Reports

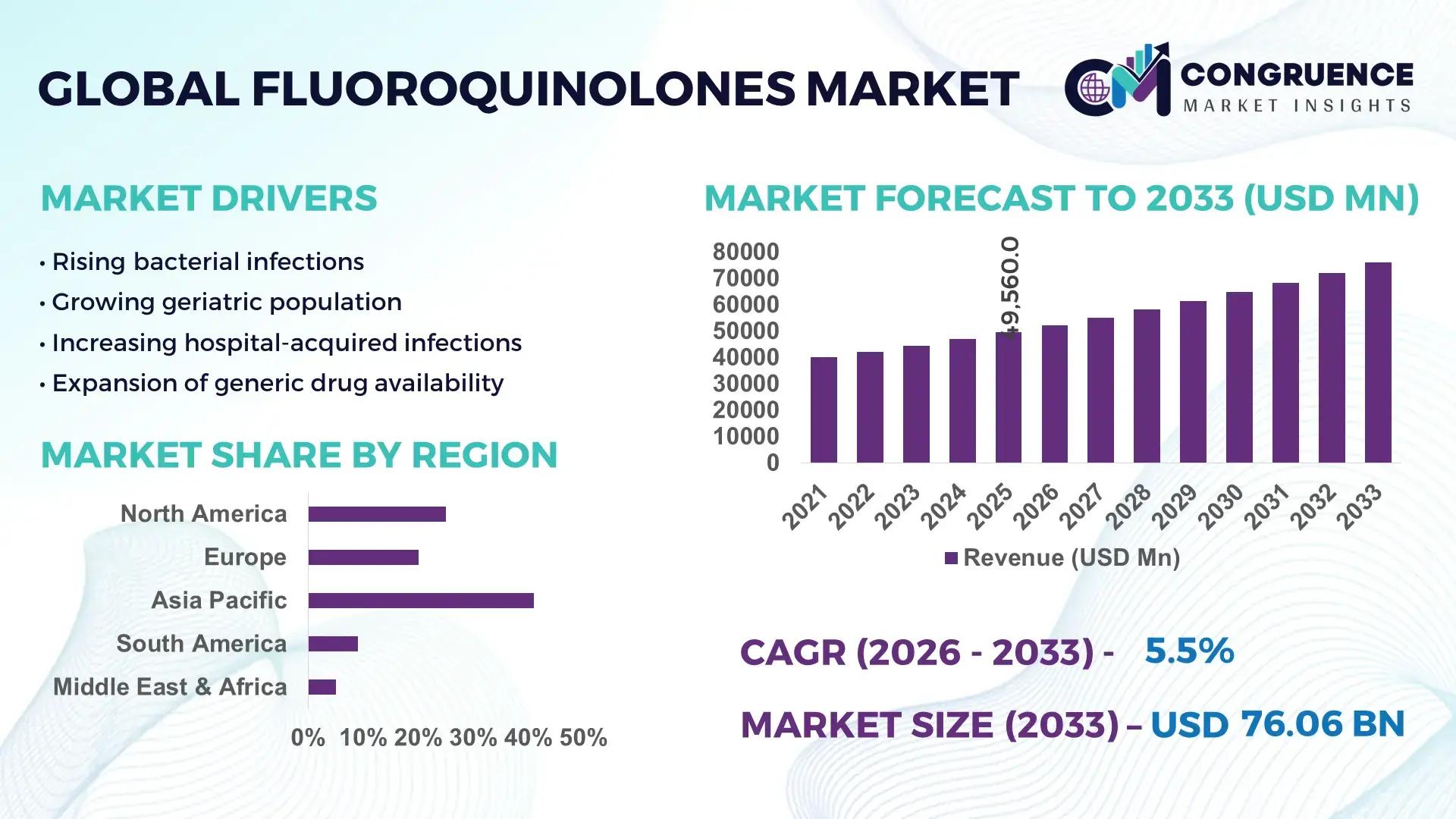

The Global Fluoroquinolones Market was valued at USD 49560 Million in 2025 and is anticipated to reach a value of USD 76059 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. Growth is supported by rising bacterial infection incidence and sustained demand for broad-spectrum antibacterial therapies.

China represents the leading production hub for fluoroquinolone active pharmaceutical ingredients (APIs), supported by large-scale antibiotic manufacturing clusters in provinces such as Zhejiang and Jiangsu. The country hosts over 150 GMP-compliant anti-infective manufacturing facilities, with annual antibiotic API output exceeding 200,000 metric tons. Significant capital investments in continuous manufacturing and fermentation optimization technologies have improved yield efficiency by nearly 18% over the past five years. Domestic pharmaceutical firms increasingly deploy advanced crystallization and impurity-control technologies to meet stringent export standards. Key applications include respiratory, urinary, and gastrointestinal infection treatments across hospital and retail channels, while government-backed pharmaceutical modernization programs continue to accelerate process automation and quality compliance upgrades.

Market Size & Growth: Valued at USD 49,560 Million in 2025, projected to reach USD 76,059 Million by 2033 at a CAGR of 5.5%, driven by higher prevalence of drug-resistant infections.

Top Growth Drivers: Hospital antibiotic utilization up 12%, outpatient prescription rates up 9%, generic drug penetration up 15%.

Short-Term Forecast: By 2028, treatment cost efficiency expected to improve by 11% through generic substitution and bulk procurement models.

Emerging Technologies: Continuous flow synthesis, AI-assisted drug formulation modeling, and advanced impurity profiling systems.

Regional Leaders: Asia Pacific USD 28,400 Million by 2033 with high generic adoption; North America USD 19,600 Million with strong hospital usage; Europe USD 15,800 Million driven by regulated prescribing practices.

Consumer/End-User Trends: Hospitals account for over 48% of demand, with increasing outpatient and telemedicine-linked prescription fulfillment.

Pilot or Case Example: A 2024 hospital antimicrobial stewardship pilot reduced broad-spectrum misuse by 17%, improving therapy targeting accuracy.

Competitive Landscape: Teva Pharmaceutical holds approximately 14% share, followed by Sun Pharma, Bayer, Aurobindo Pharma, and Viatris.

Regulatory & ESG Impact: Stricter antibiotic stewardship frameworks and wastewater discharge standards influencing manufacturing upgrades.

Investment & Funding Patterns: Over USD 2.1 Billion invested in anti-infective production modernization and capacity expansion since 2023.

Innovation & Future Outlook: Focus on resistance-monitoring platforms, combination therapies, and environmentally sustainable antibiotic production.

Fluoroquinolones are widely utilized across hospital, ambulatory, and retail healthcare channels, with respiratory and urinary infection treatments contributing over 55% of total demand. Recent product innovation emphasizes improved bioavailability and reduced side-effect profiles through advanced formulation science. Regulatory pressure to curb antimicrobial resistance is reshaping prescribing protocols, while environmental mandates are driving cleaner API production processes. Asia Pacific demonstrates strong volume consumption, whereas North America and Europe emphasize high-value, regulated usage. Growing adoption of stewardship programs, digital prescription monitoring, and combination anti-infective therapies signals a shift toward precision antibiotic utilization, positioning the sector for stable, compliance-driven growth in the coming decade.

Fluoroquinolones remain strategically relevant within the global anti-infective landscape due to their broad-spectrum efficacy, high oral bioavailability exceeding 70% in leading molecules, and strong penetration in hospital formularies for respiratory and urinary infections. Healthcare systems continue to rely on these therapies for first-line and second-line treatment protocols, particularly in regions reporting double-digit increases in antimicrobial resistance surveillance cases. From a strategy perspective, manufacturers are prioritizing cost-efficient generic production, lifecycle management, and advanced impurity-control technologies to align with tightening pharmacopoeial standards and global antibiotic stewardship frameworks.

Continuous flow synthesis delivers 20% yield efficiency improvement compared to traditional batch processing, enabling scalability and reduced solvent waste. Asia Pacific dominates in volume, while North America leads in adoption with over 65% of hospitals operating formal antimicrobial stewardship programs. By 2028, AI-driven formulation modeling is expected to improve development cycle efficiency by 18%, accelerating regulatory submission readiness and quality optimization.

Compliance and ESG performance are increasingly embedded in corporate strategies. Firms are committing to 30% solvent recovery and wastewater load reduction by 2030, supported by green chemistry investments and closed-loop manufacturing systems. In 2024, an Indian pharmaceutical manufacturer achieved a 22% reduction in production impurities through automated process analytics integration. Looking ahead, the Fluoroquinolones Market is positioned as a pillar of healthcare resilience, regulatory alignment, and sustainable pharmaceutical manufacturing growth.

Bacterial infections remain a significant contributor to global morbidity, with respiratory and urinary tract infections accounting for millions of hospital visits annually. Urbanization, aging populations, and increased chronic disease prevalence have raised susceptibility to infections requiring systemic antibacterial therapy. Hospital antibiotic utilization programs show steady year-on-year increases in treatment volumes, particularly in intensive care units where broad-spectrum coverage is required. Fluoroquinolones are favored due to high tissue penetration and oral-to-IV switch capability, reducing hospital stay duration by up to 10% in certain treatment pathways. Expanding diagnostic capabilities and faster microbial identification also lead to earlier initiation of targeted therapy. Emerging economies are scaling healthcare infrastructure, increasing hospital bed capacity and pharmaceutical access. These structural healthcare expansions directly support higher prescription volumes of established antibacterial classes, including fluoroquinolones, especially in community-acquired infection management.

The increasing prevalence of resistant bacterial strains has prompted stricter prescribing controls and guideline revisions. Surveillance programs in multiple regions report rising resistance rates in common pathogens, leading to restrictions on empirical broad-spectrum antibiotic use. Regulatory bodies now require stewardship compliance, reducing routine prescriptions and encouraging narrow-spectrum alternatives when possible. Safety concerns, including warnings related to tendon, neurological, and cardiac side effects, have also influenced physician prescribing behavior. Some healthcare systems mandate prior authorization or infectious disease specialist approval for certain indications. These policies, while clinically necessary, reduce volume growth potential. Additionally, environmental discharge regulations targeting antibiotic residues in manufacturing effluent increase operational compliance costs. Together, clinical caution and regulatory oversight constrain unrestricted usage, shifting the market toward more controlled and indication-specific deployment.

Process innovation presents substantial opportunities in improving cost efficiency and compliance. Adoption of continuous manufacturing, advanced crystallization, and real-time quality monitoring can enhance yield efficiency by over 15% while reducing solvent consumption. Novel formulations with improved pharmacokinetics and reduced adverse event profiles extend product lifecycle potential. Expanding access to healthcare in developing regions, where antibiotic penetration remains comparatively lower, opens new demand channels. Digital prescription systems and hospital informatics integration improve tracking and responsible use, supporting long-term sustainability of the drug class. Additionally, combination therapies targeting resistant organisms are under development, broadening clinical applications. Investments in environmentally sustainable production technologies also provide competitive differentiation, especially for suppliers targeting regulated export markets with stringent environmental compliance requirements.

Manufacturers face rising compliance burdens associated with global good manufacturing practice upgrades, pharmacovigilance requirements, and environmental discharge standards. Effluent treatment infrastructure investments can increase operational expenditure significantly, particularly in antibiotic API production where fermentation byproducts require advanced treatment. Regulatory inspections and documentation standards demand digital traceability and validation systems, adding capital intensity. Price pressure in generic-dominated markets compresses margins, limiting flexibility for smaller producers to modernize facilities. Supply chain disruptions, including raw material sourcing constraints, further affect cost stability. Additionally, litigation risks and stricter labeling requirements related to safety profiles necessitate ongoing post-market monitoring and risk management programs. These combined regulatory, financial, and operational factors create a challenging environment requiring scale, technological sophistication, and strong compliance frameworks for sustained participation.

Expansion of Hospital Stewardship-Driven Prescription Controls (Over 60% Institutional Adoption) Hospital antibiotic stewardship frameworks are reshaping usage patterns, with more than 60% of tertiary hospitals implementing digital prescription surveillance and restriction systems. These programs have reduced inappropriate broad-spectrum antibiotic use by nearly 18% while increasing targeted therapy compliance by 22%, improving clinical outcomes and optimizing antibacterial deployment efficiency.

Shift Toward High-Efficiency Continuous Manufacturing (15–20% Yield Improvement) Pharmaceutical producers are transitioning from batch synthesis to continuous flow production systems, achieving yield efficiency gains of 15–20% and reducing solvent waste by approximately 25%. Automated impurity profiling and in-line quality monitoring are lowering batch rejection rates by 12%, supporting consistent compliance with international pharmacopeial impurity thresholds.

Growth in Oral-to-IV Switch Protocols (Hospital Stay Reduced by 10–14%) Clinical adoption of oral bioequivalent fluoroquinolone formulations is increasing, with over 45% of hospital infection protocols incorporating early oral switch strategies. This shift has reduced inpatient stay durations by 10–14% and lowered treatment administration costs by roughly 9%, supporting hospital resource optimization and improved patient throughput.

Environmental Compliance Modernization in API Production (30% Wastewater Load Reduction Targets) Antibiotic API manufacturers are upgrading effluent treatment and solvent recovery systems, with facilities targeting 30% reductions in wastewater antibiotic residue concentrations. Closed-loop solvent recycling has improved material recovery rates by 20%, while energy-efficient drying and crystallization technologies are cutting process energy consumption by nearly 12%, aligning production with tightening environmental mandates.

The Fluoroquinolones market demonstrates structured segmentation across product type, therapeutic application, and end-user channels, reflecting diversified clinical deployment and supply chain specialization. Mature molecules dominate prescription volumes due to established safety data and broad-spectrum effectiveness, while newer-generation compounds address resistant bacterial strains and improved pharmacokinetic performance. Application-wise, respiratory and urinary tract infections account for the majority of therapeutic utilization, driven by hospital admission trends and outpatient antibiotic prescribing patterns. End-user distribution highlights institutional healthcare facilities as the central consumption hubs, supported by antimicrobial stewardship frameworks and centralized procurement systems. Retail and online pharmacies are expanding access, particularly in urban outpatient care, while specialty clinics support niche infection treatments. Manufacturing specialization aligns with formulation complexity, including ophthalmic, injectable, and oral solid dosage forms. Increasing digital prescription monitoring and hospital formulary controls further influence segment performance, reinforcing controlled utilization patterns and guideline-driven demand across all segmentation layers.

Fluoroquinolone products are categorized into ciprofloxacin, levofloxacin, moxifloxacin, ofloxacin, and other later-generation variants. Ciprofloxacin remains the leading type, accounting for approximately 38% of total prescription volume, supported by its broad antibacterial coverage and established use in urinary and gastrointestinal infections. Levofloxacin and moxifloxacin collectively represent nearly 34%, driven by strong adoption in respiratory infection management due to improved tissue penetration. Ofloxacin and other niche variants, including ophthalmic and topical formulations, together contribute about 28%, serving targeted clinical indications.

While ciprofloxacin maintains dominance, moxifloxacin represents the fastest-growing type, with adoption expanding at an estimated 6.8% CAGR as hospitals shift toward respiratory-focused therapies and once-daily dosing convenience. Its enhanced activity against atypical pathogens supports expanded use in community-acquired pneumonia protocols. Manufacturing upgrades in high-purity crystallization and impurity profiling further support lifecycle extension for premium molecules.

Application segmentation includes respiratory tract infections, urinary tract infections, gastrointestinal infections, skin and soft tissue infections, and others. Respiratory tract infections lead with around 36% of therapeutic use, supported by rising hospitalization rates for lower respiratory infections and established treatment guidelines incorporating respiratory fluoroquinolones. Urinary tract infections follow at 28%, reflecting high outpatient antibiotic prescription volumes. Gastrointestinal and skin-related infections collectively contribute nearly 24%, while other uses account for the remaining 12%.

Respiratory treatment is also the fastest-growing application, expanding at an estimated 6.5% CAGR, supported by aging populations and increased incidence of comorbid conditions that elevate infection risk. Hospitals increasingly deploy rapid diagnostics, enabling earlier and targeted therapy initiation. Oral-to-IV switch protocols further strengthen respiratory segment utilization by optimizing care efficiency.

End-user segmentation includes hospitals, specialty clinics, retail pharmacies, and online pharmacies. Hospitals dominate with approximately 48% of total consumption, reflecting centralized procurement systems, inpatient infection treatment, and antimicrobial stewardship compliance. Retail pharmacies account for nearly 27%, supported by outpatient prescription fulfillment. Specialty clinics contribute around 15%, focusing on dermatology, urology, and ophthalmology applications. Online pharmacies hold roughly 10%, benefiting from digital prescription adoption.

Online pharmacies represent the fastest-growing end-user group, expanding at an estimated 7.2% CAGR, driven by telemedicine integration and e-prescription platforms. Urban regions show over 40% digital prescription adoption, accelerating home-based treatment access.

Asia Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia Pacific leads due to large-scale API production clusters, where over 60% of global generic antibiotic manufacturing capacity is concentrated. The region records annual antibiotic output exceeding 200,000 metric tons, supported by more than 5,000 pharmaceutical manufacturing units. North America demonstrates high-value utilization, with over 70% of tertiary hospitals operating antimicrobial stewardship platforms and digital prescription tracking. Europe contributes nearly 24% of global demand, reflecting stringent prescribing controls and advanced hospital infrastructure. South America represents around 7% of consumption, while Middle East & Africa account for nearly 6%, driven by hospital infrastructure expansion. Across regions, more than 55% of hospital infection treatments rely on established broad-spectrum antibiotics, while digital prescription systems cover over 45% of urban healthcare facilities worldwide.

How are advanced hospital protocols reshaping antibacterial therapy utilization?

North America holds approximately 27% of global fluoroquinolone consumption volume, driven by hospital care, long-term care facilities, and outpatient clinics. Acute respiratory and urinary infection treatments account for nearly 58% of prescriptions. Over 70% of hospitals utilize electronic antimicrobial stewardship platforms that monitor antibiotic use in real time. Regulatory frameworks emphasize controlled prescribing and pharmacovigilance reporting, leading to improved safety oversight. Technological integration includes AI-enabled prescription auditing and digital formulary management systems. A regional pharmaceutical manufacturer has invested in automated sterile injectable production lines, improving batch consistency by 16%. Consumer behavior reflects strong institutional reliance, with healthcare providers prioritizing guideline-driven therapy selection and digital tracking systems to minimize misuse.

Why are stringent prescribing frameworks influencing antibacterial usage patterns?

Europe accounts for nearly 24% of global demand, with Germany, the UK, and France representing more than 60% of regional consumption. Regulatory authorities enforce antibiotic stewardship compliance and environmental discharge controls in pharmaceutical production. Over 65% of tertiary hospitals operate digital prescription monitoring platforms. Sustainability initiatives emphasize wastewater treatment upgrades, targeting 25% reduction in antibiotic residue discharge. Adoption of rapid diagnostics supports earlier targeted therapy. A European pharmaceutical firm has implemented solvent recovery systems that improved material reuse by 20%. Consumer patterns reflect cautious, protocol-based prescribing, with physicians adhering strictly to treatment guidelines and resistance-monitoring frameworks.

What manufacturing and healthcare expansion trends are accelerating antibacterial supply?

Asia-Pacific leads global volume consumption at 41%, with China, India, and Japan as key contributors. The region hosts over 60% of global antibiotic API facilities and thousands of formulation plants. Hospital infrastructure expansion exceeds 8% annual bed capacity growth in major economies. Continuous manufacturing adoption is improving production efficiency by 15%. Regional innovation hubs are integrating automated quality monitoring and green chemistry processes. A leading Indian pharmaceutical company expanded API capacity by 18% through high-efficiency synthesis upgrades. Consumer trends show strong reliance on hospital and retail pharmacy channels, with urban prescription digitization surpassing 40%.

How is healthcare infrastructure development influencing antibacterial access?

South America contributes about 7% of global demand, with Brazil and Argentina as leading markets. Public hospital expansion programs have increased antibiotic procurement volumes by 12% in recent years. Regional trade policies encourage generic drug imports and local formulation partnerships. Pharmaceutical distribution networks are modernizing cold-chain logistics, improving supply reliability by 14%. A Brazilian manufacturer expanded oral solid dosage capacity by 20% to support domestic hospital demand. Consumer patterns reflect growing outpatient treatment adoption, with retail pharmacy channels accounting for nearly 35% of regional antibiotic dispensing.

What modernization initiatives are shaping infection treatment access?

Middle East & Africa represent roughly 6% of global consumption, with UAE and South Africa as primary markets. Healthcare infrastructure investments include over 150 new hospital projects and expanded diagnostic facilities. Regulatory modernization emphasizes quality compliance and import standardization. Digital hospital information systems adoption has risen by 30% in urban centers. Pharmaceutical partnerships are improving regional formulation capacity. A UAE-based distributor invested in automated warehousing, improving distribution efficiency by 18%. Consumer behavior shows increased hospital-based treatment reliance, particularly in urban tertiary care facilities.

China – 23% share in the Fluoroquinolones Market, supported by extensive API manufacturing capacity and large-scale hospital demand.

United States – 18% share in the Fluoroquinolones Market, driven by advanced hospital infrastructure and strong antimicrobial stewardship implementation.

The Fluoroquinolones market exhibits a moderately fragmented competitive structure with more than 120 active pharmaceutical manufacturers globally engaged in API production, formulation development, and finished dosage distribution. The top five companies collectively account for approximately 46% of total global supply, reflecting strong competition among generic producers alongside a limited number of originator and specialty formulation providers. Market positioning centers on cost-efficient large-scale manufacturing, regulatory compliance capabilities, and portfolio breadth across oral, injectable, and ophthalmic formulations.

Strategic initiatives include capacity expansions of 10–20% at major API facilities, aimed at ensuring supply continuity and export readiness. Partnerships between formulation firms and hospital procurement networks are increasing, with over 35% of institutional supply contracts secured through long-term agreements. Product lifecycle strategies emphasize improved bioavailability formulations and preservative-free ophthalmic variants. Continuous manufacturing investments are delivering yield improvements of up to 18%, while solvent recovery technologies reduce waste output by nearly 25%. Competitive differentiation increasingly depends on environmental compliance, where firms targeting regulated markets commit to wastewater residue reductions exceeding 30%. Mergers and portfolio acquisitions have consolidated specialty anti-infective lines, while digital batch monitoring and automated quality assurance systems are reducing deviation rates by 12%, reinforcing reliability as a core competitive factor.

Aurobindo Pharma Ltd.

Viatris Inc.

Cipla Ltd.

Dr. Reddy’s Laboratories Ltd.

Lupin Limited

Zydus Lifesciences Ltd.

Hikma Pharmaceuticals PLC

Glenmark Pharmaceuticals Ltd.

Alkem Laboratories Ltd.

Technological advancement in the Fluoroquinolones market is centered on manufacturing efficiency, formulation science, quality control automation, and environmental compliance. Continuous flow synthesis is increasingly replacing conventional batch processing, delivering yield improvements of 15–20% while reducing solvent consumption by nearly 25%. Automated in-line monitoring systems equipped with real-time impurity detection sensors lower batch deviation rates by approximately 12%, strengthening compliance with stringent pharmacopeial impurity limits. High-performance crystallization technologies enhance API purity levels beyond 99.5%, which is critical for export-grade antibiotic production.

Formulation innovation is improving therapeutic performance and patient adherence. Advanced drug delivery platforms, including modified-release tablets and ophthalmic preservative-free systems, are expanding treatment options. Bioavailability optimization technologies have demonstrated up to 18% improvement in absorption efficiency in oral dosage forms. Sterile injectable production lines now integrate robotic aseptic filling systems that reduce contamination risks by nearly 30% and improve batch consistency.

Digital transformation is reshaping quality and supply chain management. More than 40% of large-scale manufacturers have adopted electronic batch records and AI-assisted process analytics, enabling predictive maintenance and reducing equipment downtime by 16%. Blockchain-based serialization platforms are improving traceability across global distribution networks, with digital track-and-trace systems covering over 50 countries. Environmental technologies such as membrane filtration and advanced effluent treatment plants target antibiotic residue reductions of up to 35% in wastewater discharge. Collectively, these innovations enhance operational resilience, regulatory alignment, and sustainable production standards across the Fluoroquinolones industry.

• In March 2025, Bayer AG announced the acquisition of global ciprofloxacin manufacturing assets and associated distribution rights, strengthening its position in the fluoroquinolone antibiotics market and enhancing global supply capacity for broad-spectrum antibacterial products.

• In December 2024, Teva Pharmaceutical Industries Ltd. entered a strategic collaboration with Sandoz to co-develop and commercialize a broad-spectrum fluoroquinolone generic portfolio across Europe, Asia, and Latin America, aiming to expand access and optimize supply networks.

• In June 2025, Dr. Reddy’s Laboratories launched a new generic levofloxacin tablet in the United States, adding to its antibacterial formulation portfolio and supporting increased outpatient and hospital-based treatment options.

• In March 2024, Amneal Pharmaceuticals received FDA approval for its ANDA to develop a generic version of ciprofloxacin and dexamethasone otic suspension, intended for middle and outer ear bacterial infections, expanding high-value treatment alternatives.

The Fluoroquinolones Market Report provides a comprehensive analysis of the antibiotic class spanning molecule types, therapeutic applications, end-user segments, regional distribution, and technology adoption. It examines key product segments including second-, third-, and fourth-generation fluoroquinolone molecules, with formulation insights covering oral, injectable, and specialty dosage forms. Detailed application analysis encompasses treatment categories such as respiratory, urinary, gastrointestinal, skin and soft tissue, ophthalmic, and other targeted infection therapies. The report further dissects end-user channels including hospitals, specialty clinics, retail pharmacies, and online pharmacies to provide clarity on institutional demand patterns and outpatient dispensing behavior. Geographic segmentation covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering volume- and share-based insights into consumption patterns influenced by healthcare infrastructure, disease burden, digital prescription adoption, and regulatory frameworks. Technological components address manufacturing innovations such as continuous flow synthesis, automated quality monitoring, advanced crystallization processes, and environmental control systems designed to improve yield, reduce waste, and ensure compliance. Additionally, the report profiles competitive strategies including strategic alliances, portfolio expansions, capacity investments, and compliance-driven initiatives. Emerging niches such as combination therapies, pediatric and geriatric formulations, and antimicrobial stewardship tools further broaden the analytical scope, delivering critical intelligence for decision-makers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bayer AG, Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Ltd., Viatris Inc., Cipla Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Limited, Zydus Lifesciences Ltd., Hikma Pharmaceuticals PLC, Glenmark Pharmaceuticals Ltd., Alkem Laboratories Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |