Reports

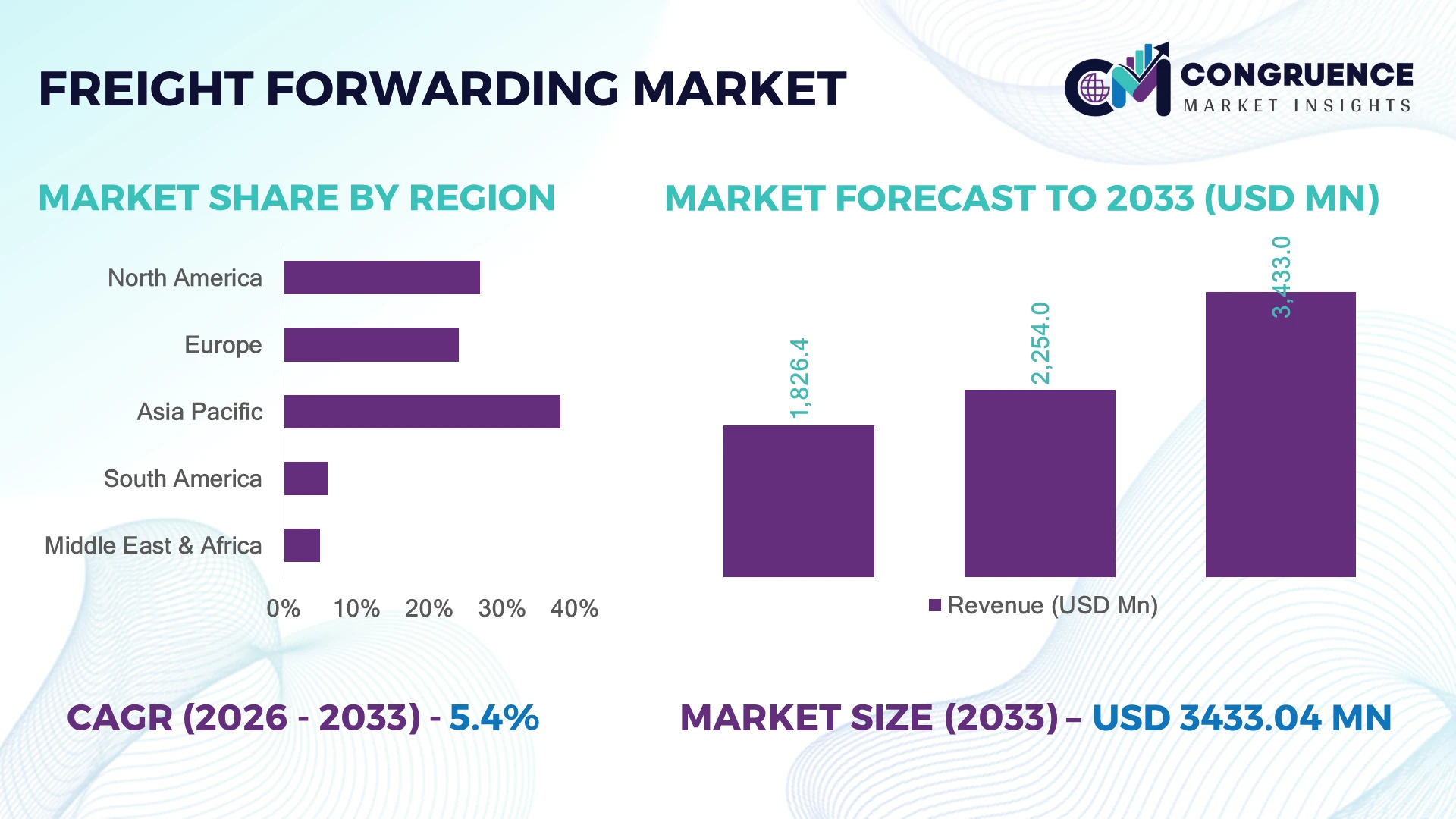

The Global Freight Forwarding Market was valued at USD 2,254.0 Million in 2025 and is anticipated to reach a value of USD 3,433.0 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. Expansion of cross-border e-commerce volumes and digitized multimodal logistics platforms is accelerating global freight forwarding efficiency across air, sea, and road corridors.

China leads with ~30% share of global forwarding capacity driven by USD 1.2 trillion export throughput, while the United States holds ~22% with high-value tech and automotive shipments, and Germany contributes ~18% through EU-integrated logistics networks. India is rapidly scaling with over 12% YoY increase in digital freight adoption and port modernization investments exceeding USD 80 billion. Compared to the U.S., China processes nearly 1.4x higher container volume efficiency, while Europe shows stronger ESG-compliant routing adoption at ~27%. Geopolitical disruptions in the Red Sea corridor have rerouted ~15% of Asia–Europe cargo flows, increasing reliance on digital freight optimization systems.

Strategically, this shift strengthens data-driven routing and regional diversification as core competitive levers for global logistics players.

Market Size & Growth: USD 2,254.0M → USD 3,433.0M with 5.4% CAGR driven by digital freight platforms

Top Growth Drivers: 42% e-commerce, 28% manufacturing trade, 18% cross-border logistics expansion

Short-Term Forecast: By 2028, shipment visibility efficiency improves by 35% via automation

Emerging Technologies: AI routing, blockchain documentation, IoT-enabled tracking increasing operational accuracy by 30%

Regional Leaders: Asia-Pacific USD 1,020M, North America USD 780M, Europe USD 690M with AI-led logistics adoption rising 25%

Consumer/End-User Trends: 58% enterprises shifting to integrated forwarding platforms for cost reduction

Pilot/Case Example: 2025 EU digital freight pilot reduced customs clearance time by 41%

Competitive Landscape: DHL holds ~12% share; Kuehne+Nagel, DSV, DB Schenker expanding digital fleets

Regulatory & ESG Impact: 22% emissions reduction targets driving modal shift to sea freight

Investment & Funding: USD 18B invested in logistics tech and port automation upgrades globally

Innovation & Future Outlook: Autonomous freight orchestration and predictive analytics boosting efficiency by 33%

Freight forwarding demand is rapidly strengthening across manufacturing-heavy corridors, with 64% of shipments now requiring end-to-end digital tracking. AI-based customs automation improves clearance speed by 38%, while blockchain documentation reduces disputes in cross-border trade. Southeast Asia shows 19% faster adoption of smart logistics platforms compared to traditional EU systems. The trend reflects tightening supply-chain compliance and rising demand for real-time visibility in global trade flows.

The freight forwarding market has become a strategic control layer for global trade efficiency, as companies compete on visibility, speed, and cost optimization rather than just transportation scale. Supply-chain fragmentation driven by geopolitical tensions and trade route disruptions has accelerated investment in digital freight ecosystems and diversified routing strategies.

AI-enabled forwarding systems reduce operational planning time by nearly 40% compared to legacy manual coordination tools, while integrated cloud logistics platforms improve shipment traceability accuracy by over 35%. North America leads in platform standardization, whereas Asia-Pacific dominates in volume-driven automation adoption, deploying smart port systems at 1.5x faster rate than Europe.

In operational practice, logistics providers are expanding partnerships with digital freight aggregators and investing in multimodal infrastructure hubs to reduce transit delays by 20–25% within the next 2–3 years. Firms are also reallocating capital toward predictive analytics and ESG-compliant routing networks to meet tightening emission constraints. Strategically, competitive advantage is shifting toward firms that can integrate real-time intelligence, resilient routing, and scalable digital infrastructure across global trade lanes.

Digitalization of freight documentation and multimodal orchestration is the primary growth engine, with over 46% of global shipments now processed through integrated forwarding platforms. The U.S. has reduced customs processing time by 32% through automated compliance systems, while China’s port digitization programs have improved container turnaround efficiency by 28%. Cross-border e-commerce expansion across India and Vietnam is further increasing air–sea hybrid logistics demand by 19%. The Russia–Ukraine disruption and Red Sea route instability have accelerated rerouting decisions, pushing enterprises toward AI-based route optimization. In response, firms such as DHL and Kuehne+Nagel are expanding digital freight corridors, investing in predictive logistics platforms and strategic hub partnerships to enhance resilience and reduce transit uncertainty.

Persistent port congestion, uneven infrastructure modernization, and fuel cost volatility continue to restrict operational scalability, with global freight cost fluctuations impacting margins by 14–18%. Latin American ports report average dwell time delays rising by 22%, while Southeast Asian inland logistics gaps account for nearly 25% inefficiency in multimodal transfers. Regulatory fragmentation across customs regimes adds compliance overhead of around 12% for cross-border operators. The ongoing variability in ocean freight rates, influenced by geopolitical disruptions in key corridors, further constrains long-term contracting stability. Companies are mitigating risks through multi-carrier diversification, long-term capacity agreements, and regional warehousing expansion in Mexico and Poland, enabling partial insulation from global routing shocks.

AI-powered freight orchestration and predictive logistics platforms present major expansion opportunities, with smart freight adoption growing 38% in digitally advanced markets like Germany and Singapore. India’s logistics tech ecosystem is attracting over 21% of new supply-chain startup investments focused on automation and visibility tools. Blockchain-based documentation is reducing settlement disputes by 30%, particularly in EU–Asia trade lanes. Emerging carbon-tracking mandates in Canada and France are accelerating demand for ESG-compliant freight optimization solutions. Companies are expanding through strategic acquisitions of digital freight startups and investing in platform interoperability to capture fragmented SME logistics demand, which still represents over 40% of global forwarding volume.

Integration complexity across legacy systems and modern digital freight platforms remains a critical barrier, with nearly 35% of global logistics firms reporting interoperability inefficiencies. Cybersecurity incidents targeting supply-chain platforms have increased by 27%, particularly in high-volume hubs such as Rotterdam and Los Angeles. The challenge intensifies as freight ecosystems expand across cloud-based APIs and third-party logistics providers, increasing exposure points. Workforce digital skill gaps further slow adoption, with only 52% of logistics operators in emerging economies trained in advanced freight analytics systems. Companies are responding by investing in unified logistics architecture, zero-trust cybersecurity frameworks, and global training programs, aiming to stabilize operational continuity and ensure scalable deployment across increasingly digitized freight networks.

AI-driven routing optimization scaling globally Real-time AI freight orchestration is now used in 44% of long-haul shipments, improving route efficiency by 31% and reducing idle container time by 18%. The U.S. and Netherlands are leading deployment through port-level automation hubs, while Singapore integrates predictive congestion mapping across 70% of container flows. Regulatory pressure on carbon reporting in the EU is accelerating adoption of algorithmic route balancing. Companies are responding by embedding AI engines into TMS platforms and forming partnerships with cloud logistics providers to reduce delivery variability and improve asset utilization.

Blockchain documentation replacing manual clearance workflows Digital bill-of-lading systems are now adopted in 36% of cross-border shipments, cutting documentation errors by 42% and reducing customs disputes by 25%. China and Germany are at the forefront of deployment, driven by export-heavy manufacturing ecosystems. A non-obvious shift is the integration of blockchain with customs AI engines, enabling automated compliance validation. Firms are scaling digital trade corridors and partnering with customs authorities to reduce clearance delays and improve trade transparency across high-volume lanes.

Multimodal freight consolidation accelerating efficiency Hybrid air–sea–rail logistics usage has increased by 29%, particularly across India–Middle East and EU–Asia corridors, reducing end-to-end transit costs by 16%. Port congestion in Los Angeles and Rotterdam has pushed 21% of shipments toward inland rail-linked hubs. Enterprises are restructuring supply chains around multimodal nodes to improve resilience against geopolitical disruptions. Logistics providers are investing in integrated terminal networks and cross-border warehousing to optimize cargo flow consistency and reduce bottlenecks.

ESG-compliant freight restructuring intensifying Around 33% of global freight contracts now include carbon reporting clauses, while sustainable fuel adoption in ocean freight has improved emission efficiency by 22%. France and Canada are enforcing stricter logistics decarbonization policies, influencing carrier selection across EU–North America lanes. Companies are responding by adopting carbon tracking APIs and redesigning fleet allocation strategies. A key insight is that ESG compliance is increasingly becoming a tender-winning factor rather than just a reporting requirement.

Air freight forwarding remains the leading type due to its dominance in high-value, time-sensitive shipments, accounting for nearly 38% of express global trade flows. Its scalability across pharmaceutical, electronics, and e-commerce sectors drives strong adoption, particularly in the U.S., China, and Germany where over 55% of premium cargo relies on air logistics integration. Sea freight continues to hold cost advantages for bulk shipments, while road and rail segments expand through regional trade agreements and inland connectivity improvements. Air freight is also the fastest-growing type in digitalized logistics networks, supported by 26% growth in automated cargo tracking and 19% increase in AI-based capacity planning tools. Sea freight is modernizing through smart containerization, while rail freight is gaining traction in Eurasian corridors with 14% higher utilization efficiency. Companies are investing in multimodal integration platforms and expanding air cargo partnerships with carriers to improve reliability and reduce delivery volatility across global trade lanes.

Manufacturing logistics remains the leading application, accounting for nearly 41% of global forwarding demand due to complex supply-chain dependencies across automotive, electronics, and industrial machinery sectors. E-commerce is the fastest-growing application, with 34% shipment growth in cross-border parcels driven by rising consumer demand in India, Southeast Asia, and the U.S. Retail logistics follows closely, while healthcare shipments are expanding due to temperature-sensitive pharmaceutical exports. E-commerce shipments increasingly rely on express air–road hybrid models, improving delivery speed by 28% and reducing last-mile inefficiencies by 17%. Manufacturing supply chains are adopting predictive freight scheduling tools to stabilize production cycles and reduce downtime risks. Companies are expanding fulfillment center networks and integrating API-based logistics systems to enhance shipment visibility and operational synchronization across global markets.

Large enterprises remain the dominant end-user group, contributing nearly 52% of total freight forwarding demand due to high-volume global supply-chain operations across manufacturing, retail, and automotive sectors. SMEs represent the fastest-growing segment, expanding adoption by 27% as digital freight platforms lower entry barriers and improve pricing transparency. Government and defense logistics also maintain steady demand through regulated and secure cargo flows. Large enterprises prioritize integrated logistics ecosystems and long-term carrier contracts to stabilize cost volatility, while SMEs increasingly rely on on-demand digital freight marketplaces. Adoption of cloud-based logistics management systems has increased by 31%, improving shipment tracking accuracy and operational coordination. Companies are targeting SMEs through flexible pricing models and API-driven logistics platforms, while strengthening enterprise partnerships to secure long-term volume commitments.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America contributes nearly 27% of global freight forwarding activity, driven by advanced automation in U.S. ports and strong demand from automotive, aerospace, and semiconductor supply chains. Around 62% of freight operators in the region now use AI-based shipment tracking, improving delivery predictability by 29%. Canada’s rail-integrated logistics corridors are expanding cross-border efficiency with the U.S. by 18%. The region is also witnessing increased investment in nearshoring logistics hubs across Mexico to reduce Asia dependency. Companies are expanding digital freight platforms and forming carrier-tech partnerships to improve resilience against port congestion and geopolitical disruptions.

United States Market Outlook: The U.S. remains the dominant logistics hub with over 70% of North American freight volume processed through its coastal ports. Automation at Los Angeles and New York-New Jersey terminals has improved container handling efficiency by 24%. Growing semiconductor and EV manufacturing clusters are increasing demand for high-speed air freight coordination, with digital customs clearance adoption rising by 33% across major trade corridors.

Europe holds nearly 24% of global freight forwarding activity, shaped by tightly integrated EU trade corridors and stringent sustainability mandates. Over 45% of freight operators in the region have adopted carbon-tracking logistics systems to comply with emission reporting requirements. Germany, the Netherlands, and Belgium serve as key transit hubs, with Rotterdam handling 32% of EU container throughput. Infrastructure upgrades across rail-linked inland terminals have improved multimodal efficiency by 21%. Companies are investing in green logistics fleets and digital customs automation to maintain competitiveness under tightening regulatory frameworks.

Germany Market Outlook: Germany acts as the core freight and industrial logistics hub in Europe, supported by its automotive and manufacturing base. Over 58% of export shipments rely on multimodal freight forwarding networks connecting Hamburg and Duisburg corridors. Adoption of AI-enabled logistics planning tools has increased operational efficiency by 27%, while industrial exporters are expanding smart warehousing systems to support just-in-time production models.

Asia-Pacific leads global freight forwarding with approximately 38% share, driven by export-heavy manufacturing ecosystems in China, India, and Southeast Asia. Over 60% of global electronics and consumer goods shipments originate from this region. China’s port automation systems have improved container processing efficiency by 31%, while India’s logistics digitization initiatives have increased real-time shipment visibility adoption by 26%. Regional trade agreements and e-commerce growth are intensifying demand for air–sea hybrid logistics networks. Companies are investing heavily in smart ports, AI-driven freight platforms, and regional consolidation hubs.

China Market Outlook: China remains the central node of Asia-Pacific freight forwarding, processing over 30% of regional container traffic. Smart port deployment across Shanghai and Shenzhen has improved cargo turnaround efficiency by 29%. Export-driven manufacturing clusters in electronics and automotive sectors continue to expand reliance on integrated digital freight systems, with over 65% of large exporters now using end-to-end logistics tracking platforms.

South America accounts for nearly 6% of global freight forwarding activity, driven primarily by commodity exports such as agriculture, mining, and energy products. Brazil and Chile are leading infrastructure upgrades, with port modernization projects improving cargo handling efficiency by 17%. Cross-border logistics corridors across Mercosur countries are enhancing trade flow efficiency, though inland transport bottlenecks still cause delays in nearly 23% of shipments. Companies are increasingly adopting digital freight platforms and regional consolidation hubs to reduce fragmentation and improve export reliability.

Brazil Market Outlook: Brazil dominates South American freight forwarding due to its large-scale agricultural and mineral export base. Over 68% of exports pass through Santos and Paranaguá ports, which have seen a 19% improvement in container processing efficiency following terminal automation upgrades. Expansion of rail-linked corridors connecting inland farming regions is improving export logistics consistency and reducing transit delays by approximately 14%.

Middle East & Africa accounts for approximately 5% of global freight forwarding activity, with rapid expansion driven by mega-port developments and trade corridor diversification. The UAE and Saudi Arabia are leading logistics transformation, with Jebel Ali and King Abdullah Port expanding handling capacity by over 22%. Africa is witnessing gradual improvement in intra-regional logistics through AfCFTA-driven trade facilitation. Companies are investing in free trade zones and multimodal logistics hubs to improve connectivity between Asia, Europe, and Africa.

United Arab Emirates Market Outlook: The UAE serves as the primary logistics gateway for the Middle East, handling over 60% of regional freight flows through Dubai’s integrated port-air network. Expansion of Jebel Ali Free Zone infrastructure has improved cargo turnaround efficiency by 26%, while digital customs clearance adoption has reached 71% across major logistics operators, strengthening its position as a global transshipment hub.

Global freight forwarding competition is led by DHL, Kuehne+Nagel, DSV, DB Schenker, C.H. Robinson, and Expeditors, where European integrators compete against U.S. asset-light brokers and Asian export-linked operators. The top five players collectively control about 45% of global forwarding volumes, driven by scale networks and digital customs platforms. Competition is based on pricing efficiency (variance ~12%), real-time shipment visibility adoption (over 60% among leaders), and value-added services improving margin performance by 8–10%. Firms are expanding through acquisitions, such as European network consolidation and U.S. last-mile logistics partnerships, while investing in AI-driven routing and warehouse automation. The competitive shift is moving toward platform-based logistics ecosystems and end-to-end supply chain control. High capital requirements, regulatory compliance, and global carrier access act as entry barriers. Winning requires digital integration strength, multimodal network depth, and superior predictive logistics capability. Consolidation accelerates as scale, technology, and network density define future market leadership globally across lanes.

Kuehne+Nagel

DSV

DB Schenker

C.H. Robinson

Expeditors

UPS Supply Chain Solutions

Nippon Express

Sinotrans

GEODIS

Hellmann Worldwide Logistics

AI-driven freight management systems, IoT-enabled tracking, and blockchain documentation are the core current technologies transforming freight forwarding operations. Around 62% of global forwarders now use AI-based routing tools, improving shipment planning efficiency by 28% and reducing idle time by 18%. IoT sensors deployed across containers enable real-time condition monitoring with 35% higher accuracy in cargo visibility, especially in temperature-sensitive pharmaceutical and electronics shipments. Blockchain adoption in digital bills of lading has reached nearly 30% of cross-border transactions, reducing documentation errors and disputes by 25%.

Legacy freight systems relying on manual booking and EDI-based tracking deliver around 45% lower processing efficiency compared to modern cloud-native logistics platforms. Digital systems reduce documentation turnaround time by nearly 38% and improve carrier utilization by 22%. Companies in the U.S. and Germany are leading migration from traditional systems to integrated logistics APIs, while cost-focused operators in Southeast Asia still rely on hybrid models. The competitive advantage is shifting toward firms that achieve real-time orchestration and predictive scheduling accuracy.

By 2026–2028, adoption of AI-driven freight orchestration and autonomous scheduling systems is expected to redefine global forwarding efficiency. Early adopters are targeting 25% reduction in logistics delays and 30% improvement in route optimization accuracy. Investment is increasingly concentrated in cloud-native logistics ecosystems and interoperable platform development across major trade corridors creating sustained competitive advantage for leaders globally now.

Feb 2025, DHL Group expanded its “AI-powered Smart Logistics Network” across European hubs, improving parcel and freight routing efficiency by 22% and increasing automated sorting throughput by 18%, strengthening cross-border fulfillment speed.

Mar 2025, DSV advanced integration planning for the DB Schenker acquisition, targeting 6–7% global market share consolidation impact and expanding multimodal capacity across Europe and Asia-Pacific, enhancing contract logistics integration.

Sep 2025, DHL Global Forwarding upgraded its U.S. peak-season resilience framework, improving shipment visibility and customs response efficiency by 20% during high-volatility trade flows across Asia–U.S. lanes. Source: www.dhl.com

2026, Kuehne+Nagel enhanced digital SeaExplorer predictive analytics, increasing ETA accuracy by 18% and reducing shipment disruption incidents by 14%, improving ocean freight reliability for global manufacturing clients.

The Freight Forwarding Market Report covers comprehensive analysis across air, sea, road, and rail forwarding services, segmented by type, application, and end-user categories. It evaluates operational efficiency trends, digital freight adoption levels, and multimodal integration across key global trade corridors. The study highlights over 60% adoption of real-time tracking systems among enterprise logistics providers and examines evolving shipment visibility and customs automation practices across major economies.

It provides regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing logistics infrastructure maturity, digital transformation adoption, and trade flow optimization. The report supports strategic decision-making by evaluating investment patterns, competitive positioning, and supply-chain resilience improvements. It also examines emerging technologies such as AI logistics orchestration and blockchain-enabled documentation workflows shaping future operational efficiency and market expansion planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,254.0 Million |

| Market Revenue (2033) | USD 3,433.0 Million |

| CAGR (2026–2033) | 5.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | DHL; Kuehne+Nagel; DSV; DB Schenker; C.H. Robinson; Expeditors; UPS Supply Chain Solutions; Nippon Express; Sinotrans; GEODIS; Hellmann Worldwide Logistics |

| Customization & Pricing | Available on Request (10% Customization Free) |