Reports

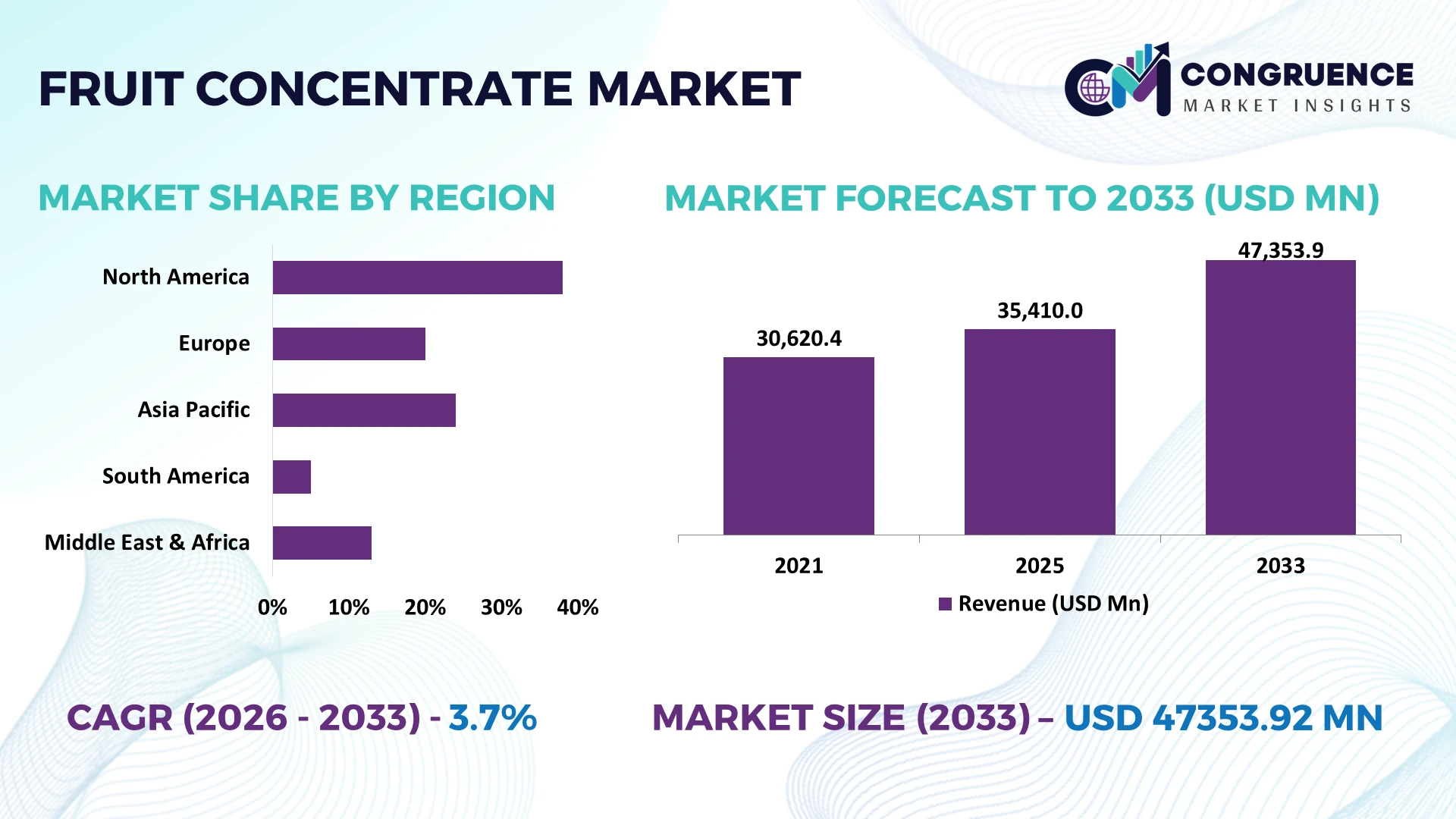

The Global Fruit Concentrate Market was valued at USD 35410 Million in 2025 and is anticipated to reach a value of USD 47353.92 Million by 2033 expanding at a CAGR of 3.7% between 2026 and 2033. Growth is being driven by advanced concentration technologies, expanding clean-label beverage manufacturing, rising fruit processing efficiency, and stronger utilization of concentrate ingredients across food, dairy, and nutrition applications.

China remains the dominant country, accounting for approximately 24% of global fruit concentrate processing capacity, supported by large-scale apple production, automated processing facilities, and continued investment in food manufacturing. Compared with Brazil, which leads citrus concentrate exports, China records over 85% automation across major processing plants, while regional supply diversification has accelerated following Red Sea shipping disruptions in 2026, strengthening resilient sourcing strategies.

Manufacturers are prioritizing geographically diversified processing networks and technology-led production to secure supply continuity, optimize margins, and strengthen long-term competitive positioning.

Market Size & Growth: USD 35410 Million (2025) to USD 47353.92 Million (2033) at 3.7% CAGR, supported by advanced processing technology and efficient fruit utilization.

Top Growth Drivers: Automation adoption exceeds 35%, premium beverage demand grows 18%, and processing yield improves 12% through advanced concentration systems.

Short-Term Forecast: By 2028, production efficiency increases 15% while processing waste declines 10% through digital manufacturing optimization.

Emerging Technologies: AI-enabled quality inspection, membrane filtration, and automated evaporation systems improve consistency and reduce energy consumption by 14%.

Regional Leaders: Asia Pacific reaches approximately USD 18.5 Billion, Europe USD 11.2 Billion, and North America USD 9.4 Billion, driven by expanding food processing and regional supply-chain localization.

Consumer/End-User Trends: More than 62% of beverage manufacturers increase usage of natural fruit concentrates to support clean-label product portfolios.

Pilot/Case Example: In 2026, an automated fruit processing project improved concentrate recovery by 11% while reducing production downtime by 9%.

Competitive Landscape: The leading supplier holds approximately 9% global share, with major competition from Döhler, Ingredion, SVZ, AGRANA, and Kanegrade.

Regulatory & ESG Impact: Water recycling and energy-efficiency initiatives reduce processing water consumption by nearly 20%, supporting stricter environmental compliance.

Investment & Funding: More than USD 1.3 Billion supports capacity expansion, automation, and regional processing facilities amid global supply-chain diversification.

Innovation & Future Outlook: High-Brix concentrates, precision processing, and AI-driven quality control accelerate next-generation manufacturing and strengthen long-term sourcing resilience.

Fruit concentrate manufacturers are expanding applications across beverages, dairy, bakery, confectionery, and nutritional products through improved flavor retention and higher ingredient functionality. Advanced membrane filtration and low-temperature concentration technologies enhance product quality while reducing energy intensity by approximately 15%. Regional processing expansion and diversified sourcing strategies continue strengthening operational resilience, creating a solid foundation for the strategic market assessment that follows.

The Fruit Concentrate Market has become strategically important as food and beverage manufacturers strengthen ingredient security, reduce formulation complexity, and expand clean-label product portfolios. Supply-chain restructuring following logistics disruptions has accelerated localized processing investments and diversified sourcing strategies. Enterprises are integrating digital quality monitoring and precision concentration systems to improve consistency while lowering operational exposure to raw material variability.

Modern membrane concentration technology delivers approximately 18% lower energy consumption and improves flavor retention by nearly 15% compared with conventional thermal evaporation, making it a preferred choice for premium applications. China continues to lead large-scale processing capacity, while Germany emphasizes high-value specialty concentrates supported by advanced automation and stringent quality standards. Over the next two to three years, digital production monitoring is expected to exceed 50% adoption across large processing facilities, enabling faster traceability and more stable production performance.

A leading deployment trend involves beverage manufacturers partnering with fruit processors to establish integrated sourcing and processing networks that reduce procurement lead times by nearly 20%. Companies are expanding regional processing facilities, investing in automated concentration technologies, and strengthening supplier partnerships to secure year-round raw material availability. Organizations that combine operational resilience with technology-led processing efficiency will strengthen competitive positioning and sustain long-term market relevance.

Advanced processing automation and premium ingredient demand are reshaping the competitive landscape of the fruit concentrate industry. Automated sorting, optical inspection, and precision evaporation systems improve production throughput by nearly 22% while reducing raw material losses by approximately 14%. In China, continued investment in integrated food processing clusters strengthens year-round manufacturing efficiency despite seasonal harvest cycles. The shift toward clean-label beverages and natural sweetening ingredients is encouraging processors to expand production capacity and establish long-term sourcing partnerships with growers. Companies are responding through automation investments, vertically integrated supply networks, and technology collaborations that improve product consistency, strengthen supply reliability, and enhance profitability across industrial-scale operations.

Seasonal fruit availability, climate variability, and fluctuating agricultural input costs continue to constrain operational planning. Fruit procurement prices in some producing regions have experienced fluctuations exceeding 20%, while energy-intensive concentration processes account for nearly 30% of total manufacturing costs. Weather-related disruptions in major producing countries such as Brazil periodically reduce citrus harvest quality, increasing procurement uncertainty for processors. Companies are mitigating these pressures through diversified sourcing across multiple countries, contract farming arrangements, and localized processing facilities positioned closer to production zones. Strategic procurement flexibility has become a critical differentiator for maintaining stable margins and uninterrupted manufacturing operations.

Growing demand for functional beverages and nutrition-focused foods is creating new opportunities for premium fruit concentrate applications. AI-enabled process optimization can improve production efficiency by approximately 16%, while advanced filtration technologies reduce water consumption by nearly 12%. India is expanding modern fruit processing infrastructure through public and private investments, supporting higher-value exports and domestic manufacturing. Companies are increasing R&D spending on low-sugar concentrates, customized fruit blends, and ingredient traceability platforms while forming partnerships with beverage and dairy producers. The combination of digital manufacturing and value-added formulation capabilities creates differentiated product portfolios with stronger pricing power and broader commercial reach.

Maintaining uniform quality across geographically dispersed processing facilities remains a significant execution challenge. Variations in fruit characteristics can reduce production consistency by nearly 10%, while quality assurance activities account for approximately 8% of operational processing time. Increasing food traceability requirements and stricter export compliance standards place additional pressure on manufacturers operating across multiple sourcing countries. Companies must integrate standardized digital quality management systems, workforce training, and real-time production analytics to ensure consistent output. Long-term competitiveness will depend on building resilient processing infrastructure capable of balancing quality, operational efficiency, regulatory compliance, and sustainable manufacturing performance across global supply networks.

Advanced Low-Temperature Processing Low-temperature concentration systems are replacing conventional thermal methods, improving flavor retention by approximately 18% while reducing energy consumption by nearly 15%. Following tighter sustainability targets across Europe, processors are upgrading evaporation lines and integrating automated process controls. Equipment suppliers are expanding technology partnerships, enabling faster production cycles, lower operating costs, and improved consistency for premium beverage and food manufacturers.

Regional Processing Network Expansion Companies are restructuring procurement by establishing processing facilities closer to fruit-growing regions, reducing transportation costs by around 12% and shortening procurement lead times by nearly 20%. Supply-chain disruptions during recent global shipping constraints accelerated localization strategies in China and Brazil. Manufacturers are expanding regional partnerships with growers and contract processors to improve raw material availability and reduce seasonal sourcing risks.

Digital Quality Traceability Systems AI-powered inspection platforms and digital traceability solutions now support more than 45% of large processing facilities, reducing quality inspection time by approximately 25% and improving batch consistency by nearly 14%. Food safety compliance requirements are driving rapid digital deployment. Leading processors are integrating cloud-based production monitoring with supplier data, strengthening export readiness and minimizing product recalls across multinational supply networks.

Functional Ingredient Portfolio Diversification Demand for customized fruit concentrate blends has increased by approximately 17%, while low-sugar formulations account for nearly 28% of new product development projects. Beverage and dairy manufacturers are reformulating products to meet evolving nutrition preferences. Companies are expanding formulation capabilities through application laboratories, strategic ingredient partnerships, and specialized concentrate portfolios that deliver differentiated functionality without increasing formulation complexity.

Apple Concentrate remains the leading product category, representing approximately 38% of global demand due to abundant raw material availability, high processing efficiency, long storage stability, and extensive use across beverages, bakery products, and food processing applications. Its cost-effective production and year-round availability make it the preferred choice for industrial manufacturers. Orange Concentrate continues to hold a strong position through juice applications, while Grape Concentrate supports natural sweetening and color enhancement across processed foods. Companies are expanding automated processing capacity and investing in higher-yield extraction technologies, improving production efficiency by nearly 15%.

Mango Concentrate is emerging as the fastest-growing segment, supported by increasing demand for tropical flavors and premium beverage formulations, with adoption expanding by approximately 16% across value-added food products. Berry Concentrate is gaining importance within functional beverages because of its naturally high antioxidant profile and premium positioning. Manufacturers are introducing customized concentrate blends, strengthening sourcing partnerships, and expanding specialty processing facilities to capture higher-margin opportunities while balancing mature and emerging product portfolios.

Beverages remain the largest application, accounting for approximately 52% of concentrate utilization due to extensive demand from juice, flavored water, energy drink, and functional beverage manufacturers. High production volumes, standardized formulations, and efficient ingredient handling continue supporting this segment's dominance. Dairy Products represent the fastest-growing application as fruit-based yogurt, cultured beverages, and protein drinks increasingly incorporate natural concentrates. Processing efficiency has improved by nearly 14%, while automated ingredient dosing has reduced formulation variability by approximately 10%.

Bakery & Confectionery applications continue expanding through fruit fillings, glazes, and natural flavoring systems, whereas Infant Nutrition increasingly adopts premium concentrates with enhanced quality assurance standards. Sauces & Dressings benefit from concentrated fruit ingredients that improve flavor consistency and shelf stability. Companies are expanding application laboratories, optimizing formulation support, and strengthening partnerships with food manufacturers to develop customized ingredient systems that improve operational flexibility and product differentiation.

Beverage Manufacturers represent the largest end-user group, accounting for approximately 47% of global concentrate procurement because of continuous high-volume production, diversified product portfolios, and extensive processing infrastructure. Their purchasing strategies increasingly prioritize standardized quality, reliable year-round supply, and traceable sourcing networks. Food Processing Companies remain significant buyers across confectionery, prepared foods, and ingredient manufacturing, while Dairy Producers are the fastest-growing customer group with concentrate utilization increasing by approximately 15% as value-added dairy formulations continue expanding.

Bakery Manufacturers increasingly integrate fruit concentrates into fillings, toppings, and flavor systems, while the Foodservice Industry expands demand through beverage customization and premium menu innovation. Companies are responding with customized concentrate specifications, flexible contract models, and integrated technical support services. Supplier partnerships, localized inventories, and application-focused product development are becoming central competitive strategies as procurement shifts toward long-term operational reliability rather than price-focused purchasing.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, South America is expected to register the fastest growth, expanding at a 4.5% CAGR between 2026 and 2033.

Advanced Processing and Premium Ingredient Integration

North America maintains a strong position through highly automated food processing infrastructure and widespread adoption of premium fruit-based ingredients across beverages, dairy products, and bakery applications. The region contributes approximately 24% of global fruit concentrate consumption, supported by vertically integrated supply chains and sophisticated cold storage networks. Digital quality management systems are deployed across more than 55% of large processing facilities, improving production consistency and reducing quality deviations. Companies continue investing in localized sourcing partnerships with growers while expanding aseptic processing capabilities to improve supply resilience. Increasing demand for clean-label formulations and functional beverages is encouraging manufacturers to modernize processing lines, strengthen traceability systems, and improve operational efficiency through automation.

United States Market Outlook: The United States remains the largest market in North America due to its extensive beverage manufacturing base, advanced food processing infrastructure, and continuous product innovation. More than 60% of commercial beverage manufacturers have integrated automated ingredient management systems to improve formulation precision and production efficiency. Companies continue expanding partnerships with domestic fruit growers while investing in modern concentration technologies that support higher throughput, enhanced quality assurance, and improved inventory management across large-scale manufacturing operations.

Sustainability-Led Manufacturing Modernization

Europe represents a mature market characterized by advanced processing technologies, strict food quality standards, and sustainability-focused manufacturing practices. The region accounts for approximately 27% of global consumption, supported by specialized ingredient manufacturers and premium beverage producers. Energy-efficient concentration equipment has reduced processing energy requirements by nearly 16% across newly modernized facilities. Circular manufacturing initiatives and water recycling investments continue reshaping industrial operations as processors respond to evolving environmental compliance requirements. Companies are prioritizing traceable sourcing, premium concentrate development, and technology upgrades to improve production efficiency while strengthening export competitiveness.

Germany Market Outlook: Germany serves as Europe's strategic processing and innovation hub with highly automated food manufacturing facilities and advanced quality control systems. More than 50% of large processing plants have implemented AI-assisted inspection technologies to improve batch consistency and regulatory compliance. German enterprises continue expanding research partnerships focused on premium fruit ingredients, sustainable production processes, and specialized concentrate formulations that support high-value food and beverage manufacturing.

Large-Scale Manufacturing and Export Leadership

Asia-Pacific leads the global market through extensive fruit production, large-scale processing infrastructure, and expanding domestic food manufacturing capacity. The region contributes approximately 42% of global processing activity, supported by integrated industrial clusters and competitive production costs. Automated concentration systems are installed across nearly 48% of newly commissioned processing facilities, increasing production efficiency and improving export quality. Rising investments in cold-chain logistics and processing modernization continue strengthening operational resilience. Companies are expanding manufacturing capacity, improving digital quality monitoring, and building long-term sourcing partnerships to support growing domestic consumption and international demand.

China Market Outlook: China remains the region's dominant market through its extensive apple processing industry, integrated manufacturing ecosystem, and advanced food processing infrastructure. Approximately 24% of global fruit concentrate processing capacity is located within the country, supported by continuous investment in automated production facilities. Chinese manufacturers continue strengthening export capabilities, deploying intelligent manufacturing technologies, and expanding integrated supply chains that improve production efficiency and year-round raw material availability.

Export-Oriented Processing Expansion

South America plays a critical role in global fruit concentrate supply through abundant agricultural resources and export-focused processing industries. The region contributes approximately 16% of global production, with citrus and tropical fruit concentrates forming the core industrial output. Investments in processing modernization have improved operational efficiency by nearly 13%, although logistics infrastructure and seasonal weather variability continue influencing supply stability. Companies are expanding processing facilities closer to cultivation areas, improving storage capacity, and strengthening grower partnerships to enhance production continuity while supporting international demand.

Brazil Market Outlook: Brazil remains the region's largest market through its globally significant citrus processing industry and well-established export infrastructure. Modern processing facilities continue expanding automated production capacity while strengthening quality assurance systems for international markets. More than 70% of large citrus processors have adopted advanced sorting and grading technologies, improving export consistency and operational efficiency while reinforcing the country's leadership in fruit concentrate manufacturing.

Investment-Led Food Processing Transformation

The Middle East & Africa market is expanding through investments in food manufacturing, cold-chain infrastructure, and import substitution strategies. The region represents approximately 8% of global demand, supported by increasing beverage production and growing processed food industries. Modern warehouse and refrigerated logistics capacity has expanded by nearly 18% across key industrial hubs, improving ingredient availability and reducing distribution inefficiencies. Manufacturers are strengthening regional partnerships, upgrading processing facilities, and investing in modern packaging technologies to improve operational performance while supporting evolving food security initiatives.

Saudi Arabia Market Outlook: Saudi Arabia has emerged as the region's strategic investment center due to expanding food manufacturing capacity, industrial diversification policies, and advanced logistics infrastructure. Food processing enterprises continue increasing automation across production facilities, with automated packaging adoption exceeding 40% among large manufacturers. Ongoing investments in integrated food industrial zones and modern cold-chain systems are strengthening domestic processing capabilities while supporting long-term supply resilience and regional distribution efficiency.

Global ingredient specialists including Döhler, SVZ, AGRANA, Ingredion, and Kanegrade compete directly with regional fruit processors and export-focused manufacturers for long-term supply contracts and premium formulation projects. The top five players collectively control approximately 34% of the market, creating a moderately consolidated competitive structure. Competition centers on processing technology, sourcing reliability, customization, and supply-chain responsiveness rather than price alone. Automated concentration systems improve processing efficiency by nearly 18%, while vertically integrated sourcing lowers procurement costs by around 12% and reduces delivery lead times by approximately 20%. Companies are expanding processing facilities, forming grower partnerships, investing in AI-enabled quality control, and strengthening regional manufacturing networks to secure raw material availability. The competitive landscape is shifting toward supply-chain control and value-added ingredient portfolios, making technology-enabled differentiation increasingly important. High capital requirements, stringent food safety compliance, and dependable fruit sourcing create significant entry barriers. Winning requires resilient procurement networks, advanced processing capabilities, consistent product quality, and customer-specific formulation expertise.

Döhler GmbH

SVZ International B.V.

AGRANA Beteiligungs-AG

Ingredion Incorporated

Kanegrade Ltd.

Diana Food

Tree Top Inc.

Louis Dreyfus Company

China Haisheng Juice Holdings Co., Ltd.

Lemon Concentrate S.L.

Rudolf Wild GmbH & Co. KG

Kiril Mischeff Group

SunOpta Inc.

Ciatti Company

Modern fruit concentrate production is transitioning from conventional thermal evaporation toward membrane filtration, AI-enabled process control, and automated quality inspection. Membrane concentration reduces energy consumption by approximately 18% while improving flavor retention by nearly 15% compared with legacy evaporation systems. Around 48% of newly upgraded processing facilities now deploy digital production monitoring, enabling continuous quality optimization, lower waste generation, and improved batch traceability across high-volume manufacturing operations.

Emerging technologies focus on intelligent automation, optical fruit sorting, and cloud-connected manufacturing execution systems. AI-powered inspection reduces quality assessment time by approximately 25%, while automated process optimization improves production throughput by nearly 16%. Large multinational ingredient suppliers benefit most because integrated digital platforms strengthen procurement planning, inventory control, and regulatory compliance while enabling faster customer response and greater operational consistency than traditional processing environments.

Between 2026 and 2028, predictive maintenance, digital twin production modeling, and advanced enzyme-assisted extraction are expected to become standard investments across large commercial processing plants. These technologies reduce equipment downtime, optimize raw material utilization, and strengthen manufacturing resilience against seasonal supply variability. Companies investing early in intelligent processing infrastructure, integrated traceability, and automated production ecosystems will secure stronger operational advantages, improve customer retention, and establish sustainable competitive differentiation as premium ingredient requirements continue becoming more demanding.

March 2025 Döhler acquired Premier Juices in North America, expanding its fruit solutions portfolio with citrus and tropical fruit concentrates while strengthening regional customer support and supply capabilities. The acquisition broadened access to more than 10 fruit categories, improving portfolio depth and market responsiveness. Source: doehler.com

September 2025 SVZ announced the full integration of Netra Agro into its core business, consolidating nearly 30 years of tropical fruit ingredient expertise ahead of the Q1 2026 transition. The move unified operations under one portfolio, improving product availability and global customer service continuity. Source: svz.com

May 2026 AGRANA reported continued investment across its Fruit and Beverage Solutions operations, allocating €64 million toward production capacity expansion, energy-efficiency upgrades, safety improvements, and new packaging infrastructure across 36 production sites, strengthening manufacturing resilience and operational productivity. Source: agrana.com

June 2026 SVZ highlighted that European spring weather was reshaping fruit harvest conditions, prompting processors to optimize sourcing strategies and production planning. The operational update emphasized proactive supply-chain adjustments to maintain ingredient availability and processing continuity throughout the 2026 harvest season. Source: svz News & Blog

The report provides a comprehensive assessment of the global Fruit Concentrate Market across Apple Concentrate, Orange Concentrate, Grape Concentrate, Mango Concentrate, and Berry Concentrate, evaluating their operational positioning, commercial adoption, and evolving product strategies. It analyzes applications spanning beverages, dairy products, bakery & confectionery, infant nutrition, and sauces & dressings, together with demand patterns across beverage manufacturers, food processing companies, dairy producers, bakery manufacturers, and the foodservice industry. More than 10 leading market participants and key technology developments are evaluated to identify competitive positioning and operational differentiation.

The study delivers detailed regional insights covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining processing modernization, digital manufacturing, automation, traceability, and sustainable production technologies. It highlights deployment trends, enterprise investment priorities, supply-chain restructuring, and evolving sourcing strategies to support expansion planning, competitive benchmarking, portfolio optimization, partnership evaluation, and long-term strategic decision-making between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 35410 Million |

Market Revenue in 2033 | USD 47353.92 Million |

CAGR (2026 - 2033) | 3.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Döhler GmbH, SVZ International B.V., AGRANA Beteiligungs-AG, Ingredion Incorporated, Kanegrade Ltd., Diana Food, Tree Top Inc., Louis Dreyfus Company, China Haisheng Juice Holdings Co., Ltd., Lemon Concentrate S.L., Rudolf Wild GmbH & Co. KG, Kiril Mischeff Group, SunOpta Inc., Ciatti Company |

Customization & Pricing | Available on Request (10% Customization is Free) |