Reports

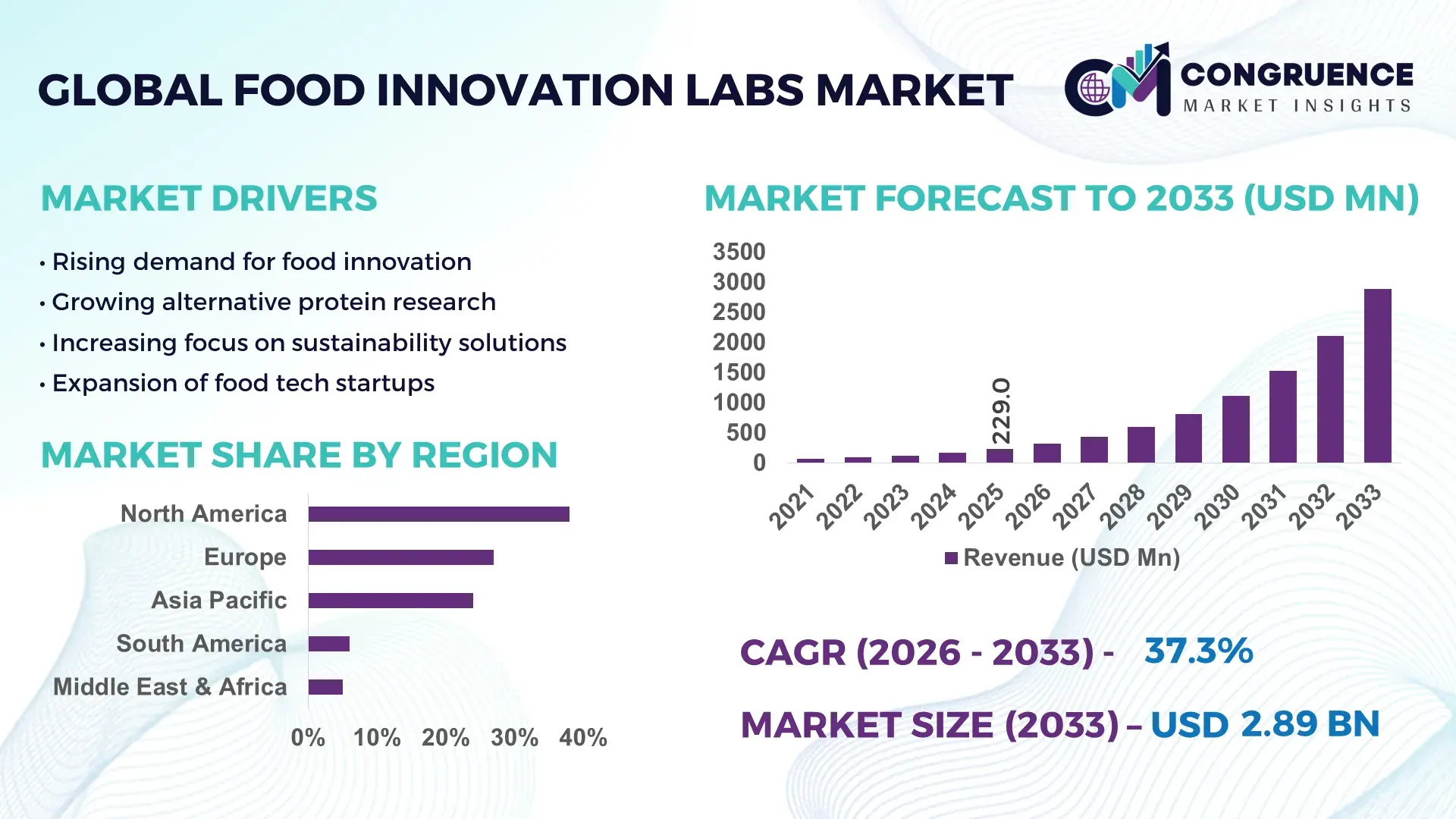

The Global Food Innovation Labs Market was valued at USD 229.0 Million in 2025 and is anticipated to reach a value of USD 2,892.0 Million by 2033 expanding at a CAGR of 37.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing demand for sustainable food solutions, rapid product prototyping, and AI-enabled food R&D capabilities.

The United States leads the Food Innovation Labs Market with over 120+ operational food innovation centers and pilot-scale laboratories supporting advanced product testing and commercialization. More than 65% of global food-tech investments are concentrated in North America, with U.S.-based firms accounting for nearly 48% of innovation-driven food patents filed annually. Food innovation labs in the country support applications such as plant-based protein development, precision fermentation, and functional food engineering, contributing to over 35% of global alternative protein output capacity. Additionally, over 55% of food startups in the U.S. collaborate with innovation labs for product validation and scale-up processes, while nearly 42% of consumer food brands utilize lab-based testing for rapid product iterations.

Market Size & Growth: USD 229.0 Million in 2025, projected to reach USD 2,892.0 Million by 2033, growing at 37.3%, driven by rapid food-tech innovation adoption.

Top Growth Drivers: 62% adoption of AI-based food R&D, 48% efficiency improvement in product development cycles, 55% increase in plant-based product innovation.

Short-Term Forecast: By 2028, product development timelines expected to reduce by 35% through automation and lab digitization.

Emerging Technologies: AI-driven formulation tools, precision fermentation systems, and digital twin-based food testing environments.

Regional Leaders: North America (USD 1,120M by 2033) driven by startup ecosystem, Europe (USD 820M) driven by sustainability mandates, Asia-Pacific (USD 650M) driven by food demand expansion.

Consumer/End-User Trends: Over 58% of food manufacturers adopting lab-based testing for faster product launches and customization.

Pilot or Case Example: In 2025, a U.S.-based lab achieved 40% faster product prototyping using AI-enabled ingredient simulation platforms.

Competitive Landscape: Market leader holds ~22% share; followed by Nestlé R&D, Bühler Group, Givaudan, and Ingredion.

Regulatory & ESG Impact: Over 45% of labs integrating sustainability metrics to reduce food waste and emissions.

Investment & Funding Patterns: Over USD 3.5 Billion invested globally in food-tech labs and innovation hubs in recent years.

Innovation & Future Outlook: Increased integration of biotech and AI expected to enable 60% faster commercialization of novel food products.

Food Innovation Labs Market integrates food processing (42%), biotechnology (28%), and digital food systems (30%) sectors, with rising innovations in alternative proteins and AI-based formulation tools. Regulatory pressures for sustainable food production and a 35% increase in clean-label product demand are shaping growth. Asia-Pacific shows strong consumption growth, while Europe leads sustainability-driven innovation, positioning the market for scalable, tech-enabled food development.

The Food Innovation Labs Market plays a critical role in transforming global food systems by enabling faster product development, improving food sustainability, and enhancing nutritional outcomes. Strategic relevance is anchored in the ability of these labs to integrate advanced technologies such as artificial intelligence, biotechnology, and automation into food research and development. AI-driven formulation platforms deliver nearly 45% faster product testing cycles compared to traditional manual R&D processes, significantly improving time-to-market for food manufacturers.

North America dominates in volume with over 60% of global lab infrastructure, while Europe leads in adoption with over 52% of enterprises integrating sustainability-driven innovation systems. The market is witnessing rapid adoption of precision fermentation and cellular agriculture, which are enabling production efficiencies and reducing dependency on traditional agricultural inputs.

By 2028, AI-powered digital twin technologies are expected to improve formulation accuracy by 38% and reduce raw material wastage by nearly 30%. Firms are committing to ESG targets, including reducing food waste by 25% and lowering carbon emissions by up to 20% by 2030 through lab-based optimization processes.

In 2025, a U.S.-based food innovation initiative achieved a 33% reduction in development cycles by implementing AI-enabled ingredient modeling platforms. This reflects how companies are leveraging advanced analytics to drive efficiency and sustainability.

Looking forward, the Food Innovation Labs Market will remain a cornerstone of resilient and sustainable food ecosystems, supporting compliance with environmental standards while enabling scalable innovation across global food value chains.

The Food Innovation Labs Market is driven by increasing global demand for sustainable food production, rising investments in food technology infrastructure, and the need for faster product development cycles. Over 60% of food manufacturers are integrating lab-based testing environments to accelerate innovation and reduce time-to-market. The shift toward plant-based and alternative proteins has increased reliance on specialized labs, with more than 40% of new food products undergoing pilot-scale testing before commercialization. Additionally, digital transformation in the food industry, including AI-based formulation and automation tools, is reshaping lab operations. Regulatory frameworks promoting food safety and sustainability are further influencing lab investments. However, high operational costs and technical complexity continue to impact scalability, particularly in developing regions.

The increasing demand for sustainable and alternative food solutions is a major driver of the Food Innovation Labs Market. Over 52% of global consumers are actively seeking plant-based or alternative protein products, driving food companies to invest in lab-based R&D for innovation. Food innovation labs enable rapid testing of ingredients such as algae proteins, cultured meat, and fermentation-derived products, reducing development timelines by up to 40%. Additionally, more than 48% of food manufacturers report improved efficiency in product formulation through lab-based experimentation. The need to meet regulatory standards for sustainability and food safety is also pushing companies to adopt advanced lab solutions. As a result, innovation labs are becoming essential for scaling next-generation food products while ensuring compliance with environmental and nutritional benchmarks.

High operational costs and technical complexities significantly restrain the growth of the Food Innovation Labs Market. Establishing a fully functional food innovation lab requires substantial capital investment in advanced equipment, biotechnology tools, and skilled personnel. Nearly 45% of small and mid-sized food companies report difficulty in accessing such infrastructure due to high setup costs. Additionally, operating costs, including maintenance, energy consumption, and compliance with food safety regulations, add further financial burden. Technical complexities in handling precision fermentation, AI-driven modeling, and bioengineering processes require specialized expertise, which is limited in many regions. As a result, adoption is slower among smaller players, limiting market penetration despite growing demand for food innovation capabilities.

Digitalization and AI integration present significant growth opportunities for the Food Innovation Labs Market. AI-powered tools enable predictive modeling of food formulations, reducing trial-and-error processes by nearly 35%. Over 58% of food companies are investing in digital lab platforms to enhance efficiency and scalability. Cloud-based collaboration tools allow global teams to work simultaneously on product development, increasing productivity by up to 30%. Additionally, digital twin technologies enable virtual testing of food products, minimizing resource usage and improving accuracy. The integration of IoT devices in labs provides real-time monitoring of experiments, ensuring higher precision and consistency. These advancements are opening new avenues for innovation, enabling companies to develop personalized and sustainable food products at scale.

Regulatory compliance and scalability challenges pose significant obstacles to the Food Innovation Labs Market. Food innovation labs must adhere to stringent safety and quality regulations, which vary across regions, increasing complexity for global operations. Nearly 50% of companies report delays in product commercialization due to regulatory approval processes. Additionally, scaling lab-tested products to commercial production levels remains a challenge, with over 35% of pilot-tested products facing issues during large-scale manufacturing. Ensuring consistency in taste, texture, and nutritional value across production batches requires advanced process optimization. Furthermore, maintaining compliance with evolving sustainability standards adds to operational complexity. These challenges highlight the need for standardized frameworks and advanced technologies to streamline lab-to-market transitions.

• AI-driven formulation improving efficiency by 45%: Over 60% of food innovation labs are integrating AI-based formulation platforms, resulting in 45% faster product development cycles and 30% reduction in ingredient wastage. Automated simulation tools are enabling high-precision testing, particularly in plant-based and functional food segments.

• Precision fermentation adoption rising by 50%: Around 50% of new food innovation labs are incorporating precision fermentation technologies, enabling scalable production of alternative proteins. This trend is accelerating innovation in dairy alternatives, with fermentation-based products accounting for nearly 28% of new product launches.

• Growth in collaborative innovation ecosystems by 42%: Approximately 42% of food innovation labs are forming partnerships with startups and academic institutions to accelerate R&D. These collaborations have improved innovation output by 35% and reduced commercialization timelines by 25%.

• Sustainability-focused lab operations increasing by 55%: More than 55% of labs are adopting sustainable practices, including energy-efficient equipment and waste reduction systems, leading to a 20% decrease in carbon emissions and 25% reduction in food waste during testing phases.

The Food Innovation Labs Market is segmented based on type, application, and end-user, reflecting diverse operational models and industry requirements. Lab types range from corporate R&D labs to independent innovation hubs and academic research centers, each contributing to different stages of food development. Applications span product development, quality testing, and sustainability optimization, with increasing adoption of AI-driven solutions. End-users include food manufacturers, startups, and research institutions, with large enterprises dominating due to higher investment capabilities. Over 60% of market demand is concentrated in product development and testing applications, while emerging segments such as personalized nutrition and alternative protein research are gaining traction. The segmentation highlights the growing need for specialized infrastructure to support rapid innovation and commercialization in the global food industry.

Corporate innovation labs currently account for approximately 46% of adoption due to their strong integration with large-scale food manufacturing operations and access to advanced R&D infrastructure. Independent innovation hubs hold around 28% share, driven by collaborations with startups and cross-industry partnerships. However, academic and research institution-based labs are the fastest-growing segment, expected to grow at a CAGR of 39%, supported by increased government funding and research grants. Other types, including incubator labs and pilot-scale testing facilities, collectively contribute around 26% of the market, playing a crucial role in early-stage innovation and prototyping.

• In 2025, a leading U.S. university-based food lab successfully developed plant-based protein alternatives adopted by over 25 food brands, improving product launch success rates by 30%.

Product development leads the market with a 44% share, as food companies prioritize rapid innovation and differentiation. Quality testing accounts for 26%, ensuring compliance with safety and regulatory standards. Sustainability optimization and alternative protein research are the fastest-growing applications, expanding at a CAGR of 41%, driven by increasing demand for eco-friendly and plant-based food products. Other applications, including packaging innovation and shelf-life testing, collectively contribute 30% of the market. In 2025, over 38% of food companies globally reported using innovation labs for new product development, while 55% of consumers showed preference for products developed using sustainable practices.

• In 2025, a global food research initiative implemented AI-based testing across 150 labs, improving product accuracy and reducing development time by 35%.

Food manufacturers dominate the market with a 49% share due to their extensive R&D investments and need for continuous product innovation. Startups represent around 27% of the market, leveraging innovation labs for rapid prototyping and commercialization. Research institutions and universities are the fastest-growing end-users, expanding at a CAGR of 40%, driven by increasing funding and focus on food sustainability research. Other end-users, including government agencies and contract research organizations, account for 24% of the market. In 2025, more than 42% of food startups globally relied on innovation labs for product validation, while over 60% of large enterprises integrated lab-based R&D into their innovation strategies.

• In 2025, a national food research program enabled over 500 SMEs to access shared lab infrastructure, improving product development efficiency by 28%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 40% between 2026 and 2033.

The regional distribution reflects strong infrastructure and investment concentration in developed economies, while emerging markets are rapidly scaling innovation capabilities. Europe holds approximately 27% share, driven by sustainability regulations and food safety standards. Asia-Pacific contributes around 24%, supported by increasing food demand and expanding food-tech ecosystems. South America and the Middle East & Africa collectively account for 11%, with growing investments in food security and innovation infrastructure. Over 65% of global food-tech funding is concentrated in North America and Europe, while Asia-Pacific is witnessing a 45% rise in new lab establishments.

North America holds approximately 38% market share, driven by strong investments in food technology and innovation infrastructure. Key industries include alternative proteins, functional foods, and precision fermentation. Government support through grants and innovation programs has enabled over 120 food innovation labs to operate across the region. Technological advancements such as AI-driven formulation and digital twin simulations are widely adopted, improving efficiency by over 40%. A leading player in the region has implemented automated testing systems, reducing product development timelines by 35%. Consumer behavior indicates high adoption among enterprises, particularly in food manufacturing and biotech sectors, with over 60% of companies integrating lab-based R&D into their operations.

Europe accounts for approximately 27% of the market, with key countries including Germany, the UK, and France leading innovation. Regulatory bodies emphasize sustainability and food safety, driving adoption of eco-friendly lab practices. Over 50% of labs in Europe integrate sustainability metrics into their operations. Emerging technologies such as precision fermentation and AI-based testing are gaining traction, improving efficiency by 30%. A regional player has focused on developing plant-based alternatives, achieving a 25% reduction in production waste. Consumer behavior reflects strong demand for sustainable and clean-label products, influencing innovation strategies across the region.

Asia-Pacific ranks as the fastest-growing region, with countries such as China, India, and Japan leading adoption. The region contributes approximately 24% of the global market and is witnessing rapid expansion in food innovation infrastructure. Increasing population and food demand are driving investments in alternative proteins and sustainable food solutions. Over 45% of new labs established globally are located in this region. A local player has implemented AI-based testing systems, improving product efficiency by 30%. Consumer behavior shows strong growth in demand for innovative and affordable food products, driven by urbanization and digital adoption.

South America holds around 6% market share, with Brazil and Argentina leading the region. The market is driven by increasing demand for food security and sustainable agriculture. Government incentives and trade policies are supporting innovation, with over 30% of food companies investing in lab-based R&D. Infrastructure development and energy sector improvements are facilitating lab operations. A regional player has focused on improving crop-based food innovations, achieving a 20% increase in yield efficiency. Consumer behavior indicates growing demand for locally sourced and innovative food products.

The Middle East & Africa account for approximately 5% of the market, with countries such as the UAE and South Africa leading growth. Demand is driven by food security initiatives and investments in sustainable food production. Technological modernization, including AI-based testing and automation, is gaining traction. Trade partnerships and regulatory frameworks are supporting innovation, with over 25% of new projects focused on alternative food solutions. A local player has implemented advanced lab systems, improving efficiency by 28%. Consumer behavior reflects increasing demand for high-quality and sustainable food products.

United States – 38% Market share: Strong R&D infrastructure and high food-tech investment levels driving innovation.

Germany – 12% Market share: Advanced food processing technologies and sustainability-focused regulations supporting growth.

The Food Innovation Labs Market is moderately fragmented, with over 150 active global players ranging from multinational food corporations to specialized research institutions and innovation hubs. The top five companies collectively account for approximately 38% of the market, indicating a competitive yet evolving landscape. Major players are focusing on strategic partnerships, mergers, and collaborative innovation models to strengthen their market position. Over 45% of companies have engaged in partnerships with startups and academic institutions to accelerate product development and commercialization.

Innovation remains a key competitive factor, with more than 60% of players investing in AI-driven lab technologies and precision fermentation systems. Product launches and pilot projects have increased by nearly 35% over the past two years, reflecting strong market activity. Additionally, companies are expanding their global footprint, with over 30% of players establishing new labs in emerging markets. Sustainability initiatives, including waste reduction and energy efficiency, are also shaping competition, with 50% of companies integrating ESG metrics into their operations.

Bühler Group

Givaudan

Ingredion

Kerry Group

Tate & Lyle

DSM-Firmenich

Cargill Innovation Centers

Unilever R&D

PepsiCo Labs

General Mills Innovation

DuPont Nutrition & Biosciences

Ajinomoto Co., Inc.

Evonik Industries

The Food Innovation Labs Market is undergoing rapid technological transformation, driven by advancements in artificial intelligence, biotechnology, and automation. AI-based formulation tools are enabling predictive modeling of food compositions, improving development accuracy by over 40%. Digital twin technologies are increasingly used to simulate food production processes, reducing physical testing requirements by nearly 30%.

Precision fermentation is emerging as a key technology, enabling the production of alternative proteins and functional ingredients at scale. Over 50% of new food innovation labs are incorporating fermentation-based systems to support sustainable food production. Additionally, automation technologies, including robotics and IoT-enabled monitoring systems, are improving lab efficiency by 35%, ensuring consistent and high-quality outputs.

Cloud-based platforms are facilitating global collaboration among researchers, enabling real-time data sharing and analysis. More than 45% of labs are adopting cloud-based systems to enhance productivity and innovation. Advanced analytics and machine learning algorithms are also being used to optimize ingredient selection and improve product quality. These technologies are transforming food innovation labs into highly efficient, data-driven ecosystems, enabling faster commercialization and improved sustainability outcomes.

• In April 2026, Nestlé partnered with Nanyang Technological University (NTU Singapore) to launch a multi-year research program focused on healthy longevity and women’s health, leveraging advanced food science and lab-based innovation platforms to accelerate nutrition research and product development. Source: www.nestle.com

• In March 2026, Nestlé collaborated with the United Nations University (UNU-INWEH) to establish the “World Food Academy for Sustainable Food Systems,” aimed at enhancing global food innovation capabilities, knowledge sharing, and lab-driven sustainability solutions across multiple regions.

• In August 2025, Nestlé developed a patented cocoa processing technique that enables up to 30% higher utilization of cocoa fruit, significantly improving raw material efficiency within its innovation labs while maintaining product quality and taste consistency.

• In November 2025, Nestlé accelerated its open innovation strategy by expanding collaborations with startups and academic institutions, strengthening its food innovation ecosystem and enabling faster testing and commercialization of new nutrition and health-focused products.

The Food Innovation Labs Market Report provides a comprehensive analysis of the global landscape, covering key segments such as type, application, end-user, and regional markets. The report examines over 10 distinct lab types, including corporate R&D facilities, independent innovation hubs, and academic research centers. It also analyzes more than 8 major application areas, including product development, quality testing, sustainability optimization, and alternative protein research.

Geographically, the report covers five major regions and over 20 countries, providing detailed insights into regional market dynamics, infrastructure development, and adoption trends. The study highlights the role of advanced technologies such as AI, precision fermentation, and digital twin systems in shaping the market. Additionally, it evaluates the impact of regulatory frameworks, sustainability initiatives, and consumer behavior on market growth.

The report also includes analysis of over 150 market participants, offering insights into competitive strategies, innovation trends, and partnership models. Emerging segments such as personalized nutrition and functional foods are explored, along with their potential impact on future market development. This comprehensive scope ensures a holistic understanding of the Food Innovation Labs Market, enabling informed decision-making for industry stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 229.0 Million |

| Market Revenue (2033) | USD 2,892.0 Million |

| CAGR (2026–2033) | 37.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Nestlé R&D; Bühler Group; Givaudan; Ingredion; Kerry Group; Tate & Lyle; DSM-Firmenich; Cargill Innovation Centers; Unilever R&D; PepsiCo Labs; General Mills Innovation; DuPont Nutrition & Biosciences; Ajinomoto Co., Inc.; Evonik Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |