Reports

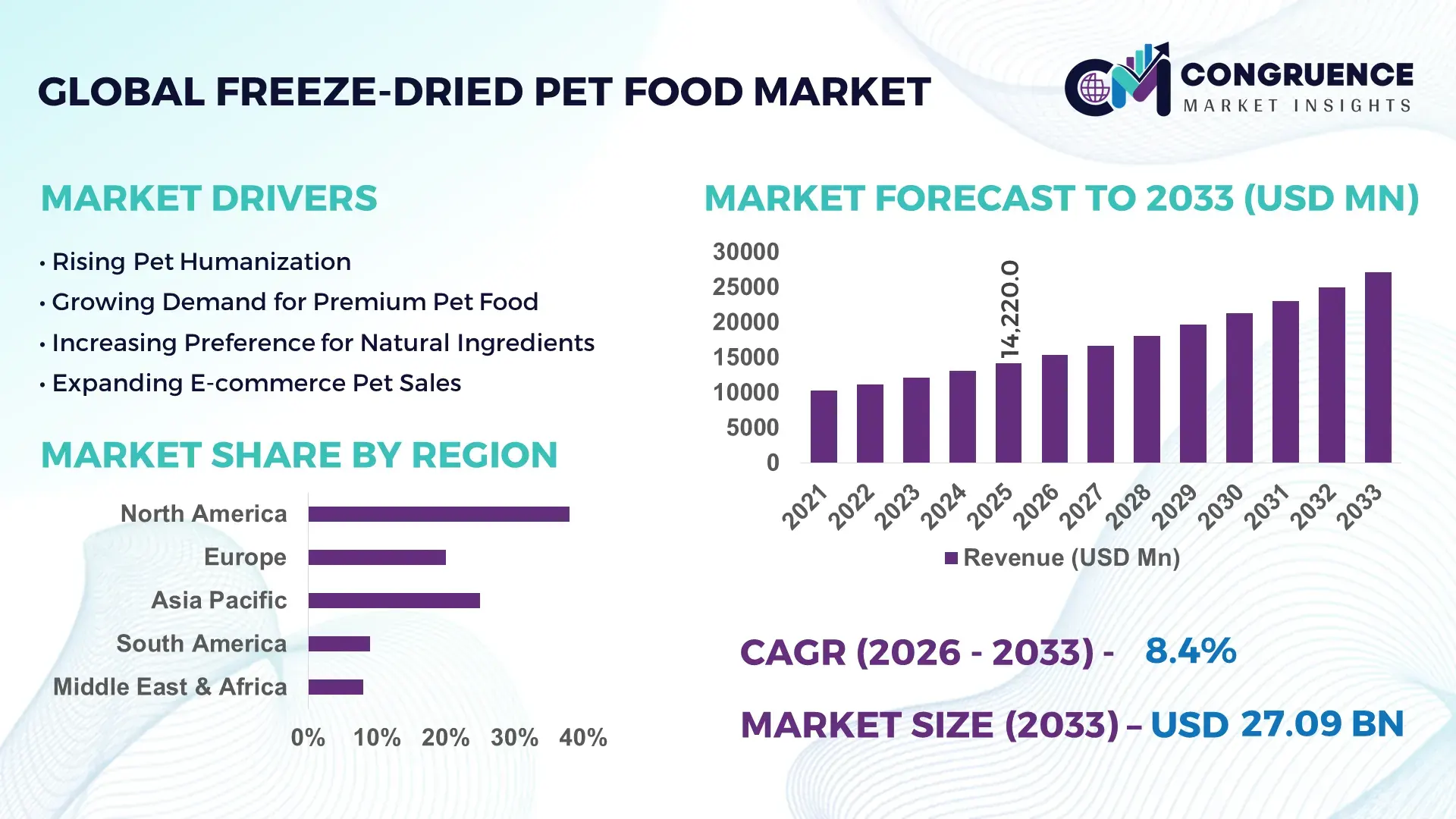

The Global Freeze-Dried Pet Food Market was valued at USD 14220 Million in 2025 and is anticipated to reach a value of USD 27090.26 Million by 2033 expanding at a CAGR of 8.39% between 2026 and 2033.

Advanced freeze-drying systems with nutrient retention rates above 92% and rising premium pet nutrition adoption across urban households are accelerating large-scale production efficiency, while direct-to-consumer subscription channels recorded over 28% order growth during 2025–2026. Between 2024 and 2026, protein sourcing diversification and stricter pet food traceability regulations across North America and Europe reshaped procurement strategies, especially after Red Sea shipping disruptions increased cold-chain logistics costs by nearly 14% for premium animal protein suppliers.

The United States dominates the global freeze-dried pet food industry with approximately 36% market share, supported by over USD 1.8 billion in premium pet nutrition manufacturing investments between 2024 and 2026. More than 68% of premium pet owners in the country actively prefer minimally processed or raw-inspired formulations, compared with below 45% adoption across several Asia-Pacific markets. The country also leads in automated freeze-drying capacity expansion, with high-efficiency processing systems reducing moisture extraction time by nearly 22% versus conventional dehydration methods. Strong veterinary nutrition partnerships, e-commerce penetration above 40% in pet food retail, and rising demand from multi-pet households continue strengthening the U.S. competitive advantage.

Manufacturers prioritizing vertically integrated protein sourcing, advanced preservation technology, and regionalized production hubs are positioned to secure stronger margins and supply resilience in the high-growth global freeze-dried pet food market.

Market Size & Growth: USD 14220 Million in 2025 to USD 27090.26 Million by 2033 at 8.39% CAGR, driven by premium raw nutrition demand and automated freeze-drying expansion.

Top Growth Drivers: Premium pet ownership expanded 31%, direct-to-consumer sales rose 28%, and nutrient-retention processing efficiency improved 22% globally.

Short-Term Forecast: By 2027, automated freeze-drying lines reduce production waste by 18% and improve batch throughput efficiency by 24%.

Emerging Technologies: AI-driven formulation systems, robotic packaging, and smart moisture-control sensors improved product consistency by over 20% in advanced facilities.

Regional Leaders: North America exceeds USD 9.4 billion demand, Europe crosses USD 6.8 billion, and Asia-Pacific surpasses USD 5.1 billion with rapid premiumization trends.

Consumer/End-User Trends: More than 64% of urban pet owners prioritize high-protein functional nutrition, while grain-free freeze-dried formulations gained 26% higher repeat purchases.

Pilot/Case Example: In 2025, a large-scale automated freeze-drying expansion project improved production capacity by 30% and reduced energy consumption by 16%.

Competitive Landscape: Top companies collectively control nearly 42% market share, with premium nutrition brands focusing on veterinary-backed formulations and subscription models.

Regulatory & ESG Impact: Sustainable packaging adoption increased 35%, while stricter ingredient traceability rules improved premium export compliance rates by 19%.

Investment & Funding: Global investments surpassed USD 2.3 billion between 2024 and 2026, driven by regional production expansion and protein sourcing partnerships.

Innovation & Future Outlook: Functional probiotics, single-ingredient protein recipes, and localized sourcing strategies are redefining next-generation freeze-dried pet nutrition portfolios.

Companion animal nutrition accounts for nearly 61% of total industry demand, while premium canine formulations contribute over 44% of product innovation activity globally. Advanced low-temperature preservation systems now improve nutrient stability by approximately 21%, supporting cleaner-label product launches and veterinary-backed nutrition positioning. North America and Western Europe remain high-value consumption hubs, while Asia-Pacific demand expanded by over 18% due to rising urban pet ownership and premium retail penetration. Manufacturers are also accelerating regional sourcing strategies to offset protein supply volatility and evolving pet food compliance standards. The market is steadily shifting toward functional, traceable, and personalized freeze-dried nutrition platforms that strengthen long-term competitive differentiation.

The freeze-dried pet food market is transforming into a strategic battleground for premium nutrition companies, ingredient processors, and automated food technology providers as consumer preference rapidly shifts toward minimally processed, protein-rich formulations. More than 63% of premium pet owners now prioritize functional nutrition with higher digestibility and ingredient transparency, forcing manufacturers to accelerate product innovation and optimize regional supply chains. Between 2024 and 2026, tighter pet food traceability regulations and protein sourcing disruptions across major export routes intensified procurement restructuring, particularly for poultry and salmon-based formulations. Companies are increasingly reallocating capital toward localized freeze-drying infrastructure, subscription commerce platforms, and veterinary-backed product lines to secure stronger customer retention and pricing power.

Advanced continuous freeze-drying technology improves production efficiency by 27% while reducing operational cost by 18% compared to legacy batch-processing systems. North America leads in production volume, while Asia-Pacific leads in adoption acceleration with premium pet food demand expanding above 21% across urban retail channels. Over the next three years, automated packaging integration and AI-driven formulation systems are projected to reduce manufacturing waste by 16% and improve production throughput by nearly 24%. Sustainable packaging conversion is also becoming a competitive advantage, lowering logistics weight costs by approximately 11% while improving export compliance across European markets.

In 2025, a major pet nutrition manufacturer expanded smart freeze-drying operations and achieved a 29% reduction in moisture variability alongside a 14% increase in shelf-life stability. Strategic partnerships between protein suppliers and pet wellness brands are accelerating, with multi-region sourcing agreements increasing by over 33% since 2024. The competitive landscape is shifting toward vertically integrated, technology-driven operators capable of balancing premium quality, supply resilience, and scalable production efficiency across global markets.

Rising demand for biologically appropriate pet nutrition and clean-label formulations is accelerating freeze-dried pet food adoption across premium retail and veterinary channels. More than 64% of urban pet owners now prioritize minimally processed diets, while high-protein freeze-dried products generate nearly 31% higher repeat purchase rates than traditional kibble. Simultaneously, advanced low-temperature preservation systems improve nutrient retention above 92%, strengthening product differentiation and pricing power. Supply chain restructuring after Red Sea logistics disruptions forced manufacturers to regionalize protein sourcing and expand localized production capacity. In response, leading companies increased automated freeze-drying investments by over 26% during 2025–2026 and accelerated strategic partnerships with poultry, seafood, and functional ingredient suppliers to secure long-term manufacturing stability and faster fulfillment efficiency.

Freeze-dried pet food production remains constrained by volatile animal protein pricing, energy-intensive processing requirements, and limited industrial freeze-drying infrastructure. Premium poultry and seafood ingredient costs increased nearly 19% between 2024 and 2026, while industrial electricity expenses for continuous freeze-drying operations rose above 14% across several manufacturing hubs. Heavy dependence on concentrated protein supply regions further exposes manufacturers to shipping delays and procurement instability during geopolitical disruptions. These pressures directly reduce margin flexibility, extend lead times, and limit scalable production expansion for mid-sized brands. To mitigate operational risk, companies are diversifying regional supplier networks, securing multi-year procurement contracts, and adopting hybrid preservation technologies that reduce energy consumption by approximately 17% while improving processing throughput and production resilience.

Functional pet nutrition and emerging-market premiumization are reshaping the future growth structure of the freeze-dried pet food industry. Demand for probiotic-infused, single-protein, and customized formulations expanded by over 24% during 2025, while Asia-Pacific premium pet ownership increased nearly 18% across urban markets. AI-assisted formulation systems now reduce ingredient optimization time by approximately 21%, enabling faster commercial launches and targeted veterinary nutrition products. Subscription-driven distribution models and direct-to-consumer retail ecosystems are also unlocking higher-margin recurring revenue streams. Companies are positioning aggressively through regional manufacturing expansion, precision nutrition R&D, and strategic partnerships with veterinary clinics and ingredient biotechnology firms. This shift is creating non-obvious advantages in product personalization, inventory efficiency, and localized supply resilience for future category leaders globally.

The freeze-dried pet food market faces execution risks tied to manufacturing scalability, regulatory complexity, and operational consistency across multi-region supply chains. Industrial freeze-drying facilities require energy consumption levels nearly 35% higher than conventional dehydration systems, while compliance costs linked to ingredient traceability and export labeling increased approximately 16% since 2024. Infrastructure limitations in emerging markets also constrain cold-storage logistics and premium product distribution efficiency. These barriers create uneven production quality, inventory imbalances, and slower international market penetration for expanding brands. Companies must aggressively invest in automated monitoring systems, renewable energy integration, and cross-border supplier partnerships to maintain stable output and regulatory alignment. Competitive positioning increasingly depends on balancing premium formulation standards with scalable, cost-efficient manufacturing and resilient procurement ecosystems.

32% increase in AI-enabled production monitoring is reshaping operational consistency across premium pet food facilities. Manufacturers are deploying sensor-based moisture tracking and automated temperature balancing systems to reduce batch variability by 19% and improve line throughput by 23%. Labor shortages in North American processing hubs accelerated robotics integration, forcing mid-sized producers to modernize legacy operations. Companies are restructuring production around high-efficiency continuous freeze-drying platforms to optimize energy use and stabilize export-grade quality standards.

27% expansion in regional protein sourcing partnerships is redefining procurement strategies and inventory planning. Following logistics disruptions across Red Sea shipping routes, pet food companies reduced dependency on single-origin poultry and seafood supply chains. Multi-region ingredient sourcing lowered procurement delays by 16% while improving production continuity across Europe and Asia-Pacific. A non-obvious shift is emerging toward localized freeze-dried ingredient processing near farming clusters, reducing transportation weight costs and improving freshness retention for premium formulations.

41% growth in subscription-driven purchasing models is shifting customer retention dynamics across online retail channels. Premium pet owners increasingly prefer recurring delivery models for customized feeding plans, increasing repeat order frequency by 29%. Companies are responding through direct-to-consumer platform expansion, personalized nutrition bundling, and integrated veterinary recommendation systems. This transition is optimizing inventory forecasting accuracy while reducing customer acquisition dependency on traditional retail networks.

24% rise in functional freeze-dried formulations is accelerating category repositioning beyond conventional feeding products. Digestive health blends, single-protein recipes, and probiotic-infused toppers now account for over 38% of new product launches globally. Stricter ingredient transparency standards across European markets are forcing brands to simplify formulations and strengthen traceability compliance. Manufacturers are rapidly scaling veterinary-backed product lines and reformulating portfolios to capture premium wellness-focused demand with higher-margin specialized nutrition offerings.

The freeze-dried pet food market is segmented by type, application, and end-user, with demand increasingly concentrated in premium nutrition and convenience-driven categories. Freeze-Dried Raw Meals and Complete Nutrition Meals collectively account for over 48% of product demand due to high protein retention and full-meal functionality. Daily Feeding dominates application usage with nearly 39% share, while Digestive Health products are expanding rapidly as functional nutrition adoption rises above 21% globally. Pet Owners and Online Retailers together contribute over 52% of purchasing activity, reflecting accelerating direct-to-consumer behavior. Companies are shifting investment toward specialized formulations, subscription-based distribution, and scalable premium product portfolios to capture evolving demand patterns and strengthen long-term market positioning.

Freeze-Dried Raw Meals dominate the freeze-dried pet food market with approximately 34% share due to strong consumer preference for minimally processed, protein-dense nutrition and higher perceived ingredient quality. Their structural dominance is reinforced by superior nutrient retention rates above 90% and increasing veterinary endorsement for raw-inspired feeding. However, Complete Nutrition Meals are emerging as the fastest-growing category, expanding by nearly 23% as pet owners prioritize convenience, portion control, and balanced nutritional profiles. Unlike Freeze-Dried Raw Meals, Complete Nutrition Meals offer easier integration into subscription feeding programs and retail distribution networks, making them highly scalable for mass premiumization strategies. Freeze-Dried Treats and Freeze-Dried Toppers collectively contribute around 31% market share, supported by rising demand for functional rewards and appetite-enhancing feeding customization. Single-Ingredient Products maintain niche strategic importance in allergy-sensitive and limited-ingredient diets, particularly across premium veterinary channels. Companies are aggressively expanding specialized production lines, introducing probiotic-enhanced formulations, and optimizing packaging formats to capture higher-margin personalized nutrition demand while reducing dependence on traditional dry pet food categories.

Daily Feeding remains the leading application segment with nearly 39% share, driven by increasing consumer transition toward complete freeze-dried nutrition as a replacement for conventional kibble products. Usage concentration is strongest among multi-pet households and premium urban consumers seeking high-protein, shelf-stable feeding solutions with simplified ingredient profiles. Meanwhile, Digestive Health applications are accelerating rapidly, expanding by over 22% due to rising awareness of gut health, probiotic supplementation, and allergy-sensitive nutrition management. Daily Feeding currently dominates through consistent purchase frequency, while Digestive Health is reshaping innovation priorities through functional ingredient integration and veterinary-backed product positioning. Training Treats and Pet Nutrition Supplements together account for approximately 29% of market demand, supported by behavioral training trends and personalized wellness routines. Travel Feeding is also gaining operational relevance as lightweight, non-refrigerated premium products improve portability and convenience. Companies are repositioning portfolios toward functional nutrition categories, scaling targeted formulations, and integrating digestive-support claims into mainstream product lines to capture higher-value recurring demand across premium retail and online channels.

Pet Owners represent the leading end-user segment with approximately 43% market share, driven by rising premiumization, direct purchasing behavior, and increasing demand for minimally processed pet nutrition. Demand concentration remains strongest among urban households with higher spending on functional feeding solutions and subscription-based purchasing models. Online Retailers are the fastest-growing end-user group, expanding by nearly 27% as consumers increasingly shift toward auto-delivery services, personalized nutrition bundles, and digital product comparison platforms. Pet Specialty Stores continue maintaining strong relevance through in-store premium product education and high-margin product positioning, while Veterinary Clinics are accelerating adoption of digestive-health and allergy-sensitive formulations. Collectively, Veterinary Clinics, Pet Boarding Centers, and Animal Shelters account for roughly 33% of specialized demand, particularly for controlled feeding programs and wellness-focused nutrition management. Companies are targeting these groups through customized packaging, clinic partnerships, loyalty-based pricing structures, and exclusive online product launches. The market is clearly shifting toward digitally influenced purchasing ecosystems where convenience, personalization, and veterinary trust are becoming decisive competitive differentiators.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.12% between 2026 and 2033.

North America leads in premium freeze-dried pet food consumption and advanced production capacity, supported by high-protein pet nutrition adoption exceeding 64% among urban pet owners. Europe contributes nearly 29% of global demand, driven by strict ingredient traceability standards and sustainable packaging integration across premium product lines. Asia-Pacific accounts for approximately 24% market share but is rapidly accelerating through localized manufacturing expansion, digital retail penetration, and rising premium pet ownership in China, Japan, and South Korea. Meanwhile, South America and the Middle East & Africa collectively represent over 9% demand, supported by growing specialty pet nutrition awareness. Global supply chain restructuring and regional protein sourcing diversification are forcing companies to prioritize localized production, automated freeze-drying infrastructure, and direct-to-consumer expansion strategies across high-growth markets.

North America controls nearly 38% of the freeze-dried pet food market due to strong premium pet ownership trends, advanced cold-chain infrastructure, and rapid adoption of minimally processed nutrition products. More than 66% of premium pet households actively prefer high-protein or raw-inspired formulations, accelerating demand for freeze-dried meals and functional toppers. Supply chain regionalization after 2024 logistics disruptions pushed manufacturers to localize protein sourcing and expand automated processing capacity. Smart freeze-drying systems improved operational throughput by approximately 24%, while large-scale production upgrades reduced moisture inconsistency by 18%. Companies are prioritizing subscription commerce, veterinary-backed formulations, and vertically integrated supply chains as consumers increasingly favor traceable, convenience-driven nutrition solutions. The region remains the primary investment destination for scalable premium product innovation and manufacturing optimization.

Europe represents approximately 29% of global freeze-dried pet food demand, led by Germany, the United Kingdom, and France through strong premium pet care spending and quality-focused purchasing behavior. Tightened ingredient traceability regulations and sustainable packaging mandates are redefining operational standards across the regional market. More than 41% of premium pet food launches now feature simplified ingredient labeling and recyclable packaging formats to align with compliance-driven consumer preferences. Manufacturers are adopting energy-efficient freeze-drying technologies that lower processing waste by nearly 15% while improving export readiness across EU markets. Retailers and veterinary networks increasingly prioritize certified functional nutrition products with transparent sourcing verification. Companies expanding in Europe are investing aggressively in compliance optimization, sustainable sourcing partnerships, and localized premium production capabilities to secure long-term competitive positioning.

Asia-Pacific ranks as the fastest-expanding freeze-dried pet food market, supported by rapid urban pet ownership growth and expanding premium retail ecosystems across China, Japan, South Korea, and Australia. The region contributes nearly 24% of global demand while recording premium pet nutrition adoption increases above 21% in major metropolitan markets. Localized manufacturing expansion and lower regional processing costs are strengthening production scalability and export competitiveness. Companies are accelerating digital commerce integration, with online premium pet food purchases rising by approximately 34% between 2024 and 2026. Strategic investments in regional freeze-drying infrastructure improved production turnaround efficiency by nearly 19%, enabling faster market responsiveness. Asia-Pacific has become critical for global expansion strategies due to its combination of scale, speed, digitally driven purchasing behavior, and manufacturing flexibility.

South America accounts for nearly 6% of global freeze-dried pet food demand, with Brazil and Argentina leading regional consumption through rising companion animal ownership and growing premium pet care awareness. Urban middle-income consumers increasingly prefer functional nutrition products, driving freeze-dried treat and topper adoption growth above 17% across specialty retail channels. However, high import dependency for premium animal proteins and limited industrial freeze-drying infrastructure continue constraining large-scale production efficiency. Logistics and cold-chain limitations also increase regional distribution costs by approximately 13%. Companies are responding through localized packaging operations, strategic distributor partnerships, and selective regional manufacturing expansion. Consumer purchasing behavior remains price-sensitive but strongly quality-focused, positioning South America as a high-potential market where operational efficiency and localized affordability determine long-term competitiveness.

The Middle East & Africa contributes approximately 3% of global freeze-dried pet food demand, led by the UAE, Saudi Arabia, and South Africa through expanding premium retail infrastructure and rising urban pet adoption. Increasing investment in modern retail ecosystems and specialized veterinary distribution networks is reshaping access to premium pet nutrition products. More than 22% of high-income urban consumers now prioritize imported or functional pet food formulations with higher protein quality and traceable ingredients. Companies are accelerating regional distributor partnerships and deploying digitally integrated retail strategies to improve premium product accessibility. Import-driven supply structures still create pricing pressure and inventory volatility, particularly during logistics disruptions. Despite infrastructure limitations, the region is emerging as a strategic long-term expansion market supported by premiumization trends and modernization-driven retail transformation.

United States Freeze-Dried Pet Food Market – 36% Market Share: Dominates through advanced freeze-drying infrastructure, high premium pet ownership, and strong direct-to-consumer subscription adoption.

China Freeze-Dried Pet Food Market – 18% Market Share: Leads growth momentum through expanding urban pet ownership, localized production scaling, and rapid digital pet retail penetration.

The freeze-dried pet food market is dominated by premium nutrition specialists competing against diversified pet food manufacturers, while regional private-label producers aggressively challenge on pricing and localized sourcing. Top players including Stella & Chewy’s, Primal Pet Foods, Vital Essentials, Open Farm, and Instinct collectively control nearly 42% market share through advanced freeze-drying capabilities, veterinary-backed formulations, and subscription-driven distribution. Competition is intensifying around nutrient retention efficiency, ingredient traceability, and supply chain control, with automated production systems improving processing throughput by 24% and reducing waste by 17%. Premium brands are vertically integrating protein sourcing and expanding regional manufacturing to offset logistics volatility and ingredient inflation pressures. Simultaneously, emerging brands are differentiating through single-protein formulations, probiotic integration, and digital retail acceleration. High capital requirements for industrial freeze-drying infrastructure and compliance-driven production standards remain major entry barriers. Winning increasingly depends on operational scalability, premium positioning, and resilient multi-region sourcing ecosystems.

Stella & Chewy’s

Primal Pet Foods

Vital Essentials

Open Farm

Instinct

Northwest Naturals

Nature’s Variety

Dr. Marty Pets

Kiwi Kitchens

Nulo Pet Food

Orijen

Steve’s Real Food

BIXBI Pet

Carnivora Pet Foods

Advanced continuous freeze-drying systems are reshaping production efficiency across premium pet nutrition manufacturing. Compared with legacy batch-processing methods, next-generation automated freeze-drying platforms improve throughput efficiency by nearly 27% while reducing energy consumption by approximately 18%. More than 44% of large-scale premium pet food facilities now deploy AI-enabled moisture monitoring and predictive temperature balancing systems to minimize nutrient degradation and improve shelf-life consistency. These technologies are optimizing operational scalability while strengthening quality control for export-focused manufacturers competing in premium retail and veterinary nutrition channels.

Emerging technologies between 2026 and 2028 are accelerating ingredient traceability, formulation precision, and smart packaging integration. Blockchain-enabled sourcing platforms and digital lot-tracking systems improved ingredient verification speed by over 31% across advanced production networks, particularly in North America and Europe where traceability compliance standards are tightening. Simultaneously, robotic packaging automation reduced packaging errors by approximately 16% and improved fulfillment speed across subscription-driven distribution models. Premium brands with vertically integrated digital supply chains are gaining stronger retailer trust and faster product deployment capabilities.

Disruptive innovation is increasingly centered around precision nutrition and functional freeze-dried formulations. AI-assisted formulation systems reduce product development timelines by nearly 21%, enabling rapid deployment of probiotic-infused, single-protein, and allergy-sensitive recipes. More than 38% of premium product launches now incorporate personalized feeding technologies or functional wellness positioning. Companies investing aggressively in automation, digital sourcing visibility, and nutrient-preservation optimization are capturing stronger competitive advantages as operational efficiency and ingredient transparency become decisive market differentiators.

December 2025 – Stella & Chewy’s expanded distribution into more than 1,400 Publix supermarkets across the Southeastern United States, accelerating mainstream retail penetration for freeze-dried raw pet nutrition products. The rollout significantly expanded shelf accessibility and strengthened omnichannel visibility for premium meal mixers and toppers. [Retail Expansion Push] Source: PetfoodIndustry

December 2025 – Stella & Chewy’s launched 19 freeze-dried raw pet nutrition products across 464 Sprouts Farmers Market locations, including 10 freeze-dried dog food SKUs. The deployment strengthened premium grocery channel presence and increased consumer access to minimally processed nutrition products nationwide. [Premium Grocery Scaling]

February 2026 – Pure Treats acquired Primal Pet Foods, adding manufacturing facilities in Texas and Colorado to expand freeze-dried and raw pet food production capacity. The acquisition strengthened operational scale, regional manufacturing reach, and vertically integrated supply capabilities within premium pet nutrition categories. [Manufacturing Consolidation Wave] Source: Pet Food Processing

September 2025 – Stella & Chewy’s expanded freeze-dried meal toppers and dinner products into more than 1,900 Target retail locations across the United States. The strategic retail deployment accelerated mainstream premium pet food adoption and improved direct consumer product exposure nationwide. [Mass Retail Penetration]

This report delivers comprehensive coverage of the freeze-dried pet food market across key product types, applications, end-users, technologies, and regional demand centers. The analysis includes Freeze-Dried Raw Meals, Freeze-Dried Treats, Freeze-Dried Toppers, Single-Ingredient Products, and Complete Nutrition Meals alongside applications such as Daily Feeding, Digestive Health, Weight Management, and Pet Nutrition Supplements. End-user evaluation spans Pet Owners, Online Retailers, Veterinary Clinics, Pet Specialty Stores, Animal Shelters, and Pet Boarding Centers. Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed assessment of production trends, premium nutrition adoption, and supply chain restructuring.

The report analyzes more than 20 strategic market indicators, including adoption shifts, ingredient traceability deployment, operational automation trends, and premium retail penetration patterns. Over 44% of large-scale manufacturers now utilize automated freeze-drying technologies, while functional freeze-dried formulations account for nearly 38% of new product launches globally. The study also profiles leading companies competing through vertical integration, AI-assisted formulation systems, sustainable packaging deployment, and direct-to-consumer distribution expansion.

From 2026 to 2033, the report highlights future-facing opportunities in precision pet nutrition, digitally integrated sourcing ecosystems, probiotic-enhanced formulations, and localized manufacturing expansion. Strategic insights support investment planning, competitive benchmarking, regional expansion decisions, and operational positioning across evolving premium pet nutrition ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14220 Million |

|

Market Revenue in 2033 |

USD 27090.26 Million |

|

CAGR (2026 - 2033) |

8.39% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stella & Chewy’s, Primal Pet Foods, Vital Essentials, Open Farm, Instinct, Northwest Naturals, Nature’s Variety, Dr. Marty Pets, Kiwi Kitchens, Nulo Pet Food, Orijen, Steve’s Real Food, BIXBI Pet, Carnivora Pet Foods |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |