Reports

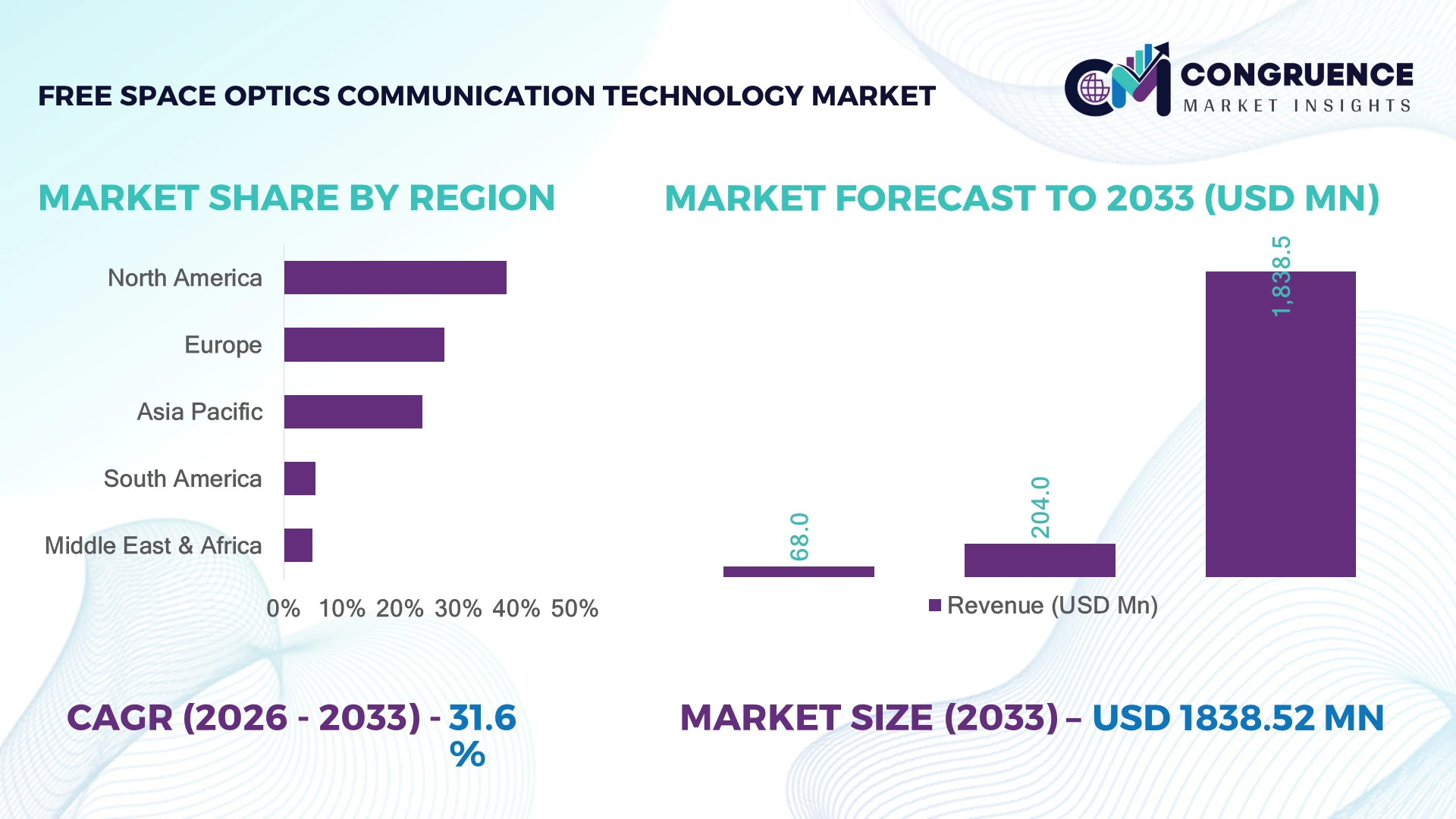

The Global Free Space Optics Communication Technology Market was valued at USD 204.0 Million in 2025 and is anticipated to reach a value of USD 1,838.5 Million by 2033 expanding at a CAGR of 31.63% between 2026 and 2033. Growth is primarily driven by accelerating deployment of high-capacity 5G/6G backhaul, secure defense communication networks, and fiber-alternative connectivity for urban and remote infrastructure.

The United States dominates the global market with an estimated 34% share, supported by Department of Defense modernization programs, commercial satellite communication expansion, and hyperscale data center investments. Compared with Germany, where industrial optical networking adoption remains below 12% of enterprise connectivity projects, the U.S. benefits from stronger defense procurement and nationwide digital infrastructure initiatives. Rising geopolitical focus on resilient communications following the Russia–Ukraine conflict has further accelerated deployment priorities.

Organizations should prioritize high-security, low-latency optical wireless solutions and strategic partnerships to capitalize on expanding infrastructure modernization programs.

Market Size & Growth: Valued at USD 204.0 Million (2025) and projected to reach USD 1,838.5 Million (2033) at 31.63% CAGR, driven by secure high-bandwidth wireless connectivity and expanding 5G backhaul deployments.

Top Growth Drivers: Defense communication modernization (40%+ of major programs), smart city optical infrastructure (25% deployment increase), and data center interconnect expansion (30% annual network upgrades).

Short-Term Forecast: By 2028, optical wireless deployment is expected to reduce last-mile installation costs by nearly 35% while improving network availability by over 20%.

Emerging Technologies: AI-enabled beam alignment, adaptive optics, hybrid RF-FSO systems, and satellite optical terminals are transforming advanced global communication networks.

Regional Leaders: North America (USD 73 Million) leads through defense adoption, Europe (USD 52 Million) advances industrial digital infrastructure, and Asia-Pacific (USD 48 Million) accelerates smart city and telecom expansion.

Consumer/End-User Trends: More than 55% of enterprise deployments focus on secure campus connectivity, financial services, defense, and telecom backhaul applications.

Pilot/Case Example: In 2024, advanced optical backhaul trials achieved approximately 45% faster deployment compared with conventional fiber installation in challenging urban environments.

Competitive Landscape: The leading supplier holds approximately 18% market share, with major participants including fSONA Networks, CableFree, Mostcom, LightPointe Communications, and BridgeComm.

Regulatory & ESG Impact: National digital infrastructure initiatives improved secure broadband accessibility by approximately 22%, while trench-free deployment reduced construction-related environmental impact.

Investment & Funding: More than USD 700 Million has been committed globally through defense contracts, telecom partnerships, and satellite optical communication initiatives amid supply-chain diversification.

Innovation & Future Outlook: Quantum-secure optical communications, integrated satellite-terrestrial networks, and AI-driven autonomous alignment are strengthening long-term competitive positioning.

Free Space Optics Communication Technology is witnessing expanding adoption across telecom backhaul, defense communications, enterprise campus networking, and satellite ground stations where high-speed, license-free connectivity is essential. Recent innovations in adaptive optics, AI-assisted beam tracking, and hybrid RF-FSO platforms have improved link reliability by nearly 30% under variable atmospheric conditions. Growing infrastructure resilience initiatives and diversified communication networks are reinforcing deployment priorities, setting the stage for broader strategic adoption across critical industries.

Free Space Optics Communication Technology has become strategically important as governments, telecom operators, and enterprises seek resilient, high-capacity communication networks without the cost and delays associated with extensive fiber deployment. Infrastructure modernization, defense communication upgrades, and digital transformation programs are accelerating adoption across metropolitan networks, industrial facilities, and remote connectivity applications. Supply-chain diversification has also encouraged operators to deploy flexible wireless optical links that reduce dependence on conventional cable infrastructure.

Modern Free Space Optics systems deliver multi-gigabit throughput while reducing deployment time by nearly 60% compared with conventional underground fiber installation in suitable environments. North America leads large-scale defense and enterprise deployments, whereas Asia-Pacific is expanding rapidly through smart city projects, 5G transport networks, and industrial automation initiatives. Over the next two to three years, AI-enabled beam steering and adaptive optics are expected to improve link availability by approximately 15%, enhancing operational reliability across dense urban environments.

Telecom operators increasingly deploy hybrid RF-FSO networks to maintain uninterrupted connectivity during infrastructure expansion, while technology providers are strengthening partnerships with satellite operators and defense agencies to broaden application coverage. Organizations that invest early in intelligent optical networking platforms, advanced security capabilities, and scalable deployment models will secure stronger competitive differentiation, faster network rollout, and long-term operational resilience.

Growing demand for fiber-equivalent connectivity without civil excavation is reshaping investment priorities across telecom, defense, and enterprise networking. More than 65% of global mobile traffic is expected to be supported through advanced backhaul upgrades by the end of the decade, while over 40% of defense communication modernization programs now emphasize optical and secure wireless technologies. In the United States, expanding 5G infrastructure and Department of Defense modernization initiatives are accelerating Free Space Optics (FSO) deployments for mission-critical applications. This structural shift reduces deployment timelines by nearly 60% compared with conventional fiber in suitable environments. Technology vendors are responding through AI-enabled beam alignment, hybrid RF-FSO solutions, and strategic partnerships with telecom operators and satellite providers, strengthening deployment flexibility and improving service continuity across dense urban and remote locations.

Atmospheric attenuation remains a structural limitation for long-distance optical wireless communication, particularly during dense fog, heavy rainfall, and snow events, where signal availability can decline by more than 30% under severe environmental conditions. Around 45% of large-scale enterprise deployments still require hybrid RF backup systems to maintain network continuity. In the United Kingdom, variable weather conditions have increased planning complexity for outdoor optical links, while inconsistent interoperability standards across vendors slow multi-network integration. These factors elevate deployment costs, extend procurement cycles, and complicate network scalability. Companies are mitigating operational risks through localized manufacturing, adaptive optics, multi-path redundancy, and long-term component sourcing agreements to improve resilience while reducing dependence on single-vendor ecosystems.

The convergence of satellite communications, AI-driven networking, and hybrid RF-FSO architectures is creating new commercial opportunities beyond conventional telecom backhaul. Industry assessments indicate hybrid optical networks can improve link availability by over 20%, while AI-assisted beam tracking enhances alignment accuracy by approximately 35% in dynamic environments. India is expanding digital infrastructure and smart city initiatives that increasingly favor rapid-deployment wireless optical connectivity where fiber rollout remains economically challenging. At the same time, low-Earth-orbit satellite integration is opening new applications across logistics, mining, ports, and disaster recovery. Companies are expanding R&D investments, forming ecosystem partnerships with satellite operators, and developing software-defined optical platforms that enable scalable, high-capacity connectivity with lower infrastructure complexity and faster deployment cycles.

Achieving consistent large-scale deployment remains challenging as Free Space Optics networks require precise alignment, continuous monitoring, and seamless integration with existing communication infrastructure. Beam misalignment caused by building movement or vibration can reduce link performance by nearly 25%, while approximately 50% of enterprise projects require integration with legacy IP and RF networking platforms. In Japan, increasingly dense urban infrastructure creates additional engineering complexity for rooftop optical deployments and network optimization. Addressing these execution challenges demands greater investment in intelligent network management, automated alignment technologies, and skilled optical networking professionals. Companies are strengthening software automation, predictive maintenance capabilities, and infrastructure partnerships to ensure operational consistency, improve long-term reliability, and maintain competitive differentiation in mission-critical communication environments.

AI-Powered Optical Link Optimization AI-assisted beam steering and adaptive optics are becoming standard in next-generation FSO systems, improving link stability by nearly 35% and reducing alignment downtime by approximately 30%. U.S. telecom operators are integrating predictive analytics into optical backhaul networks to maintain uninterrupted service during atmospheric fluctuations. Vendors are embedding machine learning into network controllers, enabling automated calibration, lowering maintenance requirements, and improving enterprise network availability while reducing field service interventions.

Hybrid RF-FSO Network Expansion Organizations are increasingly deploying hybrid RF-FSO architectures to strengthen communication resilience, with more than 45% of new enterprise optical deployments incorporating RF redundancy. This transition is accelerating following heightened focus on infrastructure resilience and critical communication continuity. Companies are expanding technology partnerships with telecom operators and defense agencies while redesigning network workflows to balance bandwidth, latency, and environmental adaptability across diverse operating environments.

Satellite Optical Communication Integration Growing deployment of low-Earth-orbit satellite constellations is accelerating demand for optical communication terminals, with optical inter-satellite links improving data transmission efficiency by over 40% compared with conventional RF architectures. Europe and the United States are prioritizing secure space-based communication infrastructure through government-supported programs. Equipment manufacturers are increasing investment in compact optical terminals, advanced photonics, and modular ground stations to support scalable satellite-terrestrial communication ecosystems.

Localized Manufacturing and Photonics Innovation Supply-chain diversification has encouraged manufacturers to regionalize production of optical components, reducing procurement lead times by approximately 25% while improving component availability by nearly 20%. Japan and Germany continue expanding precision photonics manufacturing capabilities to strengthen supply resilience. Companies are restructuring supplier networks, investing in integrated photonic technologies, and standardizing modular product designs, enabling faster deployment, improved operational flexibility, and stronger competitiveness across high-security communication applications.

Satellite platforms represent the leading segment of the Free Space Optics Communication Technology Market, accounting for an estimated 46% of global deployments due to their ability to deliver high-capacity communication across long distances without spectrum congestion. Increasing investment in low-Earth-orbit constellations, secure government communication networks, and optical inter-satellite links has reinforced demand. Major aerospace companies continue expanding optical payload development through strategic collaborations and integrated photonics innovation. Terrestrial platforms remain essential for metropolitan backhaul, enterprise campuses, and last-mile connectivity because of rapid deployment and lower civil infrastructure requirements. Airborne platforms are emerging as the fastest-growing segment as defense modernization, unmanned aerial systems, and high-altitude communication platforms gain strategic importance. Adoption of airborne optical communication has increased by nearly 28% across advanced defense programs, while terrestrial deployments continue representing approximately 38% of operational installations. Vendors are strengthening product portfolios through lightweight optical terminals, automated beam tracking, and modular communication systems, allowing customers to deploy scalable solutions across commercial, industrial, and defense applications while balancing performance and operational flexibility.

Tactical Military Applications remain the dominant application segment, representing approximately 32% of overall deployments due to increasing demand for secure, low-probability-of-intercept communications across defense operations. Governments are replacing conventional RF systems with optical communication links to improve security and bandwidth while minimizing spectrum dependency. Backhaul & Front-haul Connections continue to experience strong enterprise demand as telecom operators accelerate 5G infrastructure modernization. Data Center Interconnects and Enterprise Connectivity also maintain substantial adoption because they enable high-capacity transmission without extensive fiber construction. Inter-Satellite Communication is the fastest-growing application as commercial space operators and government agencies expand optical satellite networks. Deployment of optical satellite links has increased by approximately 30%, while Last-Mile Connectivity and Fiber Extensions continue gaining traction in underserved locations where rapid installation is operationally advantageous. Companies are expanding hybrid communication platforms, integrating AI-enabled network management, and strengthening strategic partnerships to address evolving customer requirements across broadband, industrial networking, disaster recovery, and temporary communication infrastructure.

Aerospace & Defense remains the largest end-user segment, contributing nearly 41% of market demand through extensive deployment of secure communication systems, satellite networks, and battlefield connectivity solutions. National security modernization initiatives in the United States, France, and Japan continue accelerating procurement of optical communication technologies. IT & Telecommunication follows as a major adopter, supported by expanding mobile backhaul, enterprise networking, and digital infrastructure projects. Together, these sectors account for more than 65% of overall deployment activity, encouraging manufacturers to prioritize high-capacity, software-defined optical networking solutions. IT & Telecommunication is emerging as the fastest-growing end-user category as operators expand dense urban connectivity and cloud infrastructure. Adoption within telecom infrastructure has increased by approximately 27%, while BFSI organizations are strengthening secure campus networking for high-value financial transactions. Automotive & Transportation and Media & Entertainment are steadily increasing implementation for intelligent transport systems and high-bandwidth broadcasting applications. Companies are responding through industry-specific product customization, ecosystem partnerships, managed service offerings, and integrated security capabilities that improve deployment efficiency and long-term customer retention.

North America accounted for the largest market share at 38.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 33.4% between 2026 and 2033.

North America remains the leading regional market, supported by mature telecommunications infrastructure, advanced defense modernization, and extensive deployment of optical wireless communication systems. The region contributes approximately 38.2% of global demand, with strong implementation across secure government communications, enterprise campuses, and hyperscale data center interconnects. Rapid 5G densification and increasing satellite communication investments continue accelerating optical backhaul deployment. More than 55% of new defense communication modernization initiatives incorporate optical communication capabilities to enhance bandwidth and security. Technology providers are expanding AI-enabled optical networking platforms, strengthening partnerships with satellite operators, and investing in integrated photonics manufacturing to improve deployment efficiency and network resilience.

United States Market Outlook: The United States serves as the technology and deployment hub for Free Space Optics communication through extensive defense procurement, commercial satellite programs, and digital infrastructure investments. Major aerospace contractors and telecom providers continue integrating optical wireless systems into secure communication networks, while hyperscale cloud operators expand optical interconnect capacity. More than 60% of North America's advanced optical communication projects originate in the United States, supported by Department of Defense modernization programs, growing low-Earth-orbit satellite activity, and increasing enterprise adoption of secure high-bandwidth networking solutions.

Europe accounts for approximately 27.6% of the global market, supported by advanced photonics manufacturing, industrial automation, and expanding secure communication infrastructure. Governments continue investing in sovereign digital capabilities and space-based optical communication technologies, while telecom operators deploy optical wireless systems to complement high-capacity broadband infrastructure. Nearly 35% of ongoing optical communication projects emphasize integration with satellite and industrial communication platforms. Companies are strengthening research partnerships, expanding precision photonics production, and developing software-defined optical networking technologies to improve reliability and support next-generation digital infrastructure across industrial sectors.

Germany Market Outlook: Germany leads the European market through its strong photonics industry, advanced industrial manufacturing base, and digital infrastructure modernization initiatives. Domestic technology companies continue developing precision laser communication components for enterprise and industrial applications, while Industry 4.0 programs accelerate secure factory networking. Approximately 30% of Europe's industrial photonics production capacity is concentrated in Germany, reinforcing its position as a strategic innovation center for advanced optical communication technologies.

Asia-Pacific is emerging as the fastest-growing regional market due to rapid expansion of telecommunications infrastructure, smart city development, and satellite communication investments. The region represents approximately 23.8% of global demand, with governments prioritizing high-speed connectivity across urban and remote locations. More than 40% of newly planned digital infrastructure programs in major economies include advanced optical communication technologies for secure, high-capacity connectivity. Equipment manufacturers are expanding regional production facilities, strengthening supply-chain localization, and investing in AI-enabled communication platforms to support increasing deployment requirements across enterprise, telecom, and public infrastructure applications.

China Market Outlook: China is the largest market within Asia-Pacific owing to extensive 5G deployment, expanding satellite communication capabilities, and large-scale smart infrastructure projects. Domestic manufacturers continue increasing production of optical communication equipment while research institutions advance integrated photonics technologies. More than 45% of the region's optical communication manufacturing capacity is concentrated in China, supported by national digital infrastructure initiatives and continuous investment in space communication technologies.

South America is steadily adopting Free Space Optics communication technologies to improve broadband availability, enterprise connectivity, and communication resilience where fiber deployment remains economically challenging. The region contributes approximately 5.4% of global demand, supported by telecommunications modernization and expanding digital transformation initiatives. Nearly 28% of rural connectivity projects are evaluating wireless optical solutions to accelerate deployment while minimizing civil construction requirements. Technology vendors are collaborating with regional telecom providers to introduce hybrid communication systems that improve network availability and reduce infrastructure deployment timelines despite ongoing investment constraints.

Brazil Market Outlook: Brazil leads the South American market through its large telecommunications sector, expanding enterprise digitalization, and increasing broadband infrastructure investments. National operators continue deploying optical wireless communication for metropolitan backhaul and industrial connectivity, particularly across logistics and energy operations. More than 50% of regional telecom infrastructure investments are concentrated in Brazil, creating favorable conditions for wider implementation of high-capacity optical communication technologies.

The Middle East & Africa market is gaining momentum as governments accelerate smart city programs, secure communication infrastructure, and digital economy initiatives. The region accounts for approximately 5.0% of global market demand, with increasing adoption across government, defense, energy, and telecommunications sectors. More than 30% of recently announced smart infrastructure projects include advanced wireless communication technologies to strengthen digital connectivity and operational resilience. Market participants are expanding strategic partnerships, local deployment capabilities, and integrated communication solutions to address growing requirements for secure, rapidly deployable networking infrastructure.

United Arab Emirates Market Outlook: The United Arab Emirates is the region's leading market due to ambitious smart city development, advanced digital government initiatives, and significant investment in telecommunications modernization. National operators continue implementing high-capacity communication infrastructure to support intelligent transportation, public safety, and enterprise connectivity. More than 35% of the Gulf region's smart infrastructure deployment projects are concentrated in the UAE, positioning the country as a strategic hub for advanced Free Space Optics communication technology adoption.

The market is characterized by competition between global laser communication specialists including Mynaric, Cailabs, BridgeComm, Tesat-Spacecom, and Transcelestial, established aerospace OEMs, and agile photonics innovators. The top five players collectively control approximately 48% of the market, while regional optical networking companies compete through niche deployments and customized solutions. Technology leadership outweighs price competition, with optical terminal performance improving by 30–40% and deployment timelines shortened by nearly 35% through modular architectures. Aerospace OEMs emphasize reliability and long-term contracts, whereas emerging innovators compete through rapid product development, software-defined networking, and hybrid RF-FSO integration. Companies increasingly pursue strategic partnerships with satellite operators, telecom providers, and defense agencies while expanding vertically into optical ground stations and integrated photonic components. Competition is shifting toward secure space-based optical networking and AI-enabled automation rather than standalone hardware. High certification requirements, precision manufacturing expertise, and extensive validation cycles remain significant entry barriers. Success depends on delivering scalable, interoperable, high-performance platforms supported by strong ecosystem partnerships, manufacturing capability, and continuous photonics innovation.

Mynaric AG

BridgeComm, Inc.

Tesat-Spacecom GmbH & Co. KG

Transcelestial Technologies Pte. Ltd.

LightPointe Communications, Inc.

fSONA Networks Corp.

Mostcom Ltd.

Wireless Excellence Limited (CableFree)

Astrolight

Ball Aerospace

Skyloom Global Corp.

Artificial intelligence, adaptive optics, and integrated photonics are redefining Free Space Optics communication performance across terrestrial and satellite applications. AI-powered beam acquisition and tracking reduce alignment errors by nearly 35%, while adaptive optics improve link stability by approximately 30% under atmospheric turbulence. More than 45% of advanced deployments now integrate intelligent control software to automate calibration, reduce maintenance requirements, and improve network availability. These technologies enable telecom operators, defense organizations, and satellite providers to maximize bandwidth while minimizing operational interruptions.

Integrated photonic chips and hybrid RF-FSO architectures are replacing conventional discrete optical assemblies. Compared with legacy optical terminals, next-generation photonic platforms reduce system size by nearly 40% while lowering power consumption by approximately 25%. Hybrid RF-FSO networks also improve communication availability by more than 20% during adverse weather conditions. Companies with strong photonics manufacturing capabilities and proprietary optical software gain significant competitive advantages through lower lifecycle costs, faster deployment, and improved scalability.

Between 2026 and 2028, optical inter-satellite networking, software-defined optical communication, and quantum-secure laser transmission will become strategic investment priorities. Adoption of optical communication terminals across commercial satellite constellations is expected to exceed 50% of newly deployed high-throughput systems, accelerating demand for automated networking platforms, advanced photonic integration, and intelligent communication infrastructure that delivers superior operational efficiency and long-term competitive differentiation.

May 2025 – Kepler Communications successfully validated SDA-compatible space-to-ground laser links using Cailabs optical ground station technology and TESAT SCOT80 terminals, demonstrating standardized optical data transmission across multiple scenarios. The achievement supports operational deployment of secure optical relay services. Source: www.cailabs.com

February 2025 – U.S. Electrodynamics (USEI) announced the commercial rollout of its DiamondLink global optical satellite communication service using Cailabs optical ground stations, becoming the first commercial provider of worldwide space-to-ground optical services. Business impact includes expansion of commercial optical SATCOM availability.

March 2025 – Rocket Lab announced its intention to acquire a controlling stake in Mynaric AG, strengthening its end-to-end space systems strategy by integrating laser communication terminals for air and space applications. The move enhances supply-chain control and satellite networking capabilities.

May 2025 – Astrolight secured €2.8 million in funding to accelerate development of laser communication technologies for satellite and terrestrial connectivity, expanding European optical networking innovation and strengthening commercialization of high-capacity wireless optical infrastructure.

This report provides a comprehensive assessment of the Free Space Optics Communication Technology Market across three platform types, thirteen application categories, and six end-user industries, delivering detailed analysis of deployment patterns, technology adoption, competitive positioning, and operational developments. The study evaluates demand across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining country-level investment trends, digital infrastructure expansion, and enterprise implementation strategies. It also assesses emerging areas including satellite optical networking, hybrid RF-FSO systems, adaptive optics, AI-enabled beam control, and integrated photonics.

The report combines market segmentation, regional benchmarking, company profiling, technology assessment, and competitive intelligence to support strategic decision-making between 2026 and 2033. It highlights adoption trends, deployment priorities, partnership activity, and evolving customer requirements while evaluating more than 12 major industry participants. The analysis enables stakeholders to identify expansion opportunities, strengthen competitive positioning, prioritize technology investments, optimize product development strategies, and respond effectively to changing communication infrastructure requirements across both established and emerging application segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 204.0 Million |

| Market Revenue (2033) | USD 1,838.5 Million |

| CAGR (2026–2033) | 31.63% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cailabs; Mynaric AG; BridgeComm, Inc.; Tesat-Spacecom GmbH & Co. KG; Transcelestial Technologies Pte. Ltd.; LightPointe Communications, Inc.; fSONA Networks Corp.; Mostcom Ltd.; Wireless Excellence Limited (CableFree); Astrolight; Ball Aerospace; Skyloom Global Corp. |

| Customization & Pricing | Available on Request (10% Customization Free) |