Reports

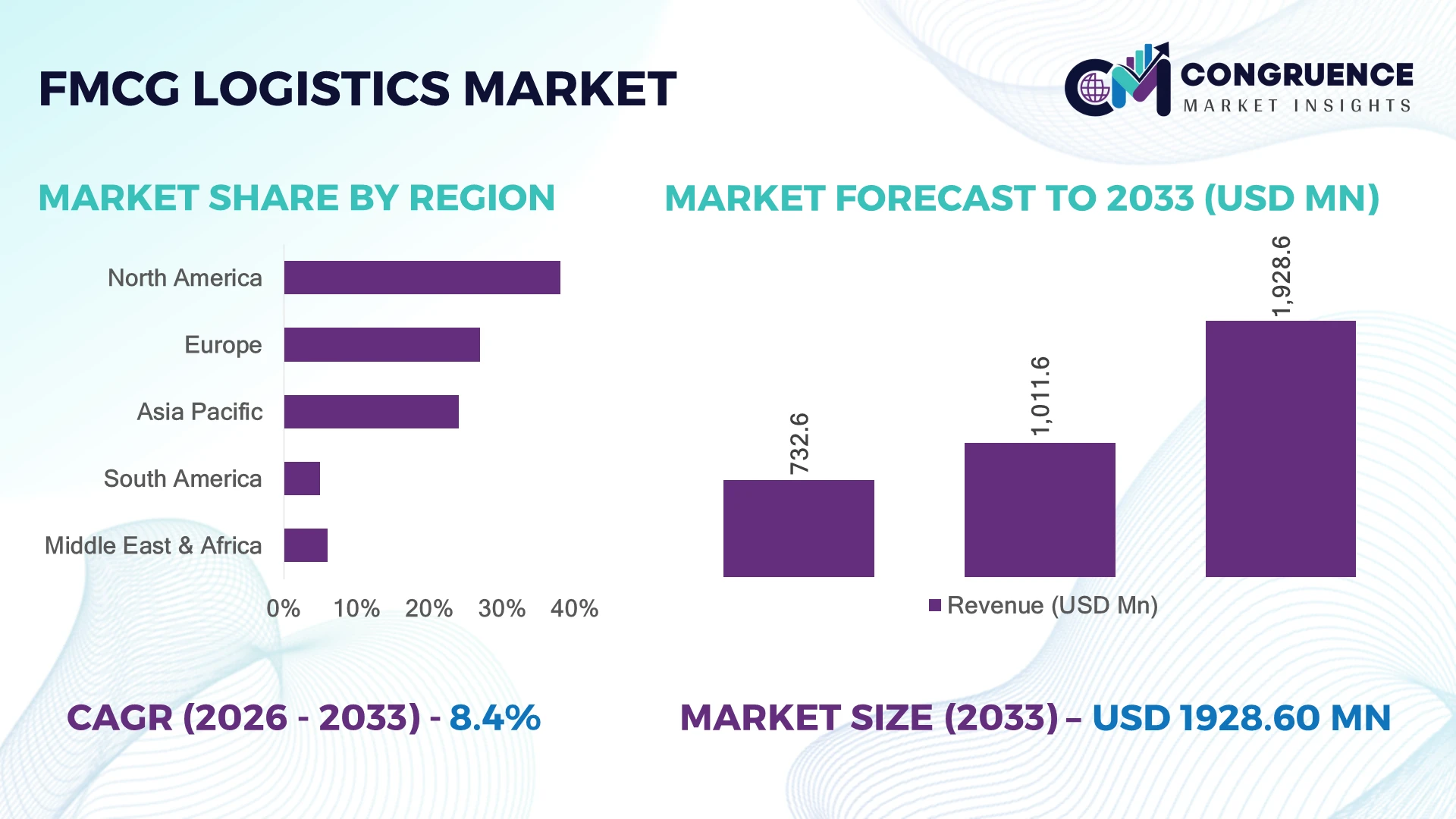

The Global FMCG Logistics Market was valued at USD 1011.6 Million in 2025 and is anticipated to reach a value of USD 1928.61 Million by 2033 expanding at a CAGR of 8.4% between 2026 and 2033. Growth is accelerating through AI-enabled route optimization, rapid dark warehouse deployment, temperature-controlled distribution expansion, and cross-border retail supply diversification driven by Red Sea shipping disruptions and rising urban same-day delivery volumes.

China dominates the global FMCG logistics market with nearly 29% distribution capacity share, supported by over 3,500 automated warehousing facilities and high-volume retail manufacturing clusters. India is recording faster fulfillment network expansion, with cold-chain capacity increasing by 18% in 2026 due to organized grocery retail growth and GST-linked interstate logistics optimization. Germany leads European automated pallet handling adoption above 42%, while Southeast Asia continues attracting regional distribution investments tied to e-commerce-led FMCG movement.

Strategic expansion now depends on regional warehousing automation, multimodal freight resilience, and last-mile delivery digitization to secure cost-efficient high-frequency FMCG distribution networks.

Market Size & Growth: USD 1011.6 Million in 2025 reaching USD 1928.61 Million by 2033, driven by AI-based route optimization and high-speed urban fulfillment expansion at 8.4% CAGR.

Top Growth Drivers: E-commerce FMCG deliveries increased 31%, cold-chain logistics adoption rose 22%, and warehouse automation deployment expanded 27% globally.

Short-Term Forecast: By 2027, smart fleet tracking and predictive inventory systems will reduce delivery delays by 19% and fuel costs by 14%.

Emerging Technologies: AI routing, robotic palletization, and IoT-enabled fleet monitoring improved warehouse productivity by 26% across advanced logistics hubs.

Regional Leaders: Asia-Pacific exceeds USD 720 Million supported by automated distribution centers, North America surpasses USD 510 Million with real-time freight analytics adoption, and Europe crosses USD 430 Million through sustainable transport integration.

Consumer/End-User Trends: Over 64% of urban consumers now expect same-day or next-day FMCG delivery, accelerating micro-fulfillment investments.

Pilot/Case Example: In 2026, a multinational FMCG distributor reduced spoilage losses by 21% after deploying AI-enabled cold-chain visibility systems across regional warehouses.

Competitive Landscape: Leading operators control nearly 38% market share, with DHL, DB Schenker, Kuehne+Nagel, CEVA Logistics, and Nippon Express expanding automated fulfillment assets.

Regulatory & ESG Impact: Electric delivery fleets lowered urban logistics emissions by 17% following stricter carbon compliance policies across Europe and Asia.

Investment & Funding: Global logistics infrastructure investments exceeded USD 24 Billion in 2026, led by warehouse robotics partnerships and regional distribution expansion strategies.

Innovation & Future Outlook: Autonomous delivery pilots, digital freight twins, and hyperlocal fulfillment networks are reshaping high-frequency FMCG supply chain competitiveness.

The FMCG Logistics Market is witnessing strong demand from organized grocery retail, quick-commerce operators, pharmaceutical FMCG distributors, and temperature-sensitive food supply chains. Automated sorting systems and AI-driven fleet analytics improved order accuracy by 24% in 2026, while regional sourcing strategies intensified following global shipping route disruptions. Sustainability-focused electric delivery fleets and micro-fulfillment centers are also strengthening operational agility, creating a strong foundation for long-term strategic logistics transformation.

The FMCG logistics market has become strategically critical as retailers, manufacturers, and e-commerce platforms compete on fulfillment speed, inventory visibility, and supply-chain resilience rather than product availability alone. Global supply-chain restructuring after Red Sea shipping disruptions and rising fuel-cost volatility accelerated investment into regional distribution hubs, automated warehousing, and multimodal transport corridors. In 2026, over 46% of large FMCG distributors integrated AI-enabled transport management systems to improve delivery predictability and reduce stock replenishment delays across high-frequency retail networks.

Automated fulfillment systems now process inventory nearly 35% faster than conventional warehouse operations while lowering manual handling costs by 22%. China continues leading large-scale robotics deployment in FMCG distribution centers, whereas India is advancing rapidly through GST-driven interstate logistics integration and dark warehouse expansion in Tier-2 cities. Germany remains ahead in electric freight fleet penetration, with sustainability-linked transport contracts increasing by 19% across organized retail supply chains.

A leading grocery distributor in Southeast Asia recently deployed IoT-enabled cold-chain monitoring across 120 logistics nodes, reducing spoilage losses by 18% and improving route compliance accuracy. Over the next three years, companies are prioritizing warehouse automation partnerships, micro-fulfillment expansion, and predictive inventory platforms to strengthen operational agility. Competitive positioning increasingly depends on logistics intelligence, delivery consistency, and scalable last-mile infrastructure capabilities.

AI-driven route optimization, warehouse automation, and quick-commerce expansion are reshaping FMCG logistics operations across high-density retail markets. In 2026, automated picking systems improved order processing efficiency by 28%, while predictive fleet analytics reduced fuel consumption by 14% in large distribution networks. India’s organized grocery retail expansion and China’s smart warehousing investments accelerated deployment of robotics-enabled fulfillment centers near urban consumption hubs. Companies are responding through regional cold-storage expansion, transport digitization, and strategic partnerships with logistics technology providers. A notable operational shift involves FMCG manufacturers relocating inventory closer to consumption zones to reduce delivery cycles below 24 hours. This structural transition is strengthening inventory turnover efficiency while improving retailer service reliability in high-frequency replenishment environments.

Rising transportation costs, fragmented warehousing infrastructure, and inconsistent multimodal connectivity continue limiting operational scalability in the FMCG logistics market. Diesel-linked freight expenses increased nearly 16% across major Asian transport corridors in 2026, while cold-chain utilization gaps in India and Indonesia still exceed 25% in secondary cities. Port congestion and customs delays linked to Red Sea route disruptions extended average cross-border FMCG shipment timelines by 11%. These pressures directly affect inventory planning, spoilage management, and delivery predictability for high-turnover consumer products. Companies are mitigating exposure through localized sourcing contracts, decentralized warehousing models, and long-term carrier agreements. A growing strategic response involves shifting from centralized mega-warehouses toward smaller urban fulfillment clusters to reduce transportation dependency and last-mile volatility.

Hyperlocal distribution models, AI-enabled demand forecasting, and electric delivery ecosystems are creating high-value opportunities across the FMCG logistics market. In 2026, micro-fulfillment deployment increased by 24% in urban retail networks, while predictive inventory systems improved stock accuracy by 31% for large grocery chains. Japan and South Korea are accelerating adoption of autonomous warehouse transport systems to address labor shortages and improve throughput consistency. Companies are increasingly investing in edge-based logistics analytics, real-time cold-chain visibility, and sustainable delivery fleets to reduce operational waste and improve urban delivery density. A non-obvious opportunity is emerging in rural digitized distribution networks, where mobile inventory tracking platforms are improving FMCG reach into underserved consumption zones with lower infrastructure investment requirements.

The FMCG logistics market faces growing execution complexity as companies integrate AI platforms, automated warehouses, legacy ERP systems, and multi-carrier transport networks simultaneously. In 2026, nearly 38% of logistics operators reported interoperability issues between warehouse management software and transport visibility platforms. Cybersecurity incidents targeting logistics infrastructure increased by 21%, particularly across digitally connected cold-chain networks handling sensitive inventory data. Workforce adaptation also remains a major pressure point, with automated fulfillment facilities in Germany and the United States facing skilled technician shortages exceeding 17%. These challenges directly impact deployment consistency, system uptime, and real-time inventory synchronization. Companies must strengthen cloud-security architecture, workforce reskilling programs, and cross-platform integration frameworks while expanding resilient digital infrastructure to sustain long-term operational competitiveness.

AI-Controlled Delivery Optimization AI-powered route orchestration platforms reduced urban FMCG delivery turnaround time by 23% in 2026, while predictive dispatch systems improved fleet utilization by 18%. Indian grocery distributors and Chinese quick-commerce operators are integrating real-time traffic analytics with warehouse management software to minimize failed deliveries and idle transport capacity. Companies are restructuring logistics workflows through cloud-based control towers and AI partnerships to improve replenishment consistency during fuel-cost volatility and congested urban distribution cycles.

Micro-Fulfillment Network Expansion FMCG retailers increased micro-fulfillment center deployment by 27% across high-density cities as same-day delivery expectations exceeded 61% among urban consumers. Automated dark warehouses now process nearly 32% more orders per hour than conventional retail backrooms. In Japan and South Korea, retailers are repositioning inventory closer to consumption clusters to reduce dependency on centralized warehousing. Companies are scaling modular storage systems and robotics integration to improve inventory rotation speed and lower last-mile transportation costs.

Electric Fleet Transition Accelerates Electric delivery vehicle adoption in FMCG logistics rose 21% following stricter urban emission regulations and rising diesel operating costs. Germany and the Netherlands expanded low-emission freight corridors, pushing logistics operators toward battery-powered fleets and AI-managed charging systems. Companies are restructuring transportation contracts and partnering with charging infrastructure providers to stabilize operating expenses. A less visible shift involves retailers prioritizing carbon-efficient suppliers within procurement-linked logistics scoring frameworks.

Cold-Chain Digitization Intensifies IoT-enabled cold-chain monitoring deployment expanded by 26% across pharmaceutical FMCG and packaged food distribution networks in 2026. Real-time temperature visibility reduced spoilage incidents by 17% while improving compliance accuracy across cross-border shipments. Southeast Asian distributors are integrating sensor-based monitoring with predictive maintenance platforms to address climate-sensitive transportation risks. Companies are investing in automated refrigeration analytics, smart pallet tracking, and regional cold-storage expansion to strengthen inventory integrity under increasingly volatile shipping conditions.

Transportation remains the leading segment within the FMCG logistics market due to its central role in high-frequency replenishment, last-mile delivery execution, and interstate inventory movement. Large FMCG distributors allocate nearly 42% of operational logistics spending toward fleet operations, freight optimization, and multimodal connectivity. AI-enabled transportation management systems improved route efficiency by 19% in 2026, particularly across India and China where same-day retail fulfillment volumes continue rising sharply. Companies are expanding electric fleet partnerships, deploying telematics-based tracking systems, and strengthening regional transport hubs to reduce delivery variability and fuel dependency.

Cold Chain Logistics is emerging as the fastest-growing segment as demand increases for temperature-sensitive packaged foods, dairy products, and pharmaceutical FMCG distribution. IoT-based refrigeration monitoring reduced spoilage losses by 18% across advanced cold-storage facilities in 2026. Warehousing and Distribution segments continue evolving through robotics deployment and automated sorting integration, while Inventory Management platforms are becoming operationally critical for predictive replenishment and stock visibility. Companies are prioritizing integrated logistics ecosystems combining transport analytics, cold-storage automation, and digital inventory synchronization to improve supply-chain resilience and retailer fulfillment accuracy.

Food and Beverages remains the dominant application segment due to high inventory turnover, temperature-sensitive transportation requirements, and continuous replenishment demand across organized retail channels. In 2026, nearly 58% of high-frequency FMCG logistics volumes were linked to packaged foods, dairy products, and beverage distribution networks. Retailers in India and the United States increased automated grocery fulfillment deployment by 24% to support rapid urban delivery expectations. Companies are strengthening cold-storage integration, AI-based demand forecasting, and regional fulfillment density to improve shelf availability and reduce spoilage exposure.

Retail Distribution is emerging as the fastest-growing application as omnichannel commerce and quick-commerce platforms reshape inventory movement patterns. Automated retail logistics systems improved order accuracy by 21% across digitally integrated fulfillment centers. Personal Care Products and Household Products continue benefiting from subscription-driven replenishment models and lightweight packaging optimization, while Packaged Goods logistics is increasingly supported through micro-fulfillment deployment and predictive inventory balancing. Companies are scaling integrated warehouse-retail ecosystems and partnering with digital commerce operators to improve replenishment speed, stock visibility, and delivery flexibility across urban consumption hubs.

Retail Chains represent the leading end-user segment due to extensive fulfillment infrastructure, high inventory throughput, and increasing dependence on real-time replenishment systems. In 2026, large retail operators accounted for nearly 37% of organized FMCG logistics deployment activity, driven by same-day delivery expansion and automated warehouse scaling. Supermarkets and Hypermarkets continue modernizing regional distribution centers through robotics integration and AI-based inventory synchronization. Companies are responding with dedicated transport contracts, customized fulfillment solutions, and predictive analytics platforms to improve shelf availability and reduce stock-out frequency in high-volume retail networks.

E-commerce Companies are emerging as the fastest-growing end-user segment as quick-commerce and app-based grocery delivery platforms expand aggressively across urban markets. Dark-store linked logistics operations improved delivery cycle efficiency by 26% in digitally integrated fulfillment environments during 2026. Food and Beverage Companies are increasing cold-chain investments, while Consumer Goods Manufacturers and Wholesale Distributors are prioritizing decentralized warehousing and transport visibility systems to improve operational responsiveness. Logistics providers are strengthening ecosystem partnerships, scalable pricing structures, and hyperlocal delivery capabilities to secure long-term contracts from rapidly digitizing FMCG distribution networks.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

Automation-Led Retail Fulfillment Modernization

North America maintains a highly advanced FMCG logistics ecosystem supported by dense warehousing infrastructure, integrated freight networks, and strong quick-commerce penetration. The region accounted for nearly 27% of global automated FMCG fulfillment deployments in 2025, led by AI-enabled inventory synchronization and robotics-driven distribution centers. Large retailers and consumer goods manufacturers are increasingly shifting toward predictive logistics platforms to improve delivery precision and reduce labor dependency. In 2026, transport visibility adoption across organized FMCG supply chains exceeded 54%, improving route efficiency and inventory replenishment consistency. Strategic partnerships between logistics operators and cloud analytics providers are strengthening high-frequency retail fulfillment capabilities, particularly across temperature-sensitive packaged food and grocery distribution operations.

United States Market Outlook: The United States leads the regional FMCG logistics market through advanced transportation infrastructure, large-scale automated warehousing, and aggressive omnichannel retail deployment. More than 62% of organized grocery retailers integrated AI-based demand forecasting platforms in 2026 to improve stock rotation and delivery speed. Major operators are investing heavily in electric delivery fleets, robotics-assisted fulfillment centers, and regional cold-chain expansion to support same-day retail logistics execution across urban and suburban distribution networks.

Sustainability-Driven Distribution Restructuring

Europe is reshaping FMCG logistics operations through low-emission freight policies, warehouse modernization, and digitally integrated transport systems. The region holds nearly 24% of global sustainable logistics deployment activity, supported by expanding electric freight corridors and carbon-linked retail procurement standards. Germany, France, and the Netherlands are accelerating smart warehouse investments to improve inventory efficiency and reduce transport-related emissions. In 2026, electric delivery fleet utilization increased by 22% across organized FMCG retail logistics networks. Companies are restructuring transportation contracts and integrating route optimization software to comply with tightening urban emission regulations while improving delivery density and operational reliability in high-volume retail corridors.

Germany Market Outlook: Germany remains the strategic logistics hub of Europe due to its advanced freight infrastructure, automated warehousing leadership, and industrial distribution connectivity. Over 45% of large FMCG distribution centers in Germany deployed robotics-assisted pallet handling systems in 2026 to improve throughput consistency and reduce labor-intensive operations. The country also leads cross-border multimodal freight integration, supporting high-volume FMCG inventory movement between manufacturing hubs and organized retail supply chains.

High-Volume Infrastructure and Quick-Commerce Expansion

Asia-Pacific dominates the FMCG logistics market through large-scale manufacturing activity, rapid urban retail expansion, and accelerated warehouse automation deployment. China and India collectively account for over 46% of regional high-frequency FMCG distribution volume, supported by dense fulfillment infrastructure and rising same-day delivery demand. In 2026, automated sorting and transport visibility systems improved operational throughput by 29% across major regional logistics hubs. Retailers and logistics providers are aggressively scaling dark warehouses, AI-enabled inventory management platforms, and decentralized delivery networks to support digitally driven consumer purchasing behavior and expanding urban consumption clusters.

China Market Outlook: China leads the regional market through its extensive automated warehousing base, advanced e-commerce logistics ecosystem, and strong manufacturing integration. More than 3,500 smart distribution facilities were operational across key industrial corridors in 2026, enabling rapid inventory movement for packaged goods and grocery retail chains. Chinese logistics operators are increasingly integrating robotics, autonomous guided vehicles, and AI-driven route planning systems to improve delivery efficiency and reduce warehouse processing delays across high-density urban markets.

Urban Distribution Network Expansion

South America is experiencing steady FMCG logistics modernization driven by urban consumption growth, organized retail expansion, and increasing investment in regional warehousing infrastructure. Brazil and Chile remain key deployment centers for automated inventory management and cold-chain logistics systems supporting packaged food and beverage distribution. In 2026, urban fulfillment capacity utilization increased by 18% across large metropolitan logistics corridors. However, inconsistent road infrastructure and customs bottlenecks continue affecting cross-border shipment predictability. Companies are responding through localized warehousing strategies, transport fleet optimization, and strategic carrier partnerships to improve replenishment speed and operational continuity across fragmented retail supply environments.

Brazil Market Outlook: Brazil dominates the South American FMCG logistics market through its extensive consumer base, expanding retail infrastructure, and growing e-commerce-linked distribution activity. In 2026, automated warehouse deployment across major FMCG retail corridors increased by 21%, particularly around São Paulo and Rio de Janeiro. Logistics operators are prioritizing route optimization systems, regional cold-storage expansion, and integrated last-mile delivery partnerships to manage rising fulfillment demand and improve inventory flow efficiency.

Infrastructure Modernization and Trade Corridor Investment

Middle East & Africa is rapidly strengthening FMCG logistics capabilities through port modernization, smart warehousing investment, and trade corridor expansion. The region is gaining strategic importance due to rising organized retail penetration and large-scale infrastructure development across Gulf economies. In 2026, smart logistics infrastructure investment across the UAE and Saudi Arabia increased by 24%, supporting automated freight handling and temperature-controlled storage expansion. Companies are increasingly deploying digital freight tracking systems and integrated transport platforms to improve inventory visibility and reduce cross-border delivery inefficiencies. Growing demand for packaged food imports and pharmaceutical FMCG distribution is also accelerating cold-chain infrastructure deployment across major urban trade hubs.

United Arab Emirates Market Outlook: The UAE remains the leading logistics gateway within the Middle East & Africa FMCG logistics market due to its advanced port infrastructure, free-trade connectivity, and high warehouse automation adoption. In 2026, over 41% of large-scale FMCG distribution facilities in the UAE integrated AI-enabled freight visibility systems to improve shipment coordination and delivery precision. The country continues attracting regional fulfillment investments linked to cross-border retail distribution and high-volume import-driven consumer supply chains.

The FMCG logistics market is dominated by competition between global logistics leaders such as DHL, Kuehne+Nagel, DB Schenker, CEVA Logistics, and Nippon Express against aggressive regional distribution specialists and technology-driven fulfillment operators. The top five players collectively control nearly 38% of organized FMCG logistics activity through integrated warehousing, multimodal transportation, and high-density retail fulfillment capabilities. Competition increasingly centers on delivery speed, automated inventory management, cold-chain reliability, and AI-enabled route optimization, with digitally integrated operators reducing operational costs by nearly 18% and warehouse processing time by 25%. Large enterprises are expanding through warehouse automation partnerships, regional acquisition strategies, and vertically integrated distribution ecosystems. Regional firms are competing aggressively on localized delivery flexibility and cost-efficient last-mile operations. Rising infrastructure investment requirements, interoperability complexity, and enterprise-scale automation costs continue creating strong entry barriers. Long-term competitive advantage now depends on logistics intelligence, fulfillment scalability, infrastructure depth, and technology-led operational consistency.

DHL Supply Chain

Kuehne+Nagel

DB Schenker

CEVA Logistics

Nippon Express

DSV A/S

XPO Logistics

C.H. Robinson

FedEx Logistics

UPS Supply Chain Solutions

Ryder System

GXO Logistics

Expeditors International

GEODIS

AI-enabled transport management systems, warehouse robotics, and IoT-based fleet monitoring currently define the operational backbone of the FMCG logistics market. In 2026, nearly 52% of large FMCG distributors integrated predictive route optimization platforms, reducing fuel consumption by 14% and delivery delays by 19%. Automated warehouse sorting systems process inventory approximately 31% faster than conventional manual workflows while lowering picking inaccuracies by 22%. Companies are integrating real-time inventory visibility with cloud-connected transport orchestration platforms to improve replenishment precision and retailer service consistency across high-frequency delivery environments.

Emerging technologies between 2026 and 2028 include autonomous guided vehicles, AI-powered demand forecasting, digital freight twins, and smart cold-chain analytics. IoT-enabled refrigeration monitoring improved spoilage control efficiency by 17% across temperature-sensitive FMCG distribution operations. Japan and Germany are accelerating deployment of robotic pallet handling systems as logistics labor shortages intensify. Companies benefiting most include organized grocery retailers, quick-commerce operators, and multinational consumer goods manufacturers requiring rapid fulfillment scalability and high inventory turnover accuracy across urban consumption corridors.

Disruptive innovation is shifting toward agentic AI logistics orchestration, edge-based fulfillment intelligence, and autonomous last-mile delivery systems. AI-assisted logistics networks achieved nearly 25% faster route responsiveness compared with legacy dispatch planning models in 2026. By 2028, competitive advantage will increasingly depend on integrated automation ecosystems, predictive freight synchronization, and digitally resilient fulfillment infrastructure capable of managing volatile supply-chain conditions and rising same-day delivery expectations.

March 2026 – DHL Supply Chain announced expansion of 10 dedicated North American logistics facilities exceeding 7 million sq ft capacity to support high-speed distribution operations and AI-driven fulfillment workflows. The move strengthens large-scale warehousing responsiveness and integrated transport execution across complex supply chains.

May 2025 – CEVA Logistics launched a new strategic warehouse project in Singapore, increasing total regional warehouse footprint to 370,000 square meters. The facility includes automated logistics capabilities designed to improve FMCG inventory throughput and regional distribution flexibility across Southeast Asian trade corridors. Source: cevalogistics.com cevalogistics.com

April 2025 – CMA CGM subsidiary CEVA Logistics agreed to acquire Borusan’s logistics division in Turkey, adding approximately 570,000 square meters of warehousing capacity and expanding annual domestic shipment handling toward 1 million deliveries. The acquisition strengthens regional FMCG transport integration and European freight connectivity.

June 2026 – DHL Supply Chain expanded Asia-Pacific logistics infrastructure with more than 160,000 square meters of dedicated warehousing capacity across Malaysia, Thailand, and Singapore. The development improves regional high-volume inventory handling, advanced logistics processing, and cross-border fulfillment efficiency under rising digital commerce demand. Source: group.dhl.com

The FMCG Logistics Market report delivers detailed analysis across transportation, warehousing, distribution, cold-chain logistics, and inventory management segments, covering operational deployment patterns, technology integration trends, and enterprise-level infrastructure strategies between 2026 and 2033. The study evaluates applications including food and beverages, packaged goods, household products, retail distribution, and personal care logistics while examining adoption behavior across retail chains, e-commerce companies, supermarkets, wholesalers, and consumer goods manufacturers. More than 45% of the analysis focuses on automation-linked logistics transformation, transport visibility systems, and AI-driven fulfillment optimization.

The report provides region-wise operational insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, warehouse automation penetration, and cross-border distribution expansion. It also examines strategic developments such as electric fleet deployment, hyperlocal fulfillment scaling, and smart cold-chain investments. Business intelligence coverage supports expansion planning, supply-chain restructuring, investment prioritization, technology benchmarking, and competitive positioning for logistics operators, FMCG enterprises, and institutional stakeholders navigating high-frequency retail distribution transformation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1011.6 Million |

|

Market Revenue in 2033 |

USD 1928.61 Million |

|

CAGR (2026 - 2033) |

8.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DHL Supply Chain, Kuehne+Nagel, DB Schenker, CEVA Logistics, Nippon Express, DSV A/S, XPO Logistics, C.H. Robinson, FedEx Logistics, UPS Supply Chain Solutions, Ryder System, GXO Logistics, Expeditors International, GEODIS |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |