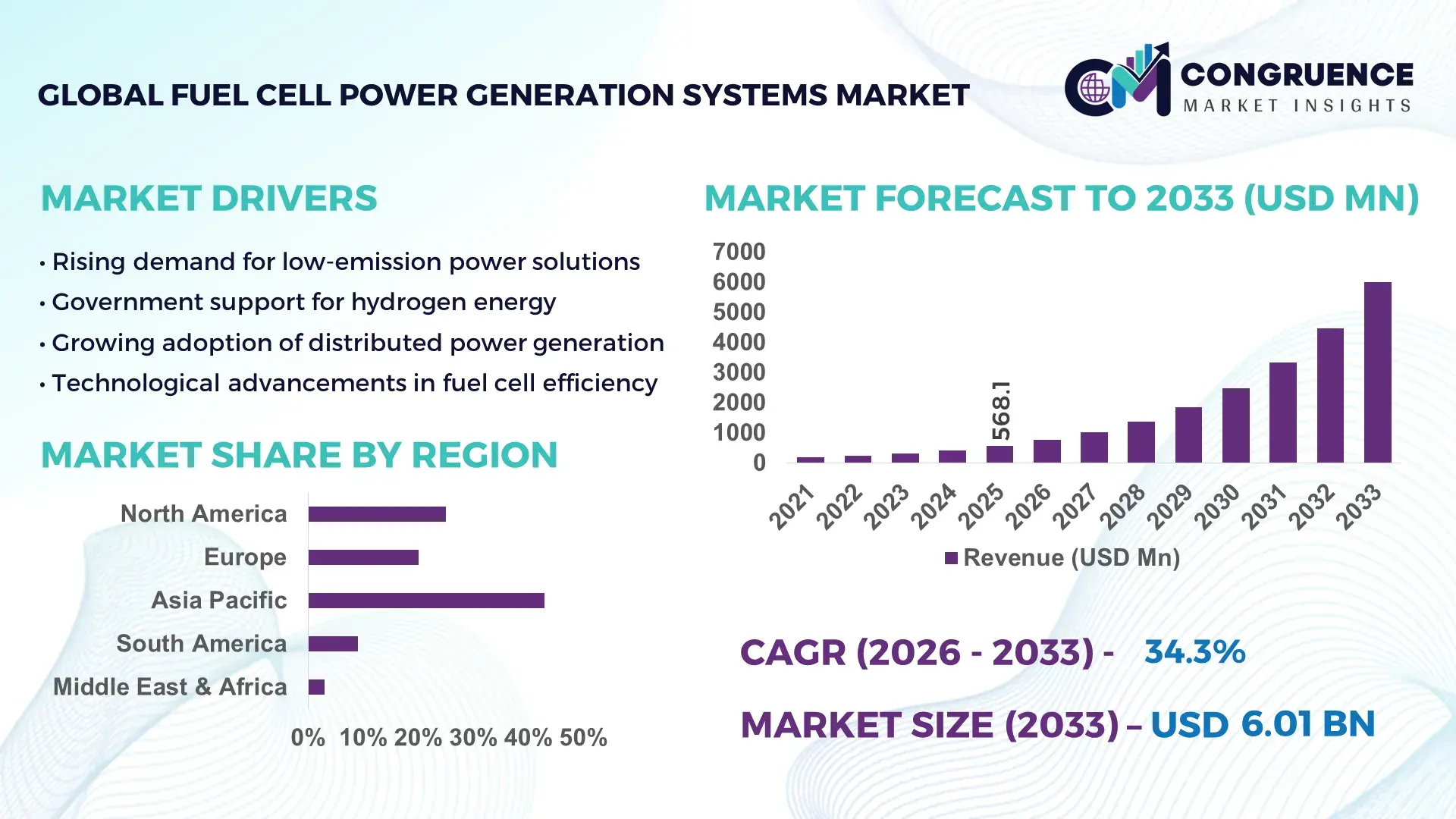

The Global Fuel Cell Power Generation Systems Market was valued at USD 568.14 Million in 2025 and is anticipated to reach a value of USD 6012.71 Million by 2033 expanding at a CAGR of 34.3% between 2026 and 2033. This rapid expansion is driven by accelerating deployment of low-emission distributed power solutions across industrial and grid-support applications.

Japan represents the dominant national ecosystem in the Fuel Cell Power Generation Systems Market, supported by advanced manufacturing capacity, large-scale deployment, and sustained capital investment. As of 2024, Japan had installed over 400,000 stationary fuel cell units under residential and commercial programs, with cumulative system capacity exceeding 1.5 GW. Annual public–private investment in hydrogen and fuel cell technologies surpassed USD 3.5 billion, focused on solid oxide and proton exchange membrane systems. Fuel cell power systems are widely applied in commercial buildings, data centers, hospitals, and microgrids, with residential combined heat and power systems accounting for over 60% of domestic installations. Technological progress includes system electrical efficiencies above 55% and operational lifetimes exceeding 80,000 hours in commercial deployments.

Market Size & Growth: USD 568.14 Million in 2025 projected to USD 6012.71 Million by 2033 at a 34.3% CAGR, driven by clean distributed power adoption.

Top Growth Drivers: Grid decarbonization targets (42%), efficiency gains over conventional generators (38%), rising hydrogen infrastructure deployment (31%).

Short-Term Forecast: By 2028, system-level cost reductions of approximately 22% supported by stack durability improvements and scaled manufacturing.

Emerging Technologies: Solid oxide fuel cells, high-temperature PEM fuel cells, and hybrid fuel cell–battery power systems.

Regional Leaders: Asia-Pacific USD 2.7 Billion by 2033 with residential CHP uptake; Europe USD 1.9 Billion via industrial decarbonization; North America USD 1.2 Billion led by data centers.

Consumer/End-User Trends: Growing adoption by data centers, hospitals, utilities, and commercial campuses for baseload and backup power.

Pilot or Case Example: A 2024 multi-megawatt fuel cell microgrid project achieved 30% efficiency improvement and 25% downtime reduction.

Competitive Landscape: Market leader holds ~18% share, followed by Bloom Energy, Doosan Fuel Cell, Mitsubishi Power, FuelCell Energy, and Ballard Power Systems.

Regulatory & ESG Impact: Net-zero mandates, hydrogen strategies, and investment tax credits accelerating deployment.

Investment & Funding Patterns: Over USD 14 Billion invested since 2022, with increased project finance and public–private partnership models.

Innovation & Future Outlook: Integration with hydrogen hubs, AI-based system optimization, and utility-scale fuel cell plants shaping long-term growth.

Fuel Cell Power Generation Systems serve critical industry sectors including commercial buildings, industrial facilities, utilities, data centers, and institutional infrastructure, with commercial and industrial users contributing more than half of total system deployments. Recent innovations such as high-durability stacks, modular megawatt-scale platforms, and hydrogen-ready designs are improving lifecycle economics and operational flexibility. Regulatory support through clean energy mandates, carbon pricing, and hydrogen roadmaps continues to strengthen market fundamentals. Consumption growth is strongest in Asia-Pacific due to urban distributed power demand, while Europe and North America are driven by industrial decarbonization and grid resilience needs. Emerging trends include integration with renewable energy storage, use of low-carbon hydrogen, and expansion of fuel cells as primary baseload power, positioning the market for sustained long-term expansion.

The strategic relevance of the Fuel Cell Power Generation Systems Market is rooted in its role as a scalable, low-emission power solution aligned with global energy transition strategies, grid resilience planning, and industrial decarbonization goals. Fuel cell systems enable continuous baseload and backup power with electrical efficiencies exceeding 55% in commercial deployments, positioning them as a strategic alternative to diesel generators and gas turbines. Solid Oxide Fuel Cell (SOFC) technology delivers approximately 18% higher electrical efficiency compared to conventional gas engine generators, while also enabling combined heat and power utilization.

From a regional perspective, Asia-Pacific dominates in volume deployment due to extensive residential and commercial installations, while Europe leads in adoption intensity, with over 46% of large industrial enterprises integrating fuel cell-based onsite power or pilot projects as part of decarbonization strategies. North America continues to scale utility and data center applications, particularly in grid-constrained regions.

Over the short term, by 2028, AI-enabled predictive maintenance and digital twin optimization are expected to improve system uptime by nearly 25% and reduce unplanned maintenance costs by 20%. ESG alignment is becoming central to procurement strategies, with firms committing to emissions intensity reductions of up to 40% and recycling or recovery of over 90% of stack materials by 2030. In 2024, South Korea achieved a 30% reduction in grid-sourced electricity consumption across public facilities through large-scale fuel cell power generation integrated with smart energy management systems. Looking ahead, the Fuel Cell Power Generation Systems Market is positioned as a foundational pillar supporting energy resilience, regulatory compliance, and long-term sustainable industrial growth.

The growing demand for uninterrupted power supply in data centers, hospitals, telecommunications, and industrial facilities is a primary driver of the Fuel Cell Power Generation Systems market. Globally, data center electricity demand alone is projected to exceed 1,000 TWh annually by the late 2020s, increasing pressure on grid reliability. Fuel cell power generation systems offer availability levels above 98% while producing near-zero local emissions, making them attractive replacements for diesel backup generators. In commercial applications, combined heat and power fuel cell systems can improve total energy utilization efficiency to over 80%, significantly lowering fuel consumption per unit of output. This reliability-performance combination is accelerating adoption in mission-critical sectors where downtime costs can exceed USD 8,000 per minute.

Despite declining system costs, fuel cell power generation systems continue to face adoption restraints due to high initial capital expenditure compared to conventional generation technologies. Installed costs for large stationary fuel cell systems remain multiple times higher than gas engine generators on a per-kilowatt basis. Additionally, hydrogen supply infrastructure remains unevenly distributed, with fewer than 15% of industrial zones globally having direct access to low-carbon hydrogen. Specialized installation requirements, long permitting timelines, and limited availability of trained service personnel further constrain rapid deployment, particularly in emerging markets. These economic and infrastructure-related barriers slow purchasing decisions even where long-term operational benefits are well recognized.

Industrial decarbonization targets and expanding hydrogen ecosystems present significant opportunities for the Fuel Cell Power Generation Systems market. Heavy industries such as chemicals, refining, and steel are increasingly adopting onsite low-emission power solutions to reduce scope 1 and scope 2 emissions. Government-backed hydrogen hubs and pipeline projects are improving fuel availability, enabling larger-scale fuel cell deployments above 10 MW capacity. Advancements in fuel flexibility now allow systems to operate on biogas, ammonia-derived hydrogen, and blended fuels, broadening application potential. These developments open new growth avenues across industrial parks, ports, and export-oriented manufacturing clusters seeking compliance with tightening carbon regulations.

The Fuel Cell Power Generation Systems market faces challenges related to complex global supply chains and fragmented regulatory standards. Critical components such as membranes, catalysts, and power electronics depend on specialized materials, including platinum group metals, which are subject to price volatility and geopolitical supply risks. Certification and interconnection standards for fuel cell systems vary widely across regions, increasing compliance costs and delaying project execution. Additionally, safety regulations for hydrogen handling differ by jurisdiction, requiring customized system designs and approvals. These challenges increase project risk and extend deployment timelines, particularly for multinational operators seeking standardized energy solutions across multiple markets.

• Accelerated Shift Toward Modular and Prefabricated Fuel Cell Installations: The rise in modular and prefabricated construction is reshaping deployment models within the Fuel Cell Power Generation Systems market. Around 55% of newly announced projects reported measurable cost benefits from modular approaches, including reductions of 20–30% in on-site labor requirements. Factory-assembled, pre-tested fuel cell modules shorten installation timelines by nearly 40% and improve quality consistency. This trend is particularly strong in Europe and North America, where over 60% of commercial and industrial buyers prioritize fast-track construction to minimize operational downtime and project risk.

• Increasing Integration of Fuel Cell Systems with Data Centers and Digital Infrastructure: Fuel cell adoption in data centers is expanding rapidly as operators seek high-reliability, low-emission baseload power. More than 35% of new hyperscale data center projects globally now evaluate fuel cell systems as part of primary or secondary power architecture. These installations achieve uptime levels above 99.99% while reducing on-site carbon emissions by up to 45% compared to diesel-based backup systems. Electrical efficiencies exceeding 55% are supporting continuous operation rather than standby-only use, marking a structural shift in application profiles.

• Advancements in Fuel Flexibility and Hydrogen Blending Capabilities: Technological progress is enabling fuel cell power generation systems to operate on diversified fuel inputs, including natural gas with hydrogen blends of 20–30% by volume. Over 40% of newly deployed stationary systems now feature fuel-flexible designs, reducing dependency on pure hydrogen supply. This capability supports phased decarbonization strategies and allows industrial users to lower direct emissions intensity by approximately 25% without major infrastructure overhauls, improving near-term adoption feasibility.

• Expansion of Long-Duration and High-Capacity Fuel Cell Power Plants: There is a clear trend toward larger-scale fuel cell installations exceeding 10 MW capacity, particularly for grid support and industrial microgrids. Systems in this category have grown by nearly 50% in unit count over the past two years. These plants deliver continuous power for over 8,000 operating hours annually and support grid load balancing with response times under 5 seconds. Utilities and municipalities are increasingly adopting such systems to enhance resilience against outages and extreme weather events.

The Fuel Cell Power Generation Systems market is segmented by type, application, and end-user, reflecting diverse technology maturity levels and deployment priorities across regions. Different fuel cell technologies address varying power capacity, efficiency, and fuel flexibility requirements, while applications range from continuous baseload generation to backup and grid-support functions. End-user adoption is shaped by reliability needs, decarbonization targets, and operational cost optimization. Industrial and commercial segments dominate installations due to high energy intensity and uptime requirements, while utilities and institutional users are expanding deployment for grid resilience and emissions compliance. Segmentation trends indicate a shift toward higher-efficiency systems, multi-megawatt applications, and long-duration operational use, supported by improvements in stack life, modularization, and digital control systems. Together, these segments illustrate a market transitioning from niche deployment toward broader integration across critical energy infrastructures.

The Fuel Cell Power Generation Systems market by type includes Solid Oxide Fuel Cells (SOFC), Proton Exchange Membrane Fuel Cells (PEMFC), Molten Carbonate Fuel Cells (MCFC), Phosphoric Acid Fuel Cells (PAFC), and other niche configurations. SOFC systems currently account for approximately 38% of total adoption due to their high electrical efficiency exceeding 55% and suitability for continuous baseload power in commercial and industrial settings. PEMFC systems represent around 27% of adoption, favored for rapid start-up and lower operating temperatures, particularly in backup and smaller distributed power applications. However, MCFC technology is the fastest-growing segment, expanding at an estimated CAGR of 14.6%, driven by its scalability above 10 MW and compatibility with carbon capture and high-temperature industrial processes. PAFC and other niche fuel cell types collectively contribute about 35% of the remaining market, serving hospitals, universities, and legacy CHP installations.

By application, the Fuel Cell Power Generation Systems market spans prime power generation, combined heat and power (CHP), backup and emergency power, grid support, and microgrid integration. Prime power and CHP applications dominate with nearly 44% share, as these systems deliver continuous electricity with total energy utilization efficiencies above 80% when thermal output is captured. Backup and emergency power applications account for roughly 26%, particularly in data centers and healthcare facilities where uptime requirements exceed 99.9%. Microgrid and grid-support applications are the fastest-growing, expanding at an estimated CAGR of 16.2%, supported by increasing deployment in industrial parks, ports, and remote communities. Other applications, including temporary power and pilot-scale demonstrations, collectively represent about 30% of installations.

End-user segmentation of the Fuel Cell Power Generation Systems market includes industrial facilities, commercial buildings, utilities, data centers, and institutional users such as hospitals and universities. Industrial users lead adoption with approximately 36% share, driven by high energy consumption, continuous operation needs, and pressure to reduce emissions intensity in manufacturing and processing activities. Commercial buildings and campuses follow with about 24% share, leveraging CHP fuel cell systems for energy cost optimization. Utilities represent the fastest-growing end-user segment, with adoption expanding at an estimated CAGR of 17.1% as utilities deploy fuel cells for distributed generation and grid resilience. Data centers and institutional users together contribute nearly 40% of remaining demand, supported by adoption rates exceeding 30% among hyperscale data center operators seeking low-emission baseload power.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 36% between 2026 and 2033.

Asia-Pacific leads due to large-scale deployment of stationary fuel cell systems, exceeding 1.9 GW of installed capacity by 2025, supported by manufacturing ecosystems and hydrogen infrastructure programs. Europe followed with nearly 28% share, driven by industrial decarbonization mandates and over 420 active fuel cell pilot and commercial projects. North America represented approximately 19% of global demand, with strong uptake across data centers and utilities, where fuel cell-powered installations supported more than 8,500 MW of critical backup and prime power capacity. South America and Middle East & Africa together accounted for about 7%, but are witnessing accelerated adoption through energy diversification programs, grid resilience investments, and hydrogen export strategies, with over 120 MW of new projects announced across these regions between 2024 and 2025.

How is enterprise-led clean power adoption reshaping distributed energy systems?

The region accounts for nearly 19% of the global Fuel Cell Power Generation Systems market by deployment volume. Demand is primarily driven by data centers, healthcare facilities, utilities, and financial institutions requiring uptime levels above 99.99%. Government support includes federal clean energy tax credits and state-level hydrogen incentives, contributing to over 650 MW of operational stationary fuel cell capacity. Technological trends emphasize AI-driven energy management, predictive maintenance, and hybrid fuel cell–battery systems. A major local player expanded multi-megawatt fuel cell installations for hyperscale data centers, achieving 40% emissions reduction versus diesel-based systems. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, where fuel cells are increasingly used for both baseload and backup power to mitigate grid volatility.

Why is regulatory alignment accelerating deployment of low-emission power systems?

Europe holds approximately 28% share of the Fuel Cell Power Generation Systems market, with Germany, the UK, and France leading installations. Industrial manufacturing, public infrastructure, and commercial buildings are key demand drivers. Sustainability initiatives under hydrogen strategies and carbon reduction frameworks have supported deployment of more than 900 MW of fuel cell-based power capacity. Adoption of solid oxide and high-temperature fuel cells is increasing due to efficiency levels above 55% and compatibility with industrial heat recovery. A regional manufacturer scaled modular fuel cell CHP units across urban districts, reducing building-level emissions by 35%. Consumer behavior reflects regulatory pressure, leading enterprises to favor transparent, certifiable fuel cell systems aligned with environmental compliance requirements.

What factors are enabling large-scale deployment of advanced power technologies?

Asia-Pacific ranks first globally by volume, accounting for about 46% of total installations. Japan, China, and South Korea dominate consumption, together representing over 1.5 million installed fuel cell units across residential, commercial, and industrial segments. Manufacturing scale, domestic stack production, and hydrogen supply chains are key enablers. Innovation hubs focus on solid oxide fuel cells, modular megawatt platforms, and long-duration systems operating beyond 8,000 hours annually. A leading regional player deployed over 300 MW of fuel cell power plants integrated with smart grids. Consumer behavior emphasizes reliability and long-term operational cost stability, particularly among commercial campuses and industrial parks.

How is energy diversification influencing adoption of alternative power systems?

South America represents close to 4% of global market share, with Brazil and Argentina as primary contributors. Adoption is driven by industrial energy diversification, mining operations, and remote infrastructure projects. Governments have introduced incentives for low-emission power generation, supporting pilot deployments exceeding 60 MW. Infrastructure modernization and off-grid applications are key growth areas. A regional energy company initiated fuel cell-powered microgrids for remote industrial sites, achieving 25% fuel efficiency improvement. Consumer behavior is closely tied to localization needs, with fuel cells increasingly used to support region-specific industrial and municipal energy demands.

Why are hydrogen strategies transforming power generation investments?

Middle East & Africa accounts for roughly 3% of current installations but leads growth momentum. Demand is concentrated in oil & gas facilities, construction projects, and smart city developments, particularly in the UAE and South Africa. Hydrogen export initiatives and energy diversification policies are driving deployment of fuel cell power systems exceeding 90 MW in announced projects. Technological modernization includes integration with renewable hydrogen and digital monitoring platforms. A regional utility launched fuel cell-powered backup systems for critical infrastructure, reducing grid dependency by 30%. Consumer behavior prioritizes resilience and energy security in harsh operating environments.

Japan – 24% market share: Dominates the Fuel Cell Power Generation Systems market due to high production capacity, extensive residential and commercial deployment, and long-term hydrogen investment programs.

Germany – 15% market share: Leads through strong industrial demand, regulatory support for clean power, and advanced deployment of high-efficiency fuel cell CHP systems.

The competitive environment of the Fuel Cell Power Generation Systems market is characterized by a moderately consolidated structure with active participation from both global technology leaders and regionally focused manufacturers. More than 35 commercially active companies operate across system manufacturing, stack development, balance-of-plant integration, and turnkey project delivery. The top five companies collectively account for approximately 62% of total global installations, reflecting strong concentration in large-scale commercial, industrial, and utility-grade deployments, while the remaining share is distributed among mid-sized and niche players serving regional or application-specific needs.

Competition is increasingly shaped by technological differentiation rather than price alone. Key players are prioritizing high-efficiency solid oxide and molten carbonate fuel cell platforms, with system electrical efficiencies surpassing 55% and operational lifetimes extending beyond 80,000 hours. Strategic initiatives include long-term supply agreements with utilities, joint ventures with hydrogen infrastructure providers, and modular product launches targeting the 1–10 MW capacity range, which now represents nearly 48% of new installations. Partnerships focused on hydrogen sourcing, digital energy management, and carbon capture integration have increased by over 30% since 2023. Innovation trends such as AI-based predictive maintenance, fuel-flexible systems supporting 20–30% hydrogen blending, and factory-prefabricated modules are intensifying competition and raising entry barriers for smaller firms.

Bloom Energy

FuelCell Energy

Mitsubishi Power

Doosan Fuel Cell

Ballard Power Systems

Cummins

Toshiba Energy Systems & Solutions

Panasonic Corporation

Plug Power

Nedstack Fuel Cell Technology

Technological advancements are a central force shaping the evolution and competitiveness of the Fuel Cell Power Generation Systems market. Current commercial deployments are dominated by high-efficiency fuel cell platforms capable of delivering continuous power with electrical efficiencies exceeding 55%, while combined heat and power configurations achieve total system efficiencies above 80%. Solid Oxide Fuel Cell (SOFC) technology is increasingly preferred for baseload and industrial applications due to operating temperatures above 700°C, enabling internal fuel reforming and compatibility with natural gas and hydrogen blends of up to 30%. Proton Exchange Membrane Fuel Cells (PEMFC) continue to advance in durability, with average stack lifetimes extending beyond 60,000 operating hours, supporting critical backup and fast-response applications.

Emerging technologies are focused on scalability, fuel flexibility, and digital optimization. Modular system architectures now allow standardized 250 kW to 1 MW units to be aggregated into multi-megawatt installations exceeding 20 MW, reducing engineering complexity and shortening deployment timelines by nearly 40%. Advances in power electronics and thermal management have improved load-following response times to under 5 seconds, enhancing grid-support capabilities. Digital technologies, including AI-driven predictive maintenance and digital twin modeling, are reducing unplanned downtime by approximately 25% and lowering maintenance intervention frequency by over 20%.

Hydrogen-ready designs and integration with carbon capture systems are gaining traction, particularly for industrial users aiming to reduce emissions intensity. Innovations in catalyst utilization have lowered precious metal content by nearly 35%, mitigating supply risk and improving system cost stability. Together, these technology developments are strengthening system reliability, expanding application scope, and positioning fuel cell power generation systems as a core component of future resilient and low-emission energy infrastructures.

• In November 2024, Bloom Energy announced the world’s largest single-site fuel cell installation — an 80 MW solid oxide fuel cell (SOFC) project in North Chungcheong Province, South Korea, to power two eco parks, scheduled for commercial operations in 2025, highlighting scalability in industrial-scale deployments. (Bloom Energy)

• In July 2024, Yanmar Energy Systems commercialized the HP35FA1Z hydrogen fuel cell power generation system, a 35 kW compact, multi-unit controllable PEM fuel cell for commercial power supply in Japan, featuring integrated control of up to 16 units and zero greenhouse gas emissions during operation. (YANMAR)

• In early 2025, FuelCell Energy expanded service operations and project backlogs with a 20-year power purchase agreement for a 7.4 MW carbonate fuel cell power plant in Hartford, Connecticut, and recognized increased long-term service revenues tied to a 58.8 MW platform in Korea, underscoring growth in utility and industrial markets. (investor.fce.com)

• In 2025, Yanmar Power Technology secured Approval in Principle (AiP) from DNV for its GH320FC maritime hydrogen fuel cell system, positioning fuel cell systems for maritime power generation and broader industrial applications beyond stationary land-based generation. (Mynewsdesk)

The Fuel Cell Power Generation Systems Market Report provides a comprehensive assessment of technology types, applications, geographic regions, and strategic industry segments shaping this energy sector’s evolution. The report covers all major fuel cell technologies deployed in stationary power generation, including proton exchange membrane fuel cells (PEMFC), solid oxide fuel cells (SOFC), molten carbonate fuel cells (MCFC), and phosphoric acid fuel cells (PAFC), with detailed analysis of capacity ranges from sub-kilowatt systems to multi-megawatt installations. It examines applications such as prime power generation, combined heat and power (CHP), grid support and microgrid integration, and backup/emergency power across commercial, industrial, utility, and institutional environments.

Geographically, the report analyzes region-wise dynamics across Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, highlighting regional infrastructure readiness, regulatory frameworks, and deployment volumes. Particular focus is given to top consuming countries and emerging markets within each region. The scope also includes segmentation by end-users, illustrating utility, data center, industrial, and commercial adoption patterns with quantitative insights into penetration rates, technology preferences, and system capacities installed.

In addition to traditional analysis, the report explores emerging market niches such as marine power generation, hydrogen integration, hybrid systems with storage, and digital optimization trends. It incorporates innovation metrics, comparative technology performance data, and strategic initiatives influencing procurement and deployment decisions. Designed for energy sector decision-makers, investors, and technology developers, the report delivers deep visibility into market segmentation, technology trends, and strategic opportunities shaping the future of fuel cell power generation systems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

34.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bloom Energy, FuelCell Energy, Mitsubishi Power, Doosan Fuel Cell, Ballard Power Systems, Cummins, Toshiba Energy Systems & Solutions, Panasonic Corporation, Plug Power, Nedstack Fuel Cell Technology |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |