Reports

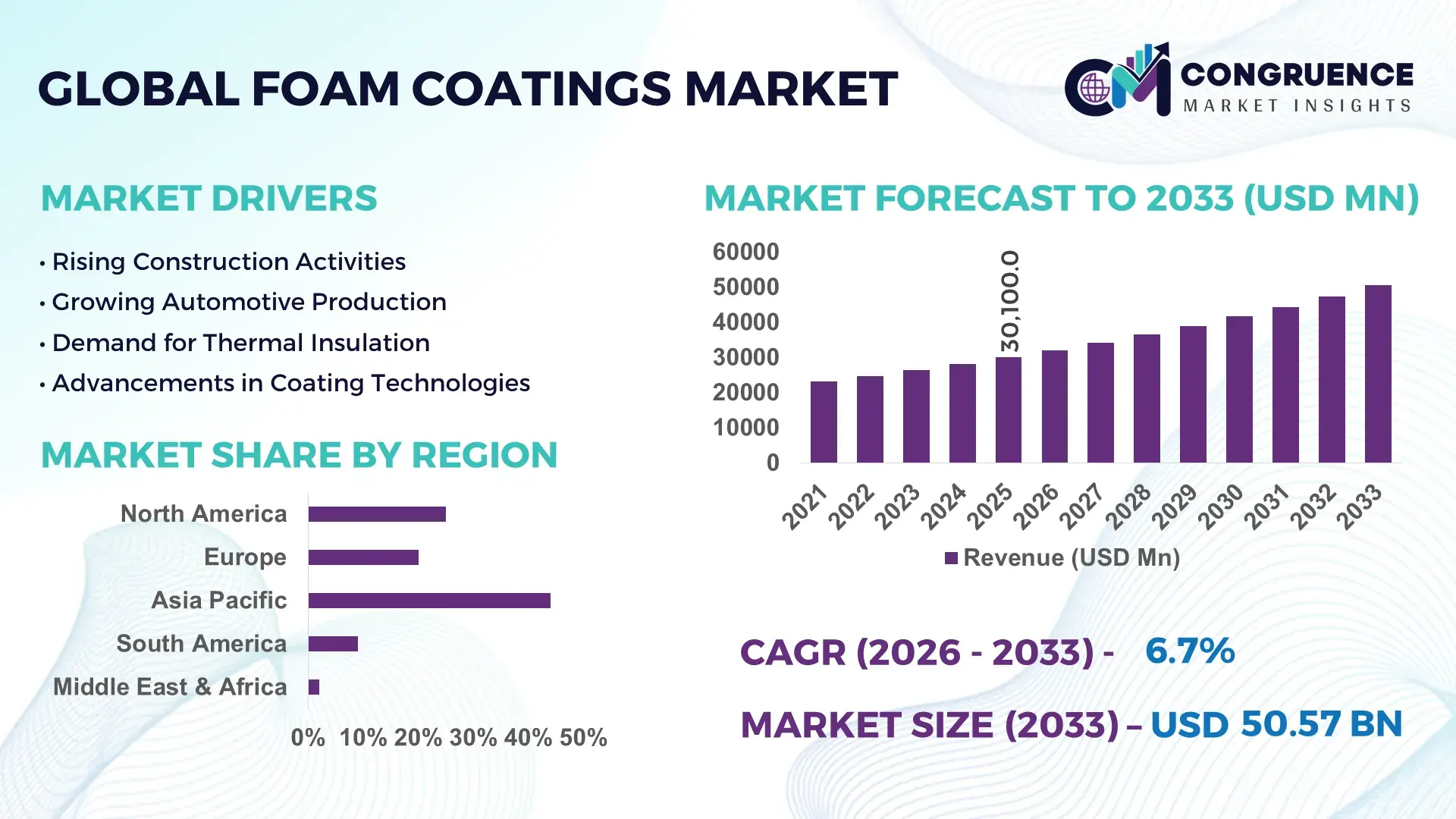

The Global Foam Coatings Market was valued at USD 30100 Million in 2025 and is anticipated to reach a value of USD 50568.7 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033. Advanced polyurethane and silicone-based foam coatings are accelerating adoption across automotive interiors, insulation panels, aerospace cushioning, and construction sealing systems, with low-VOC formulations improving coating durability by over 28% compared to conventional solvent-heavy systems.

China remains the dominant production and consumption hub, accounting for nearly 36% of global foam coatings output in 2026, supported by over USD 4 billion in industrial insulation and EV battery protection investments. The country’s automotive and construction sectors collectively represent more than 58% of domestic coating demand, while smart manufacturing deployment across major coating plants increased process efficiency by 22% since 2024. Compared with several Western markets, Chinese manufacturers deliver foam coating production at approximately 18% lower operational cost due to integrated petrochemical supply chains and high-capacity industrial clusters.

Manufacturers prioritizing bio-based chemistries, automated application systems, and localized supply networks are positioned to secure stronger margins and long-term procurement contracts across high-growth industrial sectors.

Market Size & Growth: USD 30100 Million in 2025 rising to USD 50568.7 Million by 2033 at 6.7% CAGR, driven by lightweight industrial insulation and EV component protection demand.

Top Growth Drivers: Automotive lightweighting contributes 31%, construction insulation demand 27%, and low-VOC regulatory adoption 22% of market expansion momentum.

Short-Term Forecast: By 2027, automated foam coating lines reduce application waste by 19% and improve production efficiency by 24% across high-volume manufacturing facilities.

Emerging Technologies: AI-enabled coating control, robotic spray systems, and bio-based polyurethane coatings increase material precision by 21% and reduce defects by 16%.

Regional Leaders: Asia-Pacific exceeds USD 19 billion with rapid EV adoption, Europe crosses USD 11 billion through sustainable coatings expansion, and North America surpasses USD 9 billion via industrial retrofitting projects.

Consumer/End-User Trends: More than 44% of industrial buyers prioritize thermal efficiency coatings, while automotive OEM adoption of advanced foam coatings exceeds 38% in 2026.

Pilot/Case Example: In 2025, an automated industrial insulation project improved coating consistency by 26% and lowered energy leakage losses by 18%.

Competitive Landscape: Top manufacturers collectively control nearly 41% market share, with strong competition among multinational chemical and specialty coating suppliers.

Regulatory & ESG Impact: Low-emission coating mandates reduced solvent-based product usage by 23% across Europe and accelerated water-based foam coating deployment.

Investment & Funding: Global investments surpassed USD 5.2 billion between 2024 and 2026, led by regional manufacturing expansion and supply chain localization initiatives.

Innovation & Future Outlook: Next-generation nanostructured foam coatings and recyclable polymer technologies improve thermal resistance by 17% while supporting advanced sustainable manufacturing strategies.

Automotive, construction, and industrial insulation sectors collectively contribute over 68% of global foam coatings consumption, supported by rising demand for lightweight thermal management systems and durable protective materials. Water-based and bio-derived coating technologies improved material efficiency by nearly 20% in 2026, while robotic application systems reduced coating inconsistencies by 15%. Asia-Pacific maintains dominant demand leadership, whereas Europe is accelerating adoption through stricter emission compliance standards and localized production strategies amid global supply chain restructuring. Increasing integration of recyclable polymer formulations and smart coating automation is expected to reshape competitive positioning and procurement strategies across the high-growth foam coatings ecosystem.

Foam coatings are rapidly transforming from a niche protective material into a strategic industrial solution tied directly to lightweight manufacturing, thermal efficiency, and low-emission compliance. Automotive OEMs, construction material suppliers, and aerospace manufacturers are accelerating procurement of advanced foam coating technologies to optimize insulation performance and extend product durability. Global manufacturers are restructuring supplier networks and regionalizing production after logistics disruptions between 2024 and 2026 exposed vulnerabilities in petrochemical-dependent coating supply chains. Water-based polyurethane foam coatings now dominate premium industrial applications as sustainability mandates intensify across Europe and North America.

AI-integrated robotic coating systems are reshaping operational efficiency across high-volume facilities. Smart spray automation improves coating precision by 27% while reducing operational cost by 18% compared to legacy manual systems. Asia-Pacific leads in production volume with nearly 48% share, while Europe leads in sustainable coating innovation with over 42% adoption of low-VOC technologies. Over the next three years, automated foam coating lines are projected to reduce material waste by 21% and improve production throughput by 24%. ESG-focused coating formulations are also creating a compliance advantage by lowering industrial emission exposure and reducing waste disposal expenses.

In 2025, a large-scale industrial insulation upgrade project in Germany improved thermal retention efficiency by 19% through advanced closed-cell foam coatings integrated with automated application systems. Major chemical manufacturers are shifting capital allocation toward recyclable polymer technologies, localized manufacturing hubs, and next-generation thermal barrier coatings to secure supply resilience and premium industrial contracts. Companies capable of accelerating sustainable innovation, optimizing coating automation, and transforming regional supply capabilities are positioned to dominate the next phase of competitive expansion in the global foam coatings market.

Rising demand for lightweight insulation systems and high-performance protective materials is accelerating foam coatings adoption across automotive, construction, and industrial manufacturing sectors. Advanced foam-coated components reduce thermal energy loss by nearly 26% while improving structural durability by 18%, making them essential for energy-efficient infrastructure upgrades and electric vehicle production. Global supply chain restructuring after Red Sea shipping disruptions forced manufacturers to localize coating operations and strengthen regional sourcing capabilities. Industrial buyers are rapidly shifting toward automated coating technologies that improve application consistency by 22% and reduce material wastage. In response, manufacturers are accelerating capacity expansion, forming strategic raw material partnerships, and increasing investments in water-based and bio-derived coating formulations to secure long-term competitive positioning globally.

Foam coatings manufacturers are facing mounting pressure from petrochemical raw material volatility, tightening environmental compliance standards, and fragmented supply concentration. Polyurethane feedstock prices fluctuated by over 17% between 2024 and 2026, directly increasing production costs and compressing industrial margins. Simultaneously, low-VOC compliance mandates across Europe and North America raised operational adaptation costs by nearly 14% for mid-sized coating producers. Heavy dependence on limited chemical supply hubs in Asia continues constraining production stability during geopolitical disruptions and logistics bottlenecks. These pressures are extending procurement cycles and delaying large-scale infrastructure projects. To mitigate risks, manufacturers are diversifying sourcing networks, securing long-term supply agreements, and accelerating investment in recyclable polymers and alternative low-emission coating technologies globally.

Advanced sustainable coating technologies and automated manufacturing systems are redefining future competitive opportunities across the foam coatings industry. Bio-based foam coatings improve material recyclability by 24% while reducing solvent-related emissions by nearly 31%, creating strong positioning advantages in regulated industrial markets. Emerging economies across Southeast Asia and the Middle East are accelerating infrastructure modernization, generating new demand pockets for thermal insulation and industrial protection coatings. Simultaneously, AI-driven robotic coating systems are improving production precision by 27% and lowering operational waste across high-volume facilities. Companies are aggressively expanding R&D capabilities, forming ecosystem partnerships with industrial automation providers, and scaling localized manufacturing networks to secure future dominance in advanced insulation, electric mobility, and sustainable construction applications globally.

Foam coatings producers are confronting growing execution challenges linked to scalability limitations, regulatory complexity, and inconsistent application performance across advanced industrial environments. Automated coating infrastructure requires capital investments exceeding 20% above conventional production systems, restricting adoption among smaller manufacturers. Performance inconsistency in extreme-temperature applications continues reducing operational reliability, while evolving environmental regulations are forcing rapid reformulation cycles that extend product validation timelines by nearly 16%. Infrastructure constraints and skilled labor shortages across emerging manufacturing regions are further delaying deployment efficiency. These pressures are constraining long-term production consistency and market expansion. To remain competitive, companies must accelerate investment in precision automation, advanced polymer engineering, workforce training, and strategic technology partnerships capable of supporting scalable, compliant global operations.

Automated coating deployment increased 24% across industrial facilities in 2026, reshaping production efficiency standards. Manufacturers are integrating robotic spray systems and AI-driven viscosity monitoring to reduce coating inconsistencies by 19% and lower material waste by 17%. Labor shortages in industrial manufacturing hubs are forcing faster automation adoption, particularly in Europe and East Asia. Companies are restructuring production layouts and scaling digital process control platforms to optimize throughput and stabilize coating quality across high-volume operations.

Low-VOC and water-based foam coatings captured 42% of new industrial coating installations during 2025–2026. Tightening emission regulations and procurement restrictions are shifting demand away from solvent-heavy formulations. Water-based systems reduced hazardous waste handling costs by 21% while improving regulatory compliance timelines by 16%. Coating suppliers are accelerating reformulation programs and expanding regional production capacity to secure contracts in construction insulation and transportation manufacturing sectors increasingly prioritizing sustainable material compliance.

Asia-Pacific accounted for nearly 48% of foam coatings consumption growth, while Europe accelerated premium technology adoption by 31%. China, India, and Southeast Asia are rapidly scaling infrastructure insulation projects, whereas European manufacturers are prioritizing advanced thermal barrier coatings for energy-efficient retrofitting. This regional divergence is redefining product positioning strategies, with companies balancing high-volume standardized production in Asia against high-margin customized coating solutions in Europe and North America.

Subscription-based industrial coating service models expanded 18% as manufacturers shifted toward lifecycle performance contracts. Large industrial buyers increasingly prefer bundled coating maintenance, predictive inspection, and application optimization services instead of one-time procurement. This operational shift is improving customer retention rates by 14% and reducing downtime across industrial flooring and thermal protection systems. Coating providers are forming partnerships with automation and maintenance firms to capture recurring service revenue while strengthening long-term industrial relationships.

The foam coatings market is segmented by type, application, and end-user, with polyurethane and thermal protection applications dominating industrial demand due to durability and insulation efficiency advantages. Construction and industrial manufacturing collectively contribute over 52% of total consumption, supported by large-scale infrastructure retrofitting and automated production expansion. Demand is shifting toward silicone and elastomeric coatings as industries prioritize weather resistance and low-emission performance. Waterproofing and wall insulation segments are gaining traction across Asia-Pacific and Europe following stricter energy-efficiency standards. Manufacturers are strategically expanding bio-based coating portfolios and automated application systems to capture higher-margin industrial and sustainable construction opportunities across rapidly transforming regional markets.

Polyurethane dominates the foam coatings market with approximately 38% share due to its superior thermal insulation, adhesion strength, and cost-efficient scalability across construction, automotive, and industrial applications. Its integration flexibility and resistance to moisture and abrasion continue reinforcing large-volume procurement across infrastructure and manufacturing projects. Silicone is emerging as the fastest-growing segment, recording adoption growth above 16% as industries prioritize weather-resistant and low-VOC coating technologies for energy-efficient buildings and advanced transportation systems. Compared with acrylic coatings, silicone-based systems deliver nearly 22% higher thermal stability under extreme environmental conditions, accelerating deployment in premium industrial applications.

Epoxy, acrylic, and elastomeric coatings collectively account for nearly 44% of market demand, serving strategic roles in corrosion resistance, waterproofing, and flexible surface protection. Epoxy coatings remain critical for industrial flooring and heavy-duty environments, while elastomeric solutions are gaining traction in wall insulation and crack-resistant applications. Manufacturers are shifting product development toward hybrid formulations combining polyurethane durability with silicone sustainability benefits. Capacity expansion in water-based polyurethane and high-performance silicone technologies indicates where future investment concentration is accelerating, while conventional acrylic systems are increasingly repositioned toward mid-cost construction applications requiring scalable deployment efficiency.

“According to a 2025 report by the International Energy Efficiency Council, silicone-based foam coatings were adopted by over 41% of advanced industrial insulation projects, resulting in nearly 23% improvement in thermal performance and reduced maintenance costs, reinforcing their growing strategic importance.”

Roof insulation leads the foam coatings market with nearly 29% share as commercial and residential infrastructure projects prioritize thermal efficiency, moisture resistance, and long-term energy optimization. High adoption concentration exists because coated roof insulation systems reduce energy leakage by approximately 24% and improve structural durability in extreme climates. Thermal protection is the fastest-growing application, expanding above 17% due to rising deployment in electric vehicles, industrial processing facilities, and energy infrastructure. Compared with mature waterproofing applications, thermal protection solutions are increasingly driven by operational efficiency requirements and advanced material integration.

Waterproofing, corrosion resistance, industrial flooring, and wall insulation collectively contribute around 58% of market demand, reflecting broad industrial diversification. Corrosion-resistant coatings remain essential across marine and heavy manufacturing sectors, while industrial flooring demand is accelerating through automated warehouse expansion and high-load production facilities. Companies are scaling multifunctional coating systems capable of combining insulation, waterproofing, and anti-corrosion performance within single-layer applications. Demand patterns are shifting toward high-performance coatings that lower lifecycle maintenance costs and improve operational efficiency, forcing manufacturers to reposition portfolios around durability-focused and sustainable industrial applications with stronger long-term contract potential.

“According to a 2025 report by the Global Building Performance Association, thermal protection coatings were deployed across more than 18,000 industrial and infrastructure facilities, improving energy efficiency by 21%, highlighting their rapid operational adoption.”

Construction remains the leading end-user segment, accounting for nearly 34% of foam coatings demand due to intensive usage across roof insulation, wall protection, waterproofing, and energy-efficient infrastructure retrofitting projects. Demand concentration is driven by rising adoption of sustainable building standards and advanced insulation technologies that improve thermal retention by over 25%. Automotive is the fastest-growing end-user segment, expanding above 18% as electric vehicle manufacturers increasingly deploy lightweight foam coatings for battery insulation, acoustic protection, and interior durability optimization. Compared with construction’s high-volume standardized demand, automotive procurement is shifting toward customized, performance-engineered coating systems.

Aerospace, industrial manufacturing, marine, and energy and utilities collectively contribute approximately 49% of total market consumption. Industrial manufacturing continues accelerating adoption of automated coating technologies to improve production efficiency and reduce maintenance downtime, while marine applications prioritize corrosion-resistant and weatherproof systems for long-life asset protection. Companies are targeting these sectors through application-specific product customization, long-term supply partnerships, and integrated coating service contracts. Demand is shifting toward premium high-performance coatings capable of supporting sustainability compliance and operational efficiency, forcing suppliers to strengthen technical support capabilities and localized manufacturing responsiveness across strategic industrial markets.

“According to a 2025 report by the Advanced Manufacturing Standards Council, adoption among automotive manufacturers increased by 19%, with over 7,500 production facilities implementing advanced foam coating solutions, leading to nearly 18% improvement in thermal efficiency and component durability, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 48% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

Asia-Pacific dominates foam coatings demand through large-scale construction activity, automotive manufacturing expansion, and cost-efficient chemical production networks concentrated in China, India, and Southeast Asia. Europe contributes nearly 26% of global demand and leads sustainable coating innovation, with low-VOC adoption rates exceeding 42% due to tightening environmental compliance standards. North America holds approximately 21% share, driven by industrial retrofitting and advanced insulation deployment across transportation and manufacturing sectors. Meanwhile, Middle East & Africa is accelerating infrastructure-led demand through energy diversification projects and industrial modernization programs. Global supply chain restructuring and regionalized production strategies are forcing manufacturers to rebalance sourcing and capacity expansion. Companies are increasingly prioritizing Asia-Pacific for scale, Europe for innovation leadership, and Middle East & Africa for long-term infrastructure-driven expansion opportunities.

North America represents nearly 21% of global foam coatings demand, supported by strong adoption across industrial manufacturing, commercial construction, and electric vehicle insulation applications. Energy-efficiency retrofitting projects and advanced warehouse infrastructure are accelerating deployment of thermal protection and waterproofing coatings. Stricter low-emission regulations and rising labor costs are forcing manufacturers to adopt automated spray-coating technologies that improve operational efficiency by 23% while reducing material waste. Industrial buyers increasingly prioritize durable, low-maintenance coating systems capable of lowering lifecycle operating expenses. In 2026, multiple regional manufacturers expanded localized production capacity by over 18% to reduce import dependency and strengthen supply resilience. Companies continue prioritizing North America because the region combines premium industrial demand, compliance-driven procurement, and rapid adoption of automated coating technologies.

Europe accounts for approximately 26% of global foam coatings consumption, led by Germany, France, and Italy through strong demand in sustainable construction, automotive insulation, and industrial retrofitting. Aggressive low-VOC regulations and carbon-reduction mandates are accelerating the shift toward water-based and recyclable coating technologies. More than 42% of new industrial coating installations now utilize sustainable formulations designed to improve compliance efficiency and reduce hazardous waste exposure. Manufacturers are optimizing automated coating systems to improve material precision by 19% while reducing energy-intensive application processes. Enterprise buyers increasingly prioritize high-durability coatings with verified environmental performance over low-cost alternatives. Europe is forcing suppliers to accelerate innovation, strengthen sustainable product portfolios, and redesign production strategies around stricter environmental compliance and premium performance expectations.

Asia-Pacific leads the foam coatings market with nearly 48% of global consumption, supported by large-scale manufacturing expansion, infrastructure modernization, and rapidly growing automotive production across China, India, Japan, and Southeast Asia. Integrated petrochemical supply chains and lower operational costs provide strong production advantages for regional manufacturers. Industrial coating deployment across major manufacturing hubs increased by 27% during 2025–2026 as companies accelerated localized production and automated coating integration. Construction and transportation sectors continue prioritizing scalable, cost-efficient insulation systems capable of supporting high-volume infrastructure projects. Multiple coating manufacturers expanded regional production capacity by over 20% to strengthen export competitiveness and reduce delivery lead times. Asia-Pacific remains critical for companies seeking manufacturing scale, rapid deployment speed, and long-term industrial demand concentration.

South America contributes approximately 7% of global foam coatings demand, with Brazil and Argentina leading adoption across commercial construction, industrial flooring, and waterproofing applications. Infrastructure modernization and energy-efficiency retrofitting projects are increasing demand for thermal insulation coatings, particularly in logistics and manufacturing facilities. However, currency volatility and dependence on imported chemical feedstocks continue constraining production scalability and raising procurement costs by nearly 14% across several industrial sectors. Companies are responding through localized distribution partnerships and selective expansion of regional blending operations to improve supply responsiveness. Industrial buyers remain highly price-sensitive, prioritizing durable coatings with lower maintenance requirements and long operational lifecycles. South America presents strong long-term expansion potential, but operational flexibility and localized cost management remain essential for sustainable market penetration.

Middle East & Africa represents nearly 8% of global foam coatings demand, driven by large-scale infrastructure projects, oil and gas facility modernization, and commercial construction expansion across Saudi Arabia, the UAE, and South Africa. Government-backed industrial diversification programs are accelerating demand for thermal protection and corrosion-resistant coating systems. Deployment of advanced insulation coatings across industrial facilities increased by 22% during 2025–2026 as enterprises prioritized energy optimization and asset durability. Regional manufacturers and international suppliers are forming strategic partnerships to expand localized coating production and improve supply efficiency. Buyers increasingly prefer high-performance coatings capable of withstanding extreme environmental conditions while lowering maintenance frequency. The region is emerging as a strategic expansion market where infrastructure investment, industrial modernization, and localized partnerships are reshaping long-term competitive positioning.

China – Holds approximately 36% share of the global Foam Coatings Market due to large-scale manufacturing capacity, integrated petrochemical supply chains, and strong construction and automotive demand.

United States – Accounts for nearly 18% share of the Foam Coatings Market, supported by advanced industrial retrofitting, premium insulation demand, and rapid adoption of automated coating technologies.

The foam coatings market is dominated by global chemical leaders competing directly against regional cost-focused manufacturers and specialized coating innovators. Major players including BASF, Dow, Huntsman, Sherwin-Williams, and AkzoNobel collectively control nearly 44% of market activity through broad product portfolios and integrated supply capabilities. Competition is increasingly centered on sustainable formulations, automated application performance, and regional supply resilience rather than price alone. Advanced water-based coating technologies improve operational efficiency by 21%, while localized production strategies reduce delivery lead times by nearly 18%, creating strong differentiation advantages. Global suppliers are accelerating vertical integration, expanding regional manufacturing, and forming automation partnerships to secure industrial contracts and strengthen procurement reliability. Meanwhile, mid-sized regional manufacturers compete aggressively through lower-cost customized solutions for infrastructure and industrial flooring applications. Rising compliance standards and raw material volatility are increasing entry barriers, forcing companies to combine innovation speed, scalable manufacturing, and supply chain control to sustain competitive positioning.

BASF SE

Dow Inc.

Huntsman Corporation

AkzoNobel N.V.

Sherwin-Williams Company

PPG Industries, Inc.

RPM International Inc.

Covestro AG

Axalta Coating Systems

Sika AG

Kansai Paint Co., Ltd.

Nippon Paint Holdings Co., Ltd.

Jotun Group

Hempel A/S

Advanced water-based polyurethane and silicone foam coating systems are redefining industrial coating performance across construction, automotive, and thermal insulation applications. More than 46% of new coating deployments in 2026 utilize low-VOC formulations integrated with automated spray technologies to improve material consistency and reduce overspray waste. AI-enabled viscosity monitoring systems are improving application precision by 24% while lowering coating defects by 18% across high-volume manufacturing facilities. Compared with conventional solvent-heavy coating systems, automated water-based technologies reduce operational energy consumption by nearly 21% and improve curing efficiency by 27%, creating measurable cost and compliance advantages for large-scale industrial users.

Emerging technologies are accelerating integration between smart manufacturing and high-performance coating chemistry. Nanostructured thermal barrier coatings and graphene-enhanced foam systems are increasing heat resistance by approximately 19% while extending coating lifecycle durability under extreme industrial conditions. Robotic coating lines now operate across nearly 38% of advanced industrial facilities, particularly in automotive and aerospace applications where precision and throughput optimization are critical. Companies investing in hybrid polyurethane-silicone formulations are securing competitive advantages through faster deployment cycles, lower maintenance frequency, and stronger compliance positioning in regulated infrastructure projects.

Disruptive technologies between 2026 and 2028 are shifting focus toward recyclable polymer coatings, predictive maintenance integration, and adaptive coating intelligence systems. Smart sensor-enabled coatings capable of monitoring thermal stress and surface degradation are moving from pilot deployment into industrial-scale applications. Leading manufacturers are accelerating partnerships with automation and specialty materials providers to optimize production resilience and reduce lifecycle servicing costs. Businesses acting now on advanced sustainable formulations, AI-driven coating automation, and intelligent thermal protection technologies are positioning themselves ahead of tightening compliance standards and rapidly evolving industrial procurement requirements.

March 2025 – BASF expanded polyester and polyurethane resin production capacity at its Caojing facility in Shanghai from 8,000 to 18,800 metric tons annually to strengthen automotive coating supply reliability across Asia-Pacific. The highly automated facility also operates on 100% renewable energy, improving regional production responsiveness and sustainability positioning. [Capacity Scale-Up] Source: BASF

June 2025 – Huntsman Corporation launched the POLYRESYST® EV5005 intumescent polyurethane coating system for electric vehicle battery protection, enhancing passive fire resistance without compromising structural flexibility. The development supports stricter EV safety requirements and strengthens Huntsman’s positioning in advanced automotive thermal protection technologies. [EV Safety Push] Source: Huntsman Corporation

May 2024 – AkzoNobel established a dedicated Sustainable Innovation Team within its Industrial Coatings division to accelerate low-emission coating development and support carbon reduction initiatives targeting a 50% value-chain emissions reduction objective by 2030. The move strengthens sustainability-led product alignment across packaging, wood, and industrial coating segments. [Sustainability Integration] Source: AkzoNobel

February 2026 – Evonik announced expansion of global hydroxyl-terminated polybutadiene production capacity in Germany and Asia, with new infrastructure scheduled for operational deployment in 2027. The initiative improves regional supply proximity and strengthens advanced coating material availability for high-performance industrial applications. [Supply Localization] Source: Evonik

This report delivers comprehensive coverage of the foam coatings market across key product types including polyurethane, acrylic, silicone, epoxy, and elastomeric coatings. It evaluates major applications such as roof insulation, waterproofing, thermal protection, corrosion resistance, industrial flooring, and wall insulation while assessing demand across construction, automotive, aerospace, marine, industrial manufacturing, and energy sectors. The analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, incorporating operational trends, production shifts, supply chain restructuring, and sustainability-driven technology adoption patterns shaping the market between 2026 and 2033.

The report analyzes more than 15 strategic market indicators, including adoption intensity, regional production concentration, technology deployment levels, and procurement transformation trends. Advanced water-based coating systems account for over 42% of new industrial installations, while automated coating technologies are improving application efficiency by nearly 24% across large-scale manufacturing facilities. The study also evaluates emerging technologies such as AI-integrated coating automation, nanostructured thermal barriers, and recyclable polymer formulations that are redefining industrial performance standards.

Strategically, the report supports investment prioritization, regional expansion planning, supplier benchmarking, and competitive positioning by identifying where demand concentration, technology acceleration, and operational transformation are reshaping future industry leadership.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 30100 Million |

|

Market Revenue in 2033 |

USD 50568.7 Million |

|

CAGR (2026 - 2033) |

6.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Dow Inc., Huntsman Corporation, AkzoNobel N.V., Sherwin-Williams Company, PPG Industries, Inc., RPM International Inc., Covestro AG, Axalta Coating Systems, Sika AG, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Jotun Group, Hempel A/S |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |