Reports

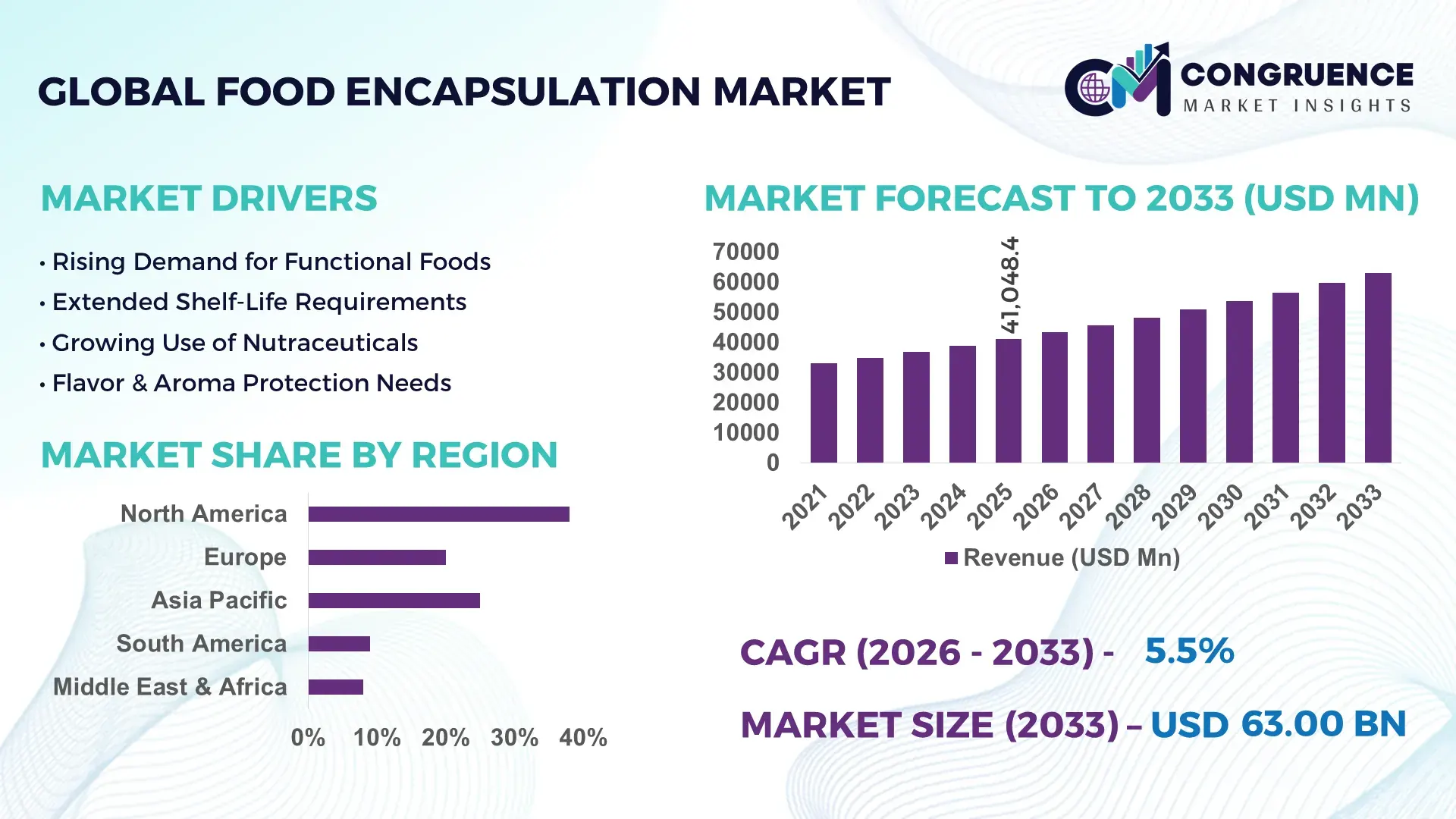

The Global Food Encapsulation Market was valued at USD 41048.36 Million in 2025 and is anticipated to reach a value of USD 62996.36 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. This growth is driven by increasing demand for functional foods and enhanced ingredient stability.

In the United States, which leads in food encapsulation deployment, advanced manufacturing infrastructure supports over 1,200 kilotonnes per annum of encapsulated ingredient output capacity across dairy, nutraceuticals, and flavor systems. U.S. investments in encapsulation technologies exceeded USD 450 million in 2024, focusing on high‑pressure homogenization and spray drying automation. Key industry applications in the U.S. include fortified beverages, probiotic delivery systems, and controlled‑release flavor ingredients, with consumer adoption rates for encapsulated nutraceutical additives exceeding 35% in urban retail segments. Technological advancements emphasize microencapsulation process optimization and real‑time quality analytics in commercial production.

Market Size & Growth: Estimated at USD 41.05 Bn in 2025; projected to reach ~USD 62.99 Bn by 2033 at a 5.5% CAGR, underpinned by rising functional ingredient utilization and processing efficiency improvements.

Top Growth Drivers: Adoption of fortified foods (~30% increase), demand for extended shelf life (~25% improvement), and health‑oriented ingredient encapsulation (~40% uptake).

Short‑Term Forecast: By 2028, encapsulation efficiency gains expected to reduce ingredient degradation by ~20%.

Emerging Technologies: High‑pressure homogenization enhancements, advanced coacervation, and AI‑driven process monitoring.

Regional Leaders: North America (~USD 18 Bn by 2033 with strong food tech integration), Europe (~USD 15 Bn with functional dairy trends), Asia‑Pacific (~USD 13 Bn with rapid retail expansion).

Consumer/End‑User Trends: Growth in sports nutrition, fortified beverages, and clean‑label encapsulated flavors; urban adoption outpacing rural.

Pilot or Case Example: In 2024, a major beverage processor implemented nanoencapsulation, improving active retention by ~22% in product shelf life trials.

Competitive Landscape: Market leader with ~28% share, followed by key competitors at ~15–8% each across global supply chains.

Regulatory & ESG Impact: Stricter labeling standards, food safety incentives, and sustainability criteria shaping encapsulation formulation and packaging.

Investment & Funding Patterns: Over USD 600 million in recent funding rounds; increasing venture interest in plant‑based encapsulation technologies.

Innovation & Future Outlook: Integration of biotechnology for targeted release, scalable spray drying platforms, and predictive quality analytics spearheading next‑gen applications.

The Food Encapsulation Market exhibits diversified growth across key sectors such as beverages, dairy, nutraceuticals, and bakery, where encapsulated flavors and probiotics contribute significantly to product differentiation. Recent innovations include bio‑based encapsulating materials, nanoencapsulation for enhanced nutrient delivery, and modular spray dryer systems reducing operational costs. Regulatory frameworks around food additive safety and environmental sustainability are accelerating adoption of clean label encapsulation solutions, while Asia‑Pacific consumption patterns reflect strong demand for fortified foods. Emerging trends point to personalized nutrition delivery systems and digital process control as core drivers of future market expansion.

The strategic relevance of the Food Encapsulation Market lies in its role as a foundational technology for improving the stability, delivery, and sensory performance of functional ingredients in food and beverage products. Encapsulation technologies protect vitamins, probiotics, flavors, and bioactive compounds through processing, storage, and digestion, enabling manufacturers to meet increasing consumer demand for fortified and health‑oriented foods while complying with stringent food safety and quality standards. For example, emerging nanoencapsulation delivers up to 95% retention of active nutrients during thermal processing compared to roughly 60% with traditional unencapsulated formats, enhancing product performance in heat‑intensive applications such as dairy and powdered beverages.

North America dominates in production volume due to its mature food processing infrastructure, while Asia‑Pacific leads in adoption, with over 42% of enterprises integrating advanced encapsulation systems into R&D pipelines for functional foods in 2025. By 2028, AI‑driven process optimization is expected to improve encapsulation process efficiency by 18–22%, reducing batch cycle times and material waste. Firms are committing to ESG metrics, targeting a 25% reduction in energy consumption per unit of encapsulated product by 2030 through increased use of low‑temperature spray chilling and energy‑efficient dryers. Advanced analytical controls combined with IoT monitoring have already enabled a major formulation partner to achieve a 20% reduction in quality deviations in 2025.

Future pathways emphasize hybrid technologies that merge micro and nano strategies, development of plant‑based wall materials with enhanced biodegradability, and predictive release systems tailored for personalized nutrition. These innovations position the Food Encapsulation Market as a pillar of resilience, regulatory compliance, and sustainable growth across the global food value chain.

The increasing consumer demand for functional foods and fortified products is a major driver of the Food Encapsulation Market. Encapsulation enables the incorporation of sensitive nutrients, probiotics, antioxidants, and omega‑3 fatty acids without compromising taste or stability, supporting manufacturers in delivering enhanced health benefits. Functional foods accounted for over 44% of encapsulated ingredient utilization in 2025, reflecting widespread integration of encapsulated bioactives in mainstream product lines such as fortified cereals, enhanced dairy beverages, and nutrient‑rich snacks. Dietary supplements are also leveraging encapsulation to improve ingredient stability and convenience, with microencapsulation techniques enabling time‑release delivery formats and improved consumer compliance. Rapid urbanization and heightened health consciousness among consumers have further accelerated the appetite for encapsulated nutrient delivery systems across food categories.

One of the principal restraints in the Food Encapsulation Market is the high cost of advanced encapsulation equipment and processes. Technologies such as electrohydrodynamic encapsulation and nanoencapsulation often require specialized machinery, skilled operators, and stringent process controls, increasing upfront capital expenditure and operational complexity. Advanced systems like freeze‑dryers or electrospinning units can incur 50–80% higher production costs compared with conventional spray drying, making them less accessible for smaller manufacturers. Raw materials for sophisticated wall matrices, including modified proteins or polysaccharides, often command premium prices, further elevating production costs. This cost burden can slow technology penetration in price‑sensitive segments and limit experimentation with next‑generation encapsulation methods despite their performance advantages.

Emerging opportunities in the Food Encapsulation Market stem from the shift toward clean‑label, plant‑based materials that align with consumer preferences for natural, sustainable products. Innovations in plant‑based polysaccharide carriers, such as alginate, pectin, and inulin, provide biodegradable alternatives to traditional wall materials while maintaining high encapsulation efficiencies, often exceeding 85–90% in research settings. This shift opens new avenues for encapsulating bioactive phenolics, pigments, and omega‑3 fatty acids in products targeted at vegan, organic, and health‑conscious demographics. Nanoencapsulation also presents opportunities in personalized nutrition delivery, enabling tailored nutrient profiles based on individual consumer needs. Expansion into emerging markets with rising disposable incomes and functional food adoption further enhances growth potential, especially in Asia‑Pacific and Latin America.

A core challenge facing the Food Encapsulation Market is navigating complex regulatory landscapes while ensuring consistent raw material performance. Regulatory frameworks governing food additives, clean‑label claims, and health benefit assertions vary across regions, requiring manufacturers to adapt formulations to comply with differing standards. Approval processes for novel encapsulating materials can be lengthy, and consumer perceptions of nano‑scale ingredients may limit adoption in certain markets. Supply chain variability in raw materials like proteins, lipids, and polysaccharides can lead to inconsistencies in encapsulation efficiency, impacting product quality and performance. In addition, maintaining quality and safety across high‑volume production environments demands rigorous process control systems and validation protocols, increasing operational overheads and posing barriers for smaller food processors. These factors require manufacturers to invest in robust quality assurance frameworks and cross‑functional compliance expertise to sustain growth initiatives in this evolving market.

Expansion of Nanoencapsulation Techniques: The adoption of nanoencapsulation is accelerating, with over 38% of functional beverage and dairy manufacturers integrating nanoscale delivery systems in 2025. These technologies enhance bioactive retention by up to 92% during thermal processing and improve solubility by 65%, enabling more stable and nutrient-rich products in competitive food segments.

Shift Toward Plant-Based Wall Materials: More than 47% of new encapsulated product formulations in 2024–2025 use plant-derived carriers such as pectin, alginate, and inulin. These materials demonstrate encapsulation efficiency of 85–90% and contribute to a 30% reduction in synthetic additive usage, aligning with consumer demand for clean-label and sustainable solutions across beverages, snacks, and nutraceuticals.

Integration of AI and Process Automation: By 2025, 41% of medium and large-scale food processing facilities implemented AI-driven encapsulation monitoring systems, improving process accuracy by 22% and reducing production downtime by 18%. Real-time analytics enable predictive maintenance, precise ingredient dosing, and optimized drying cycles, enhancing operational efficiency in high-volume production.

Regional Adoption and Innovation Leadership: North America leads in volume, producing over 1,200 kilotonnes of encapsulated ingredients annually, while Asia-Pacific shows the highest adoption rate with 42% of enterprises deploying advanced encapsulation for functional foods. Europe demonstrates a strong shift toward precision microencapsulation, achieving 25% higher nutrient retention compared to conventional techniques, particularly in fortified dairy and beverage segments.

The Food Encapsulation Market is structured around three primary segmentation categories: types, applications, and end-users, each reflecting unique technological adoption patterns and industry requirements. By type, encapsulation solutions are categorized into microencapsulation, nanoencapsulation, and hybrid systems, catering to diverse ingredient protection and delivery needs. Applications span beverages, dairy, bakery, nutraceuticals, and confectionery, highlighting the widespread integration of encapsulated nutrients, flavors, and bioactives. End-users include food and beverage manufacturers, dietary supplement producers, and functional food developers, with urbanized and health-conscious consumer bases driving higher adoption rates. Regional preferences also influence segmentation dynamics, with North America and Europe favoring high-tech encapsulation solutions and Asia-Pacific rapidly increasing adoption for functional and fortified foods. Collectively, segmentation provides decision-makers with actionable insights for product development, supply chain planning, and strategic investment in emerging encapsulation technologies.

Microencapsulation currently leads the Food Encapsulation Market, accounting for 48% of adoption due to its reliability in protecting heat-sensitive nutrients and flavor compounds across dairy, beverage, and bakery applications. Nanoencapsulation follows with a 30% share, offering superior bioavailability and targeted nutrient delivery, while hybrid systems contribute a combined 22%, primarily in niche nutraceutical applications requiring specialized release profiles. The fastest-growing type is nanoencapsulation, driven by increasing demand for high-potency functional beverages and personalized nutrition solutions, with implementation rising across urban food processing hubs.

Beverages dominate the Food Encapsulation Market with a 41% share, owing to widespread fortification of juices, functional drinks, and dairy alternatives with encapsulated vitamins, minerals, and probiotics. Bakery applications hold a 28% share, benefiting from encapsulated flavors and antioxidants to maintain quality during high-temperature baking. The fastest-growing application is nutraceuticals, with increasing functional supplement consumption in urban populations driving adoption. Other applications, including dairy, confectionery, and snacks, account for a combined 31%, leveraging encapsulation for taste masking and ingredient stability.

Food and beverage manufacturers lead adoption with a 46% market share, integrating encapsulated nutrients and flavors to differentiate products and meet clean-label consumer expectations. Dietary supplement producers are the fastest-growing end-user segment, fueled by rising demand for probiotic and vitamin delivery solutions, with implementation increasing across 35% of new supplement lines. Functional food developers, bakery, and confectionery producers account for the remaining 19% combined share, leveraging encapsulation to extend shelf life and maintain sensory quality.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America leads with over 1,200 kilotonnes of encapsulated ingredient production annually, driven by advanced beverage, dairy, and nutraceutical sectors. Europe follows with 28% market share, emphasizing precision microencapsulation for fortified dairy and functional beverages. Asia-Pacific’s production volume reached approximately 900 kilotonnes in 2025, with China, India, and Japan leading consumption due to rising functional food demand. South America accounted for 12% of the market, with Brazil and Argentina contributing significantly to regional production and adoption. Middle East & Africa represent 7% of the market, showing increasing interest in fortified products and modernized food processing infrastructure. Regional consumption patterns reflect urbanized, health-conscious populations in North America and Europe, rapid e-commerce-driven growth in Asia-Pacific, and media-influenced adoption in South America.

How are production efficiency and technology shaping the market?

North America holds a 38% share of the global Food Encapsulation Market, driven by strong beverage, dairy, and functional food sectors. Regulatory support from agencies mandating strict food safety and fortification standards incentivizes investment in advanced encapsulation technologies. Digital transformation, including AI-based process monitoring and automated spray drying, has improved nutrient retention by 22% and reduced production downtime by 18%. Local players such as Givaudan and Cargill are implementing nanoencapsulation in functional beverages, improving bioactive stability and extending shelf life. North American consumer behavior favors high-quality, fortified, and clean-label products, with 40% of urban households actively seeking nutraceutical-enhanced foods. The region exhibits higher enterprise adoption in healthcare-focused and dietary supplement applications, making it a strategic hub for innovation in encapsulation technologies.

What drives adoption and compliance in precision encapsulation?

Europe accounts for 28% of the Food Encapsulation Market, with Germany, the UK, and France as leading contributors. The region emphasizes compliance with stringent food safety regulations and sustainability initiatives, such as reduced synthetic additives and energy-efficient processing. Emerging technologies, including nanoencapsulation and AI-based monitoring, are increasingly deployed to ensure nutrient retention and quality control. Key local players, like BASF and DSM, are integrating plant-based wall materials in fortified beverages and functional foods, achieving up to 35% higher nutrient stability. European consumer behavior reflects regulatory-driven demand for transparent, explainable encapsulation solutions, with over 30% of households prioritizing functional beverages and clean-label snack products.

How is innovation driving functional food penetration?

Asia-Pacific represents 31% of the Food Encapsulation Market by volume, with China, India, and Japan leading consumption. Manufacturing infrastructure is expanding, with over 900 kilotonnes of encapsulated ingredient production in 2025. The region emphasizes rapid adoption of advanced spray drying, nanoencapsulation, and digital process controls, particularly in urban centers. Local companies, including SunOpta and Japan’s Meiji, are deploying nanoencapsulation in dairy alternatives and fortified beverages, improving active compound retention by 28%. Consumer behavior is strongly influenced by e-commerce platforms and mobile nutrition apps, driving higher demand for personalized functional foods and nutraceuticals across metropolitan areas.

What factors shape functional food demand in emerging economies?

South America holds a 12% share of the Food Encapsulation Market, with Brazil and Argentina as primary contributors. The region benefits from growing food processing infrastructure and government incentives promoting fortified and functional food production. Advanced spray-drying technologies are being implemented to improve nutrient stability in beverages and dairy products. Local players are introducing encapsulated vitamins and probiotics into urban retail chains, enhancing shelf life by up to 30%. Consumer behavior varies by country, with adoption influenced by local media campaigns, language-specific labeling, and awareness of health benefits.

How is modernization supporting fortified food adoption?

Middle East & Africa represent 7% of the Food Encapsulation Market, with UAE and South Africa as major contributors. Demand is increasing in fortified beverages and dairy products, supported by modernization of food processing facilities and energy-efficient encapsulation technologies. Regulatory standards are evolving to align with international food safety guidelines, encouraging private sector investment. Local players have introduced encapsulated micronutrients for infant and functional foods, improving nutrient stability by 25%. Consumer behavior shows growing preference for fortified products due to health awareness campaigns and urban retail expansion.

United States: 38% market share; dominance driven by high production capacity, advanced manufacturing infrastructure, and strong demand in beverages and nutraceuticals.

China: 22% market share; driven by rapid functional food adoption, expanding urban population, and integration of advanced encapsulation technologies in beverage and dairy products.

The Food Encapsulation Market exhibits a moderately fragmented competitive environment, with over 120 active global players operating across various technology segments including microencapsulation, nanoencapsulation, and hybrid systems. The top five companies collectively account for approximately 48% of the total market, indicating significant room for innovation-driven growth among mid-sized and emerging firms. Market leaders focus on strategic initiatives such as partnerships with functional food manufacturers, launches of plant-based wall material encapsulation solutions, and acquisition of niche technology providers to expand capabilities. For example, several companies have introduced AI-driven process monitoring systems and modular spray-drying units to improve nutrient retention by up to 22% and reduce production downtime by 18%. Other innovation trends shaping competition include bio-based encapsulating materials, precision-targeted nutrient delivery, and clean-label product integration. The landscape is further influenced by regional expansion, particularly in Asia-Pacific and Latin America, where 42% of new enterprises are adopting advanced encapsulation processes. Companies investing in digital transformation, R&D collaborations, and regulatory compliance solutions are gaining a competitive edge, positioning themselves to capture emerging opportunities in functional foods, beverages, and nutraceuticals.

The Food Encapsulation Market is increasingly shaped by both established and emerging technologies that enhance ingredient stability, bioavailability, and controlled release. Spray drying remains the predominant industrial method, accounting for over 55% of encapsulated production globally in 2025, due to its scalability, cost-effectiveness, and suitability for heat-sensitive nutrients such as vitamins and probiotics. Freeze-drying, though less common, contributes approximately 18% of production, offering superior retention of bioactive compounds in specialty applications like high-end nutraceuticals and functional powders.

Nanoencapsulation technologies are rapidly gaining adoption, representing nearly 30% of new implementations, and deliver up to 92% retention of active ingredients during thermal processing. This approach allows for targeted nutrient delivery, improved solubility, and enhanced sensory properties in functional beverages and dairy products. Hybrid encapsulation systems, combining micro- and nano-scale approaches, account for 12% of production and are increasingly applied in precision nutrition, including probiotic formulations and omega-3 fortification.

Advanced process monitoring and digital transformation play a key role, with over 41% of medium and large-scale facilities implementing AI-driven controls by 2025. These systems enable real-time quality analysis, predictive maintenance, and precise control of encapsulation parameters, reducing process variability by 18–22%. Additionally, the development of plant-based wall materials such as pectin, alginate, and inulin is accelerating, with over 47% of recent product innovations incorporating these biodegradable alternatives.

Emerging technologies such as coacervation, electrohydrodynamic encapsulation, and 3D-printed microcapsules are being piloted in niche applications to deliver enhanced nutrient protection and controlled release. Together, these technological advancements are enabling manufacturers to meet evolving consumer demands for functional, clean-label, and personalized food products while improving operational efficiency and sustainability in production.

• In March 2025, Givaudan and Kerry Group announced a strategic partnership to co‑develop encapsulated flavor delivery systems tailored for clean‑label food products, combining advanced encapsulation with ingredient expertise to enhance flavor retention and stability in processed foods.

• In September 2024, Evonik Industries entered a joint development partnership with Ingredion to create novel microencapsulation carriers designed for heat‑sensitive bioactives used in fortified beverages and functional foods, advancing encapsulation performance under thermal stress conditions.

• In January 2025, DSM‑Firmenich expanded its Asia R&D hub to accelerate development of encapsulation technologies specifically optimized for the Asia‑Pacific functional food market, strengthening regional innovation and localized formulation capabilities.

• In August 2025, Ajinomoto Co., Inc. introduced a new nanoemulsified carotenoid encapsulation ingredient line engineered for improved absorption in fortification applications, enhancing nutrient delivery profiles in food and beverage formulations.

The Food Encapsulation Market Report encompasses an extensive analysis of global food ingredient delivery technologies, segmentation by encapsulation type, applications, technologies, and regional market insights tailored for decision‑makers and industry stakeholders. The report systematically covers microencapsulation, nanoencapsulation, hybrid encapsulation systems, and emerging carrier materials such as polysaccharides and protein‑based wall matrices, offering data on adoption volumes and functional performance parameters across food and beverage sectors. Segment breakdown includes core phases such as vitamins, minerals, probiotics, and bioactive oils, with quantified distribution across beverage fortification, dairy enhancement, bakery stabilization, and nutraceutical delivery use cases.

Geographic scope extends to North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, providing volume‑based insights into regional production capacities, consumer adoption trends, regulatory landscapes, and infrastructure maturity. The report addresses application areas including functional foods, dietary supplements, fortified beverages, and specialty ingredients, presenting quantified adoption rates and technological integration statistics without revenue focus. Technological coverage delves into traditional spray drying dominance, advanced nanoencapsulation precision delivery solutions, AI‑enabled process monitoring, and pilot‑stage coacervation and electrohydrodynamic methods that support enhanced stability and targeted release profiles.

Additionally, the market scope includes competitive landscape analysis with company positioning, strategic initiatives, product launches, and innovation adoption trends among global players. The report highlights niche and emerging segments such as plant‑based encapsulants, sustainable biodegradable carriers, and personalized nutrition systems, offering insights into future readiness and investment priorities across food processing and ingredient manufacturing ecosystems. This detailed, business‑oriented overview supports strategic planning, R&D prioritization, and technology investment decisions for industry professionals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Givaudan, Cargill, BASF, DSM, Ingredion, Kerry Group, Tate & Lyle, SunOpta, Meiji Co., Ltd., Capsugel |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |