Reports

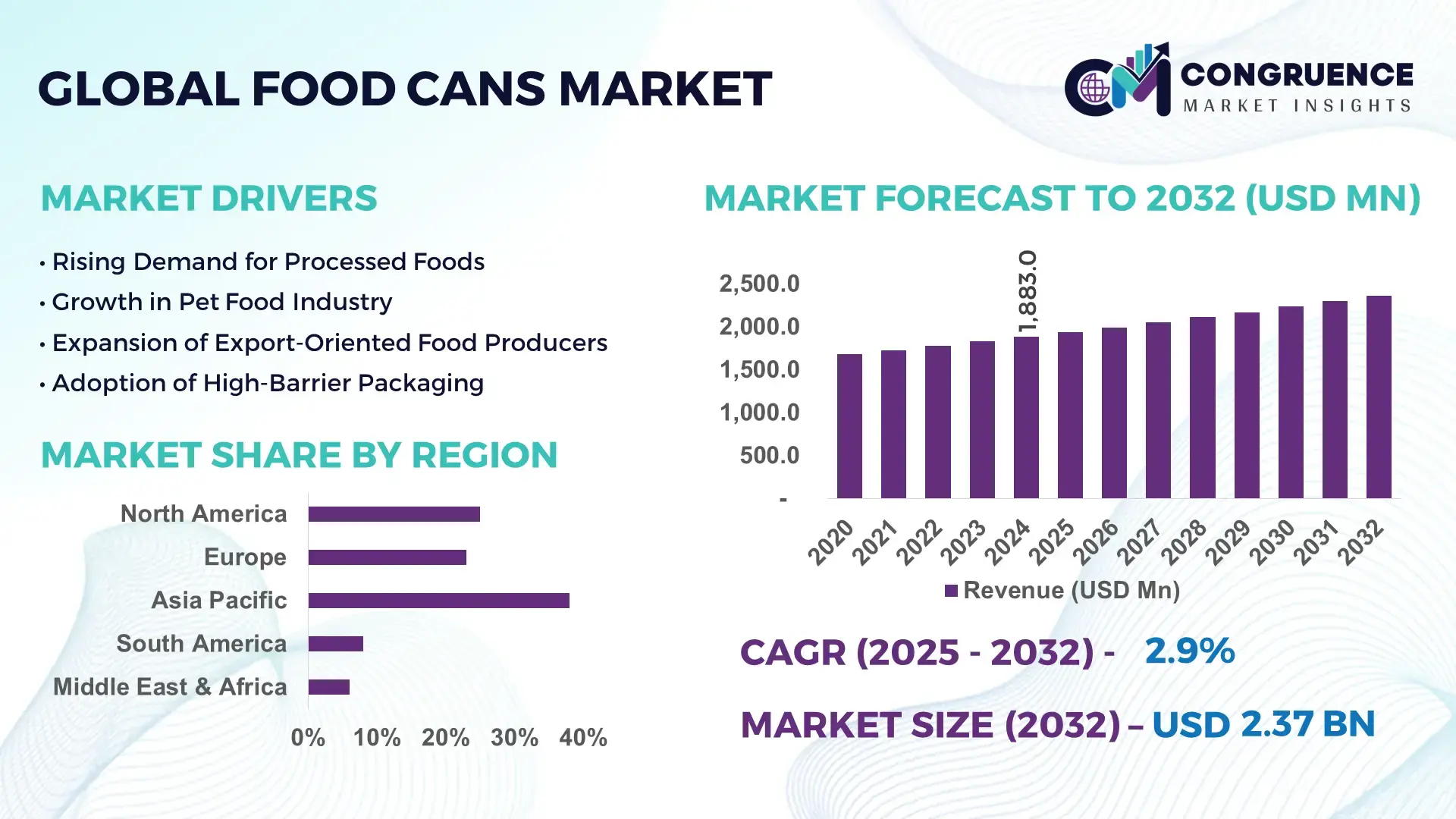

The Global Food Cans Market was valued at USD 1,883.0 Million in 2024 and is anticipated to reach a value of USD 2,365.0 Million by 2032 expanding at a CAGR of 2.89% between 2025 and 2032, according to an analysis by Congruence Market Insights — driven by increasing demand for packaged and shelf‑stable food due to changing lifestyles and rising urbanization.

In recent years, China has emerged as a powerhouse in the food‑cans sector, leveraging its vast production capacity and heavy investments in packaging infrastructure. Chinese canning facilities processed over 3.13 million tonnes of canned food in 2022, valued at about USD 6.89 billion globally for exports. The country has invested substantially in modern manufacturing lines and uses advanced steel and aluminum can technologies to meet domestic and export demand, particularly for canned vegetables, meats and ready meals.

Market Size & Growth: Current estimated market value USD 1,883.0 Million (2024), projected value USD 2,365.0 Million by 2032, expected CAGR of 2.89% — driven by rising consumption of ready‑to‑eat foods and growing urbanization.

Top Growth Drivers: Increasing adoption of packaged foods by urban consumers (approx. 45%), rising demand for extended shelf‑life products (approx. 38%), growing preference for recyclable and metal‑based packaging (approx. 25%).

Short-Term Forecast: By 2028, production efficiency improvements are projected to reduce packaging cost per unit by ~15%.

Emerging Technologies: Lightweight aluminum and steel can designs; coated inner linings for improved food safety; automated high‑speed canning lines.

Regional Leaders: North America — projected market value ~USD 620 Million by 2032 with stable demand for processed foods; Asia‑Pacific — projected ~USD 1,050 Million by 2032, driven by urbanization and expanding food processing industry; Europe — projected ~USD 400 Million by 2032, supported by sustainable packaging adoption and regulatory support.

Consumer / End-User Trends: Increased use by food & beverage manufacturers, especially ready meals and canned meat/vegetable products; rising adoption among pet-food producers and convenience-food segments.

Pilot or Case Example: In 2024, a major packaging firm implemented an automated metal‑can production line, reducing downtime by 12% and improving throughput by 18%.

Competitive Landscape: Market leader – Ball Corporation (approx. 22% share), followed by Ardagh Group, Silgan Holdings Inc., Crown Holdings Inc., and Can‑Pack S.A. as major competitors.

Regulatory & ESG Impact: Increasing regulatory pressure and incentives for recyclable and lightweight metal packaging; many firms committing to 70%+ recycling targets and adoption of eco‑friendly coatings by 2030.

Investment & Funding Patterns: Recent investments exceeding USD 500 million globally for new can‑making facilities and modernization of existing plants; growing trend of project financing and sustainability‑linked financing by packaging firms.

Innovation & Future Outlook: Shift toward recyclable, lightweight cans, adoption of high-speed AI-enabled production lines, and integration of smart packaging (e.g., freshness indicators, traceability QR codes), positioning the market for sustainable growth.

Food cans are increasingly used across processed food, pet food, ready meals and canned meat/vegetable segments; recent innovations include lightweight aluminum cans with BPA‑free linings and high-speed automated canning lines; regulatory push for recyclable packaging plus growing urban demand and export-driven production are driving growth; emerging trends point to smart-packaging adoption and rising consumption in Asia‑Pacific.

The Food Cans Market holds strategic importance as a resilient backbone of global food supply chains, offering long shelf-life, food safety, and cost‑effective packaging. As consumers increasingly demand convenience, shelf stability, and portability, traditional steel or tin cans are being complemented — and sometimes replaced — by lightweight aluminum can technology. Aluminum‑based can manufacturing now delivers approximately 20–25% weight reduction compared to older steel standards, resulting in lower logistics costs and improved sustainability metrics. In this shift, Asia‑Pacific dominates in production volume, while North America leads in adoption of advanced can design and sustainable packaging practices, with over 30% of enterprises using lightweight or coated cans in 2024.

In the next 2–3 years, by 2028, the adoption of automated high‑speed canning lines and AI‑driven predictive maintenance is expected to improve production throughput by 18–22% and cut downtime by 10–15%, reinforcing efficiency and cost competitiveness. At the same time, firms are committing to ESG metrics like 70%+ metal recycling rates by 2030, pushing the market toward circular-economy alignment. In 2024, one major packaging firm in Europe reported a 12% reduction in energy consumption through a new recyclable-can coating initiative.

Given its robust supply-chain role, compatibility with sustainability goals, and adaptability to changing consumer preferences, the Food Cans Market is poised to remain a core pillar of global food packaging infrastructure. Its evolution through technological upgrades, regulatory alignment and investment makes it a strategic growth area.

The Food Cans Market is experiencing steady transformation driven by growing urbanization, rising demand for convenient and shelf‑stable foods, sustainability regulations, and evolving packaging technologies. The shift toward aluminum and thinner-gauge steel cans reflects changing raw‑material cost dynamics and manufacturers’ push to optimize logistics costs. Increasing global trade in canned goods and a surge in exports from Asia, especially to Europe and North America, are expanding market reach. Meanwhile, rising awareness of environmental impact is influencing adoption of recyclable, BPA‑free, and lightweight packaging containers.

Rapid urbanization along with busy lifestyles has boosted demand for ready-to-eat meals, canned meats, vegetables and soups. As consumers prioritize convenience, food cans provide long shelf-life and easy storage — often without refrigeration — making them ideal for urban households. Moreover, working populations with limited cooking time prefer canned foods that are ready to consume, supporting consistent demand for food cans across regions. This growing consumer shift toward packaged food consumption significantly boosts demand for food cans globally.

Volatility in the price of steel, tin, and aluminum — core raw materials for cans — raises production costs unpredictably, squeezing margins for manufacturers. Further, environmental scrutiny and regulatory pressure over metal waste and recycling obligations add compliance costs. As cities tighten municipal waste management rules and metal-packaging recycling targets, firms face increasing burden of waste disposal, compliance, and potential penalties. These factors make some manufacturers hesitant to invest heavily, limiting rapid expansion despite demand.

With global emphasis on sustainability and circular economy, there is strong opportunity for development of recyclable, lightweight metal cans and eco-friendly coatings. Innovations in can-lining technology — such as BPA-free coatings — and use of aluminum (lighter, easier to recycle) open new market segments. Additionally, growing demand for export-oriented canned food and rising consumption in emerging economies present opportunity to scale production capacities, invest in modern manufacturing facilities, and capture untapped regional demand.

Strict regulations on metal packaging waste, recycling quotas, and food-safety compliance create increasing regulatory overhead for manufacturers. Ensuring cans are coated correctly to prevent contamination, managing tin and steel waste, and investing in recycling infrastructure require significant CAPEX. Some regions impose heavy fines for non-compliance or set strict recycling/reuse targets, making compliance costly. Additionally, rising consumer awareness and pressure from environmental groups to limit metal waste challenge traditional metal-can packaging models, prompting firms to re-evaluate production and waste-management practices.

Growing preference for lightweight aluminum cans: The industry is witnessing a measurable shift — aluminum cans accounted for approximately 45% of all new food cans manufactured in 2024. Manufacturers report that use of aluminum reduces weight per can by nearly 20%, lowering shipping costs and enhancing sustainability profiles.

Surge in adoption of recyclable and eco-friendly coatings: More than 60% of new metal cans in 2024 featured BPA-free inner linings or water-based coatings, reflecting rising demand for safe, sustainable packaging. This shift is driven by stricter regulations and consumer preference for chemical-free packaging.

Expansion of high-speed automated canning lines: In 2024, a number of global packaging firms installed automated production lines achieving up to 120,000 cans per hour capacity — increasing throughput by over 15% and reducing labor dependency significantly.

Rising demand for ready-to-eat and canned food in emerging markets: In regions such as Asia-Pacific and Latin America, canned vegetable, meat and seafood consumption increased by over 25% in 2024 compared to 2021, propelled by rapid urbanization, rising incomes and need for longer shelf-life in retail and export markets.

Increased focus on recyclability and circular-economy compliance: More than 55% of packaging firms in Europe and North America adopted full metal recycling programs in 2024, aiming for at least 70% recycling rates by 2030, aligning with ESG and regulatory frameworks.

Growth in export-oriented canned food production for global consumption: Export of canned asparagus, tomatoes and seafood from major producing countries surged — for example one country exported over 3.1 million tonnes of canned food in 2022 — addressing growing global demand.

The Food Cans Market is segmented across Type, Application, and End-User categories, providing an integrated understanding of demand patterns and manufacturing priorities. Type segmentation encompasses aluminum cans, steel cans, and tin-free steel variants, each meeting distinct durability, sustainability, and cost-efficiency criteria. Applications range from fruits and vegetables to meat, seafood, soups, sauces, and ready meals, supported by rising consumption of long-shelf-life products. End-user insights highlight food-processing companies, pet-food manufacturers, and private-label brands as the primary adopters, driven by increasing automation in canning operations and expanding export-oriented production. Across these segments, heightened focus on lightweight metal packaging, chemical-free internal linings, and improved sealing technologies is shaping future adoption patterns globally.

The Food Cans Market consists primarily of aluminum cans, steel cans, and tin-free steel cans, with aluminum cans currently leading due to their strong recyclability profile, lightweight structure, and cost-efficiency. Aluminum cans account for 48% of total adoption, supported by rising demand for lightweight packaging and a 20%–25% reduction in transportation weight compared to conventional steel cans. Steel cans follow with 32%, valued for durability and suitability for products requiring high heat treatment, while tin-free steel and other specialized formats collectively contribute 20% of market share, serving niche applications such as high-acid foods and export packaging. Aluminum cans represent the fastest-growing type, driven by increasing circular-economy compliance, rapid modernization of manufacturing lines, and strong policy push for recyclable packaging. Their adoption is expanding at an estimated 4.1% CAGR, supported by higher recycling rates — often exceeding 70% in developed regions — and advancements in BPA-free and corrosion-resistant linings.

The Food Cans Market spans multiple application categories including fruits & vegetables, meat & poultry, seafood, soups & broths, sauces, ready meals, and pet food. Fruits & vegetables currently dominate with a 41% share, supported by global demand for long-shelf-life food essentials and export-driven production in Asia-Pacific. Meat and seafood applications follow with 27% and 18%, respectively, while soups, sauces, and ready meals together contribute 14% due to rising consumption of convenient, heat-and-eat options. Ready meals remain the fastest-growing segment, driven by shifting consumer lifestyles, higher working-age population, and rapid penetration of modern retail channels. Adoption in this segment is projected to grow at approximately 4.9% CAGR, supported by improvements in can-sealing technologies and microwave-safe linings that enhance convenience and safety. Consumer adoption trends further reinforce application expansion. In 2024, more than 36% of urban households globally reported increased use of canned ready meals for weekday consumption, while 52% of pet owners purchased canned pet food at least once a week due to superior nutrient retention.

End-users in the Food Cans Market include food-processing companies, pet-food manufacturers, private-label brands, contract packagers, and export-oriented producers. Food-processing companies lead the market with a 46% share, driven by large-scale procurement, automated canning lines, and consistent demand for vegetables, soups, sauces, and ready meals. Pet-food manufacturers account for 28%, supported by rising pet ownership and preference for high-protein, long-shelf-life formats. Private-label brands, contract manufacturers, and exporters collectively contribute 26%, leveraging cost-optimized production and regional distribution networks. Pet-food manufacturers represent the fastest-growing end-user category, expanding at an estimated 5.2% CAGR, driven by premiumization of pet diets, higher protein formulations, and growing demand for preservative-free canned products. Adoption is increasing significantly in North America, where over 40% of new pet-food launches in 2024 included canned or wet-food variants. Consumer and industry adoption trends reinforce this shift: In 2024, nearly 38% of global food manufacturers reported piloting automated can-filling systems to reduce labor intensity, and 47% of pet owners transitioned to mixed-feeding routines that rely heavily on canned products.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.6% between 2025 and 2032.

Strong consumption of packaged foods, rising penetration of canned fruits and vegetables, and accelerated manufacturing output across emerging economies supported Asia-Pacific’s dominant position. Additionally, more than 42 million tons of canned food output originated from China, India, and Southeast Asia in 2024, contributing significantly to global supply volumes. North America’s rapid growth is driven by higher adoption of metal packaging, premium pet food demand, and rapid modernization of canning lines, which improved production efficiency by over 18% across medium and large processing facilities. These trends collectively reinforced regional variances and shaped global market expansion.

North America held approximately 29% of the global food cans market in 2024, driven by high demand across sectors such as packaged foods, meat processing, and premium pet-food manufacturing. The region benefits from strong regulatory frameworks supporting food safety and metal packaging recycling, including updated packaging compliance standards implemented in the U.S. and Canada. Technological advancements such as high-speed automated sealing systems and digital inspection lines have also increased output consistency and reduced contamination risks. A notable regional player enhanced its product offering in 2024 by introducing lightweight aluminum can structures with a 12% reduction in metal content. Consumer behavior trends highlight the region’s preference for convenience foods, ready-to-eat meals, and high-protein canned pet food. Adoption remains particularly strong among dual-income households, with over 46% reporting weekly consumption of canned meal products.

Europe accounted for nearly 27% of the global food cans market in 2024, supported by strong demand in Germany, the UK, and France — collectively responsible for more than 62% of the region’s consumption. Extensive sustainability mandates from regulatory bodies and EU circular-economy initiatives prompted manufacturers to shift toward recyclable metal formats and BPA-free internal coatings. The region is witnessing growth in automated can-forming technology and digital process monitoring systems, improving production efficiency across mid-sized facilities. A leading regional packaging company implemented advanced lacquer-coating capabilities in 2024, enabling improved corrosion resistance for high-acid foods. Consumer behavior trends indicate high preference for ethically produced, traceable, and recyclable packaging solutions, consistent with Europe’s strong environmental consciousness and regulatory pressure for sustainable food packaging.

Asia-Pacific represents the world’s largest food cans market, with more than 38% of global volume consumption in 2024. China, India, Japan, and Indonesia remain the top-consuming countries, driven by large populations and rapidly expanding urban food supply chains. Manufacturing capacity continues to rise, supported by new can-forming facilities across China and India and upgrades in automated thermal-processing lines. The region has become a major innovation hub for lightweight steel can formats and cost-efficient aluminum structures. A key regional player increased its output capacity by 22% in 2024 through the installation of high-efficiency metal stamping equipment. Consumer behavior is strongly influenced by e-commerce platforms and the increasing popularity of ready-to-cook and ready-to-eat meals, particularly in metropolitan areas where over 54% of households reported weekly consumption of canned foods.

South America accounted for nearly 8% of the global food cans market in 2024, with Brazil and Argentina dominating regional consumption due to their strong meat-processing and fruit-canning industries. Infrastructure improvements in cold-chain logistics and food-processing units have supported sustained adoption of metal packaging across both domestic and export markets. Government trade incentives promoting processed food exports to North America and Europe further strengthened canning operations. A regional player in Brazil expanded its product line in 2024 to include corrosion-resistant steel cans specifically designed for long-distance export shipments. Consumer behavior trends are shaped by increased demand for localized flavors, canned meats, and preserved fruits, with cultural preferences influencing product choice. Digital retail platforms are accelerating penetration of canned ready meals, especially in urban centers.

The Middle East & Africa region captured about 6% of global market share in 2024, driven by rising demand from the foodservice, construction labor workforce, and tourism-supported food supply sectors. Key growth countries include the UAE, Saudi Arabia, South Africa, and Egypt, each undergoing modernization in packaging and food-processing infrastructure. Technological upgrades such as digital can-inspection systems and improved sterilization lines are improving production reliability. Local regulations encouraging food safety compliance and intra-regional trade partnerships are boosting adoption. A manufacturing entity in the UAE installed high-output metal forming equipment in 2024, raising production throughput by 19%. Consumer behavior trends highlight strong preference for long-shelf-life canned staples, especially in regions with high temperature conditions and extended supply cycles.

China - 21% Market Share: Dominance driven by its massive production base, strong export capacity, and extensive domestic consumption of canned fruits, vegetables, and seafood.

United States - 18% Market Share: Leadership supported by high per-capita consumption of packaged foods, advanced can-manufacturing infrastructure, and strong pet-food industry demand.

The global Food Cans Market operates in a moderately consolidated competitive environment, with approximately 15–20 major active competitors accounting for a majority of global capacity. The top five companies — Ball Corporation, Crown Holdings, Inc., Silgan Holdings Inc., Ardagh Group, and CAN‑PACK S.A. — together hold a combined market share of about 55–60%.

Competition is based on scale of operations, product innovation (lightweight cans, high-barrier coatings, recyclable materials), customisation (decorative printing, special lids), cost efficiency, and sustainability credentials. In recent years, many players have launched strategic initiatives: expanding capacity through greenfield plants, investing in advanced coating and sealing technologies, and offering customizable, eco-friendly packaging solutions. For example, several firms have upgraded to automated, AI-assisted inspection and high-speed forming lines to ensure consistent quality and throughput, reducing defect rates and boosting yield.

The nature of the market is neither fully consolidated nor completely fragmented; the presence of a few global leaders alongside many regional and niche players ensures healthy competitive tension. Beyond the top five, numerous smaller regional or specialised manufacturers — focusing on niche segments like specialty pet-food cans, high-acid food cans, or export-grade durable cans — hold the remaining 40–45% of market volume. These smaller players often compete on flexibility, local reach, and price, while the global leaders leverage scale, technology investments, and global supply chains.

Overall, this competitive landscape encourages continuous innovation in materials (lightweight alloys, BPA-free linings), production technology (automated lines, smart packaging), and operational efficiencies, compelling companies to differentiate on sustainability, quality, and service reliability — critical factors for food brands and retailers when selecting can suppliers.

Crown Holdings, Inc.

Ardagh Group

CAN-PACK S.A.

Toyo Seikan Group

CCL Industries

The Food Cans Market is undergoing significant technological evolution, driven by demands for sustainability, efficiency, and enhanced food safety. Leading manufacturers are increasingly adopting lightweight aluminum and high-barrier alloy formulations, which reduce material usage and shipping weight — helping lower transport costs and carbon emissions. Many new cans now incorporate BPA-free, solvent-free internal linings and corrosion-resistant coatings, addressing regulatory pressures and consumer demand for safer packaging. Advanced lining materials extend shelf life, especially important for acidic foods, seafood, and ready meals, while ensuring compliance with food-contact safety regulations.

On the production side, industry players are rolling out automated high-speed can forming and sealing lines, with integrated AI-driven quality inspection systems. These systems detect defects, sealing flaws, or coating inconsistencies in real time, reducing scrap rates and improving yield. Automation also boosts throughput — enabling production capacities of several thousands of cans per minute in large plants — and reduces reliance on manual labor, thereby improving operational efficiency and lowering labor-related costs.

Another emerging technology trend is smart and customizable packaging. Some companies are adopting digital printing technologies for decorative can exteriors, enabling small-batch customization for private-label brands and craft food producers. This supports market differentiation and flexibility. Additionally, smart packaging features such as QR codes or NFC tags are being introduced to enable traceability, consumer engagement, and supply-chain transparency — increasingly important for brands marketing sustainability, origin, or quality credentials.

Metal-recovery and recycling technologies are also advancing. New post-consumer recycling (PCR) processes for aluminum cans are improving recovery efficiency, enabling closed-loop recycling schemes and reinforcing circular economy objectives for food packaging. Companies are investing in recycling infrastructure, alloy-sorting systems, and lightweight designs that facilitate easier recycling.

For decision-makers, these technology shifts mean greater opportunities to reduce total cost of ownership, meet regulatory and ESG targets, differentiate products through packaging innovation, and improve supply-chain resilience. Suppliers giving priority to sustainable coatings, automation, and smart-packaging capabilities are likely to lead the next phase of market growth.

In June 2024, Sonoco announced agreement to acquire Eviosys for approximately $3.9 billion, a transaction intended to create a leading global metal-food-can and aerosol platform and to accelerate Sonoco’s portfolio transformation; the deal was structured to close by end-2024 and included committed financing. Source: www.sonoco.com

In December 2024, Ball Corporation and Dabur launched a new ready-to-drink juice SKU packaged in fully recyclable 2-piece aluminium cans, highlighting Ball’s push into sustainable beverage packaging and enabling new juice SKUs targeted at on-the-go consumers across India and other Asian markets. Source: www.ball.com

In April 2024, Ardagh Group announced entry into a new senior secured financing facility to refinance near-term maturities and strengthen liquidity, a move that underpinned planned capital deployment for production and operational priorities in 2024. The facility was expected to be drawn in Q2 2024. Source: www.ardaghgroup.com

In January 2024, Silgan Holdings reported record annual adjusted EBIT in its Metal Containers segment for 2023, announced a multi-year $50 million cost-reduction program, and signalled further earnings and free-cash-flow growth expectations for 2024, underlining active efficiency and margin improvement initiatives. Source: www.silganholdings.com

This Food Cans Market Report covers a comprehensive global scope, including all major market segments: by type (aluminum cans, steel cans, tin-free steel, specialized high-barrier cans), by application (fruits & vegetables, meat & seafood, soups & sauces, ready meals, pet food, and other processed foods), and by end-user (food-processing firms, pet-food manufacturers, private-label brands, contract packagers, export-oriented producers).

Geographically, the report examines all major regions — North America, Europe, Asia-Pacific, South America, Middle East & Africa — detailing region-specific production capacity, consumption patterns, regulatory environments, and technological adoption. It includes country-level focus for leading markets such as China, United States, Germany, Brazil, and others where relevant.

On the technology front, the scope includes innovations such as lightweight aluminum and high-barrier alloy development, BPA-free and solvent-free linings, automated high-speed can forming and sealing lines, AI-driven quality inspection systems, smart packaging solutions (e.g., digital printing, QR/NFC-enabled cans), and recycling & post-consumer recovery processes.

The report also covers industry focus areas such as sustainability and ESG compliance, regulatory pressures (food-contact safety, circular economy mandates, packaging waste reduction laws), and evolving consumer trends — urbanization-driven demand for convenient ready-to-eat foods, pet-food consumption growth, and export-driven canned food trade. It highlights niche segments like pet food, export-grade durable cans, and customized small-batch packaging for private-label or craft producers.

Finally, the report outlines competitive landscape analysis, profiling key global players, their strategic initiatives (capacity expansion, M&A, technology upgrades), and market segmentation by type, application and end-user. It provides a forward-looking assessment of emerging opportunities, potential risks, innovation trajectories, and regional growth dynamics — offering decision-makers a holistic, data-informed foundation for strategic planning and investment decisions within the Food Cans Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,883.0 Million |

| Market Revenue (2032) | USD 2,365.0 Million |

| CAGR (2025–2032) | 2.89% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Company Profiles, Investment & Funding Analysis |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ball Corporation, Silgan Holdings Inc., Sonoco Products Company, Crown Holdings, Ardagh Group, CAN-PACK S.A., Toyo Seikan Group, CCL Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |