Reports

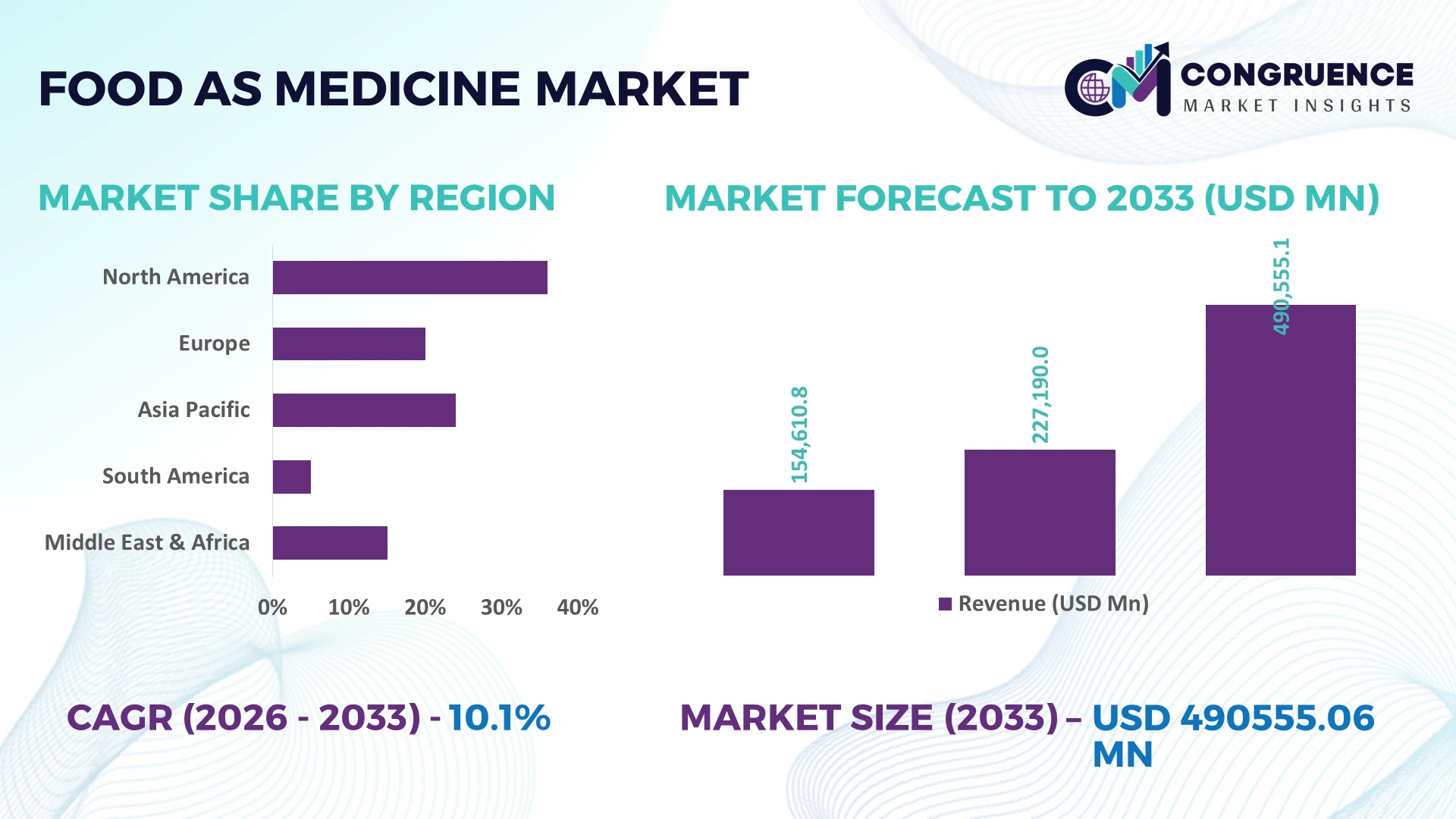

The Global Food as Medicine Market was valued at USD 227190 Million in 2025 and is anticipated to reach a value of USD 490555.06 Million by 2033 expanding at a CAGR of 10.1% between 2026 and 2033. Growth is driven by expanding clinical nutrition programs, precision nutrition technologies, rising metabolic disease management, and stronger integration of medically tailored foods into preventive healthcare systems.

The United States leads the global Food as Medicine Market with approximately 36% market share, supported by over USD 3 billion in nutrition-focused healthcare investments, widespread digital nutrition platforms, and strong adoption across hospitals and retail health networks. Compared with Germany, where preventive nutrition programs continue expanding under European health initiatives, the U.S. demonstrates faster commercialization and nearly 65% adoption of digital dietary management solutions. Ongoing healthcare resilience efforts following global supply-chain disruptions have accelerated localized ingredient sourcing and functional food manufacturing capacity.

Strategic investments in clinically validated nutrition products, digital health integration, and resilient supply chains will define long-term competitive positioning across the global Food as Medicine Market.

Market Size & Growth: USD 227190 Million (2025) to USD 490555.06 Million (2033) at 10.1% CAGR, driven by precision nutrition, clinical food innovation, and healthcare integration.

Top Growth Drivers: Clinical nutrition adoption (+34%), preventive healthcare spending (+29%), functional ingredient demand (+26%).

Short-Term Forecast: By 2028, personalized nutrition delivery efficiency improves 24% through AI-enabled dietary planning and optimized distribution.

Emerging Technologies: AI nutrition analytics, microbiome-based formulations, and wearable health integration accelerate advanced product development.

Regional Leaders: North America leads above USD 170 billion, Europe exceeds USD 135 billion, Asia-Pacific surpasses USD 120 billion with rapid healthcare digitization.

Consumer/End-User Trends: More than 58% of health-conscious consumers actively purchase functional food products supporting disease prevention and wellness.

Pilot/Case Example: 2026 hospital nutrition initiative reduced patient nutrition-related readmissions by 18% through medically tailored meal programs.

Competitive Landscape: Leading companies collectively account for approximately 38% market share, supported by Nestlé Health Science, Danone, Abbott, Herbalife, and DSM-Firmenich.

Regulatory & ESG Impact: Sustainable ingredient sourcing reduced production-related emissions by nearly 17% while strengthening compliance with nutrition labeling standards.

Investment & Funding: More than USD 6 billion supports partnerships, manufacturing expansion, digital nutrition platforms, and clinical food innovation amid regional supply-chain diversification.

Innovation & Future Outlook: Advanced personalized nutrition, bioactive ingredients, and AI-driven dietary recommendations strengthen long-term healthcare-focused business strategies.

Growing demand for medically tailored meals, functional beverages, personalized supplements, and microbiome-based nutrition is reshaping the Food as Medicine Market. AI-enabled dietary assessment, precision formulation, and clinically validated functional ingredients are improving patient outcomes, while nearly 42% of new product launches emphasize preventive health benefits. Regulatory alignment and regional ingredient localization continue strengthening operational resilience, setting the stage for deeper strategic market evaluation.

The Food as Medicine Market has become a strategic priority as healthcare systems shift from treatment-focused models toward preventive nutrition supported by clinical evidence. Regulatory recognition of medically tailored nutrition, expanding digital health ecosystems, and localized ingredient sourcing are reshaping competitive positioning across food, pharmaceutical, and healthcare industries. Companies are integrating nutrition science with healthcare delivery while restructuring supply chains to improve traceability, ingredient consistency, and regulatory compliance.

AI-enabled nutrition platforms process dietary assessments nearly 45% faster than conventional manual consultation models while reducing nutrition planning costs by approximately 22%, enabling scalable personalized interventions. The United States leads clinical deployment through integrated healthcare providers and digital nutrition platforms, whereas Japan emphasizes aging-focused functional nutrition supported by advanced food science and precision manufacturing. Over the next two to three years, more than 35% of large healthcare organizations are expected to incorporate digitally supported nutrition management into chronic disease care pathways.

Hospital systems partnering with food manufacturers and digital health providers increasingly deploy medically tailored meal programs linked with remote patient monitoring, improving treatment adherence and operational efficiency. Companies are expanding investments in clinical validation, AI-powered nutrition platforms, and ingredient innovation while strengthening strategic partnerships across healthcare networks. Organizations establishing integrated nutrition ecosystems and resilient sourcing capabilities will secure stronger competitive differentiation and long-term operational advantage.

Healthcare providers are embedding evidence-based nutrition into chronic disease management, creating sustained demand for clinically validated food products and personalized nutrition services. Approximately 62% of major hospital networks now evaluate nutrition interventions alongside conventional therapies, while AI-assisted dietary assessment improves care planning efficiency by nearly 40%. The United States continues expanding reimbursement pilots supporting medically tailored meals, encouraging broader commercial adoption. In response, food manufacturers, digital health companies, and ingredient suppliers are investing in clinical research, strategic healthcare partnerships, and specialized manufacturing facilities. A key strategic shift involves combining nutrition data with electronic health records, enabling differentiated patient outcomes and strengthening long-term product competitiveness.

Scientific validation requirements and inconsistent functional ingredient quality remain significant operational barriers. Clinical substantiation can extend product development timelines by approximately 25%, while premium bioactive ingredient costs remain 18–24% above conventional food inputs. Canada and several European countries continue enforcing stricter health-claim requirements, increasing compliance complexity for multinational suppliers. Variable agricultural output also affects botanical ingredient consistency and procurement planning. Companies are reducing exposure through diversified sourcing networks, localized ingredient processing, long-term supplier agreements, and standardized quality management systems. Strong supply governance has become an operational differentiator for maintaining product reliability and protecting commercial margins.

AI-driven nutrition platforms, microbiome analytics, and continuous health monitoring are creating scalable commercial opportunities beyond traditional functional foods. Digital nutrition engagement improves personalized dietary adherence by nearly 32%, while precision nutrition recommendations increase intervention effectiveness by approximately 28%. India is expanding digital healthcare infrastructure, supporting broader deployment of preventive nutrition services through connected health platforms. Companies are accelerating investment in microbiome research, digital therapeutics partnerships, and personalized product portfolios targeting metabolic disorders. A notable strategic opportunity lies in integrating wearable health data with nutrition planning, enabling subscription-based preventive care models and stronger long-term customer retention.

Expanding Food as Medicine programs requires coordinated healthcare infrastructure, interoperable digital systems, and qualified nutrition professionals. Nearly 37% of healthcare providers continue using fragmented nutrition data workflows, limiting coordinated patient management, while specialized clinical nutrition workforce shortages exceed 20% in several developed healthcare systems. Germany and other advanced healthcare markets face integration challenges between hospital information systems and external nutrition platforms. Companies must invest in interoperable digital architecture, workforce development, standardized clinical protocols, and secure health data management. Organizations solving integration complexity while maintaining consistent clinical outcomes will achieve stronger operational resilience and sustainable competitive positioning.

AI-Enabled Nutrition Planning: Healthcare providers are embedding AI-powered nutrition engines into clinical workflows, reducing personalized meal planning time by nearly 42% while improving dietary adherence by approximately 29%. U.S. health systems are integrating nutrition recommendations with electronic health records following broader digital healthcare adoption, allowing companies to expand software partnerships, automate patient monitoring, and streamline clinical nutrition delivery.

Localized Ingredient Sourcing Expands: Manufacturers are restructuring procurement networks as supply-chain resilience becomes a strategic priority, increasing regional ingredient sourcing by nearly 31% and reducing procurement lead times by about 18%. European producers are strengthening partnerships with domestic agricultural suppliers, improving traceability and ingredient consistency while lowering logistics exposure through localized production and long-term sourcing agreements.

Clinical Validation Gains Momentum: Evidence-backed nutrition products are replacing generalized wellness formulations as hospitals require stronger clinical outcomes. More than 48% of newly introduced therapeutic nutrition products now include clinical validation, while enterprise investment in nutrition research has increased by roughly 24%. Companies are expanding collaborations with research institutions and healthcare providers to accelerate product acceptance and improve reimbursement opportunities.

Personalized Functional Foods Accelerate: Precision nutrition supported by microbiome analysis and wearable health devices is reshaping product development, with personalized nutrition subscriptions increasing approximately 36% and digital consumer engagement improving nearly 27%. Japan and South Korea are accelerating commercial deployment through integrated health ecosystems, prompting companies to automate formulation processes, expand customized product portfolios, and strengthen direct-to-consumer digital channels.

Functional Foods remain the dominant segment due to broad consumer acceptance, retail scalability, and seamless integration into daily dietary habits. They account for approximately 39% of market consumption as manufacturers expand clinically supported formulations targeting metabolic health, cardiovascular wellness, and immune function. Fortified Foods continue strengthening public health initiatives, while Dietary Supplements retain importance through convenient dosage formats and specialized nutrient delivery. Companies are expanding manufacturing capacity, reformulating products with cleaner ingredient profiles, and strengthening retail partnerships to improve accessibility and repeat purchases.

Medical Foods represent the fastest-growing type as healthcare providers increasingly prescribe disease-specific nutritional interventions supported by clinical evidence. Adoption across chronic disease management programs has expanded by nearly 26%, while investment in therapeutic nutrition research has increased approximately 22%. Nutraceuticals continue gaining traction through precision ingredient innovation and microbiome-focused formulations. Companies are prioritizing clinical validation, pharmaceutical partnerships, and advanced formulation technologies, shifting investment toward products capable of delivering measurable health outcomes alongside regulatory compliance.

Diabetes Management remains the leading application because healthcare providers increasingly integrate nutrition therapy into long-term disease management programs. Approximately 35% of clinically targeted nutrition products focus on blood glucose management, supported by continuous glucose monitoring and personalized dietary recommendations. Heart Health maintains a mature position through cholesterol-lowering and cardiovascular-support formulations, while Immune Support continues stable demand across preventive healthcare channels. Companies are expanding evidence-based product portfolios and integrating digital nutrition tracking into disease management services.

Weight Management is the fastest-growing application as AI-guided nutrition planning, metabolic monitoring, and personalized meal programs become more widely deployed. Adoption of digitally supported weight management solutions has increased by approximately 30%, while personalized nutrition engagement has improved nearly 25%. Digestive Health is also expanding through microbiome-focused innovation and probiotic development. Companies are strengthening healthcare collaborations, deploying personalized nutrition platforms, and increasing investment in clinically differentiated formulations to capture long-term preventive healthcare demand.

Hospitals represent the largest end-user segment because they integrate medically tailored nutrition into inpatient care, chronic disease management, and post-discharge recovery pathways. Nearly 41% of clinically prescribed nutrition programs originate within hospital networks, supported by multidisciplinary care teams and digital patient monitoring systems. Clinics continue expanding outpatient nutrition services, while Pharmacies strengthen accessibility through specialized therapeutic nutrition offerings. Companies are responding by developing hospital-specific formulations, strengthening healthcare partnerships, and expanding clinical distribution networks.

Retail Consumers represent the fastest-growing end-user group as preventive healthcare awareness, digital nutrition platforms, and personalized wellness programs reshape purchasing behavior. Direct-to-consumer nutrition subscriptions have increased by approximately 33%, while digital health engagement has improved nearly 28%. Wellness Centers and Long-Term Care Facilities are also increasing nutrition-focused services for aging populations and chronic disease prevention. Companies are investing in personalized product portfolios, omnichannel distribution strategies, and subscription-based nutrition ecosystems to strengthen customer retention and long-term market positioning.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 12.4% CAGR between 2026 and 2033.

Clinical nutrition integration strengthens healthcare delivery

North America maintains leadership through advanced healthcare infrastructure, established clinical nutrition programs, and strong collaboration between healthcare providers and food manufacturers. The region contributes approximately 38.4% of global market activity, supported by widespread deployment of digital nutrition platforms and medically tailored meal programs across integrated health systems. More than 60% of large hospital networks have incorporated nutrition management into chronic disease care pathways, improving patient engagement and treatment coordination. Enterprise partnerships between food technology firms, insurers, and healthcare organizations continue expanding product accessibility while investments in precision nutrition platforms accelerate operational efficiency and clinically validated product commercialization.

United States Market Outlook: The United States remains the regional growth engine because of its mature healthcare ecosystem, advanced digital health infrastructure, and strong clinical research capabilities. More than 65% of leading healthcare providers utilize digital nutrition management tools alongside chronic disease programs, encouraging wider deployment of personalized nutrition services. Domestic manufacturers continue expanding functional ingredient production, AI-enabled dietary assessment platforms, and strategic partnerships with hospitals, strengthening commercialization and long-term competitive positioning.

Preventive healthcare policies reshape commercial adoption

Europe benefits from robust food safety regulations, preventive healthcare initiatives, and growing demand for clinically supported functional nutrition. The region represents nearly 28% of global market activity, with healthcare systems increasingly incorporating nutrition-based interventions into long-term disease management. Regulatory harmonization has encouraged broader commercialization of evidence-backed products, while localized ingredient sourcing has improved supply stability by approximately 18%. Companies continue investing in sustainable manufacturing, clean-label innovation, and research collaborations that strengthen product differentiation and regulatory compliance across mature consumer markets.

Germany Market Outlook: Germany leads regional development through advanced food manufacturing capabilities, nutrition science research, and strong industrial collaboration between healthcare and food companies. Nearly 52% of large food innovation projects incorporate clinically validated ingredients or functional health claims, supporting premium product development. Companies continue investing in precision fermentation, ingredient traceability technologies, and pharmaceutical partnerships, reinforcing Germany's position as a strategic innovation hub for evidence-based nutrition solutions.

Manufacturing scale accelerates personalized nutrition

Asia-Pacific is emerging as the fastest-expanding regional market through expanding healthcare infrastructure, large-scale food manufacturing capacity, and increasing adoption of preventive nutrition. The region contributes roughly 24% of global demand while production of functional nutrition ingredients continues expanding to support domestic and export markets. Investment in digital healthcare platforms has increased by approximately 30%, enabling broader deployment of personalized nutrition services. Food manufacturers are strengthening automation, localized production, and cross-border partnerships to improve supply resilience and product availability across rapidly urbanizing economies.

China Market Outlook: China dominates regional manufacturing through extensive functional food production capacity, integrated ingredient supply chains, and supportive nutrition innovation policies. More than 40% of newly commissioned production facilities incorporate intelligent manufacturing technologies that improve quality consistency and production efficiency. Domestic enterprises continue expanding microbiome research, digital nutrition platforms, and international partnerships, strengthening export competitiveness while supporting rising preventive healthcare adoption across urban populations.

Preventive nutrition gains commercial traction

South America is experiencing steady market expansion as preventive healthcare awareness improves and food manufacturers diversify into clinically supported nutrition products. Brazil and neighboring economies account for most regional deployment, supported by expanding retail distribution and healthcare partnerships. Functional food production capacity has increased by approximately 16% through manufacturing modernization initiatives, although logistics limitations and uneven healthcare access continue affecting deployment consistency. Companies are responding by strengthening regional production networks, improving ingredient sourcing strategies, and expanding collaborations with healthcare providers to improve commercial reach.

Brazil Market Outlook: Brazil serves as the regional center for functional food manufacturing, supported by a large agricultural base and expanding food processing infrastructure. Approximately 45% of regional nutrition product launches originate from Brazilian manufacturers focused on fortified foods and nutraceutical innovation. Companies continue investing in processing modernization, domestic ingredient sourcing, and distribution partnerships, improving production efficiency while strengthening competitive positioning across South American healthcare and consumer markets.

Healthcare modernization supports nutrition innovation

The Middle East & Africa market is advancing through healthcare infrastructure modernization, government wellness initiatives, and increasing investment in preventive care. Gulf countries lead deployment by integrating nutrition services into hospital systems and expanding specialized healthcare facilities. Healthcare-related nutrition programs have increased by approximately 21% over recent years, encouraging greater demand for clinically supported food products. Companies are establishing regional partnerships, localized packaging operations, and distribution networks to improve product availability while adapting portfolios to evolving regulatory and nutritional requirements.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through healthcare transformation programs, advanced hospital infrastructure, and strong investment in preventive healthcare services. More than 50% of newly established specialized healthcare facilities have incorporated nutrition-focused patient management capabilities alongside digital health systems. Domestic and international companies are expanding manufacturing partnerships, nutrition research collaborations, and localized supply networks, positioning the country as a strategic hub for future Food as Medicine deployment across the Middle East.

The competitive landscape is shaped by Nestlé Health Science, Danone, Abbott, Herbalife, DSM-Firmenich, and clinically focused nutrition innovators competing against regional functional food manufacturers and private-label producers. The top five players collectively control approximately 41% of the market, while regional companies compete through localized formulations and cost-efficient manufacturing. Global leaders differentiate through clinical validation, precision nutrition technologies, and integrated supply chains, whereas regional firms emphasize affordability and faster product localization. AI-enabled nutrition platforms reduce personalized recommendation time by nearly 40%, while vertically integrated ingredient sourcing lowers procurement costs by approximately 18% and improves fulfillment reliability by 22%. Companies are strengthening positions through acquisitions, healthcare partnerships, ingredient innovation, and manufacturing expansion to secure clinical credibility and distribution access. Competition is shifting toward evidence-backed products and digital nutrition ecosystems rather than conventional functional foods alone. Clinical validation requirements and regulatory compliance create significant entry barriers. Sustainable competitive advantage depends on combining scientific evidence, scalable manufacturing, digital capabilities, resilient supply chains, and healthcare partnerships.

Nestlé Health Science

Danone

Abbott

DSM-Firmenich

Herbalife

Glanbia plc

Arla Foods

Kerry Group

FrieslandCampina

Ajinomoto Co., Inc.

BASF SE

PepsiCo

General Mills

Unilever

Artificial intelligence, precision nutrition platforms, microbiome analytics, and digital health integration are redefining Food as Medicine product development and clinical deployment. More than 46% of leading healthcare organizations now utilize digital nutrition assessment platforms, while AI-supported dietary planning improves workflow efficiency by approximately 41%. Automated formulation systems also reduce product development cycles by nearly 19%, enabling faster commercialization of clinically targeted nutrition products with greater formulation consistency.

Emerging technologies increasingly combine wearable health devices, continuous biomarker monitoring, and microbiome sequencing to deliver individualized dietary recommendations. Compared with conventional nutrition planning, AI-driven personalized nutrition improves intervention accuracy by approximately 33% while lowering consultation time by nearly 27%. Companies with integrated healthcare, food science, and digital analytics capabilities gain stronger competitive positioning because they can deliver measurable clinical outcomes alongside personalized consumer experiences, creating higher customer retention and healthcare adoption.

Between 2026 and 2028, digital therapeutic nutrition, predictive nutrition algorithms, and smart manufacturing platforms will become core competitive differentiators. Adoption of cloud-connected nutrition management systems is expected to exceed 55% among large healthcare providers, improving patient engagement and operational scalability. Companies investing early in interoperable digital ecosystems, advanced ingredient research, and automated production infrastructure will achieve stronger regulatory readiness, faster innovation cycles, and durable competitive advantage in evidence-based nutrition markets.

April 2024 – Nestlé India and Dr. Reddy’s Laboratories formed a joint venture to commercialize Nestlé Health Science nutraceutical brands across India and agreed international markets, combining pharmaceutical distribution with nutrition expertise to accelerate consumer access and strengthen preventive healthcare offerings. Source: Nestlé India

June 2025 – Danone introduced its Iron Up! initiative featuring IronBiotics technology, delivering up to 3× higher iron absorption in selected formula products. The innovation strengthened evidence-based nutritional solutions and reinforced the company's science-led specialized nutrition portfolio. Source: Danone

October 2025 – Nestlé Health Science entered a strategic partnership with the University of California, Davis Innovation Institute for Food & Health to accelerate research in metabolic, gastrointestinal, oncology, and pediatric nutrition while expanding commercialization pathways for clinically validated nutrition innovations. Source: UC Davis Innovation Institute for Food & Health

March 2026 – Danone completed its acquisition of Huel, adding a digitally driven complete nutrition portfolio with products sold in over 100 countries, strengthening its Food as Medicine positioning through expanded direct-to-consumer capabilities and science-based nutrition offerings. Source: Danone Press Release

This report delivers comprehensive analysis of the Food as Medicine Market across Functional Foods, Medical Foods, Nutraceuticals, Dietary Supplements, and Fortified Foods, while evaluating key applications including diabetes management, heart health, weight management, digestive health, and immune support. It assesses demand across hospitals, clinics, retail consumers, pharmacies, wellness centers, and long-term care facilities, supported by regional and country-level business intelligence spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of the assessment emphasizes operational deployment, product innovation, and enterprise strategies.

The study further examines precision nutrition, AI-enabled dietary platforms, microbiome science, digital health integration, and advanced functional ingredient technologies shaping industry transformation between 2026 and 2033. It provides competitive benchmarking, segmentation insights, technology evaluation, regional comparisons, and investment priorities while identifying adoption trends, deployment patterns, partnership activity, and emerging niche opportunities. The analysis supports strategic expansion planning, portfolio optimization, competitive positioning, supply-chain decisions, and long-term market development.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 227190 Million |

Market Revenue in 2033 | USD 490555.06 Million |

CAGR (2026 - 2033) | 10.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Nestlé Health Science, Danone, Abbott, DSM-Firmenich, Herbalife, Glanbia plc, Arla Foods, Kerry Group, FrieslandCampina, Ajinomoto Co., Inc., BASF SE, PepsiCo, General Mills, Unilever |

Customization & Pricing | Available on Request (10% Customization is Free) |