Reports

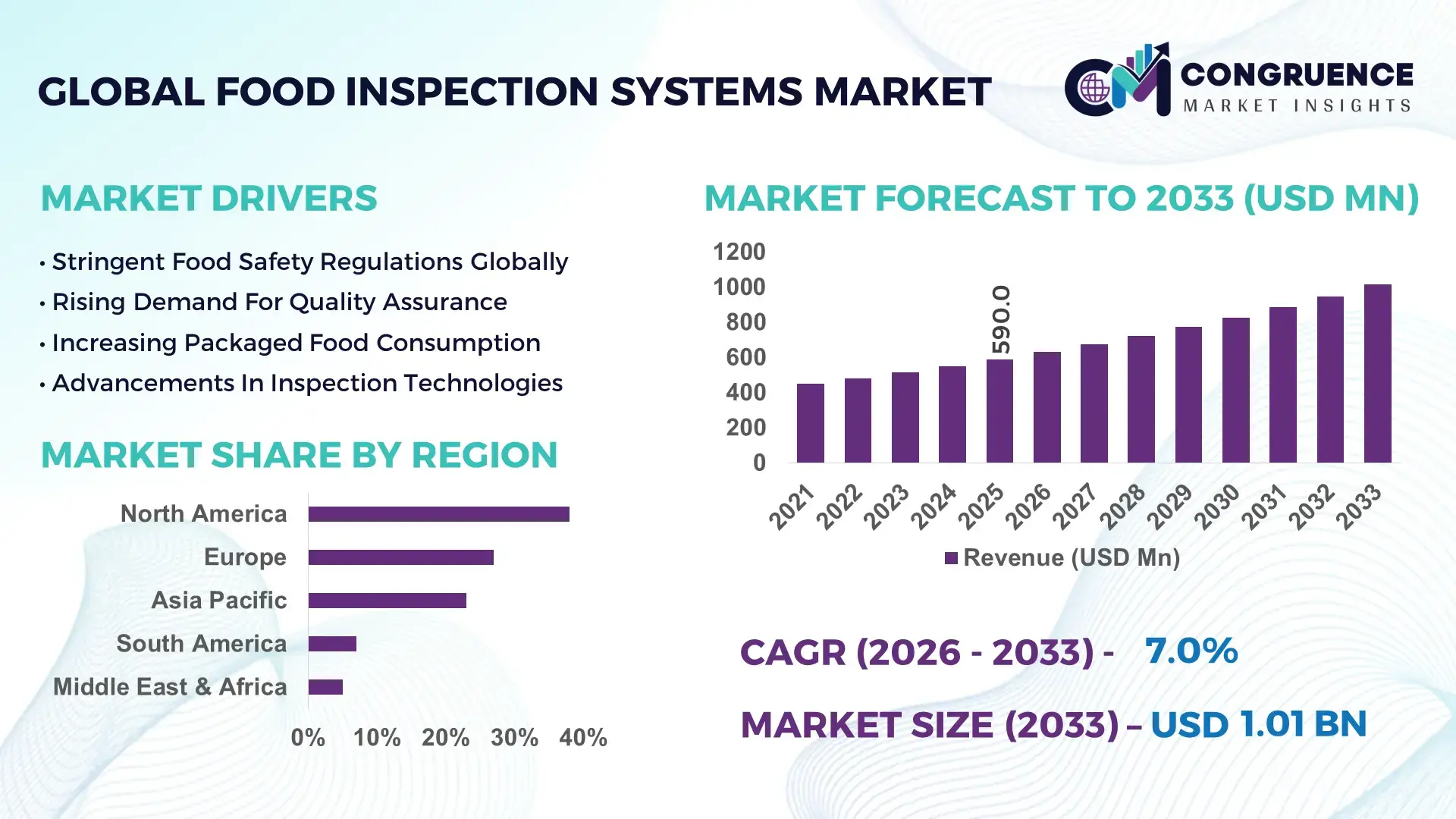

The Global Food Inspection Systems Market was valued at USD 590.0 Million in 2025 and is anticipated to reach a value of USD 1,013.7 Million by 2033 expanding at a CAGR of 7.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing regulatory compliance requirements and rising demand for automated food safety solutions across processing industries.

The United States dominates the Food Inspection Systems Market with advanced production capabilities and strong technological adoption across food processing industries. The country operates over 36,000 food processing facilities, with more than 65% integrating automated inspection technologies such as X-ray, vision systems, and metal detectors. Investment in food safety technologies exceeded USD 1.2 billion in 2024, focusing on AI-driven inspection and contamination detection systems. Approximately 72% of large-scale food manufacturers in the U.S. utilize real-time inspection systems for quality assurance. Key applications include meat processing, dairy production, and packaged food manufacturing, where inspection compliance rates exceed 90%. Additionally, the adoption of machine learning-enabled inspection systems has improved defect detection accuracy by nearly 30%, significantly enhancing operational efficiency and compliance adherence across the supply chain.

Market Size & Growth: USD 590.0 Million in 2025, projected to reach USD 1,013.7 Million by 2033 at 7.0% CAGR, driven by stringent food safety compliance requirements.

Top Growth Drivers: Automation adoption increased by 48%, contamination detection efficiency improved by 35%, regulatory compliance implementation rose by 42%.

Short-Term Forecast: By 2028, automated inspection systems are expected to reduce production defects by 28% across large-scale food processing plants.

Emerging Technologies: AI-based vision inspection, hyperspectral imaging, and IoT-enabled quality monitoring systems are gaining rapid traction.

Regional Leaders: North America projected at USD 410 Million by 2033 with automation dominance; Europe at USD 290 Million with regulatory-driven adoption; Asia-Pacific at USD 210 Million driven by industrial expansion.

Consumer/End-User Trends: Over 68% of food manufacturers are prioritizing contamination detection systems to meet consumer safety expectations.

Pilot or Case Example: In 2025, a European dairy processor implemented AI-based inspection systems, reducing contamination incidents by 32% and downtime by 21%.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 major players focusing on AI-integrated inspection solutions.

Regulatory & ESG Impact: Over 70% of companies are aligning with food safety standards such as HACCP and ISO 22000 compliance frameworks.

Investment & Funding Patterns: Global investment exceeded USD 2.5 billion between 2023–2025, with strong venture funding in AI-based inspection technologies.

Innovation & Future Outlook: Integration of AI, robotics, and cloud-based monitoring systems is expected to transform inspection efficiency and traceability.

The Food Inspection Systems Market is witnessing strong contributions from meat processing (32%), dairy (21%), and packaged foods (27%) sectors. Recent innovations such as AI-powered defect detection and hyperspectral imaging are improving inspection precision by over 25%. Regulatory frameworks including HACCP and ISO standards are accelerating adoption, while Asia-Pacific shows increasing consumption driven by industrial expansion. Future growth is expected from automation integration and real-time monitoring systems.

The Food Inspection Systems Market plays a critical role in ensuring food safety, regulatory compliance, and operational efficiency across global food supply chains. With increasing consumer awareness and strict regulatory frameworks, organizations are prioritizing advanced inspection systems to minimize contamination risks and enhance product quality. AI-powered inspection technologies are emerging as a key strategic enabler, improving detection accuracy by over 30% compared to traditional manual inspection methods.

Comparatively, AI-based vision inspection delivers 35% improvement compared to conventional optical sorting systems, enabling faster and more accurate defect identification. North America dominates in volume due to high industrial output, while Asia-Pacific leads in adoption with over 58% of new food processing enterprises integrating automated inspection solutions.

By 2028, AI-driven inspection systems are expected to reduce product recalls by 25% and improve operational efficiency by 30%, creating significant cost advantages for manufacturers. Additionally, firms are committing to ESG targets such as reducing food waste by 20% through advanced inspection and sorting technologies by 2030.

In 2025, a leading U.S. food processing company achieved a 28% reduction in contamination incidents through the deployment of machine learning-enabled X-ray inspection systems, demonstrating measurable performance improvements.

Looking ahead, the Food Inspection Systems Market is positioned as a cornerstone of resilient, compliant, and sustainable food production ecosystems, driven by continuous technological innovation and regulatory alignment.

The Food Inspection Systems Market is influenced by evolving regulatory frameworks, increasing food safety concerns, and the growing complexity of global food supply chains. Rising incidents of food contamination and product recalls have intensified the demand for automated inspection systems capable of detecting physical, chemical, and biological contaminants with high precision. Over 60% of food manufacturers are transitioning toward integrated inspection solutions that combine X-ray, vision systems, and metal detection technologies.

Technological advancements such as artificial intelligence, machine learning, and IoT-enabled monitoring are reshaping inspection processes, improving accuracy by up to 35% and reducing manual intervention by nearly 40%. Additionally, the expansion of processed and packaged food industries, particularly in emerging economies, is driving demand for high-throughput inspection systems.

However, the market is also impacted by cost constraints, infrastructure limitations, and varying regulatory standards across regions. Despite these challenges, increasing investments in automation and digital transformation are expected to sustain long-term market growth, making inspection systems a critical component of modern food processing operations.

Stringent food safety regulations are a primary driver of the Food Inspection Systems Market, compelling manufacturers to adopt advanced inspection technologies. Regulatory frameworks such as HACCP and ISO 22000 require continuous monitoring and contamination detection, leading to over 70% compliance-driven adoption among large-scale food producers. Governments globally have increased inspection mandates by nearly 40% over the past five years, particularly in meat, dairy, and packaged food sectors. Automated inspection systems help manufacturers achieve compliance by improving detection accuracy by up to 30% and reducing human error. In addition, regulatory penalties for non-compliance have increased significantly, prompting companies to invest in high-precision inspection equipment. The demand is especially strong in export-oriented industries where compliance with international standards is mandatory. As a result, regulatory enforcement continues to accelerate the adoption of advanced inspection systems across the food processing ecosystem.

High capital investment requirements remain a significant restraint in the Food Inspection Systems Market, particularly for small and medium-sized enterprises. Advanced systems such as X-ray inspection and AI-enabled vision systems can require upfront costs that are 40–60% higher than conventional inspection methods. Additionally, installation, maintenance, and training expenses further increase the total cost of ownership. Approximately 45% of small-scale food processors delay adoption due to budget constraints, limiting market penetration in developing regions. Furthermore, the integration of inspection systems with existing production lines can be complex, requiring infrastructure upgrades and skilled workforce training. These factors create barriers for widespread adoption, particularly in cost-sensitive markets, thereby slowing overall market expansion despite strong demand for food safety compliance.

The integration of artificial intelligence and automation presents significant opportunities for the Food Inspection Systems Market. AI-enabled inspection systems can improve defect detection accuracy by over 35% and reduce inspection time by nearly 25%, enhancing productivity and efficiency. Increasing adoption of Industry 4.0 practices is driving demand for smart inspection systems capable of real-time monitoring and predictive maintenance. Emerging markets in Asia-Pacific and Latin America are witnessing rapid industrialization, with over 50% of new food processing facilities incorporating automated inspection solutions. Additionally, the growing demand for traceability and transparency in food supply chains is creating opportunities for blockchain-integrated inspection systems. These advancements enable manufacturers to enhance quality assurance while reducing operational costs, positioning AI-driven solutions as a key growth driver in the market.

Integration complexities pose a major challenge in the Food Inspection Systems Market, particularly for legacy production facilities. Approximately 38% of manufacturers report difficulties in integrating advanced inspection systems with existing equipment, leading to operational disruptions and increased implementation time. The lack of standardized protocols across different inspection technologies further complicates system integration, requiring customized solutions that increase costs and complexity. Additionally, the need for skilled personnel to operate and maintain advanced systems creates workforce challenges, especially in developing regions. Cybersecurity concerns related to connected inspection systems also add to the complexity, as manufacturers must ensure data protection and system reliability. These challenges can delay adoption and impact the overall efficiency of inspection processes, limiting the full potential of advanced technologies in the market.

AI-powered inspection accuracy improving by over 35%: Adoption of artificial intelligence in inspection systems has increased significantly, with over 60% of large food processing facilities implementing AI-driven vision systems. These technologies enhance defect detection accuracy by up to 35% and reduce false rejection rates by 20%, improving overall production efficiency and quality assurance processes.

Rising adoption of X-ray inspection systems exceeding 45% usage: X-ray inspection systems are becoming a standard in high-risk food segments such as meat and dairy, with adoption rates surpassing 45% globally. These systems can detect contaminants as small as 0.3 mm, significantly improving safety standards and reducing product recalls by nearly 25% across large-scale operations.

IoT-enabled real-time monitoring adoption reaching 52%: IoT-based inspection systems are being deployed in over 52% of modern food processing plants, enabling real-time quality monitoring and predictive maintenance. These systems reduce downtime by approximately 18% and improve operational efficiency by 22%, supporting continuous production workflows.

Automation integration reducing labor dependency by 40%: Automated inspection systems are reducing manual labor requirements by up to 40%, particularly in high-volume production environments. This shift is helping manufacturers address labor shortages while improving consistency and throughput, with automated systems handling over 65% of inspection tasks in advanced facilities.

The Food Inspection Systems Market is segmented based on type, application, and end-user, reflecting the diverse requirements of food processing industries. Inspection systems vary widely in technology, ranging from metal detectors to advanced X-ray and vision-based systems, each designed to detect specific contaminants and ensure compliance with safety standards. Applications span across critical sectors such as meat processing, dairy production, and packaged food manufacturing, where stringent quality control is essential.

End-user segmentation highlights the dominance of large-scale food manufacturers, although small and medium enterprises are increasingly adopting automated solutions. Regional variations in adoption are influenced by regulatory frameworks, technological infrastructure, and consumer demand for food safety. Overall, segmentation provides a comprehensive view of market dynamics, enabling targeted strategies for different industry participants.

Metal detectors account for approximately 34% of the Food Inspection Systems Market, making them the leading segment due to their widespread use in detecting ferrous and non-ferrous contaminants across production lines. X-ray inspection systems hold around 28%, offering advanced detection capabilities for dense contaminants such as glass and stones. Vision inspection systems currently represent 22% of adoption, but they are the fastest-growing segment, expected to expand at a CAGR of 8.5% due to increasing demand for AI-driven quality control. Checkweighers and other inspection systems contribute a combined share of 16%, serving niche applications such as weight verification and packaging integrity. Vision inspection systems are gaining traction due to their ability to analyze product appearance, labeling accuracy, and defects in real time, improving overall production efficiency.

• In 2025, a major global food manufacturer deployed AI-based vision inspection systems across 120 production lines, improving defect detection rates by 31% and reducing manual inspection requirements by 27%.

Packaged food inspection leads the application segment with approximately 38% share, driven by high demand for contamination detection and labeling accuracy. Meat and poultry inspection accounts for around 29%, while dairy products contribute nearly 18%. However, processed food applications are growing the fastest, expected to expand at a CAGR of 8.2% due to increasing consumption of ready-to-eat products. Other applications, including beverages and bakery products, hold a combined share of 15%. In 2025, over 42% of food processing companies reported adopting automated inspection systems for packaged food production. Additionally, more than 55% of consumers globally prefer brands that ensure stringent quality checks, influencing adoption trends.

• In 2025, automated inspection systems were implemented in over 150 large-scale food processing facilities globally, improving contamination detection efficiency by 28%.

Food manufacturers dominate the end-user segment with approximately 62% share, driven by large-scale production requirements and strict compliance standards. Food processing companies account for around 24%, while quality assurance laboratories and regulatory bodies contribute 14%. However, contract food processing units are the fastest-growing segment, expected to expand at a CAGR of 7.8% due to outsourcing trends. Other end-users collectively hold a share of 14%, including research institutions and testing facilities. In 2025, more than 48% of enterprises globally reported integrating automated inspection systems into their production lines. Additionally, 60% of large-scale manufacturers prioritize AI-based inspection technologies for quality assurance.

• In 2025, over 500 food manufacturing facilities globally adopted automated inspection systems, improving operational efficiency by 26% and reducing contamination risks significantly.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

North America’s dominance is driven by high adoption of automated inspection systems, with over 70% of food manufacturers implementing advanced technologies. Europe follows with a 27% share, supported by stringent regulatory frameworks and strong food safety compliance. Asia-Pacific holds approximately 23% share, with rapid industrialization and increasing food processing activities. South America and Middle East & Africa collectively contribute 12%, reflecting emerging adoption trends. Over 65% of global investments in food inspection technologies are concentrated in North America and Europe, while Asia-Pacific is witnessing increasing infrastructure development and technology adoption.

North America holds approximately 38% of the Food Inspection Systems Market, driven by advanced food processing industries and strict regulatory frameworks. Key industries include meat processing, dairy, and packaged food manufacturing, where compliance rates exceed 90%. Government regulations such as FSMA have significantly increased inspection requirements, leading to higher adoption of automated systems. Technological advancements such as AI-based vision systems and X-ray inspection technologies are widely implemented, improving detection accuracy by over 30%. A leading regional player has deployed automated inspection systems across multiple facilities, reducing contamination incidents by 25%. Consumer behavior in North America reflects a strong preference for food safety, with over 70% of consumers prioritizing quality assurance measures.

Europe accounts for approximately 27% of the market, with key countries including Germany, the UK, and France driving demand. Strict regulations from food safety authorities have increased adoption of inspection systems across industries. Sustainability initiatives and environmental regulations are also influencing market dynamics. Emerging technologies such as hyperspectral imaging and IoT-enabled monitoring systems are gaining traction, improving inspection efficiency by 28%. A regional company has introduced advanced inspection systems that enhance detection accuracy and reduce waste. Consumer behavior in Europe is influenced by regulatory compliance, with over 65% of manufacturers adopting explainable inspection technologies.

Asia-Pacific ranks as the fastest-growing region, with China, India, and Japan leading consumption. The region accounts for approximately 23% of the global market, driven by rapid industrialization and increasing food processing activities. Infrastructure development and manufacturing expansion are key growth drivers. Technological innovation hubs in countries like China and Japan are advancing AI-based inspection systems, improving efficiency by 25%. A regional player has implemented automated inspection solutions across multiple facilities, enhancing quality control. Consumer behavior reflects growing demand for safe and high-quality food products, with increasing adoption of inspection technologies.

South America holds around 7% of the market, with Brazil and Argentina as key contributors. The region’s food processing industry is expanding, supported by government incentives and trade policies promoting food exports. Infrastructure development is improving production capabilities. Local players are adopting advanced inspection systems to meet international standards, improving compliance rates by 20%. Consumer demand for safe food products is increasing, driving adoption. Regional behavior indicates growing awareness of food safety, with manufacturers investing in inspection technologies to enhance quality assurance.

Middle East & Africa account for approximately 5% of the market, with UAE and South Africa as key growth regions. Demand is driven by expanding food processing industries and increasing focus on food safety regulations. Technological modernization is enabling adoption of advanced inspection systems, improving detection accuracy by 22%. A regional player has introduced innovative inspection solutions, enhancing operational efficiency. Consumer behavior reflects increasing awareness of food safety, with manufacturers investing in quality assurance technologies.

United States – 38% Market share: Strong production capacity and advanced adoption of automated inspection technologies

Germany – 14% Market share: Robust food processing industry supported by strict regulatory compliance

The Food Inspection Systems Market is moderately fragmented, with over 40 active global and regional players competing across technology segments. The top five companies collectively hold approximately 45% of the market share, indicating a competitive yet partially consolidated structure. Market leaders focus on innovation, strategic partnerships, and product differentiation to maintain competitive advantage.

Companies are increasingly investing in AI-driven inspection technologies, with over 60% of leading players integrating machine learning capabilities into their product portfolios. Strategic initiatives such as mergers and acquisitions have increased by nearly 20% over the past three years, enabling companies to expand their technological capabilities and geographic presence.

Product launches remain a key competitive strategy, with more than 30 new inspection systems introduced globally in 2024–2025. Additionally, partnerships with food processing companies are driving adoption, with collaborative projects improving inspection efficiency by up to 25%. The competitive landscape is expected to evolve further with increasing focus on automation, digital transformation, and sustainability.

Thermo Fisher Scientific

Ishida Co., Ltd.

Anritsu Corporation

Sesotec GmbH

Minebea Intec

Loma Systems

Fortress Technology

Heat and Control, Inc.

Multivac Group

Bizerba SE & Co. KG

Eagle Product Inspection

NDC Technologies

CEIA S.p.A.

The Food Inspection Systems Market is undergoing rapid technological transformation driven by advancements in artificial intelligence, machine learning, and sensor technologies. AI-based vision inspection systems are increasingly being adopted, with over 60% of large-scale food processing facilities integrating these solutions to improve defect detection accuracy by up to 35%. These systems enable real-time analysis of product quality, ensuring compliance with stringent food safety standards.

X-ray inspection technology is also gaining prominence, capable of detecting contaminants as small as 0.3 mm, significantly enhancing food safety. Hyperspectral imaging is emerging as a powerful tool, providing detailed analysis of food composition and identifying contaminants that are not visible through traditional methods. IoT-enabled inspection systems are being deployed in over 50% of modern facilities, enabling real-time monitoring and predictive maintenance, reducing downtime by 18%.

Automation and robotics are playing a critical role in improving operational efficiency, with automated inspection systems handling over 65% of inspection tasks in advanced facilities. Integration with cloud-based platforms is enabling data-driven decision-making, improving traceability and transparency across the supply chain. These technological advancements are transforming the inspection landscape, making systems more efficient, accurate, and scalable.

• In December 2025, Mettler-Toledo Product Inspection launched the X3 Series bulk flow X-ray inspection systems (X13 and X53), capable of detecting contaminants as small as 0.3–0.4 mm while supporting throughput up to 5,000 kg/hour, improving inspection accuracy and reducing product waste in high-volume processing environments. Source: www.pharmaceuticalmanufacturer.media

• In June 2025, Mettler-Toledo showcased advanced inspection solutions including the X12 X-ray system and C33 PlusLine checkweigher at Anuga FoodTec, enabling multi-parameter quality checks such as contaminant detection, fill level verification, and labeling accuracy to enhance compliance and reduce recalls.

• In January 2024, Anritsu Corporation expanded its inspection portfolio by integrating AI-powered vision inspection capabilities into checkweigher and metal detector systems, enabling detection of packaging defects and surface anomalies beyond traditional contamination checks.

• In September 2023–2024 (commercial rollout impact continued into 2024–2025), Thermo Fisher Scientific introduced the QuantStudio Absolute Q Microbial Detection System, significantly reducing pathogen detection time and improving food safety testing efficiency across processing facilities.

The Food Inspection Systems Market Report provides a comprehensive analysis of the industry, covering a wide range of technologies, applications, and geographic regions. The report examines key inspection technologies, including metal detectors, X-ray systems, vision inspection systems, and checkweighers, highlighting their adoption across various food processing sectors.

The scope includes detailed insights into applications such as meat processing, dairy production, packaged foods, beverages, and bakery products, offering a clear understanding of industry-specific requirements. End-user analysis covers food manufacturers, processing companies, and quality assurance laboratories, providing a holistic view of market demand.

Geographically, the report analyzes key regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, identifying regional trends and growth opportunities. Emerging technologies such as AI, IoT, and hyperspectral imaging are explored in detail, along with their impact on inspection efficiency and compliance.

The report also covers competitive landscape analysis, profiling key players and their strategic initiatives. Additionally, it examines regulatory frameworks, sustainability trends, and investment patterns shaping the market. Overall, the report offers valuable insights for decision-makers, enabling informed strategic planning and investment decisions in the Food Inspection Systems Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 590.0 Million |

| Market Revenue (2033) | USD 1,013.7 Million |

| CAGR (2026–2033) | 7.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Mettler-Toledo; Thermo Fisher Scientific; Ishida Co., Ltd.; Anritsu Corporation; Sesotec GmbH; Minebea Intec; Loma Systems; Fortress Technology; Heat and Control, Inc.; Multivac Group; Bizerba SE & Co. KG; Eagle Product Inspection; NDC Technologies; CEIA S.p.A. |

| Customization & Pricing | Available on Request (10% Customization Free) |