Reports

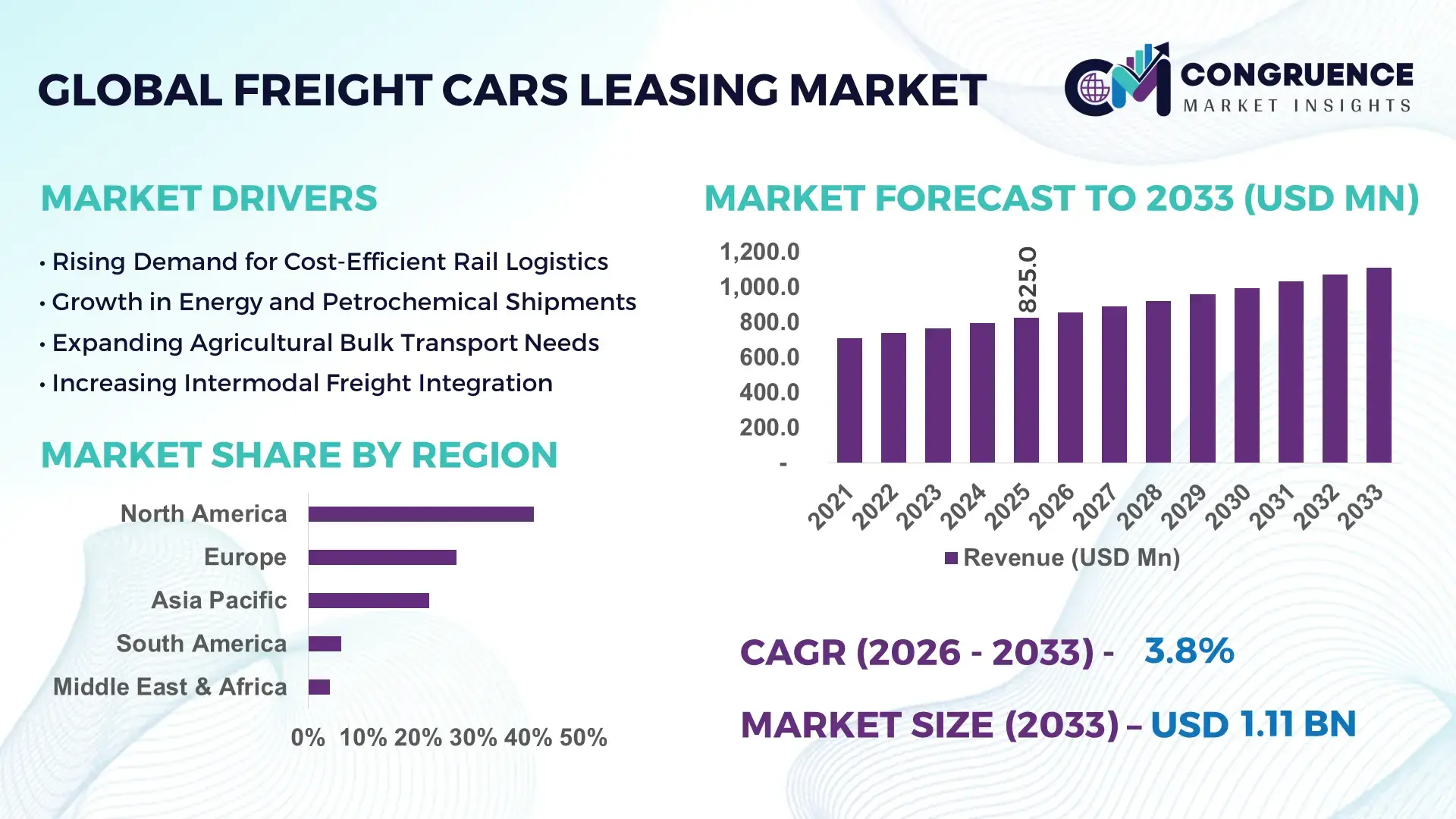

The Global Freight Cars Leasing Market was valued at USD 825.0 Million in 2025 and is anticipated to reach a value of USD 1,111.8 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising rail freight volumes, increasing preference for asset-light logistics models, and fleet modernization initiatives across heavy industries.

The United States remains the dominant country in the Freight Cars Leasing Market, supported by a freight rail network exceeding 140,000 route miles and annual rail freight volumes above 1.6 billion tons. Over 70% of railcars in operation are privately owned or leased, reflecting strong asset-leasing penetration. The country operates more than 1.7 million freight railcars, including tank cars, covered hoppers, and intermodal units. Significant investments in predictive maintenance, telematics-enabled railcars, and automated inspection portals are enhancing fleet utilization rates by 8–12%. Key industry applications include energy, agriculture, chemicals, and automotive logistics, with tank and hopper cars representing over 50% of leased rolling stock demand.

Market Size & Growth: USD 825.0 Million (2025) projected to reach USD 1,111.8 Million by 2033 at 3.8% CAGR, driven by increasing industrial freight volumes and fleet optimization strategies.

Top Growth Drivers: 65% rise in intermodal freight adoption, 40% preference for asset-light logistics models, 30% improvement in fleet utilization through telematics integration.

Short-Term Forecast: By 2028, predictive maintenance adoption is expected to reduce unplanned downtime by 18% and improve asset turnaround time by 12%.

Emerging Technologies: IoT-enabled smart railcars, AI-based predictive analytics, automated wayside inspection systems.

Regional Leaders: North America projected at USD 420 Million by 2033 with high private railcar ownership; Europe at USD 310 Million driven by cross-border freight corridors; Asia-Pacific at USD 240 Million supported by industrial rail expansion.

Consumer/End-User Trends: Energy, chemicals, agriculture, and automotive sectors account for over 75% of leased car demand with rising multi-year lease contracts.

Pilot or Case Example: In 2024, a U.S. rail leasing operator implemented AI-driven monitoring, achieving 15% reduction in maintenance costs and 10% improvement in fleet availability.

Competitive Landscape: Market leader holds approximately 22% share, followed by major competitors including GATX, Trinity Industries, VTG, Ermewa, and CIT Rail.

Regulatory & ESG Impact: Emission reduction mandates and rail safety modernization programs are accelerating replacement of aging fleets with 20% lower-emission railcars.

Investment & Funding Patterns: Over USD 2.5 Billion invested in fleet expansion, refurbishment, and digital fleet management platforms in recent years.

Innovation & Future Outlook: Integration of digital twins, blockchain-enabled asset tracking, and lightweight composite railcar materials is shaping next-generation leasing strategies.

Freight cars leasing demand is concentrated in energy (28%), agriculture (22%), chemicals (18%), and automotive logistics (12%). Technological innovations such as telematics-enabled tank cars and automated brake monitoring systems are improving safety compliance by over 15%. Environmental regulations encouraging modal shift from road to rail support higher leasing penetration in North America and Europe, while Asia-Pacific expansion is fueled by industrial corridor development and export-oriented manufacturing growth.

The Freight Cars Leasing Market holds strategic relevance as global supply chains increasingly prioritize cost efficiency, operational flexibility, and sustainability. Leasing models enable industrial shippers to avoid high upfront capital expenditure while ensuring access to technologically upgraded rolling stock. Telematics-enabled smart railcars deliver 25% faster fault detection compared to manual inspection standards, significantly improving safety and compliance metrics.

North America dominates in volume due to its extensive freight rail infrastructure, while Europe leads in adoption with nearly 60% of cross-border freight operators relying on leased rolling stock for corridor flexibility. Asia-Pacific is rapidly expanding, supported by industrial corridor projects and export-driven rail freight investments. By 2028, AI-based predictive fleet analytics is expected to cut maintenance-related downtime by 20%, enhancing asset turnover and contract profitability.

From a compliance perspective, firms are committing to ESG metrics such as 30% carbon emission reduction by 2030 through modal shifts and lightweight railcar adoption. In 2024, a major U.S. leasing company achieved a 14% improvement in fuel efficiency through aerodynamic retrofits and digital load optimization systems.

Strategically, the Freight Cars Leasing Market is evolving into a technology-driven asset management ecosystem, combining digital tracking, performance analytics, and green fleet modernization. As global trade patterns shift toward resilient and low-carbon logistics, the Freight Cars Leasing Market is positioned as a critical pillar of industrial continuity, regulatory compliance, and sustainable long-term growth.

The Freight Cars Leasing Market is shaped by industrial production cycles, rail infrastructure capacity, commodity trade flows, and regulatory compliance standards. Growing preference for rail over road freight in bulk commodities such as coal, chemicals, and agricultural products is influencing leasing demand patterns. Fleet modernization initiatives are accelerating replacement of aging railcars, particularly in North America and Europe, where safety standards are becoming stricter. Digitalization trends, including IoT sensors and automated inspection systems, are improving fleet reliability and turnaround times. Additionally, volatile fuel prices and carbon reduction targets are encouraging modal shifts to rail, which emits nearly 75% less greenhouse gas per ton-mile compared to road transport. Long-term leasing contracts and diversified rolling stock portfolios are increasingly used to stabilize operational risks and optimize capacity utilization.

Global rail freight demand continues to expand, with bulk commodities accounting for over 45% of rail transport volumes worldwide. Agricultural exports, petrochemical shipments, and construction materials require specialized tank and hopper cars, many of which are leased rather than owned. In North America alone, more than 70% of freight railcars are leased, reflecting strong asset-light adoption. Intermodal rail traffic has grown by approximately 6–8% annually in key trade corridors, increasing demand for container-compatible flatcars. Industrial production expansion in emerging markets has also increased cross-border rail flows by over 10% in select corridors. Leasing allows shippers to rapidly scale fleets during peak demand without long-term capital lock-in, improving operational agility and supply chain responsiveness.

Freight railcars require significant capital investment, with specialized tank or refrigerated units costing up to 20–30% more than standard boxcars. Maintenance compliance standards mandate periodic inspections every 5–10 years, increasing lifecycle costs. Rising steel prices have pushed manufacturing costs upward by nearly 15% in recent years, affecting new fleet expansion. Furthermore, regulatory changes in hazardous material transport require retrofitting or replacing older tank cars, creating financial pressure on smaller leasing operators. Limited rail infrastructure capacity in developing regions also constrains fleet deployment efficiency, leading to longer turnaround times and reduced utilization rates during congestion periods.

Digital transformation is unlocking significant opportunities in the Freight Cars Leasing Market. IoT-enabled sensors can reduce manual inspection time by 30% and improve fault detection accuracy by 25%. Automated wayside monitoring systems identify wheel and brake defects in real time, lowering derailment risks by over 10%. Demand for environmentally optimized railcars with lightweight materials is increasing, offering up to 8% higher load efficiency. Asia-Pacific rail corridor expansion projects covering over 20,000 kilometers create substantial opportunities for fleet leasing expansion. Furthermore, long-term public-private rail infrastructure partnerships are facilitating stable multi-year leasing contracts for industrial clients.

Aging freight car fleets, particularly in mature rail markets, present operational and financial challenges. Approximately 25% of existing railcars in North America exceed 20 years of service life, requiring refurbishment or replacement. Compliance with enhanced braking and tank safety standards demands retrofitting investments that can increase per-car upgrade costs by 10–15%. Cross-border regulatory differences in Europe complicate interoperability, requiring technical modifications for multi-country operations. Additionally, supply chain disruptions affecting steel and component availability have extended railcar manufacturing lead times by up to 6 months, limiting rapid fleet renewal and impacting leasing availability.

Rapid Expansion of Telematics-Enabled Smart Railcars: Over 45% of newly leased freight cars are equipped with GPS and condition-monitoring sensors. These systems improve fleet visibility by 35% and reduce cargo loss incidents by 12%. Real-time data transmission enables predictive interventions, cutting inspection turnaround time by 20% and enhancing compliance with safety regulations.

Increased Adoption of Long-Term Leasing Contracts: More than 60% of industrial shippers now prefer multi-year leasing agreements exceeding five years. This shift has improved fleet utilization rates by 15% and stabilized capacity planning. Energy and chemical sectors account for nearly 46% of these long-duration contracts, reflecting stable commodity transport requirements.

Growth in Intermodal and Cross-Border Rail Freight: Intermodal traffic volumes have increased by 8–10% across major trade corridors. Leasing demand for flatcars and container wagons has risen by 18%, driven by export-oriented manufacturing and port connectivity upgrades. Europe reports over 50% of cross-border freight relying on leased rolling stock to ensure operational flexibility.

Fleet Modernization and Lightweight Material Integration: Approximately 30% of new railcar production incorporates high-strength lightweight steel, improving load capacity by 6–8%. Advanced braking systems have enhanced stopping efficiency by 14%, while aerodynamic retrofits have improved fuel efficiency by 5–7%, supporting ESG-driven fleet upgrades and sustainable logistics transformation.

The Freight Cars Leasing Market is segmented by type, application, and end-user, reflecting the operational diversity of rail-based logistics across industrial economies. Product differentiation is largely based on cargo specialization, including tank cars, covered hoppers, boxcars, flatcars, refrigerated cars, and specialized high-capacity wagons. Demand patterns are closely tied to commodity cycles, intermodal freight growth, and regulatory requirements for hazardous material transport. Applications range from bulk commodity transport and petrochemical logistics to automotive distribution and intermodal container movement. End-user adoption is heavily concentrated in energy, agriculture, chemicals, mining, and manufacturing sectors, which collectively account for over 75% of leased rolling stock utilization. Leasing penetration rates are highest in regions with privatized freight rail systems, where over 65% of railcars are non-railroad owned. Segmentation trends indicate a steady transition toward technologically enhanced and environmentally optimized railcars, particularly in tank and intermodal categories, as operators prioritize safety compliance, fuel efficiency, and predictive maintenance capabilities.

The Freight Cars Leasing Market by type includes tank cars, covered hopper cars, boxcars, flatcars (including intermodal well cars), refrigerated cars, and specialized freight cars. Tank cars represent the leading segment, accounting for approximately 34% of leased fleet demand, primarily due to sustained shipments of crude oil, refined petroleum products, chemicals, and food-grade liquids. Covered hopper cars follow with nearly 26% share, supported by agricultural grains, cement, and plastic resin transport. Flatcars and intermodal well cars collectively hold around 18% of adoption, reflecting rising containerized trade flows. While tank cars dominate current deployment, intermodal well cars are the fastest-growing segment, expanding at an estimated 5.6% CAGR, driven by 8–10% annual growth in containerized rail freight across major trade corridors. Refrigerated cars and specialized high-capacity wagons together contribute roughly 12% of total leased stock, serving niche sectors such as perishable goods and automotive components.

By application, the Freight Cars Leasing Market is categorized into energy and petrochemicals transport, agriculture and food products, chemicals and industrial materials, automotive logistics, mining and metals, and intermodal/containerized freight. Energy and petrochemical transport leads with approximately 31% share, supported by high volumes of crude oil, liquefied gases, and refined fuels requiring compliant tank cars. Agriculture and food products account for around 24%, driven by bulk grain and fertilizer shipments. Chemicals and industrial materials represent close to 18%, reflecting steady demand for specialized containment and safety-certified railcars. Intermodal freight applications are the fastest-growing segment, expanding at an estimated 6.1% CAGR due to port connectivity upgrades and modal shift strategies aimed at reducing highway congestion. Automotive and mining applications collectively contribute nearly 17% of total leasing demand. In 2025, over 48% of large-scale logistics operators reported increasing reliance on leased intermodal railcars for cross-border shipments. Additionally, nearly 55% of industrial shippers indicated preference for leasing specialized tank cars rather than capital ownership to maintain financial flexibility.

End-user segmentation of the Freight Cars Leasing Market highlights energy and utilities, agriculture producers and cooperatives, chemical manufacturers, mining and metals companies, automotive OEMs, and third-party logistics providers. Energy and utilities constitute the leading end-user segment, accounting for approximately 29% of leased railcar utilization, largely due to ongoing petroleum, LNG, and refined product distribution requirements. Agriculture producers follow at around 23%, supported by seasonal grain exports and fertilizer distribution cycles. Chemical manufacturers hold nearly 19%, reflecting continuous demand for compliant tank car fleets. While energy remains dominant, third-party logistics providers are the fastest-growing end-user group, expanding at approximately 5.9% CAGR as outsourcing and integrated logistics models gain traction. Mining, metals, and automotive OEMs together represent nearly 21% of leased fleet deployment. In 2025, more than 52% of North American industrial enterprises reported using leased rolling stock as part of asset-light supply chain strategies. Additionally, 46% of chemical manufacturers indicated investments in sensor-enabled leased tank cars to enhance safety monitoring.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America’s leadership is supported by a freight rail network exceeding 220,000 kilometers and more than 1.7 million freight railcars in operation, with over 70% privately owned or leased. Europe represents approximately 27% of global demand, driven by cross-border freight corridors spanning 9 core TEN-T routes and increasing modal shift policies targeting 30% rail freight share by 2030. Asia-Pacific holds nearly 22% share, backed by rapid industrialization and rail infrastructure projects exceeding 25,000 kilometers under development. South America contributes around 6%, largely concentrated in Brazil and Argentina, while the Middle East & Africa account for roughly 4%, driven by mineral exports and energy logistics expansion. Increasing digital fleet integration—now present in over 45% of newly leased railcars globally—continues to reshape regional competitiveness and operational efficiency benchmarks.

North America represents approximately 41% of the global Freight Cars Leasing Market, supported by extensive freight rail infrastructure and high private railcar ownership exceeding 70% of total fleet volume. Key industries driving demand include energy (crude oil, LNG, refined fuels), agriculture (grain, fertilizers), chemicals, and automotive logistics. The region transports over 1.6 billion tons of freight annually by rail, reinforcing strong leasing dependency. Regulatory measures such as enhanced tank car safety standards and Positive Train Control (PTC) mandates have accelerated replacement of aging fleets, prompting up to 25% of older railcars to undergo refurbishment or retirement. Digital transformation is advancing rapidly, with nearly 50% of newly leased cars equipped with GPS tracking and predictive maintenance sensors. A leading regional player, GATX Corporation, continues expanding its fleet modernization programs, managing over 150,000 railcars globally while integrating telematics to enhance fleet utilization by double-digit percentages. Enterprise adoption behavior reflects preference for long-term leasing contracts exceeding five years, especially among energy and chemical shippers seeking cost stability and regulatory compliance.

Europe accounts for approximately 27% of the global Freight Cars Leasing Market, driven by strong inter-country rail freight integration. Germany, France, and the United Kingdom represent the largest contributors, collectively handling more than 55% of the region’s rail freight volumes. Regulatory frameworks under the European Green Deal aim to shift 30% of road freight over 300 kilometers to rail by 2030, stimulating leasing demand for compliant and energy-efficient wagons. Sustainability initiatives emphasize low-noise braking systems and lightweight wagon structures, improving load efficiency by 6–8%. Over 40% of freight wagons in Western Europe are leased rather than state-owned, reflecting mature private-sector participation. A key regional operator, VTG AG, manages a fleet exceeding 90,000 railcars and is actively investing in digital coupling technology to reduce shunting time by nearly 20%. Regional adoption patterns show strong preference for interoperable railcars capable of multi-country certification, aligning with stringent cross-border compliance requirements.

Asia-Pacific holds around 22% of the global Freight Cars Leasing Market and ranks as the fastest-growing regional cluster. China, India, and Japan are the primary consuming countries, collectively operating more than 800,000 freight railcars. Infrastructure expansion projects exceeding 25,000 kilometers of new or upgraded freight corridors are strengthening long-haul capacity. Industrial manufacturing and export-driven logistics contribute significantly to hopper and container wagon demand. Technological trends include automated freight terminals and AI-based cargo scheduling systems improving turnaround time by 15%. In India, public-private partnerships are accelerating private wagon leasing schemes, increasing non-state-owned freight car participation beyond 30%. Regional consumer behavior indicates strong demand from e-commerce-linked supply chains and steel manufacturing sectors. Leasing adoption is also increasing among mid-sized logistics firms seeking asset-light expansion amid volatile commodity cycles.

South America represents approximately 6% of the global Freight Cars Leasing Market, with Brazil and Argentina serving as the largest contributors. Brazil alone operates more than 30,000 kilometers of freight rail network primarily dedicated to mining and agricultural exports. Bulk commodities such as soybeans, iron ore, and corn account for over 60% of regional rail freight volumes, supporting hopper and gondola wagon leasing. Government concessions and rail privatization initiatives have encouraged fleet modernization, leading to refurbishment of nearly 15% of aging wagons over recent years. Local operators are increasingly integrating condition-monitoring technologies to reduce cargo loss by up to 10%. Consumer behavior is closely tied to export cycles, with leasing demand peaking during harvest seasons. Energy and mining firms show preference for medium-term leasing contracts to manage cyclical commodity fluctuations efficiently.

The Middle East & Africa account for roughly 4% of the global Freight Cars Leasing Market, with demand largely concentrated in oil, gas, mining, and construction material transport. The United Arab Emirates and South Africa are among the leading markets, supported by expanding freight corridors and port connectivity upgrades. Rail infrastructure investments in the Gulf Cooperation Council region exceed several billion dollars, targeting integrated logistics networks linking industrial zones to export terminals. Technological modernization includes adoption of automated inspection portals and digital asset management platforms, improving maintenance cycle efficiency by 12–15%. Trade partnerships and regional logistics diversification strategies are stimulating cross-border rail freight flows. Consumer adoption patterns reveal increasing interest from mining and petrochemical exporters seeking flexible leasing models to reduce capital intensity while meeting international safety compliance standards.

United States – 38% Market Share: It leads globally due to its 140,000+ route-mile freight rail network and high private railcar ownership exceeding 70%, driving sustained leasing penetration.

Germany – 11% Market Share: It is strengthened by advanced cross-border rail integration, strong chemical and automotive freight demand, and regulatory-driven wagon modernization initiatives.

The Freight Cars Leasing Market is moderately consolidated, with approximately 25–30 active leasing companies operating across North America, Europe, and Asia-Pacific. The top five companies collectively account for nearly 55% of the global leased freight car fleet, reflecting strong scale advantages in procurement, refurbishment, and fleet optimization. Leading players typically manage portfolios exceeding 80,000 to 150,000 railcars each, spanning tank cars, covered hoppers, boxcars, and intermodal platforms.

Competitive positioning is influenced by fleet size, asset diversification, digital integration capability, and long-term contractual relationships with energy, agriculture, and chemical shippers. Strategic initiatives between 2023 and 2025 have included multi-thousand railcar fleet expansions, joint ventures for cross-border wagon interoperability, and acquisitions of regional leasing specialists to expand geographic reach. Over 45% of new railcars added to leasing fleets are equipped with telematics and condition-monitoring systems, demonstrating innovation-driven competition.

Mergers and portfolio restructuring activities have strengthened market concentration in North America and Europe, while Asia-Pacific remains comparatively fragmented with rising participation from public-private logistics partnerships. Increasing regulatory compliance requirements and sustainability mandates are pushing operators to replace or retrofit nearly 20–25% of aging fleets, intensifying competition around modernization capabilities. Long-term contracts exceeding five years now represent over 60% of leasing agreements, reinforcing revenue visibility and strengthening incumbent advantage in large industrial corridors.

Ermewa Group

CIT Rail

The Greenbrier Companies

Union Tank Car Company

SMBC Rail Services

Touax Rail

Wascosa AG

Beacon Rail

Akiem Group

Chicago Freight Car Leasing

Andersons Rail Group

Technology integration is reshaping the Freight Cars Leasing Market by enhancing fleet visibility, safety compliance, and lifecycle asset management. Approximately 45–50% of newly manufactured leased railcars are now equipped with GPS tracking, IoT sensors, and automated condition-monitoring systems. These systems provide real-time data on wheel temperature, brake pressure, vibration patterns, and cargo integrity, reducing manual inspection requirements by nearly 30%.

Predictive maintenance platforms using AI-driven analytics can detect component wear up to 20% earlier than traditional maintenance schedules, minimizing derailment risk and lowering unplanned downtime by 15–20%. Automated wayside inspection portals, capable of scanning railcars at speeds exceeding 60 mph, use high-resolution imaging and thermal sensors to detect structural anomalies, improving inspection accuracy by over 25%.

Lightweight high-strength steel and composite materials are increasingly used in tank and hopper cars, enhancing load capacity by 6–8% while reducing tare weight. Advanced braking technologies, including electronically controlled pneumatic (ECP) brakes, improve stopping distance by up to 14% compared to conventional air brake systems. Digital twin models are being implemented by large lessors to simulate stress loads and maintenance cycles, extending asset life by up to 10%.

Blockchain-enabled documentation systems are also gaining traction for lease contract management and cargo tracking, improving documentation transparency and reducing administrative processing time by nearly 18%. These technology advancements are transforming leasing companies into data-driven asset managers, enabling performance benchmarking across fleets exceeding 100,000 railcars and supporting compliance with increasingly stringent international safety standards.

• In April 2025, GATX Corporation Reports 2025 First‑Quarter Results announced a 99.2% fleet utilization rate at GATX Rail North America, net income of $78.6 million, and ~$300 million first-quarter investment volume, reaffirming strong asset demand and leasing performance in North America. Source: www.businesswire.com

• In October 2025, GATX Corporation Reports 2025 Third‑Quarter Results reported continued robust performance with fleet utilization above 93% in Rail Europe and 100% in Rail India, and $877.0 million year-to-date investment volume, signaling broad global leasing strength through diversified geographies. Source: www.businesswire.com

• In February 2026, Trinity Industries, Inc. Announces Fourth Quarter and Full‑Year 2025 Results detailed full-year results including lease fleet utilization of 97.1%, 9,500 railcars delivered, and $91 million net gains on lease portfolio sales, affirming continued operational momentum in freight leasing services. Source: www.trin.net

• In January 2026, Trinity Industries, Inc. Completes Railcar Partnership Restructuring; Raises EPS Guidance completed a strategic restructuring of railcar investment partnerships, increasing expected EPS and realigning ownership in fleets totaling over 23,000 railcars, enhancing capital structure and long-term leasing capabilities. Source: www.trin.net

The Freight Cars Leasing Market Report provides a comprehensive analysis of leasing models, rolling stock categories, application industries, and regional deployment patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report evaluates over six primary freight car types, including tank cars, covered hoppers, boxcars, flatcars, refrigerated wagons, and specialized heavy-haul units. It examines operational metrics such as fleet age distribution, private ownership penetration rates exceeding 65% in mature markets, and digital adoption levels approaching 50% for new railcars.

Industry coverage spans key end-user sectors including energy, agriculture, chemicals, mining, automotive, and intermodal logistics, which collectively represent more than three-quarters of leased railcar utilization. Geographic analysis includes infrastructure scale assessments, with over 220,000 kilometers of freight rail networks evaluated across major economies. The report also reviews regulatory compliance frameworks influencing tank car retrofits, sustainability mandates targeting emission reductions of 20–30%, and safety modernization requirements impacting nearly one-quarter of aging fleets.

Additionally, the scope includes technological benchmarking of telematics integration, predictive maintenance systems, digital coupling pilots, and lightweight material innovations. Competitive profiling covers more than 14 global leasing companies and evaluates strategic initiatives such as fleet acquisitions, modernization programs, and cross-border expansion efforts. The report is structured to support strategic decision-making related to asset allocation, long-term leasing contracts, fleet diversification, and investment planning within the evolving global freight rail ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 825.0 Million |

| Market Revenue (2033) | USD 1,111.8 Million |

| CAGR (2026–2033) | 3.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | GATX Corporation; Trinity Industries, Inc.; VTG GmbH; Ermewa Group; CIT Rail; The Greenbrier Companies; Union Tank Car Company; SMBC Rail Services; Touax Rail; Wascosa AG; Beacon Rail; Akiem Group; Chicago Freight Car Leasing; Andersons Rail Group |

| Customization & Pricing | Available on Request (10% Customization Free) |