Reports

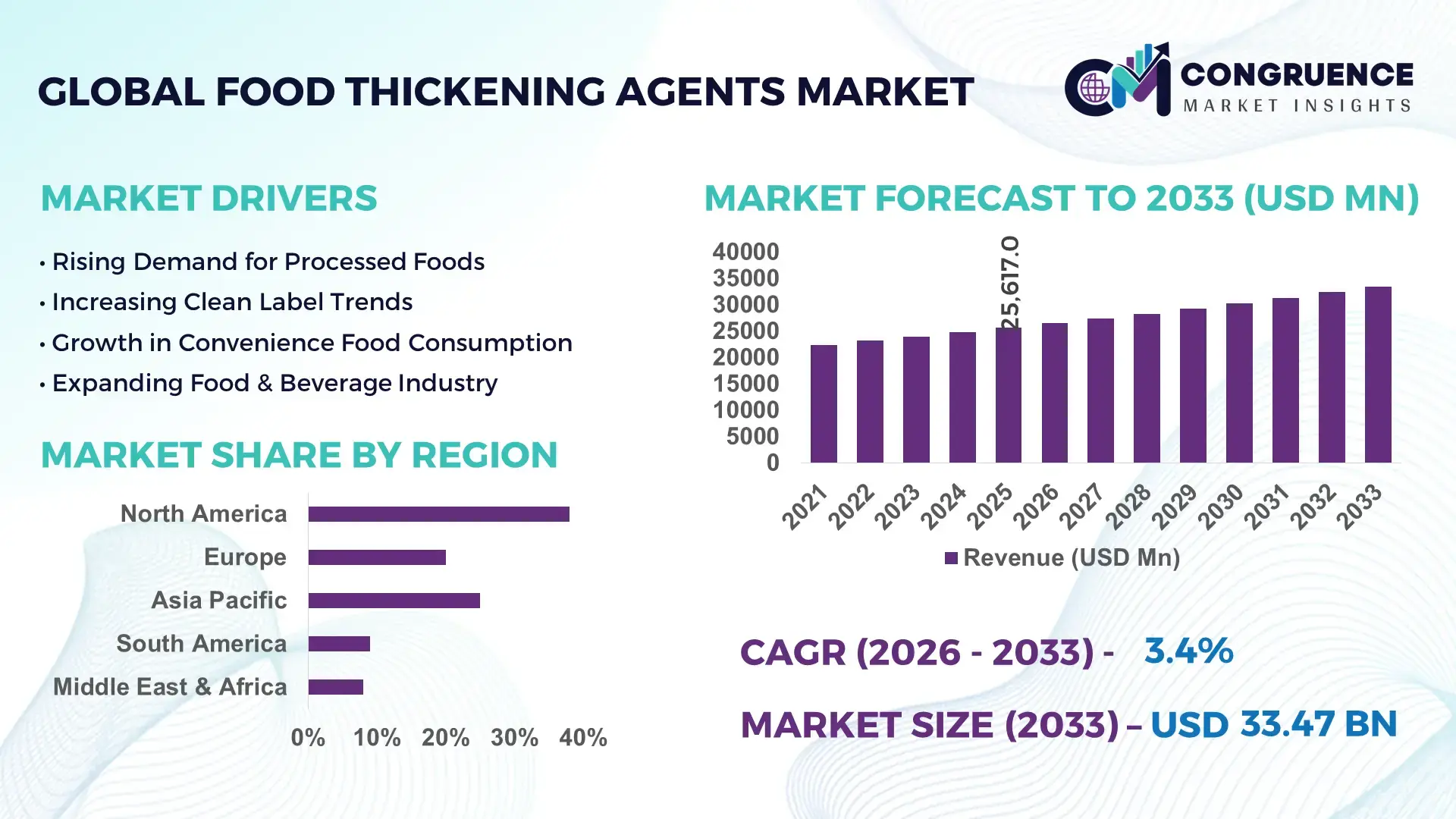

The Global Food Thickening Agents Market was valued at USD 25616.97 Million in 2025 and is anticipated to reach a value of USD 33472.81 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033. This growth is primarily driven by increasing demand for processed and convenience foods across urban populations.

The United States remains a dominant country in the food thickening agents market, supported by advanced food processing infrastructure and strong investment in ingredient innovation. The country accounts for a significant portion of industrial starch and hydrocolloid production, with over 60% of processed food manufacturers integrating stabilizers and thickeners into ready-to-eat meals, sauces, and dairy products. Investments exceeding USD 2 billion annually in food ingredient R&D have accelerated the development of clean-label thickening agents such as modified starches and plant-based gums. Additionally, nearly 75% of large-scale food processing facilities in the U.S. utilize automated blending systems for ingredient consistency, enhancing production efficiency and quality control.

Market Size & Growth: Valued at USD 25616.97 Million in 2025, projected to reach USD 33472.81 Million by 2033, growing at 3.4% CAGR due to rising demand for texture-enhanced food products.

Top Growth Drivers: Processed food consumption up by 35%, clean-label ingredient demand increased by 28%, plant-based product adoption surged by 32%.

Short-Term Forecast: By 2028, manufacturing efficiency in thickening agent production is expected to improve by 18% through automation and advanced formulation techniques.

Emerging Technologies: Enzyme-modified starch technology, microencapsulation techniques, and AI-driven formulation systems are transforming product development.

Regional Leaders: North America projected at USD 11 billion by 2033 with high processed food adoption; Europe at USD 9.2 billion driven by clean-label regulations; Asia-Pacific at USD 10.5 billion due to rising urban consumption trends.

Consumer/End-User Trends: Food manufacturers increasingly prefer natural hydrocolloids, with over 45% of new product launches incorporating plant-based thickeners.

Pilot or Case Example: In 2024, a European food processor achieved a 20% viscosity consistency improvement using enzyme-treated starch formulations.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including multinational ingredient manufacturers and regional suppliers.

Regulatory & ESG Impact: Over 40% of companies are adopting sustainable sourcing practices aligned with global food safety standards.

Investment & Funding Patterns: Recent investments exceeded USD 3.5 billion, focusing on bio-based thickening solutions and production capacity expansion.

Innovation & Future Outlook: Increasing integration of precision fermentation and plant-based innovation is expected to reshape the competitive landscape.

The food thickening agents market demonstrates strong integration across key sectors including bakery, dairy, beverages, and convenience foods, with dairy applications contributing nearly 30% of overall consumption. Recent advancements in hydrocolloid blends and starch modification technologies have enhanced product stability, shelf life, and texture optimization. Regulatory frameworks promoting clean-label ingredients and reduced chemical additives are influencing product innovation, particularly in Europe and North America. Asia-Pacific is witnessing rapid consumption growth due to urbanization and changing dietary patterns, with over 40% of processed food products incorporating thickening agents. Emerging trends such as plant-derived gums, sustainable sourcing, and functional ingredient innovation are expected to drive long-term market expansion while addressing evolving consumer preferences.

The strategic relevance of the food thickening agents market lies in its critical role in enhancing food texture, stability, and shelf life across a wide range of applications including dairy, bakery, sauces, and ready-to-eat meals. As global food supply chains evolve, manufacturers are increasingly leveraging advanced formulation technologies to meet consumer expectations for consistency and clean-label products. For instance, enzyme-modified starch technology delivers 25% higher viscosity stability compared to conventional chemically modified starch, enabling improved product performance under varying processing conditions.

From a regional perspective, Asia-Pacific dominates in volume due to large-scale food production, while Europe leads in adoption with over 55% of food manufacturers prioritizing natural and organic thickening agents. The market is also witnessing rapid digital transformation, where AI-driven formulation platforms are optimizing ingredient combinations and reducing development cycles. By 2028, such technologies are expected to improve formulation efficiency by up to 20%, significantly lowering production costs and waste.

Sustainability and compliance are becoming central to market strategies, with firms committing to measurable ESG targets such as 30% reduction in synthetic additive usage and increased reliance on renewable raw materials by 2030. In 2024, a leading food manufacturer in Germany achieved a 22% reduction in formulation costs and improved product consistency through AI-based ingredient optimization systems. Looking ahead, the food thickening agents market is positioned as a key pillar supporting resilient food systems, regulatory compliance, and sustainable product innovation, with strong alignment to evolving consumer preferences and environmental standards.

The increasing consumption of processed and ready-to-eat food products is a major driver for the food thickening agents market. Globally, over 60% of urban consumers rely on packaged foods due to time constraints and lifestyle changes, leading to higher demand for texture-enhancing ingredients. Thickening agents play a crucial role in maintaining consistency, mouthfeel, and shelf stability in products such as soups, sauces, and dairy items. In addition, the expansion of quick-service restaurants and food delivery platforms has further boosted demand, with nearly 45% of foodservice operators incorporating advanced thickening solutions to ensure product quality during transportation. The rise of frozen and instant food segments has also increased the need for stabilizers that can withstand temperature fluctuations, driving innovation in modified starches and hydrocolloid blends.

Volatility in raw material prices presents a significant restraint for the food thickening agents market, particularly for natural ingredients derived from agricultural sources. Key raw materials such as corn, cassava, and seaweed are subject to fluctuations due to climate conditions, geopolitical factors, and supply chain disruptions. For instance, global seaweed production experienced variability of up to 15% annually, impacting the availability and pricing of carrageenan. Similarly, starch prices have shown fluctuations of approximately 10–12% due to changes in crop yields and demand from biofuel industries. These inconsistencies affect production costs and profit margins for manufacturers, making it challenging to maintain stable pricing strategies. Additionally, reliance on imported raw materials in certain regions increases exposure to currency fluctuations and trade restrictions, further complicating supply chain management.

The growing demand for clean-label and plant-based food products presents significant opportunities for the food thickening agents market. Consumers are increasingly seeking products with natural ingredients and minimal processing, leading to a surge in demand for plant-derived thickeners such as pectin, agar, and guar gum. Currently, over 50% of new food product launches in developed markets emphasize clean-label claims, creating a favorable environment for innovation in natural thickening solutions. Furthermore, the expansion of vegan and vegetarian diets has driven the use of plant-based stabilizers in dairy alternatives, with plant-based milk products experiencing adoption growth of over 30% in recent years. Advances in extraction and processing technologies are also improving the functionality and scalability of natural thickeners, enabling manufacturers to meet rising demand while maintaining product quality.

Regulatory complexities and formulation challenges pose significant obstacles to the growth of the food thickening agents market. Different regions have stringent regulations regarding food additives, labeling requirements, and permissible usage levels, creating compliance challenges for global manufacturers. For example, variations in approval standards for hydrocolloids across regions can delay product launches and increase testing costs by up to 20%. Additionally, achieving the desired texture and stability while meeting clean-label requirements can be technically demanding, requiring extensive research and development efforts. Formulation constraints are particularly evident in reduced-fat and sugar-free products, where maintaining consistency without compromising taste or quality is difficult. These challenges necessitate continuous innovation and investment in advanced formulation technologies, increasing operational complexity for market participants.

• Accelerated Shift Toward Clean-Label and Natural Ingredients: The transition toward clean-label formulations has intensified, with over 52% of newly launched packaged food products incorporating natural thickening agents such as pectin, agar, and guar gum. Consumer preference surveys indicate that nearly 68% of global buyers actively check ingredient labels, pushing manufacturers to replace synthetic additives. In Europe, approximately 60% of food processors have reformulated at least one product line using plant-based thickeners, while North America has seen a 35% increase in organic hydrocolloid usage in the past three years.

• Technological Advancements in Starch Modification and Hydrocolloid Blends: Innovations in enzyme-modified starch and multi-functional hydrocolloid blends are improving product stability and texture consistency by up to 25% compared to traditional formulations. Around 40% of large-scale food manufacturers now deploy precision blending systems integrated with digital monitoring tools, reducing formulation variability by 18%. Additionally, microencapsulation techniques have enhanced shelf stability in processed foods by nearly 20%, particularly in dairy and frozen product segments.

• Expansion of Plant-Based and Alternative Protein Applications: The rapid growth of plant-based food products has significantly increased the demand for advanced thickening agents, with over 45% of plant-based dairy alternatives relying on specialized stabilizers. Global consumption of plant-based beverages has risen by 30%, necessitating improved viscosity control and mouthfeel enhancement. Manufacturers are increasingly using customized hydrocolloid systems, with adoption rates in alternative protein applications exceeding 38% across developed markets.

• Rising Adoption of Automation and AI in Ingredient Formulation: Digital transformation is reshaping formulation processes, with nearly 33% of leading ingredient manufacturers implementing AI-driven systems to optimize thickener combinations. These technologies have reduced product development cycles by 22% and improved formulation accuracy by 17%. In Asia-Pacific, over 50% of large food processing facilities have adopted automated dosing and mixing systems, enhancing production efficiency and reducing raw material wastage by approximately 15%.

The food thickening agents market is segmented based on type, application, and end-user industries, reflecting diverse functional requirements across the global food processing ecosystem. By type, the market includes starch-based thickeners, hydrocolloids, and protein-based agents, each offering distinct performance characteristics such as viscosity control, stability, and emulsification. Applications span across bakery, dairy, beverages, sauces, and convenience foods, with varying demand patterns driven by consumer preferences and regional dietary habits. End-user segmentation highlights the dominance of large-scale food manufacturers, followed by foodservice providers and small-scale processors. Notably, over 65% of industrial food production processes incorporate at least one form of thickening agent, underscoring their critical role in product formulation. Increasing demand for clean-label and plant-based products is further influencing segmentation trends, with natural and multifunctional ingredients gaining traction across all categories.

The food thickening agents market by type is primarily categorized into starch-based thickeners, hydrocolloids, and protein-based agents. Starch-based thickeners dominate the segment, accounting for approximately 48% of total adoption due to their cost-effectiveness, wide availability, and versatility across multiple food applications such as soups, sauces, and processed meals. Hydrocolloids, including xanthan gum, carrageenan, and guar gum, represent around 32% of the market, offering superior stability and functionality in complex formulations. Protein-based thickeners hold a smaller share of about 20%, primarily used in specialized applications such as dairy alternatives and nutritional products.

Hydrocolloids are the fastest-growing segment, expanding at an estimated CAGR of 5.2%, driven by increasing demand for clean-label and plant-based solutions. These ingredients provide enhanced viscosity control and stability under varying temperature and pH conditions, making them ideal for premium and functional food products. Meanwhile, starch-based thickeners continue to evolve through enzyme modification technologies, improving performance characteristics. Other niche segments, including cellulose derivatives and gelatin-based thickeners, collectively account for nearly 15% of the market, serving specific applications such as confectionery and processed meats.

The application segmentation of the food thickening agents market includes bakery and confectionery, dairy and frozen desserts, beverages, sauces and dressings, and convenience foods. Dairy and frozen desserts lead the segment with approximately 34% share, driven by the need for consistent texture, improved mouthfeel, and extended shelf stability in products such as yogurt, ice cream, and cheese spreads. Sauces and dressings account for around 26% of usage, where thickening agents are essential for viscosity control and emulsion stability.

Convenience foods represent the fastest-growing application segment, expanding at a CAGR of 5.8%, fueled by increasing urbanization and demand for ready-to-eat meals. These products require advanced thickening systems to maintain quality during storage and reheating processes. Beverage applications, including plant-based drinks and smoothies, contribute about 18% of the market, with growing demand for texture enhancement and suspension stability. Other applications, such as bakery and confectionery, collectively hold nearly 22% share, leveraging thickeners for moisture retention and structural integrity.

End-user segmentation in the food thickening agents market includes large-scale food manufacturers, foodservice providers, and small and medium-sized enterprises (SMEs). Large-scale food manufacturers dominate the segment, accounting for approximately 58% of total demand, due to their extensive production capacities and continuous need for consistent product quality across multiple product lines. These manufacturers rely heavily on advanced thickening systems to ensure uniformity and scalability in mass production.

Foodservice providers, including restaurants and catering businesses, represent around 27% of the market, utilizing thickening agents to maintain product consistency and quality in prepared meals. SMEs contribute approximately 15%, often focusing on niche and artisanal products with customized formulations. The SME segment is the fastest-growing, expanding at an estimated CAGR of 6.1%, driven by increasing demand for specialty and clean-label food products. These businesses are adopting innovative thickening solutions to differentiate their offerings and meet evolving consumer preferences. Collectively, foodservice and SME segments account for about 42% of total market demand.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

North America’s dominance is supported by high processed food consumption, where over 70% of packaged food products utilize thickening agents for texture and stability. Europe follows with approximately 28% share, driven by strict clean-label regulations and sustainability mandates influencing ingredient selection. Asia-Pacific holds nearly 26% of the market, with China, India, and Japan contributing over 65% of regional demand due to rapid urbanization and rising disposable incomes. South America accounts for around 6%, while the Middle East & Africa collectively contribute close to 4%, supported by expanding food processing industries. Globally, more than 68% of industrial food manufacturers integrate hydrocolloids or starch-based thickeners into production processes, with demand rising steadily across dairy, bakery, and convenience food segments.

How Are Advanced Food Processing Technologies Driving Ingredient Innovation?

North America holds approximately 36% of the global food thickening agents market, driven by a highly developed food processing sector and strong demand for convenience foods. Key industries include ready-to-eat meals, dairy processing, and beverage manufacturing, with over 72% of large-scale food producers incorporating thickening agents in product formulations. Regulatory frameworks emphasize food safety and clean-label compliance, with more than 60% of manufacturers reformulating products to eliminate synthetic additives. Technological advancements such as AI-based formulation systems and automated ingredient blending have improved production efficiency by nearly 20%. A notable regional player has invested in enzyme-modified starch solutions, enhancing viscosity performance by 18% in processed foods. Consumer behavior reflects a strong preference for organic and natural ingredients, with nearly 65% of consumers opting for clean-label products, influencing market expansion and product innovation.

What Factors Are Accelerating Demand for Sustainable Ingredient Solutions?

Europe accounts for around 28% of the global food thickening agents market, with key markets including Germany, the United Kingdom, and France contributing over 60% of regional consumption. Strict regulatory frameworks focused on food safety and sustainability have led to increased adoption of natural hydrocolloids, with over 58% of food manufacturers prioritizing plant-based thickeners. Regulatory initiatives promoting reduced chemical additives have influenced nearly 45% of product reformulations across the region. Advanced technologies such as precision fermentation and enzyme modification are being widely adopted, improving product stability by up to 22%. A leading European ingredient manufacturer has introduced biodegradable thickening solutions, reducing environmental impact by 15%. Consumer behavior shows a strong inclination toward transparency, with approximately 70% of consumers preferring products with clearly labeled natural ingredients, reinforcing demand for sustainable and compliant solutions.

Why Is Rapid Industrialization Transforming Ingredient Demand Patterns?

Asia-Pacific represents approximately 26% of the global food thickening agents market and ranks as the fastest-growing region in terms of consumption volume. Major markets such as China, India, and Japan collectively account for over 65% of regional demand, driven by increasing urban populations and expanding food processing industries. The region has witnessed a 40% rise in processed food production over the past five years, significantly boosting demand for thickening agents. Manufacturing trends include large-scale adoption of automated processing systems, with over 50% of facilities integrating digital technologies to enhance efficiency. Innovation hubs in countries like Japan are focusing on advanced hydrocolloid formulations, improving product consistency by 20%. A regional manufacturer has expanded production capacity by 25% to meet rising demand. Consumer behavior is influenced by affordability and convenience, with over 60% of urban consumers preferring ready-to-eat food products.

How Are Expanding Food Industries Supporting Ingredient Adoption Trends?

South America holds approximately 6% of the global food thickening agents market, with Brazil and Argentina accounting for nearly 70% of regional consumption. The growth is supported by expanding food processing infrastructure and increasing demand for packaged food products. Government initiatives promoting local agricultural production have improved raw material availability, with corn and cassava output increasing by over 12% in recent years. Trade policies encouraging exports have further strengthened market growth, with processed food exports rising by 15%. Technological adoption remains moderate, with around 35% of manufacturers integrating automated systems to improve efficiency. A regional food ingredient producer has introduced cost-effective starch-based thickeners, reducing production costs by 10%. Consumer behavior reflects a growing preference for affordable packaged foods, with nearly 55% of households relying on processed food products for daily consumption.

What Role Do Emerging Food Processing Investments Play in Market Growth?

The Middle East & Africa region accounts for approximately 4% of the global food thickening agents market, with countries such as the UAE and South Africa leading demand. The region is experiencing increased investment in food processing infrastructure, with production capacity expanding by nearly 18% over recent years. Demand trends are influenced by the growing hospitality and retail sectors, where over 50% of packaged food products require stabilizers and thickening agents. Technological modernization is gaining momentum, with approximately 30% of manufacturers adopting advanced processing equipment to enhance product quality. Trade partnerships and import policies have facilitated access to high-quality raw materials, improving supply chain efficiency by 12%. A regional supplier has focused on introducing halal-certified thickening agents, catering to local consumer preferences. Consumer behavior is driven by convenience and dietary requirements, with rising demand for processed and ready-to-cook food products across urban areas.

United States – 31% share in the Food Thickening Agents market, driven by high processed food consumption and advanced food manufacturing infrastructure.

China – 24% share in the Food Thickening Agents market, supported by large-scale production capacity and strong demand from expanding urban populations.

The food thickening agents market is moderately fragmented, with over 120 active global and regional players competing across diverse product categories such as starch-based thickeners, hydrocolloids, and protein-based agents. The top five companies collectively account for approximately 42% of the market, indicating a competitive yet moderately consolidated structure. Leading players are focusing on product innovation, strategic partnerships, and capacity expansion to strengthen their market positions. Over 35% of recent competitive strategies involve the development of clean-label and plant-based thickening solutions to meet evolving consumer preferences.

Mergers and acquisitions have increased by nearly 18% in the past three years, enabling companies to expand their geographic footprint and diversify product portfolios. Technological innovation remains a key differentiator, with more than 40% of major players investing in advanced formulation technologies such as enzyme-modified starch and precision fermentation. Additionally, around 30% of companies are integrating digital tools for supply chain optimization and production efficiency. Competitive intensity is further heightened by the presence of regional manufacturers offering cost-effective solutions, particularly in emerging markets, where pricing strategies and local sourcing play a critical role in market penetration.

Cargill Incorporated

Archer Daniels Midland Company

Ingredion Incorporated

Tate & Lyle PLC

Kerry Group

DuPont Nutrition & Biosciences

Ashland Global Holdings Inc.

CP Kelco

Darling Ingredients Inc.

Roquette Frères

Jungbunzlauer Suisse AG

Avebe U.A.

Technological advancements in the food thickening agents market are increasingly centered on improving functionality, sustainability, and processing efficiency. One of the most significant developments is enzyme-modified starch technology, which enhances viscosity stability by up to 25% under varying temperature and pH conditions. This advancement allows manufacturers to maintain consistent product texture in complex formulations such as ready-to-eat meals and frozen foods. Additionally, hydrocolloid blending technologies are enabling multi-functional performance, with optimized combinations improving water-binding capacity by nearly 30% and reducing syneresis in dairy products by 18%.

Digital transformation is playing a growing role, with approximately 35% of large-scale ingredient manufacturers adopting AI-driven formulation systems. These systems reduce development cycles by 20% and improve formulation accuracy by 15%, enabling faster product innovation. Automation technologies, including precision dosing and continuous mixing systems, have increased production efficiency by over 22% while minimizing raw material wastage by nearly 12%.

Emerging technologies such as microencapsulation are enhancing the stability and controlled release of thickening agents, improving shelf life in processed foods by up to 20%. Furthermore, advancements in plant-based extraction processes have increased yield efficiency of natural thickeners like pectin and guar gum by approximately 18%, supporting the shift toward clean-label products. Precision fermentation is also gaining traction, enabling the production of bio-based hydrocolloids with consistent quality and reduced environmental impact. Collectively, these innovations are reshaping the competitive landscape and enabling manufacturers to meet evolving regulatory and consumer demands with greater efficiency and sustainability.

• In March 2025, Ingredion Incorporated expanded its NOVATION® range of functional native starches, enhancing clean-label formulation capabilities for processed foods. The new variants improved texture stability by up to 20% and supported simplified ingredient labeling across multiple food applications. Source: www.ingredion.com

• In September 2024, Tate & Lyle PLC launched a new line of tapioca-based texturizers designed for plant-based dairy alternatives. These solutions demonstrated a 15% improvement in mouthfeel consistency and enabled manufacturers to replace modified starches with label-friendly ingredients. Source: www.tateandlyle.com

• In January 2025, Kerry Group introduced an advanced hydrocolloid system targeting ready-to-eat meals, delivering up to 18% improvement in viscosity control and thermal stability during reheating processes. The innovation supports growing demand for convenience foods with enhanced texture performance. Source: www.kerry.com

• In June 2024, Cargill Incorporated upgraded its pectin production facility to increase output efficiency by 12% and reduce water usage by 10%, aligning with sustainability goals while strengthening supply capacity for food thickening applications. Source: www.cargill.com

The scope of the food thickening agents market report encompasses a comprehensive evaluation of key segments, technologies, applications, and geographic trends shaping the industry. The report covers a wide range of product types, including starch-based thickeners, hydrocolloids, protein-based agents, and emerging bio-based alternatives, collectively used in over 70% of industrial food processing applications. It provides detailed segmentation across major application areas such as dairy, bakery, beverages, sauces, and convenience foods, where dairy and processed foods together account for more than 50% of total usage.

Geographically, the report analyzes five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with a focus on consumption patterns, production capabilities, and regional regulatory frameworks. Asia-Pacific is highlighted for its rapidly expanding manufacturing base, while Europe is emphasized for its stringent clean-label and sustainability regulations influencing product innovation.

The report also examines technological advancements such as enzyme modification, precision fermentation, and AI-driven formulation systems, which are improving efficiency and product performance by up to 25%. Additionally, it includes insights into emerging niche segments such as plant-based and organic thickening agents, which are gaining traction with over 50% of new product launches incorporating natural ingredients. Industry focus areas extend to supply chain optimization, raw material sourcing, and environmental sustainability, with more than 40% of manufacturers adopting eco-friendly production practices. This structured scope enables stakeholders to gain a holistic understanding of market dynamics, competitive positioning, and future growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, Tate & Lyle PLC, Kerry Group, DuPont Nutrition & Biosciences, Ashland Global Holdings Inc., CP Kelco, Darling Ingredients Inc., Roquette Frères, Jungbunzlauer Suisse AG, Avebe U.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |