Reports

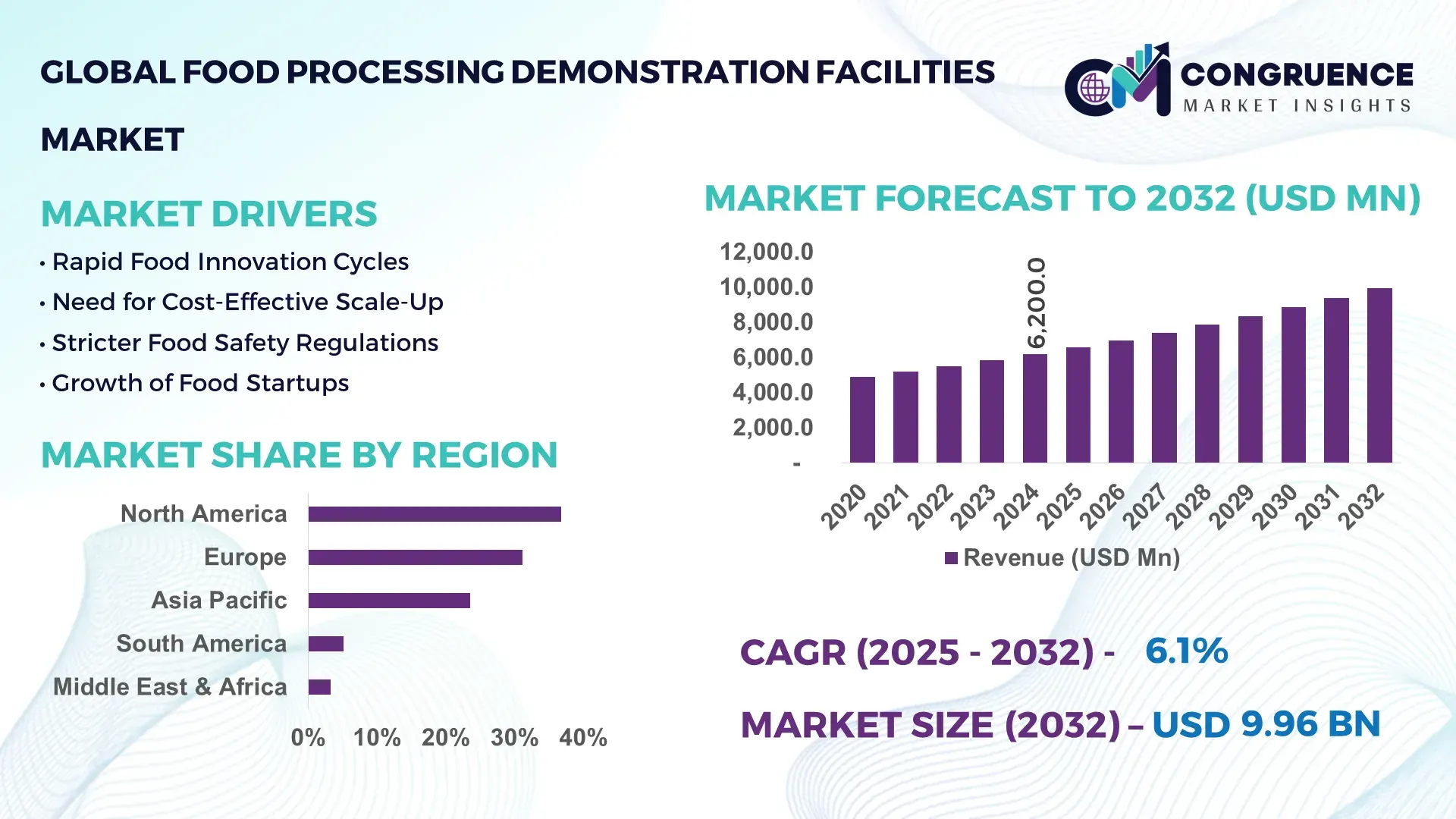

The Global Food Processing Demonstration Facilities Market was valued at USD 6,200.0 Million in 2024 and is anticipated to reach a value of USD 9,956.7 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. The market is driven by increasing demand for pilot-scale validation, faster commercialization of food innovations, and stricter regulatory compliance requirements.

The United States dominates the Food Processing Demonstration Facilities Market with a well-established food innovation ecosystem and extensive pilot infrastructure. The country operates more than 250 active food processing demonstration and pilot facilities linked to universities, federal research centers, and private manufacturers. Annual investment in food processing R&D infrastructure exceeds USD 4.5 billion, with approximately 18% allocated to pilot and demonstration facilities. These centers support applications across dairy, plant-based proteins, beverages, and functional foods, while adoption of automation, continuous processing, and digital twin technologies has increased processing validation efficiency by over 30%.

Market Size & Growth: Valued at USD 6,200.0 Million in 2024 and projected to reach USD 9,956.7 Million by 2032, growing at a CAGR of 6.1%, supported by faster pilot-to-commercial transitions.

Top Growth Drivers: Pilot facility adoption increased by 42%, process efficiency improved by 28%, and regulatory testing demand rose by 35%.

Short-Term Forecast: By 2028, operating costs are expected to decline by 22% due to automation and modular facility designs.

Emerging Technologies: Digital twins, AI-driven process optimization, and continuous thermal processing systems.

Regional Leaders: North America projected at USD 3,650.0 Million by 2032, Europe at USD 3,120.0 Million, and Asia Pacific at USD 2,480.0 Million, each driven by localized innovation adoption.

Consumer/End-User Trends: Food startups and mid-sized processors account for approximately 46% of facility utilization.

Pilot or Case Example: In 2023, a pilot dairy facility achieved a 31% reduction in formulation downtime through smart monitoring systems.

Competitive Landscape: Bühler Group leads with ~18% share, followed by Tetra Pak, GEA Group, SPX FLOW, and Alfa Laval.

Regulatory & ESG Impact: Facilities support food safety compliance while enabling 25–30% reductions in processing waste.

Investment & Funding Patterns: Recent investments exceeded USD 1.8 billion, with increasing public–private partnership models.

Innovation & Future Outlook: Smart analytics, modular processing lines, and scalable validation platforms are shaping future development.

Food Processing Demonstration Facilities support dairy (28%), plant-based foods (24%), beverages (18%), and bakery products (15%). Continuous processing systems and hygienic automation have improved pilot success rates by over 30%. Sustainability regulations, regional food security initiatives, and localized production models are influencing demand, while AI-enabled scale-up validation is shaping future growth.

Food Processing Demonstration Facilities are strategically critical for bridging laboratory research and commercial-scale food production. These facilities enable manufacturers to validate processing parameters, optimize cost structures, and ensure regulatory compliance before large-scale capital investments. Continuous processing technology delivers nearly 35% efficiency improvement compared to traditional batch processing systems. North America dominates in processing volume, while Europe leads in adoption, with nearly 48% of food enterprises utilizing demonstration facilities for product validation.

By 2027, AI-based process analytics are expected to reduce scale-up failure rates by 25% through predictive performance modeling. Companies are committing to ESG improvements such as 40% water reuse and 30% energy intensity reduction by 2030 within pilot operations. In 2024, Germany achieved a 27% reduction in validation time through digital twin deployment across multiple demonstration facilities. The Food Processing Demonstration Facilities Market is emerging as a pillar of operational resilience, regulatory readiness, and sustainable growth.

The Food Processing Demonstration Facilities Market is influenced by rapid food innovation cycles, regulatory scrutiny, and sustainability-driven processing requirements. Manufacturers increasingly depend on pilot-scale facilities to validate new formulations and technologies under real-world conditions. Collaboration among food producers, equipment suppliers, and research institutions is strengthening, while modular infrastructure and digital monitoring systems are enhancing operational flexibility across regions.

Shorter product life cycles and changing consumer preferences are increasing reliance on demonstration facilities. Over 60% of new food products now undergo pilot-scale validation to minimize commercial risk. These facilities help reduce development timelines by nearly 30% while ensuring compliance with food safety and quality standards. Growth in alternative proteins and functional foods further accelerates demand.

Establishing demonstration facilities requires high upfront investment, specialized equipment, and skilled technical staff. Average setup costs range between USD 15–20 million per facility. Ongoing compliance, energy usage, and maintenance expenses further limit adoption, particularly among small and mid-sized food manufacturers.

Sustainability-focused demonstration facilities are gaining traction. Pilot testing of energy-efficient processing, waste valorization, and water recycling has achieved waste reductions of up to 35%. Multinational food producers increasingly use these facilities to validate ESG-aligned processing models before commercialization.

Facilities must comply with diverse regional food safety regulations, increasing operational complexity. Integration of AI, automation, and data systems requires skilled personnel and standardized platforms. These challenges can extend implementation timelines and increase operational risk, particularly for multi-location facilities.

Rise in Modular and Prefabricated Construction: Modular construction is increasingly adopted, with 55% of new facilities reporting cost savings. Modular designs reduce construction time by up to 40% and improve scalability.

Growth of Digital Twin Implementation: Approximately 38% of facilities now use digital twins, improving process accuracy by 32% and reducing pilot failure rates by 24%.

Expansion of Alternative Protein Pilot Facilities: Nearly 41% of new projects focus on plant-based and alternative protein processing, with pilot throughput volumes increasing by 29%.

Increased Automation and Smart Monitoring: Automation adoption reached 46% in 2024, delivering 21% energy savings and 34% labor efficiency improvements.

The Food Processing Demonstration Facilities Market is segmented based on type, application, and end-user, each playing a distinct role in shaping adoption patterns and investment priorities. By type, pilot-scale facilities and modular demonstration units dominate usage due to their flexibility in testing formulations and processing parameters before commercial deployment. Application-wise, product development and process validation account for the largest utilization, reflecting rising demand for faster innovation cycles and regulatory compliance testing. From an end-user perspective, food manufacturers remain the primary users, followed by startups and research institutions leveraging these facilities for risk mitigation and scalability assessments. Segmentation trends indicate growing diversification, with sustainability testing, alternative protein processing, and smart manufacturing validation emerging as high-interest areas across regions.

Pilot-scale demonstration facilities represent the leading type in the Food Processing Demonstration Facilities Market, accounting for approximately 44% of total adoption, driven by their ability to replicate industrial processing conditions at lower operational risk. Modular and prefabricated demonstration facilities follow with nearly 29% share, offering faster installation and scalability advantages. However, mobile and containerized demonstration facilities are the fastest-growing type, expanding at an estimated 7.8% CAGR, supported by demand for decentralized testing and on-site validation near raw material sources. Fixed full-scale demonstration plants and hybrid facilities collectively contribute around 27% of market adoption, serving niche requirements such as continuous processing trials and regulatory certification.

Product development and formulation testing dominate application usage, representing approximately 38% of total facility utilization, as manufacturers increasingly validate taste, texture, and shelf-life before commercialization. Process optimization and scale-up validation follow closely with 31% share, supporting efficiency benchmarking and throughput optimization. Regulatory compliance testing and sustainability validation applications are expanding rapidly and collectively account for 31%, with sustainability-focused applications growing fastest at an estimated 8.1% CAGR, driven by water reuse, energy efficiency, and waste reduction mandates. In 2024, over 41% of food enterprises globally reported piloting demonstration facilities for clean-label and alternative protein products, while nearly 36% integrated these facilities into sustainability assessment workflows.

Large and mid-sized food manufacturers constitute the leading end-user segment, accounting for approximately 47% of facility utilization, due to their need for risk-controlled innovation and regulatory readiness. Food startups and scale-ups follow with 28% share, leveraging shared demonstration infrastructure to reduce capital exposure. Research institutions, contract processors, and government-supported innovation centers collectively contribute around 25%. Food startups represent the fastest-growing end-user group, expanding at an estimated 8.6% CAGR, fueled by increased venture-backed product innovation and demand for pilot validation prior to commercialization. In 2024, nearly 39% of food startups globally reported using shared demonstration facilities to validate processing feasibility, while over 33% of multinational food companies integrated pilot facilities into ESG-driven innovation programs.

North America accounted for the largest market share at 36.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

Europe followed North America with a 31.2% share, supported by strong regulatory-driven adoption, while Asia-Pacific captured 23.6% of global demand driven by expanding food manufacturing infrastructure. South America and the Middle East & Africa jointly accounted for 8.4% of the market, reflecting early-stage but accelerating adoption. Over 420 active food processing demonstration facilities are currently operational across the top three regions, with North America hosting nearly 160 facilities, Europe 145, and Asia-Pacific 115. Regional demand is influenced by food innovation intensity, regulatory testing requirements, sustainability mandates, and the scale of food manufacturing investments.

The region held approximately 36.8% of the global Food Processing Demonstration Facilities Market in 2024, making it the largest regional contributor. Demand is driven by dairy, plant-based proteins, beverages, and functional food industries, which collectively represent over 65% of facility utilization. Government-backed food innovation programs and updated food safety modernization frameworks have increased pilot validation requirements. Digital twins, AI-based process monitoring, and continuous processing systems are deployed in nearly 48% of facilities. A major regional equipment provider expanded modular pilot lines across multiple innovation hubs in 2024, enabling 30% faster scale-up validation. Consumer behavior reflects high enterprise adoption, with over 44% of mid-to-large food manufacturers integrating demonstration facilities into product development workflows.

Europe accounted for approximately 31.2% of global market share in 2024, led by Germany, the UK, and France, which together contribute over 62% of regional demand. Strong sustainability frameworks and food safety harmonization requirements are driving the need for validation facilities. More than 52% of European demonstration facilities now incorporate energy-efficient processing and waste minimization testing. Advanced automation and hygienic robotic handling systems are widely adopted. A leading European processing technology firm introduced standardized pilot modules in 2023, reducing validation timelines by 28%. Consumer behavior reflects regulatory-driven adoption, with enterprises prioritizing explainable, auditable processing validation over speed alone.

Asia-Pacific ranked third by market share at 23.6% in 2024 and represents the fastest-growing regional market by volume expansion. China, India, and Japan collectively account for nearly 71% of regional facility usage. Rapid expansion of food manufacturing parks, export-oriented processing units, and localized production models is fueling demand. Over 40% of new facilities commissioned since 2022 are located within industrial food clusters. Regional innovation hubs emphasize automation, smart sensors, and rapid throughput testing. A major Asian food conglomerate deployed mobile demonstration units across 12 production zones, reducing pilot setup costs by 26%. Consumer behavior shows strong growth driven by e-commerce food brands and rapid product localization.

South America accounted for approximately 5.1% of global market share in 2024, led by Brazil and Argentina, which together represent over 68% of regional adoption. Demand is tied to export-focused food processing, especially meat, grains, and beverages. Infrastructure upgrades and energy-efficient processing initiatives are increasing pilot testing requirements. Government incentives supporting food exports and regional trade agreements have accelerated facility usage. A Brazilian processing cooperative implemented shared demonstration facilities across 9 production centers, improving export compliance testing efficiency by 22%. Consumer behavior indicates demand linked to localization, labeling compliance, and regional language customization.

The Middle East & Africa accounted for approximately 3.3% of global demand in 2024, with UAE and South Africa leading regional adoption. Growth is supported by food security initiatives, industrial diversification programs, and import substitution strategies. Nearly 34% of facilities focus on shelf-life testing and packaging validation for hot climates. Technological modernization includes automation and cold-chain integration. A UAE-based food innovation center expanded pilot processing capacity by 18% in 2024 to support regional manufacturers. Consumer behavior reflects demand driven by urbanization, packaged food consumption, and halal-compliant processing validation.

United States – 24.5% Market Share: Strong pilot infrastructure density, high food R&D investment, and advanced regulatory validation requirements.

Germany – 14.8% Market Share: Advanced processing technology deployment, sustainability-focused validation, and strong industrial collaboration.

The Food Processing Demonstration Facilities Market is characterized by a moderately fragmented competitive structure, with a mix of global processing technology leaders, specialized pilot facility providers, and regional engineering firms. More than 60 active competitors operate globally, offering modular pilot plants, fixed demonstration units, and mobile validation systems. The top five companies collectively account for approximately 46–49% of total market activity, indicating moderate consolidation with strong competitive intensity.

Leading players compete primarily on technological depth, customization capability, automation integration, and regulatory compliance expertise rather than pricing alone. Strategic initiatives include cross-industry partnerships with food manufacturers, expansion of modular pilot platforms, and integration of digital twins and AI-enabled process monitoring. Between 2023 and 2024, over 35% of major players launched upgraded pilot solutions focused on sustainability validation, waste reduction testing, and energy optimization.

Mergers remain limited, while collaborative innovation agreements increased by nearly 28%, particularly between equipment suppliers and research institutions. Innovation competition is centered on reducing validation timelines by 25–35%, increasing pilot throughput efficiency by 30%, and enabling multi-product testing within a single facility footprint. The market favors companies with strong global service networks and the ability to support localized regulatory testing across multiple geographies.

SPX FLOW

JBT Corporation

Krones AG

Marel

FAM STUMABO

Heat and Control

Technology evolution is a core competitive differentiator in the Food Processing Demonstration Facilities Market. Modular and prefabricated processing systems are increasingly adopted, with over 55% of new facilities using modular layouts to reduce installation time by up to 40%. Digital twin technology is now implemented in approximately 38% of operational facilities, enabling real-time simulation, throughput optimization, and predictive maintenance testing.

Automation and smart sensor integration have reached nearly 46% penetration, improving labor productivity by 30–35% and enhancing data accuracy during pilot trials. Continuous processing technologies, including thermal, extrusion, and aseptic systems, are replacing batch setups in over 33% of new demonstration installations due to improved scalability and hygiene compliance.

Sustainability-focused technologies such as water reuse validation systems, energy-efficient heat recovery units, and waste valorization modules are increasingly embedded into pilot environments. Facilities testing circular processing models have achieved 25–35% waste reduction benchmarks. Advanced hygienic design, robotic handling, and AI-assisted quality inspection further strengthen validation accuracy.

Looking ahead, integration of AI-driven process optimization, cloud-based pilot data platforms, and interoperable control systems is expected to redefine demonstration facilities as strategic innovation assets rather than transitional infrastructure.

In June 2025, Tetra Pak opened its New Food Technology Development Centre in Karlshamn, Sweden, a dedicated pilot plant supporting biomass and precision fermentation-derived food producers to scale operations from prototype to commercial volumes. The facility offers modular fermentation and downstream process lines, plus tailored programmes for process evaluation and productivity validation to reduce investment risk and accelerate time to market. Source: www.tetrapak.com

In September 2025, GEA supplied a multipurpose pilot-scale beverage processing plant to Geisenheim University’s Beverage Technology Center, equipping the facility with flash pasteurization, CIP/SIP systems, carbonator, separator, and automated process controls to facilitate applied research and hands-on training in industrial beverage production processes. Source: www.gea.com

In March 2025, Fortifi Food Processing Solutions launched a global food processing machinery and automation platform, integrating brands and technologies across dairy, protein, and produce sectors to enhance processing productivity and worker safety for food manufacturers in over 15 countries.

In January 2025, Adani Wilmar Limited commenced operations at its consolidated food processing facility in Haryana, India, beginning shipment of 100 metric tonnes of rice as part of its expanded production capacity, marking a key milestone in modern processing infrastructure deployment.

The Food Processing Demonstration Facilities Market Report provides comprehensive coverage of pilot-scale and demonstration-level infrastructure used across the global food processing industry. The scope includes detailed analysis of facility types such as modular, fixed, mobile, and hybrid demonstration units, along with their functional capabilities and deployment models. The report evaluates applications spanning product formulation testing, process optimization, regulatory validation, sustainability assessment, and scale-up feasibility analysis.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with insights into facility density, industrial adoption patterns, and regional innovation priorities. The report further examines technology integration, including automation, digital twins, continuous processing systems, and sustainable processing modules.

End-user coverage includes large food manufacturers, mid-sized processors, startups, research institutions, and government-supported innovation centers, highlighting usage intensity and operational objectives. Emerging niches such as alternative protein pilot facilities, clean-label processing validation, and circular food processing models are also addressed.

Overall, the report is designed to support strategic planning, investment evaluation, technology benchmarking, and competitive positioning for decision-makers operating across food manufacturing, processing technology, and innovation infrastructure development.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 6,200.0 Million |

| Market Revenue (2032) | USD 9,956.7 Million |

| CAGR (2025–2032) | 6.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bühler Group, GEA Group, Alfa Laval, Tetra Pak, SPX FLOW, JBT Corporation, Krones AG, Marel, FAM STUMABO, Heat and Control |

| Customization & Pricing | Available on Request (10% Customization Free) |