Reports

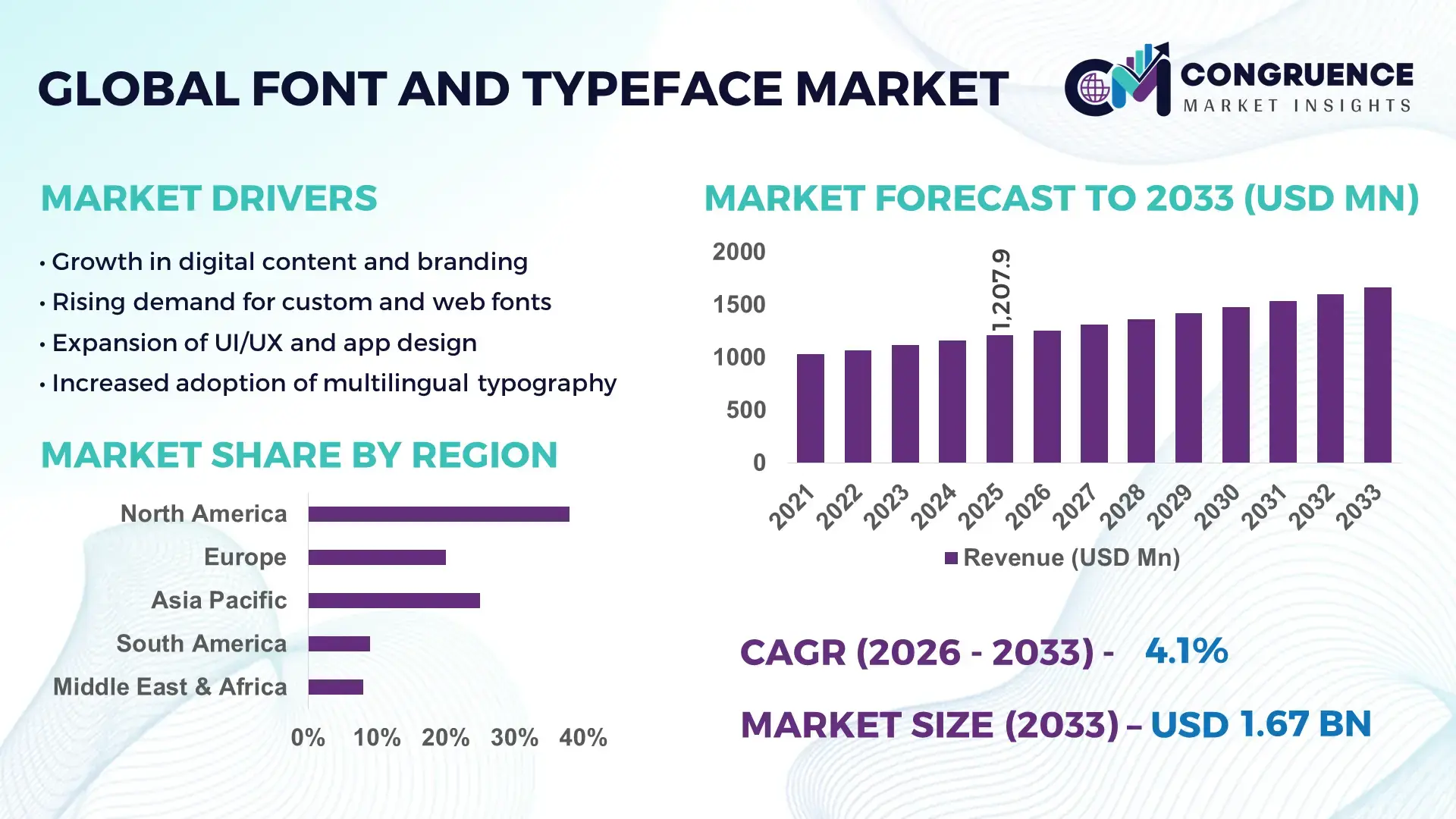

The Global Font and Typeface Market was valued at USD 1207.87 Million in 2025 and is anticipated to reach a value of USD 1665.81 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Growth is supported by rising digital content creation, brand differentiation needs, and expanding multilingual publishing requirements.

The United States represents the dominant country in the Font and Typeface Market, supported by a mature digital design ecosystem and strong commercial licensing activity. Over 65% of enterprise-grade font production tools are developed or headquartered in the U.S., with annual private and corporate investments exceeding USD 180 million in typography software, AI-based font generation, and variable font technologies. Key applications span advertising, UI/UX design, media publishing, and enterprise branding, with more than 78% of Fortune 1000 companies using proprietary or licensed typefaces. Consumer adoption is high, with over 70% of digital designers in North America using subscription-based font platforms, while variable fonts now account for nearly 45% of newly deployed web typography projects.

Market Size & Growth: USD 1207.87 Million (2025) projected to USD 1665.81 Million by 2033 at a CAGR of 4.1%, driven by digital branding expansion and multilingual content demand.

Top Growth Drivers: Digital media adoption 62%, brand personalization impact 48%, UI/UX optimization efficiency 35%.

Short-Term Forecast: By 2028, automated font deployment is expected to reduce design cycle costs by 22%.

Emerging Technologies: Variable fonts, AI-assisted font creation, cloud-based font licensing platforms.

Regional Leaders: North America USD 620 Million by 2033 with enterprise branding focus; Europe USD 480 Million driven by publishing digitization; Asia-Pacific USD 410 Million led by mobile app localization.

Consumer/End-User Trends: Enterprises and digital creators increasingly prefer subscription licensing and cross-platform font compatibility.

Pilot or Case Example: In 2024, a global e-commerce platform implemented variable fonts, improving page load speed by 18%.

Competitive Landscape: Monotype leads with ~35% share, followed by Adobe Fonts, Google Fonts, Linotype, and FontShop.

Regulatory & ESG Impact: Stronger IP enforcement and digital copyright regulations support licensed font adoption.

Investment & Funding Patterns: Over USD 520 Million invested recently in font-tech, SaaS licensing, and AI typography tools.

Innovation & Future Outlook: Integration of typography with AI design systems and real-time personalization engines is accelerating.

The Font and Typeface Market serves advertising, digital media, publishing, software UI/UX, education, and corporate branding, with digital media and software interfaces contributing over 55% of total demand. Recent innovations include AI-generated custom fonts, responsive variable typography, and cloud-based licensing models. Regulatory emphasis on intellectual property protection and growing ESG-driven digital accessibility standards influence adoption. Regionally, North America and Europe show high enterprise usage, while Asia-Pacific records faster growth due to mobile-first content consumption. Future trends indicate deeper AI integration, multilingual font expansion, and increased demand for performance-optimized web typography solutions.

The Font and Typeface Market holds strategic relevance as typography has evolved from a creative asset into a functional, performance-driven digital infrastructure component across branding, software interfaces, and content delivery platforms. Enterprises increasingly view fonts as intellectual property assets that enhance brand consistency, user engagement, and accessibility compliance. Variable font technology delivers up to 30% file-size reduction and 25% faster page rendering compared to static font standards, making it a preferred benchmark for performance-oriented digital ecosystems. North America dominates in volume due to enterprise licensing demand, while Asia-Pacific leads in adoption with nearly 58% of digital-first enterprises integrating multilingual and mobile-optimized typefaces.

From a strategic planning perspective, typography platforms are being embedded into AI-driven design workflows. By 2028, AI-based font generation and automated typographic optimization are expected to improve design turnaround time by 35% and reduce manual intervention costs by 20%. ESG and compliance considerations are also reshaping the market, with firms committing to digital accessibility metrics such as 100% WCAG-compliant typography libraries and a 40% reduction in redundant font data storage by 2030. In 2024, a leading U.S.-based SaaS design firm achieved a 22% improvement in content accessibility scores by deploying AI-assisted font contrast and readability optimization tools. Looking ahead, the Font and Typeface Market is positioned as a pillar of operational resilience, regulatory alignment, and sustainable digital growth across industries.

The rapid expansion of digital branding and UI/UX design is a primary growth driver for the Font and Typeface Market. Over 75% of enterprises now prioritize consistent typography across digital touchpoints to enhance brand recognition and user trust. In software and mobile applications, optimized typography has been shown to improve user retention by nearly 20% through better readability and visual hierarchy. The rise of omnichannel marketing has increased demand for scalable font families that function seamlessly across web, mobile, and print formats. Additionally, variable fonts reduce the number of font files required by up to 60%, directly supporting faster deployment cycles and improved performance metrics in digital products.

Intellectual property risks and complex licensing structures act as restraints within the Font and Typeface Market. Unauthorized font usage remains prevalent, with industry audits indicating that nearly 30% of digital assets use fonts outside permitted licensing terms. This exposes organizations to legal risks, compliance costs, and brand reputational damage. Moreover, licensing models vary significantly by platform, user count, and deployment method, increasing administrative burden for enterprises managing large digital portfolios. Small and mid-sized businesses often delay adoption of premium typefaces due to uncertainty around long-term licensing costs and enforcement policies, slowing broader market penetration.

AI-driven typography presents substantial opportunities for the Font and Typeface Market by enabling rapid customization, localization, and performance optimization. AI-generated fonts can reduce initial design time by nearly 40% while supporting automated kerning, spacing, and readability adjustments based on device or user behavior. Personalized typography is gaining relevance in e-learning, e-commerce, and digital advertising, where adaptive fonts improve engagement metrics by up to 18%. Emerging markets also present opportunities as demand grows for localized scripts and multilingual font libraries, particularly in mobile-first economies where content personalization directly influences user acquisition and retention.

Technological fragmentation remains a key challenge for the Font and Typeface Market. Inconsistent support for advanced font formats across browsers, operating systems, and legacy devices limits uniform deployment. While variable fonts offer efficiency gains, compatibility gaps still affect nearly 15% of older enterprise systems. Performance constraints also persist, as poorly optimized typography can increase page load times by up to 10%, negatively impacting user experience and SEO rankings. Additionally, the rapid pace of technological change requires continuous updates to font libraries and rendering engines, increasing maintenance complexity and skill requirements for organizations managing large-scale digital assets.

Expansion of Variable and Responsive Typography: Variable fonts are rapidly reshaping deployment strategies across digital platforms by consolidating multiple font styles into a single file. Around 48% of newly launched websites now use variable fonts, reducing font file requests by nearly 60% and improving page load performance by approximately 25%. Enterprises adopting responsive typography report up to 18% improvement in user readability scores across devices, particularly in mobile-first environments where screen adaptability is critical.

AI-Driven Font Creation and Optimization: Artificial intelligence is increasingly embedded in font design and management workflows. Nearly 42% of professional design teams now use AI-assisted tools for kerning, spacing, and weight optimization, cutting manual design time by about 35%. AI-generated fonts also support rapid multilingual adaptation, enabling companies to deploy localized typography up to 30% faster while maintaining consistent brand identity across global markets.

Shift Toward Subscription-Based and Cloud Licensing Models: Cloud-based font licensing is becoming the preferred procurement model, with over 65% of enterprises transitioning from perpetual licenses to subscription access. This shift enables centralized font governance and reduces compliance violations by nearly 28%. Cloud delivery also supports real-time updates and cross-platform synchronization, which has lowered internal font management overheads by approximately 20% for large organizations managing multiple digital assets.

Growing Focus on Accessibility and Performance Compliance: Accessibility-driven typography is gaining prominence as digital regulations tighten. More than 55% of new enterprise digital projects now mandate WCAG-compliant font contrast and readability standards. Organizations implementing accessibility-optimized typefaces have recorded up to 22% improvement in content engagement among diverse user groups. Additionally, performance-optimized fonts have reduced data transfer volumes by nearly 15%, aligning typography strategies with broader sustainability and digital efficiency goals.

The Font and Typeface Market is segmented by type, application, and end-user, reflecting diverse usage patterns across digital, commercial, and institutional environments. By type, demand varies between static fonts, variable fonts, and AI-generated or adaptive typefaces, driven by performance, flexibility, and customization needs. Application-wise, branding and advertising dominate usage, followed by digital interfaces, publishing, and educational content, each requiring distinct typographic capabilities. End-user segmentation highlights strong adoption by enterprises and digital-first organizations, while independent creators, educational institutions, and government bodies represent steadily expanding user bases. Across all segments, decisions are increasingly influenced by compatibility, licensing efficiency, accessibility compliance, and multilingual support rather than purely aesthetic considerations.

The Font and Typeface Market by type is led by static fonts, which currently account for approximately 46% of total adoption due to their simplicity, broad compatibility, and entrenched use in print publishing and legacy digital systems. Variable fonts represent around 34% of adoption, offering measurable advantages such as reducing font file counts by nearly 60% and improving rendering performance across screen sizes. However, AI-generated and adaptive fonts are the fastest-growing type, expanding at an estimated CAGR of 18.2%, driven by demand for rapid customization, multilingual scalability, and automated optimization in digital products. Other niche types, including icon fonts and decorative or display-only fonts, collectively contribute about 20% of the market, serving branding, gaming, and creative industries.

By application, branding and advertising remain the leading segment, accounting for nearly 38% of Font and Typeface usage, as consistent typography is central to brand recognition and customer engagement. Digital interfaces, including websites, mobile applications, and software dashboards, hold around 31% adoption, supported by the need for responsive and performance-optimized typography. Publishing and media applications account for approximately 17%, while education, gaming, and other specialized uses contribute a combined 14%. Among these, digital interface applications are the fastest-growing, with an estimated CAGR of 16.5%, fueled by mobile-first design strategies and UI/UX optimization requirements.

Enterprises constitute the leading end-user segment in the Font and Typeface Market, representing about 44% of total usage, as corporations invest heavily in proprietary and licensed typefaces to maintain brand consistency across global operations. Independent designers and creative professionals account for roughly 26%, supported by subscription-based font platforms and freelance digital content creation. The fastest-growing end-user group is small and medium-sized enterprises, expanding at an estimated CAGR of 17.8%, driven by increased digital marketing activity and e-commerce adoption. Educational institutions, government organizations, and non-profits collectively contribute around 30%, with adoption rates rising due to accessibility mandates and multilingual communication needs.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America’s leadership is supported by high enterprise licensing penetration, with over 72% of large organizations using licensed or proprietary typefaces. Europe followed with a 29% share, driven by publishing digitization and regulatory-led accessibility adoption across more than 24 languages. Asia-Pacific held nearly 25% of global demand in 2025, supported by mobile-first content consumption, where over 68% of digital users access content primarily via smartphones. South America and the Middle East & Africa together accounted for approximately 8%, reflecting growing localization needs, regional language digitization, and expanding digital media ecosystems. Region-wise differences are strongly influenced by enterprise digitization maturity, multilingual requirements, and regulatory emphasis on accessibility and intellectual property compliance.

How is enterprise-scale digital transformation shaping typography demand?

North America accounts for approximately 38% of the global Font and Typeface Market, supported by strong demand from technology, media, finance, and healthcare industries. More than 70% of enterprises in this region integrate typography standards into brand governance frameworks. Regulatory emphasis on digital accessibility has increased adoption of WCAG-compliant fonts across public and private platforms. Technological trends include widespread deployment of variable fonts and AI-assisted font management tools, now used by nearly 45% of professional design teams. Local players such as Monotype are expanding cloud-based font licensing platforms, enabling centralized compliance management for thousands of enterprise clients. Consumer behavior reflects higher enterprise adoption, particularly in healthcare and financial services, where readability, security, and compliance are critical.

Why is regulation-driven digital standardization influencing typography adoption?

Europe holds close to 29% of the Font and Typeface Market, with Germany, the UK, and France accounting for more than 60% of regional demand. Regulatory bodies emphasize accessibility, data protection, and intellectual property enforcement, increasing demand for licensed and explainable typography solutions. Over 58% of new digital public-sector projects mandate accessibility-compliant fonts. Emerging technologies such as variable fonts and multilingual script optimization are widely adopted to support cross-border communication. European design firms are increasingly investing in sustainable digital assets, reducing redundant font usage by nearly 20%. Consumer behavior is shaped by regulatory pressure, leading to higher demand for transparent licensing and standardized font usage.

How are mobile-first economies accelerating typography adoption?

Asia-Pacific ranks as the fastest-growing region and accounts for about 25% of global Font and Typeface demand. China, India, and Japan are the top consuming countries, together representing over 65% of regional usage. Rapid growth in e-commerce, gaming, and mobile applications drives high demand for multilingual and performance-optimized fonts. More than 75% of digital content in the region is consumed on mobile devices, increasing adoption of responsive typography. Regional innovation hubs are investing in AI-based font generation to support complex scripts. Consumer behavior is strongly influenced by mobile apps and localized digital experiences, particularly in e-commerce and social media platforms.

Why is language localization becoming a critical typography driver?

South America represents approximately 5% of the global Font and Typeface Market, with Brazil and Argentina leading regional adoption. Growth is supported by expanding digital media, online education, and advertising sectors. Government-backed digital inclusion programs have increased demand for accessible and localized typography. Trade policies supporting creative industries have encouraged regional font development initiatives. Local design studios are focusing on Latin-script optimization and multilingual support. Consumer behavior in this region is closely tied to media consumption and language localization, with over 60% of digital platforms prioritizing region-specific typography for engagement.

How is digital modernization influencing typography demand?

The Middle East & Africa account for roughly 3% of the Font and Typeface Market, with the UAE and South Africa as major growth countries. Demand is linked to digital modernization in construction, education, and government services. Smart city initiatives and e-government platforms are increasing the need for Arabic and multilingual font solutions. Technological upgrades in digital infrastructure have led to a 28% increase in licensed font adoption across public-sector platforms. Regional consumer behavior emphasizes bilingual and culturally adaptive typography, particularly in media and public communication.

United States Font and Typeface Market – 32% share: Strong enterprise demand, advanced digital infrastructure, and widespread adoption of licensed and proprietary typefaces.

China Font and Typeface Market – 18% share: Large-scale digital content creation, high mobile user base, and strong demand for localized and multilingual typography solutions.

The Font and Typeface market exhibits a moderately consolidated competitive structure, characterized by the presence of approximately 120–150 active commercial font developers, digital typography platforms, and design technology providers globally. The top five companies collectively account for nearly 62% of total licensed font usage, reflecting strong concentration around established intellectual property portfolios, enterprise-grade licensing capabilities, and cloud-based distribution models. Market leaders differentiate themselves through expansive multilingual libraries exceeding 25,000 font families, AI-assisted font optimization tools, and integrated design-software partnerships. Strategic initiatives remain central to competition, with over 40% of leading players engaging in platform integrations, SaaS-based licensing expansions, or AI-driven product launches between 2023 and 2025. Partnerships with software vendors, web development platforms, and branding agencies have increased enterprise penetration rates by more than 20%. Innovation trends include variable font deployment, automated compliance tracking, and real-time typography analytics, which have reduced font management inefficiencies by up to 30% for large organizations. Despite consolidation at the top, the market remains competitive at the mid-tier level, where independent foundries and regional players continue to capture niche demand through culturally localized and script-specific typeface offerings.

Monotype

Adobe Fonts

Google Fonts

Linotype

FontShop

Dalton Maag

Hoefler & Co.

Typotheque

Emigre

House Industries

Technology is fundamentally reshaping the Font and Typeface Market, transforming typography from static visual assets into intelligent, performance-optimized digital components. One of the most impactful advancements is the adoption of variable font technology, which allows multiple weights, widths, and styles to be embedded within a single font file. This approach reduces font file volumes by up to 60% and improves web and mobile rendering speeds by approximately 25%, making it a preferred choice for large-scale digital platforms managing high traffic loads.

Artificial intelligence is increasingly integrated into font design, testing, and deployment processes. Nearly 45% of professional design teams now use AI-assisted tools for automated kerning, spacing, and contrast optimization, reducing manual design effort by around 35%. AI-generated typefaces also support rapid localization, enabling the creation of complex scripts and multilingual variants up to 30% faster than traditional design workflows. Machine learning models are further applied to predict readability and user engagement outcomes, allowing enterprises to align typography with user behavior analytics.

Cloud-based font management and licensing platforms represent another major technological shift. Over 65% of enterprises now deploy fonts through centralized cloud environments, enabling real-time updates, cross-platform synchronization, and automated compliance tracking. This has reduced licensing violations by nearly 28% and improved governance efficiency across distributed teams. Additionally, emerging technologies such as responsive typography engines, accessibility-first font frameworks, and API-driven font delivery are supporting regulatory compliance and ESG-driven digital accessibility goals. Collectively, these technologies are positioning typography as a strategic digital infrastructure layer rather than a purely creative resource.

• In April 2025, Monotype expanded its long-standing collaboration with Adobe, integrating over 750 premium typefaces—including Helvetica, Avenir, and Gotham—into Adobe Creative Cloud, giving subscribers seamless access to more than 2,800 Monotype fonts across key design applications. (monotype.com)

• In December 2024, Monotype marked a year of industry partnerships and technological expansion, adding new foundry libraries and announcing the acquisition of font management solution Extensis Connect, enhancing unified font inventory and software capabilities for enterprise users.

• During 2025, Monotype and Canva celebrated a design milestone with over 1 billion creations using Monotype library fonts, showcasing the prevalence of curated typography assets in both professional and amateur design ecosystems.

• In July 2025, social platform Instagram introduced a bespoke font based on global artist Rosalía’s handwriting, designed collaboratively with Monotype, highlighting the growing trend of personalized typefaces in brand identity and social media engagement.

The scope of the Font and Typeface Market Report encompasses comprehensive segmentation across product types, applications, and end-user categories to enable decision-makers to understand both breadth and depth of the market. The report analyzes main font categories including static, variable, and AI-generated typefaces, exploring their performance implications in print, web, and software UI contexts. It also examines application areas such as branding and advertising, digital interfaces, publishing, education, and multimedia, with measurable insights into adoption rates, format usage, and script support requirements across regions. Geographic analysis covers key regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing differences in consumer behavior, language diversity, technological integration, and regulatory pressures that shape typeface demand.

Technological trends addressed include automation in font creation, AI-assisted optimization workflows, cloud-based font licensing and management platforms, and responsive typography systems that support cross-device performance needs. The report also highlights niche segments such as multilingual script libraries, accessibility-optimized typography frameworks, and enterprise governance tools for font compliance. Regional policy environments—such as accessibility mandates and intellectual property enforcement—are summarized to provide context for strategic planning. Focus areas emphasize practical insights on deployment efficiency, licensing models, design system integration, and innovation trajectories, positioning the Font and Typeface report as a decision-support tool for brand leaders, digital product strategists, and design technology professionals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Monotype, Adobe Fonts, Google Fonts, Linotype, FontShop, Dalton Maag, Hoefler & Co., Typotheque, Emigre, House Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |