Reports

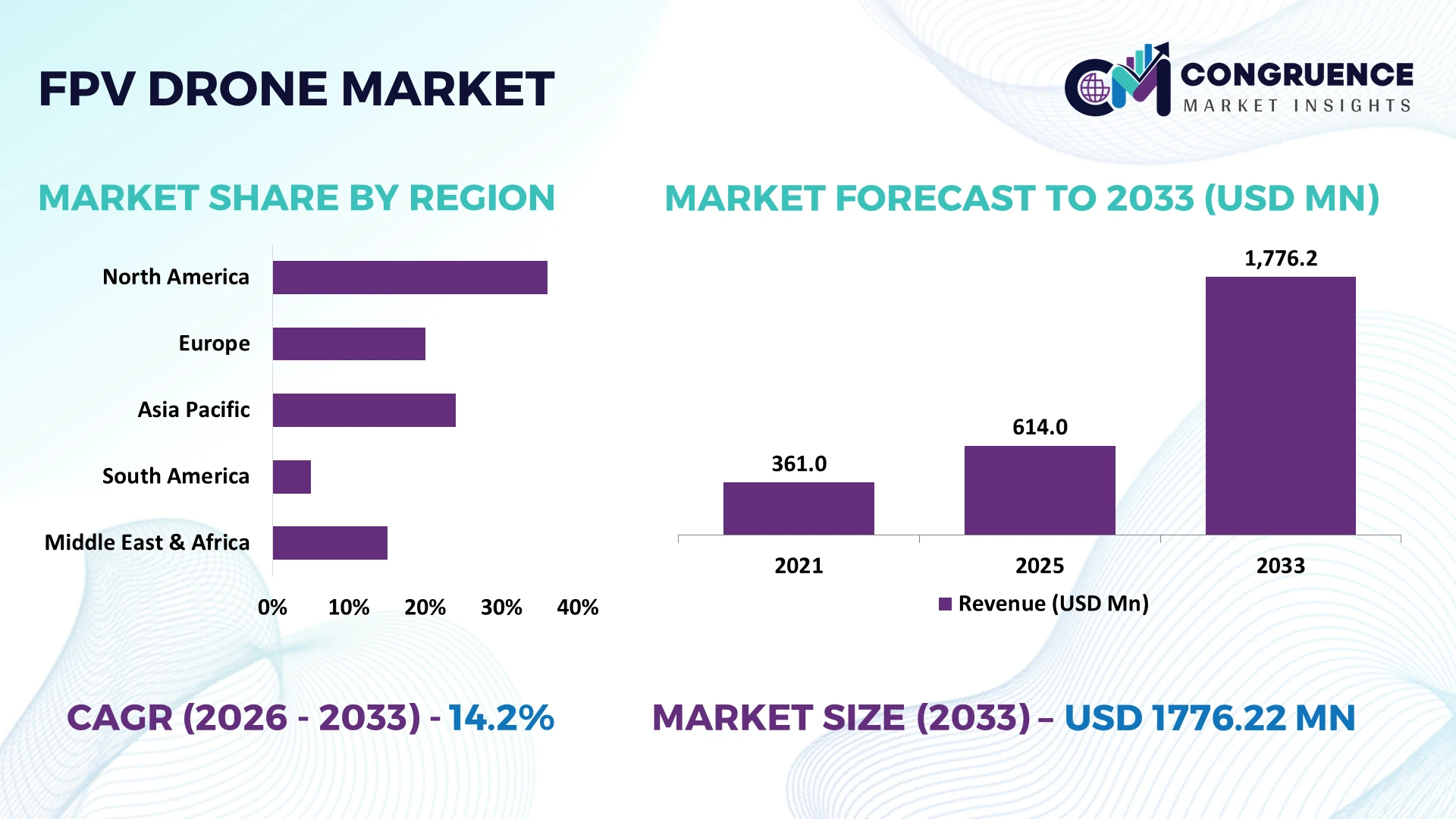

The Global FPV Drone Market was valued at USD 614 Million in 2025 and is anticipated to reach a value of USD 1776.22 Million by 2033 expanding at a CAGR of 14.2% between 2026 and 2033. Rapid deployment of AI-enabled flight control, secure digital video transmission, compact propulsion systems, and expanding defense, industrial inspection, and emergency response operations are accelerating adoption across advanced FPV drone applications.

China dominates the global FPV drone ecosystem with approximately 68% of manufacturing capacity, supported by vertically integrated electronics production and large-scale battery supply networks. The United States accounts for nearly 36% of advanced defense-oriented FPV drone deployments, while European manufacturers continue expanding localized production following geopolitical trade restrictions and export control measures introduced across critical technology supply chains. This manufacturing concentration and regional diversification are reshaping procurement strategies for commercial and government buyers.

Organizations prioritizing resilient component sourcing, intelligent flight capabilities, and localized manufacturing partnerships will secure stronger long-term competitive positioning.

Market Size & Growth: USD 614 Million in 2025 to USD 1776.22 Million by 2033 at a CAGR of 14.2%, driven by AI-enabled autonomous navigation and expanding defense modernization programs.

Top Growth Drivers: Defense applications contribute approximately 34% of demand, industrial inspection 27%, and precision agriculture 18%, supporting sustained global market expansion.

Short-Term Forecast: By 2028, autonomous mission efficiency is projected to improve by nearly 30%, while inspection costs decline by approximately 18% through intelligent automation.

Emerging Technologies: AI vision systems, edge computing, digital low-latency transmission, and lightweight carbon-fiber airframes improve operational performance by nearly 25%.

Regional Leaders: Asia-Pacific exceeds USD 760 Million through manufacturing leadership, North America approaches USD 470 Million through defense adoption, and Europe surpasses USD 330 Million with industrial automation investments.

Consumer & End-User Trends: More than 40% of enterprise users are integrating FPV drones into infrastructure inspection, energy asset monitoring, and emergency response operations.

Pilot Case Example: In 2026, AI-assisted utility inspection programs increased inspection productivity by approximately 35% while reducing manual field exposure across critical infrastructure.

Competitive Landscape: DJI leads with an estimated 28% global share alongside Autel Robotics, Skydio, Parrot, and BetaFPV, intensifying innovation across commercial and professional platforms.

Regulatory & ESG Impact: Updated operational standards improve flight safety compliance by over 20%, while regional supply-chain diversification strengthens manufacturing resilience amid global trade realignment.

Investment & Funding: More than USD 1.2 Billion has been directed toward autonomous software, production expansion, strategic partnerships, and regional manufacturing capabilities.

Innovation & Future Outlook: Autonomous swarm technology, AI-powered object recognition, secure communication architectures, and modular payload platforms are defining the next generation of high-performance FPV drones.

Demand for FPV drones continues to strengthen across defense surveillance, industrial asset inspection, emergency response, precision agriculture, and commercial mapping applications. Manufacturers are introducing AI-assisted navigation, digital low-latency communication systems, and modular payload platforms that improve operational efficiency by approximately 30%. At the same time, regional supply-chain diversification and evolving export control policies are encouraging localized production, creating a stronger foundation for long-term strategic expansion across the global FPV drone market.

FPV drones are becoming strategically important as governments and enterprises prioritize real-time situational awareness, autonomous inspection, and low-cost aerial intelligence across defense, energy, logistics, and public safety operations. Supply-chain restructuring following export restrictions on critical electronic components has encouraged manufacturers to localize production and diversify semiconductor sourcing, reducing procurement lead times by nearly 20% while improving component availability for mission-critical platforms.

Modern AI-assisted FPV drones complete infrastructure inspections approximately 35% faster than conventionally piloted aerial systems while reducing manual operational exposure by nearly 30% through autonomous navigation and intelligent obstacle avoidance. China continues to lead large-scale manufacturing through vertically integrated electronics ecosystems, whereas the United States emphasizes high-performance autonomous software and secure communication platforms for defense and industrial applications. Over the next two to three years, enterprise deployments are expected to increase by more than 25% as inspection automation, emergency response, and precision agriculture become standard operational practices.

A growing number of utility operators are deploying FPV drones for transmission-line inspections, reducing maintenance downtime while improving asset visibility across remote locations. In response, manufacturers are expanding AI software capabilities, forming battery technology partnerships, and establishing localized assembly operations to strengthen delivery resilience. Companies that combine autonomous intelligence, secure supply chains, and scalable production will establish lasting competitive advantages across high-value commercial and government markets.

Defense modernization programs, industrial inspection requirements, and autonomous infrastructure monitoring are reshaping FPV drone adoption across major economies. Defense-related procurement represents approximately 34% of operational demand, while industrial inspection applications account for nearly 27%, supported by AI-enabled navigation that improves mission efficiency by around 30%. The United States continues expanding unmanned aerial capabilities, while China strengthens domestic production through vertically integrated electronics manufacturing. In response, leading companies are increasing investments in autonomous flight software, lightweight composite platforms, and digital transmission technologies while forming strategic partnerships with defense contractors and industrial solution providers. This combination of operational capability and manufacturing expansion is creating sustainable competitive differentiation beyond conventional consumer drone markets.

The FPV drone market continues to face structural constraints from dependence on specialized semiconductor chips, optical sensors, and battery cells, with nearly 60% of critical electronic components concentrated within limited manufacturing ecosystems. Export restrictions and certification requirements have increased procurement timelines by approximately 20%, while compliance-related testing expenses continue rising across commercial deployments. These conditions directly affect production scalability, delivery consistency, and profitability for manufacturers serving regulated industries. Companies are responding by diversifying supplier networks, expanding localized assembly facilities, and securing long-term procurement agreements for strategic components. Increasing investment in alternative sourcing strategies is reducing operational vulnerability while improving supply continuity across high-priority defense and industrial programs.

Autonomous mission planning, AI-powered object recognition, and edge-based analytics are opening new commercial opportunities beyond traditional aerial imaging. Intelligent navigation systems improve inspection productivity by approximately 35%, while predictive maintenance software reduces operational downtime by nearly 22%. Japan and India are expanding digital infrastructure programs that support drone integration across utilities, transportation, and precision agriculture, creating demand for enterprise-grade autonomous platforms. Manufacturers are strengthening research partnerships, investing in modular payload architectures, and developing software ecosystems capable of supporting multiple industrial applications from a single platform. The strongest competitive advantage will belong to companies delivering integrated hardware, AI software, and cloud-enabled operational intelligence rather than standalone drone platforms.

Long-term market expansion depends on achieving secure, interoperable, and large-scale drone operations across complex commercial environments. More than 45% of enterprise operators identify cybersecurity and secure communication as primary deployment priorities, while integration with existing asset management systems increases implementation complexity by nearly 25%. Workforce shortages in autonomous flight operations and advanced drone analytics further constrain deployment consistency across large industrial projects. Companies must invest in secure communication architectures, operator training, AI validation frameworks, and standardized software integration to support enterprise-scale implementation. Organizations capable of combining cybersecurity, interoperability, and operational reliability will secure stronger positions as FPV drones become essential infrastructure intelligence platforms.

AI Flight Intelligence Expansion AI-assisted flight control is becoming a standard feature across enterprise FPV platforms, improving autonomous navigation accuracy by nearly 32% while reducing pilot intervention by approximately 28%. Growing certification requirements for beyond-visual-line operations are accelerating software integration, prompting manufacturers to expand AI partnerships and embed edge computing for faster mission execution and lower operational workloads.

Localized Manufacturing Networks Supply-chain restructuring continues to shift component sourcing beyond traditional manufacturing clusters, reducing procurement lead times by around 18% and lowering inventory risk by nearly 20%. Chinese producers are expanding overseas assembly capabilities while North American companies strengthen domestic supplier ecosystems, improving delivery reliability and reducing dependence on single-country electronic component sourcing.

Enterprise Inspection Workflow Integration Utilities, energy operators, and infrastructure owners are integrating FPV drones directly with digital asset management platforms, reducing inspection reporting time by approximately 35% and increasing maintenance planning efficiency by nearly 25%. Technology providers are responding through cloud-based analytics, automated reporting software, and strategic partnerships that simplify enterprise deployment across large operational networks.

Secure Communication Platform Adoption Rising cybersecurity expectations are accelerating deployment of encrypted digital transmission systems capable of reducing communication interference by approximately 30% while improving mission reliability by nearly 22%. Defense contractors and industrial solution providers are prioritizing secure software architectures, modular communication hardware, and long-term technology collaborations to strengthen operational resilience under evolving regulatory and security requirements.

Racing FPV drones remain the largest product category, accounting for approximately 33% of overall deployments due to their proven performance, lower acquisition costs, and mature manufacturing ecosystem. High-speed maneuverability, standardized component availability, and broad aftermarket support continue to make racing platforms the preferred choice for enthusiasts and professional pilot training. Cinematic FPV drones represent the fastest-growing segment as professional content production, tourism marketing, and commercial filmmaking increasingly demand stabilized, high-definition aerial footage. Manufacturers are introducing lighter airframes, AI-assisted stabilization, and modular camera integration to strengthen competitiveness across premium commercial applications.

Freestyle drones continue gaining popularity among experienced recreational users seeking greater maneuverability, while long-range platforms expand adoption across infrastructure inspection and remote monitoring where extended flight capability improves operational efficiency. Micro FPV drones remain strategically relevant for indoor inspection, education, and confined-space operations because of their compact design and lower operating costs. Companies are balancing investments between high-performance racing systems and enterprise-focused cinematic and long-range platforms to diversify product portfolios and address evolving commercial demand.

Defense remains the dominant application, representing approximately 38% of FPV drone deployments due to increasing requirements for tactical reconnaissance, intelligence gathering, and real-time battlefield awareness. Secure communications, autonomous navigation, and compact operational capability continue strengthening military procurement priorities. Inspection is the fastest-growing application as energy companies, utilities, and industrial operators automate infrastructure monitoring, reducing inspection cycles by approximately 35% while improving worker safety. Technology providers are integrating AI analytics and cloud-based reporting platforms to simplify large-scale enterprise deployment.

Surveillance applications continue expanding across border monitoring, disaster response, and public infrastructure protection, while aerial photography maintains steady demand through media production and commercial content creation. Drone racing remains a valuable innovation ecosystem that accelerates flight control technologies later adopted in commercial products. Manufacturers are scaling application-specific software, modular payload systems, and industry partnerships to improve operational flexibility while expanding their presence across both commercial and government procurement channels.

Defense organizations represent the largest end-user group with approximately 41% of FPV drone deployments, supported by continuous investments in tactical surveillance, reconnaissance, and secure operational capabilities. Large-scale procurement programs, specialized mission requirements, and sustained modernization initiatives maintain strong purchasing activity. Public Safety is the fastest-growing end-user category as emergency responders increasingly deploy FPV drones for disaster assessment, search-and-rescue operations, and rapid incident response, improving field assessment efficiency by approximately 30%. Manufacturers are expanding ruggedized product lines and encrypted communication capabilities to meet operational requirements.

Media & Entertainment continues driving demand for cinematic FPV systems capable of producing immersive aerial content, while Construction companies increasingly adopt drones for project monitoring and site documentation. Agriculture is strengthening adoption through crop surveillance and precision field assessment using intelligent imaging technologies. Companies are introducing customized solutions, industry-focused software ecosystems, and strategic service partnerships to address diverse operational requirements while strengthening long-term customer retention across specialized industry verticals.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a 15.4% CAGR between 2026 and 2033.

Defense-Led Innovation Accelerates Enterprise Deployment

North America remains a global innovation center for advanced FPV drone technologies, supported by defense modernization, industrial automation, and strong software development capabilities. The region represents approximately 28% of global market demand, driven by widespread adoption across military operations, infrastructure inspection, emergency response, and energy asset monitoring. AI-enabled autonomous navigation, encrypted communication systems, and cloud-connected fleet management continue improving operational efficiency. During 2026, several defense and industrial technology partnerships accelerated testing of next-generation autonomous drone platforms, reducing mission planning time by nearly 25%. Companies are prioritizing domestic manufacturing, advanced battery technologies, and secure software ecosystems to strengthen supply resilience while meeting increasingly stringent operational and cybersecurity requirements.

United States Market Outlook: The United States remains the largest FPV drone market in North America through its extensive defense procurement programs, advanced aerospace ecosystem, and enterprise technology leadership. More than 40% of enterprise drone deployments focus on defense, public safety, and infrastructure inspection, encouraging manufacturers to expand autonomous software development, secure communications, and localized production. Strong collaboration between defense contractors, AI developers, and drone manufacturers continues accelerating commercial technology transfer into industrial applications.

Regulatory Harmonization Supports Commercial Expansion

Europe continues strengthening its FPV drone ecosystem through harmonized aviation regulations, industrial automation, and increasing investment in digital infrastructure. The region contributes approximately 22% of global demand, supported by expanding deployment across utilities, construction, logistics, and public safety operations. Standardized certification frameworks are simplifying enterprise adoption while improving cross-border operational consistency. During 2026, industrial inspection programs using autonomous drone platforms improved maintenance productivity by approximately 28%, encouraging greater investment in intelligent flight technologies. Manufacturers are strengthening regional partnerships, localized assembly capabilities, and software integration to improve compliance while reducing operational complexity across commercial deployments.

Germany Market Outlook: Germany leads the European FPV drone market through its advanced manufacturing base, engineering expertise, and industrial digitalization initiatives. Enterprise users continue integrating drones into automotive production, energy infrastructure, and construction monitoring, while technology companies invest in AI-enabled navigation and industrial software platforms. Approximately 32% of commercial deployments are linked to industrial inspection and manufacturing support, reinforcing Germany's position as a regional technology leader.

Manufacturing Scale Drives Global Leadership

Asia-Pacific remains the largest FPV drone manufacturing and deployment hub, accounting for approximately 46% of the global market through integrated electronics production, battery manufacturing, and component supply chains. Strong manufacturing ecosystems enable competitive production costs while accelerating commercialization across consumer and enterprise applications. Export-oriented manufacturing continues expanding alongside investments in autonomous flight technologies and advanced imaging systems. During 2026, localized component production improved manufacturing efficiency by nearly 20%, helping producers strengthen delivery performance despite ongoing global supply-chain adjustments. Companies continue expanding production capacity, developing intelligent software platforms, and increasing strategic investments in advanced drone technologies.

China Market Outlook: China dominates the global FPV drone industry through vertically integrated electronics manufacturing, advanced battery production, and comprehensive supplier ecosystems. Approximately 68% of worldwide FPV drone manufacturing capacity is concentrated within the country, enabling rapid product innovation and large-scale exports. Domestic manufacturers continue investing in AI-powered flight systems, digital transmission technologies, and automated production facilities while expanding international manufacturing partnerships to improve supply-chain resilience.

Infrastructure Monitoring Expands Commercial Demand

South America is experiencing increasing FPV drone adoption across mining, agriculture, utilities, and infrastructure inspection as organizations seek greater operational efficiency in geographically dispersed environments. The region represents approximately 6% of global market activity, with deployment expanding through enterprise modernization and public infrastructure monitoring initiatives. Agricultural operators increasingly utilize FPV drones for precision field assessment, while mining companies integrate aerial inspection to improve worker safety and operational visibility. During 2026, enterprise drone programs reduced remote inspection time by approximately 24%, encouraging additional investment in autonomous monitoring technologies. Manufacturers are expanding distributor networks, regional service capabilities, and application-focused software to strengthen commercial adoption despite infrastructure and connectivity challenges.

Brazil Market Outlook: Brazil represents the largest FPV drone market in South America due to its extensive agricultural sector, mining operations, and expanding infrastructure development. Commercial organizations continue deploying drones for crop monitoring, asset inspection, and environmental surveillance, supported by growing investments in digital agriculture. Approximately 35% of enterprise deployments are associated with precision agriculture and industrial inspection, creating sustained demand for specialized FPV platforms.

Strategic Modernization Supports Deployment Growth

The Middle East & Africa is strengthening its FPV drone market through infrastructure modernization, defense capability enhancement, and expanding smart city initiatives. The region contributes approximately 5% of global demand while increasing adoption across energy facilities, border surveillance, construction, and emergency response operations. Government-backed digital transformation programs continue supporting drone integration into critical infrastructure management. During 2026, several smart infrastructure projects improved inspection efficiency by nearly 26% through autonomous aerial monitoring and AI-enabled analytics. Companies are establishing regional partnerships, expanding technical support capabilities, and introducing specialized enterprise platforms to address demanding environmental and operational conditions.

Saudi Arabia Market Outlook: Saudi Arabia leads regional FPV drone adoption through major infrastructure development programs, defense modernization initiatives, and large-scale industrial projects. Energy operators, construction companies, and government agencies continue expanding drone deployment for inspection, surveillance, and asset management. More than 30% of enterprise implementations are associated with infrastructure and energy operations, encouraging technology providers to establish local partnerships and strengthen long-term operational support capabilities.

The FPV Drone Market is shaped by competition between global technology leaders including DJI, Autel Robotics, Skydio, Parrot, and BetaFPV, regional manufacturers specializing in cost-efficient platforms, and enterprise solution providers focused on defense and industrial applications. The top five companies collectively control approximately 58% of the global market, while regional firms compete through localized production and faster customer support. Technology leadership remains the primary differentiator, with AI-enabled navigation improving mission efficiency by nearly 30% and secure digital transmission reducing communication latency by around 25%. Cost-focused manufacturers compete through vertically integrated supply chains that lower production expenses by approximately 18%. Companies are strengthening market positions through manufacturing expansion, AI software partnerships, modular platform development, and battery technology integration. The competitive landscape is shifting toward autonomous intelligence and supply-chain control as localization reduces dependency on imported components. High certification requirements, software capability, and component sourcing remain major entry barriers. Sustainable competitive advantage requires integrated hardware, intelligent software, secure supply chains, and rapid product innovation.

DJI

Autel Robotics

Skydio

Parrot

BetaFPV

iFlight

Holybro

GEPRC

EMAX USA

Walksnail

Caddx FPV

Rotor Riot

Team BlackSheep (TBS)

Autonomous flight intelligence is transforming FPV drone operations through AI-powered navigation, computer vision, edge processing, and real-time obstacle avoidance. Compared with conventional manually piloted systems, AI-assisted platforms improve mission completion efficiency by approximately 35% while reducing operator workload by nearly 30%. More than 45% of enterprise deployments now integrate autonomous flight software for infrastructure inspection, surveillance, and emergency response, enabling faster decision-making and improved operational consistency. Defense organizations and industrial operators benefit most from these intelligent capabilities because they require secure, repeatable, and highly accurate aerial operations.

Digital low-latency transmission, lightweight carbon-composite airframes, and modular payload architectures are becoming standard across professional FPV platforms. New digital communication systems reduce signal interference by approximately 28% compared with legacy analog technologies while improving image quality and operational reliability. Around 40% of newly introduced commercial platforms now support modular payload integration, allowing operators to switch between inspection, surveillance, mapping, and thermal imaging without replacing complete drone systems. This flexibility lowers lifecycle costs while improving asset utilization across multiple industries.

Between 2026 and 2028, AI-enabled swarm coordination, onboard edge analytics, secure communication protocols, and digital twin integration will become major competitive differentiators. Manufacturers investing early in intelligent software ecosystems, cybersecurity, and scalable autonomous platforms will strengthen enterprise adoption, reduce deployment complexity, and secure long-term competitive leadership as commercial and defense requirements become increasingly software-driven.

January 2024 DJI introduced the FlyCart 30 delivery drone globally, expanding its enterprise drone portfolio with a maximum payload capacity of 40 kg, strengthening industrial logistics and heavy-load aerial operations.

July 2025 Autel Robotics announced its strategic exit from the consumer drone business to concentrate on enterprise and professional platforms, discontinuing the EVO Nano and EVO Lite product lines while maintaining support until 2030. The shift refocused resources toward higher-value commercial markets. Source: (TechRadar)

April 2026 Skydio secured USD 110 million in Series F funding to accelerate U.S. drone manufacturing and autonomous technology development, reinforcing production capacity for defense, critical infrastructure, and public safety deployments. Source: (Skydio)

May 2026 DJI released findings from an independent security assessment covering its drone systems, reinforcing cybersecurity validation across enterprise platforms and supporting broader commercial and government adoption through strengthened data protection assurance. Source: (DJI Official)

The report provides comprehensive analysis across Racing, Freestyle, Cinematic, Long-Range, and Micro FPV drone segments, evaluating deployment patterns, technology adoption, and evolving product positioning. It examines applications including aerial photography, drone racing, surveillance, inspection, and defense while assessing demand across media & entertainment, defense, construction, agriculture, and public safety. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational trends, manufacturing concentration, enterprise adoption, and competitive positioning.

The study evaluates AI-enabled navigation, autonomous flight control, digital transmission systems, secure communications, edge computing, and modular payload technologies shaping next-generation FPV drones. It assesses competitive strategies across leading manufacturers, technology innovators, and enterprise solution providers while highlighting adoption trends exceeding 40% in industrial applications and increasing localization of manufacturing. The report supports investment decisions, product expansion strategies, partnership planning, competitive benchmarking, and long-term market positioning between 2026 and 2033 through actionable business intelligence and forward-looking operational insights.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 614 Million |

Market Revenue in 2033 | USD 1776.22 Million |

CAGR (2026 - 2033) | 14.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | DJI, Autel Robotics, Skydio, Parrot, BetaFPV, iFlight, Holybro, GEPRC, EMAX USA, Walksnail, Caddx FPV, Rotor Riot, Team BlackSheep (TBS) |

Customization & Pricing | Available on Request (10% Customization is Free) |