Reports

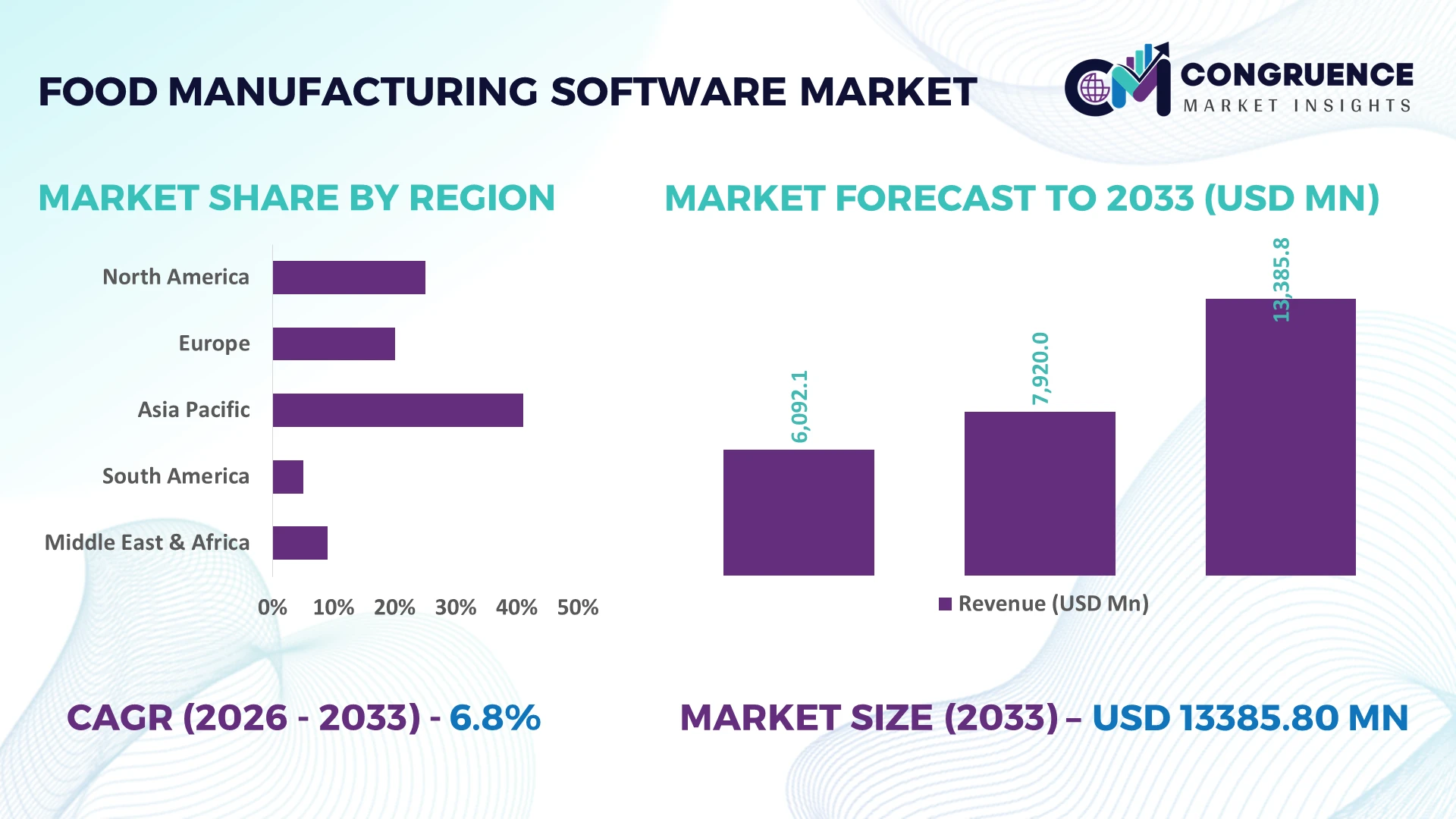

The Global Food Manufacturing Software Market was valued at USD 7920 Million in 2025 and is anticipated to reach a value of USD 13385.8 Million by 2033 expanding at a CAGR of 6.78% between 2026 and 2033. Growth is driven by AI-enabled production planning, stricter food traceability regulations, digital quality management, and cloud-based manufacturing execution systems improving operational efficiency across food processing facilities.

The United States dominates the global Food Manufacturing Software Market with approximately 34% market share, supported by over 38,000 food and beverage manufacturing facilities and sustained investments in smart factory modernization. AI-driven production scheduling and automated compliance platforms exceed 60% adoption among large manufacturers. Compared with Germany, where Industry 4.0 integration continues accelerating digital factory deployment, the U.S. benefits from larger enterprise-scale investments despite ongoing global supply-chain diversification following Red Sea shipping disruptions, reinforcing technology adoption across production networks.

The market favors software vendors delivering integrated, compliance-focused, AI-powered platforms that enhance operational resilience, traceability, and production efficiency across multinational food manufacturing enterprises.

Market Size & Growth: USD 7920 Million in 2025, reaching USD 13385.8 Million by 2033 at 6.78% CAGR, supported by AI-powered production planning and digital factory transformation.

Top Growth Drivers: AI deployment (+42%), cloud manufacturing adoption (+39%), and food traceability investments (+36%) accelerate enterprise software implementation.

Short-Term Forecast: By 2028, automated production scheduling reduces operational downtime by 18% while improving manufacturing efficiency by 22%.

Emerging Technologies: AI analytics, cloud MES platforms, and digital twin technology improve production visibility, predictive maintenance, and quality assurance.

Regional Leaders: North America exceeds USD 4.7 Billion, Europe approaches USD 3.6 Billion, and Asia-Pacific surpasses USD 3.2 Billion through smart manufacturing expansion.

Consumer/End-User Trends: More than 61% of large food manufacturers prioritize integrated ERP and quality management platforms for real-time production control.

Pilot/Case Example: In 2026, an AI-enabled production optimization deployment improved batch efficiency by 21% while reducing ingredient waste by 15%.

Competitive Landscape: Leading vendors collectively hold approximately 48% market share, with SAP, Oracle, Infor, Aptean, and Siemens maintaining strong enterprise presence.

Regulatory & ESG Impact: Digital compliance systems reduce documentation time by 35% while supporting stricter food safety and sustainability reporting requirements.

Investment & Funding: More than USD 2.3 Billion supports cloud modernization, strategic partnerships, AI integration, and manufacturing software expansion worldwide.

Innovation & Future Outlook: Generative AI, predictive quality analytics, and connected factory platforms strengthen resilient production amid global supply-chain realignment.

Growing investment in digital production management is strengthening demand across bakery, dairy, meat processing, beverage, and packaged food manufacturing operations. AI-enabled quality inspection, predictive maintenance, and cloud-native manufacturing platforms improve production accuracy, with automated workflows increasing operational productivity by nearly 20%. Evolving food safety compliance requirements and resilient supply-chain strategies continue shaping software innovation, setting the stage for deeper strategic market evaluation.

Food manufacturing software has become a strategic investment priority as processors modernize production, strengthen food traceability, and improve resilience against supply-chain disruptions. Stricter digital compliance requirements, factory automation, and real-time production intelligence are reshaping competitive positioning across the industry. Manufacturers increasingly integrate manufacturing execution systems, quality management, and enterprise resource planning into unified platforms to improve operational visibility and accelerate decision-making.

Cloud-native software platforms process production data up to 45% faster than conventional on-premise systems while lowering infrastructure maintenance costs by nearly 30% through centralized deployment and automated updates. The United States leads enterprise-scale implementation across multinational food manufacturers, whereas Japan emphasizes highly automated precision manufacturing supported by robotics and advanced factory digitization. Over the next two to three years, AI-assisted production scheduling is expected to exceed 55% adoption among large food processors as predictive analytics becomes a standard operational capability.

A global dairy manufacturer deploying AI-enabled production optimization can reduce ingredient waste while improving batch consistency through real-time monitoring and automated quality control. Software providers are expanding cloud infrastructure, strengthening cybersecurity capabilities, and forming technology partnerships to deliver integrated compliance platforms. Organizations establishing scalable, interoperable digital manufacturing ecosystems will secure stronger operational resilience, faster regulatory response, and sustainable competitive differentiation.

Food manufacturers are rapidly replacing fragmented production management systems with integrated software platforms that improve planning, compliance, and factory visibility. More than 62% of large processors now prioritize AI-enabled production optimization, while automated quality management reduces manual inspection workloads by approximately 35% and production scheduling improves equipment utilization by nearly 20%. The United States continues expanding smart manufacturing investments following stricter digital traceability expectations across food supply chains. This operational shift enables faster regulatory compliance and minimizes production losses. Software vendors are responding through AI innovation, cloud platform expansion, strategic partnerships with automation providers, and integrated analytics capabilities, creating stronger operational resilience and measurable productivity improvements across food manufacturing facilities.

Many food manufacturers continue operating legacy production systems that complicate enterprise software deployment and increase implementation costs. Around 47% of mid-sized processors report interoperability challenges between existing ERP, manufacturing execution, and quality management platforms, while implementation timelines often extend by more than 25% because of complex data migration requirements. Germany's highly diversified manufacturing base illustrates how legacy equipment slows digital integration despite advanced industrial capabilities. These structural limitations delay productivity improvements and increase operational complexity. Companies are mitigating risks by adopting phased cloud migration strategies, localizing implementation services, negotiating long-term technology contracts, and standardizing industrial communication protocols to improve deployment consistency.

AI-powered predictive analytics, digital twins, and edge computing create substantial opportunities to transform production efficiency beyond traditional manufacturing software capabilities. Intelligent production optimization can reduce material waste by approximately 18%, while predictive maintenance lowers unexpected equipment downtime by nearly 25%. India is emerging as an important deployment market as food processing modernization programs accelerate factory digitization and cloud adoption. Software providers are increasing investment in modular SaaS architectures, API-driven ecosystems, and industrial AI platforms that enable rapid implementation across multiple production sites. Companies building interoperable digital ecosystems today will capture long-term value through scalable automation, continuous optimization, and data-driven operational decision-making.

Expanding connected manufacturing environments significantly increases cybersecurity exposure and operational complexity across food processing facilities. Approximately 58% of industrial organizations identify cyber resilience as a top digital manufacturing priority, while nearly 40% report shortages of professionals capable of managing advanced manufacturing software platforms and industrial analytics. The growing adoption of connected factory infrastructure across the United States increases the need for secure real-time data exchange between production systems. Organizations must strengthen cybersecurity architecture, expand workforce training, and establish standardized governance frameworks. Technology providers are investing in secure cloud environments, industrial cybersecurity partnerships, and AI-assisted threat detection to ensure reliable long-term software deployment and operational continuity.

AI-Driven Production Intelligence: AI-enabled production analytics is becoming a standard capability across large food manufacturing facilities, with deployment increasing by approximately 42% and predictive scheduling improving line utilization by nearly 18%. Rising labor shortages in the United States and stricter digital traceability requirements are accelerating workflow automation. Software vendors are expanding machine-learning capabilities, integrating real-time shop-floor data, and strengthening industrial partnerships to improve production consistency while reducing manual intervention across multi-site manufacturing operations.

Cloud-Native Platform Expansion: Cloud deployment now accounts for more than 58% of new enterprise software implementations, reducing system maintenance costs by around 28% and accelerating software updates by nearly 35%. Multi-plant manufacturers increasingly replace isolated legacy applications with unified cloud environments to standardize operations. Enterprise providers are restructuring product portfolios around modular SaaS architectures, enabling faster deployment, simplified scalability, and centralized governance without disrupting ongoing production activities.

Integrated Compliance Automation: Digital compliance platforms are reshaping quality assurance as automated documentation reduces audit preparation time by approximately 40% while electronic batch records improve reporting accuracy by over 30%. Regulatory modernization across the European Union and export-focused manufacturing requirements encourage integrated quality management. Companies are embedding compliance workflows directly into production software, allowing quality teams to identify deviations earlier and minimize costly product recalls through continuous digital verification.

Connected Supply Chain Visibility: Manufacturers are integrating production planning with inventory and logistics platforms, improving inventory accuracy by nearly 22% and reducing raw material shortages by approximately 17%. Food supply-chain restructuring following global transportation disruptions has increased investment in end-to-end operational visibility. A notable shift is the growing use of supplier performance analytics alongside manufacturing software, prompting technology providers to expand ecosystem partnerships and deliver synchronized planning across procurement, production, and distribution networks.

ERP Software remains the dominant segment because it unifies production planning, procurement, finance, inventory, and compliance within a single enterprise platform, improving operational coordination across large manufacturing networks. Nearly 48% of enterprise food manufacturers prioritize ERP modernization as part of digital transformation initiatives, while integrated ERP deployments reduce administrative processing time by approximately 26%. Production Planning continues supporting scheduling optimization, Inventory Management strengthens raw material visibility, and Quality Management improves regulatory compliance through standardized digital workflows. Vendors are enhancing ERP platforms with AI capabilities and cloud integration to strengthen scalability and enterprise interoperability.

MES Software represents the fastest-growing segment as manufacturers require real-time production monitoring and equipment-level visibility. MES implementation improves production traceability by roughly 34% while reducing unplanned downtime by nearly 20%. Companies increasingly bundle MES with ERP and Quality Management platforms through strategic partnerships and modular deployment models, allowing phased digital transformation without disrupting production. Investment priorities are shifting toward integrated manufacturing ecosystems that connect operational technology with enterprise decision-making, creating stronger production intelligence and faster operational response.

Production Management accounts for the largest application share because manufacturers require centralized control over scheduling, resource allocation, production performance, and operational efficiency. Around 57% of digital transformation projects prioritize production management capabilities, while AI-assisted scheduling improves production throughput by approximately 19%. Quality Control remains a mature application driven by stricter food safety expectations, Inventory Tracking enhances warehouse accuracy, and Compliance Management supports continuous regulatory documentation. Vendors continue expanding integrated production platforms that combine planning, analytics, and execution within unified operational environments.

Supply Chain Management is the fastest-growing application as manufacturers respond to procurement volatility and distribution complexity. Digital supply-chain applications improve demand forecasting accuracy by nearly 24% while reducing inventory imbalances by approximately 18%. Companies are integrating logistics, procurement, and production data through cloud platforms while expanding automation capabilities across supplier networks. This operational convergence strengthens manufacturing agility, improves fulfillment performance, and enables more responsive production planning across increasingly diversified sourcing environments.

Food Processors represent the largest end-user segment because of extensive production complexity, diverse product portfolios, and continuous compliance obligations requiring integrated digital operations. Approximately 52% of large food processors have expanded enterprise manufacturing software deployment across multiple production facilities, while automated production planning reduces scheduling conflicts by nearly 21%. Beverage Manufacturers continue investing in production optimization and traceability, Dairy Producers prioritize quality assurance and batch control, and Bakery Companies increasingly adopt cloud-based manufacturing platforms to improve operational consistency. Technology providers are strengthening industry-specific functionality through configurable software modules and enterprise partnerships.

Meat & Poultry Processors constitute the fastest-growing end-user segment as stricter traceability requirements, export compliance, and cold-chain monitoring increase digital manufacturing investment. Automated quality and production systems improve processing visibility by approximately 32% while reducing documentation workloads by nearly 27%. Companies are responding with specialized compliance solutions, flexible pricing models, and integrated analytics tailored to high-volume processing environments. Competitive positioning increasingly depends on delivering scalable platforms capable of supporting complex production workflows and evolving food safety standards.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 7.9% CAGR between 2026 and 2033.

Integrated Smart Manufacturing Strengthens Enterprise Competitiveness

North America maintains the leading position through extensive digitalization across food processing, beverage manufacturing, and packaged food production. Nearly 65% of large food manufacturers operate integrated ERP and manufacturing execution platforms to improve traceability, production planning, and regulatory compliance. Cloud-native deployments continue replacing legacy software, while AI-enabled production analytics improve factory utilization and operational responsiveness. Technology providers are expanding strategic partnerships with industrial automation firms to deliver unified manufacturing ecosystems. Ongoing modernization of processing facilities and investment in connected factory infrastructure reinforce the region's leadership in enterprise software deployment.

United States Market Outlook: The United States remains the regional growth engine due to its extensive food processing infrastructure, advanced cloud adoption, and strong investment in industrial automation. More than 38,000 food manufacturing facilities increasingly deploy AI-enabled manufacturing software to strengthen production scheduling, digital quality management, and inventory optimization. Enterprise software vendors continue expanding industry-specific platforms and cybersecurity capabilities, enabling large manufacturers to standardize operations across multiple production locations while improving compliance and operational resilience.

Regulatory Digitalization Drives Manufacturing Modernization

Europe continues strengthening digital manufacturing through strict food safety regulations, sustainability initiatives, and Industry 4.0 implementation. Approximately 58% of large manufacturers have expanded digital production management capabilities, while automated compliance workflows reduce documentation efforts by nearly 35%. Manufacturers increasingly integrate production planning with quality management to support export competitiveness and operational transparency. Enterprise software providers continue enhancing cloud deployment, interoperability, and advanced analytics to address evolving regulatory requirements while supporting highly automated manufacturing environments.

Germany Market Outlook: Germany leads regional implementation through its advanced industrial base, highly automated manufacturing sector, and strong Industry 4.0 ecosystem. Large food manufacturers increasingly integrate manufacturing execution systems with enterprise software, improving production visibility and equipment utilization across complex facilities. Continued investment in factory automation, industrial connectivity, and intelligent production management strengthens Germany's position as the primary innovation hub for digital food manufacturing operations.

Industrial Expansion Accelerates Digital Factory Deployment

Asia-Pacific is experiencing the fastest operational transformation as food processing capacity expands alongside industrial automation and cloud manufacturing adoption. Around 44% of new enterprise software deployments target expanding production facilities, while AI-assisted manufacturing platforms improve production efficiency by approximately 20%. Governments and private manufacturers continue investing in food processing modernization, digital quality assurance, and connected factory infrastructure. Software companies are expanding regional partnerships and localized cloud platforms to support rapidly growing manufacturing ecosystems and increasingly diversified supply chains.

China Market Outlook: China remains the region's largest market due to its extensive food manufacturing base, large-scale factory modernization, and accelerating smart manufacturing initiatives. Digital production management, automated quality inspection, and integrated enterprise platforms continue expanding across high-volume processing facilities. More than half of newly modernized food manufacturing plants incorporate cloud-connected production management systems, supporting improved productivity, export competitiveness, and standardized manufacturing performance throughout the country's industrial network.

Food Export Modernization Expands Digital Adoption

South America is steadily increasing software deployment as export-oriented food manufacturers modernize production operations and strengthen traceability capabilities. Approximately 39% of enterprise implementation projects focus on integrated production management and compliance systems to improve operational transparency. Cloud-based manufacturing platforms are gaining preference because they reduce infrastructure complexity while supporting distributed production facilities. Technology vendors continue expanding implementation partnerships and localized support services to address varying digital maturity levels while improving enterprise software accessibility across major food processing industries.

Brazil Market Outlook: Brazil leads regional demand through its globally competitive food processing sector, extensive agricultural value chain, and expanding investment in digital manufacturing technologies. Large processors increasingly deploy integrated manufacturing software to optimize production scheduling, inventory visibility, and regulatory reporting. Enterprise technology providers continue introducing localized solutions and implementation partnerships that support scalable deployment across Brazil's diversified food manufacturing ecosystem while strengthening export readiness and operational efficiency.

Industrial Diversification Supports Manufacturing Digitalization

The Middle East & Africa market is advancing through food security initiatives, industrial diversification strategies, and investment in modern food processing infrastructure. Around 33% of newly established processing facilities incorporate digital manufacturing management systems during initial deployment, improving production control and operational consistency. Governments continue encouraging industrial modernization through technology investment and advanced manufacturing programs. Software providers are expanding regional implementation capabilities, cloud infrastructure, and automation partnerships to support efficient factory operations across emerging food manufacturing hubs.

Saudi Arabia Market Outlook: Saudi Arabia represents the strongest national opportunity through sustained investment in food manufacturing expansion, industrial diversification, and smart factory development. Food producers increasingly implement integrated production management, quality control, and compliance software to strengthen domestic manufacturing capabilities. Government-backed industrial modernization programs continue accelerating enterprise technology adoption, while manufacturers invest in automated production environments that improve traceability, operational efficiency, and long-term manufacturing competitiveness.

The competitive landscape is shaped by SAP, Oracle, Infor, Aptean, Siemens, and specialized manufacturing software providers competing for enterprise food processors, while regional vendors target mid-sized manufacturers through lower implementation costs and localized support. The top five companies collectively control approximately 49% of the market, creating intense competition between global platform providers and agile industry-focused developers. Technology integration, deployment speed, and regulatory functionality determine market positioning, with AI-enabled production planning improving operational efficiency by nearly 20% and cloud implementations reducing maintenance costs by around 28%. Vendors increasingly compete through cloud expansion, strategic automation partnerships, industry-specific product development, and integrated ERP-MES ecosystems rather than pricing alone. Competition is shifting toward unified digital manufacturing platforms combining predictive analytics, traceability, cybersecurity, and compliance management, accelerating consolidation around comprehensive enterprise solutions. High implementation complexity and deep operational integration create substantial entry barriers. Winning requires scalable cloud architecture, advanced AI capabilities, rapid deployment, strong compliance functionality, and long-term customer integration strategies.

SAP

Oracle

Infor

Aptean

Siemens

Plex Systems

Epicor

IFS

Microsoft

QAD

Sage

Deskera

Current technology investment centers on AI-powered production planning, cloud-native ERP, manufacturing execution systems, and digital quality management. More than 60% of large food manufacturers prioritize integrated software platforms that connect production, inventory, and compliance through real-time data exchange. AI-assisted scheduling improves equipment utilization by approximately 22%, while predictive maintenance lowers unplanned downtime by nearly 25%. Compared with legacy on-premise software, cloud-based manufacturing platforms reduce infrastructure maintenance costs by around 30% while enabling significantly faster enterprise-wide software deployment and standardized operational governance.

Emerging technologies include digital twins, edge computing, computer vision inspection, and industrial IoT integration that strengthen production visibility and process optimization. Adoption of AI-enabled quality inspection has exceeded 40% among large multinational processors, reducing manual inspection workloads by nearly 35%. Enterprise manufacturers benefit most because integrated operational technology and information technology environments enable continuous production optimization, faster regulatory reporting, and more accurate demand planning across multiple manufacturing facilities.

Between 2026 and 2028, generative AI, autonomous production optimization, and connected supplier ecosystems will redefine manufacturing software competitiveness. Vendors expanding interoperable platforms, cybersecurity capabilities, and industrial automation partnerships will strengthen market leadership. Companies investing now in modular cloud architectures and unified data environments will accelerate decision-making, improve production resilience, shorten implementation cycles, and establish durable competitive advantages as digital manufacturing ecosystems become the operational standard across global food processing industries.

February 2026 Oracle introduced new process manufacturing capabilities within Oracle Fusion Cloud Supply Chain & Manufacturing, strengthening recipe, formula, and batch execution management in one platform for regulated food producers. The unified architecture improves real-time production visibility across 100% of connected manufacturing workflows, accelerating compliance and operational control. Source: qualityassurancemag.com

March 2026 Scapta expanded its partnership with Aptean to accelerate deployment of Aptean Food & Beverage ERP across Belgium and the Netherlands. The collaboration builds on Scapta's experience delivering more than 50 SaaS ERP projects, increasing implementation capacity and strengthening digital transformation for food and beverage manufacturers. Source: ictrl.com

September 2025 Aptean launched its Foundation Bundle for Food & Beverage ERP in the Benelux market, introducing a standardized cloud deployment model integrated with Microsoft AI Copilot. The solution delivers one standardized implementation package, enabling faster deployment, stronger traceability, and improved scalability for small and mid-sized food manufacturers. Source: aptean.com

September 2025 SAP announced that Nilons Enterprises adopted RISE with SAP to modernize its food processing operations through a unified cloud ERP platform connecting procurement, manufacturing, compliance, and finance. The deployment supports more than 300 users across multiple locations, improving operational visibility and enterprise-wide decision-making. Source: news.sap.com

This report provides a comprehensive assessment of the Food Manufacturing Software Market between 2026 and 2033, covering enterprise software adoption, digital manufacturing strategies, competitive positioning, technology evolution, and operational transformation. The analysis evaluates five major solution types, five core application areas, and five primary end-user categories while assessing deployment patterns, cloud migration trends, AI integration, and enterprise modernization priorities. Regional evaluation spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level strategic insights.

The report examines competitive dynamics across leading software providers, integrated manufacturing platforms, and emerging digital ecosystems while highlighting adoption patterns exceeding 60% among large enterprises for cloud-enabled manufacturing solutions. It delivers actionable intelligence on production optimization, compliance management, supply-chain integration, industrial automation, and cybersecurity priorities, enabling stakeholders to strengthen investment planning, product expansion strategies, partnership decisions, market entry evaluation, and long-term competitive positioning across both mature and emerging food manufacturing markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 7920 Million |

Market Revenue in 2033 | USD 13385.8 Million |

CAGR (2026 - 2033) | 6.78% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | SAP, Oracle, Infor, Aptean, Siemens, Plex Systems, Epicor, IFS, Microsoft, QAD, Sage, Deskera |

Customization & Pricing | Available on Request (10% Customization is Free) |