Reports

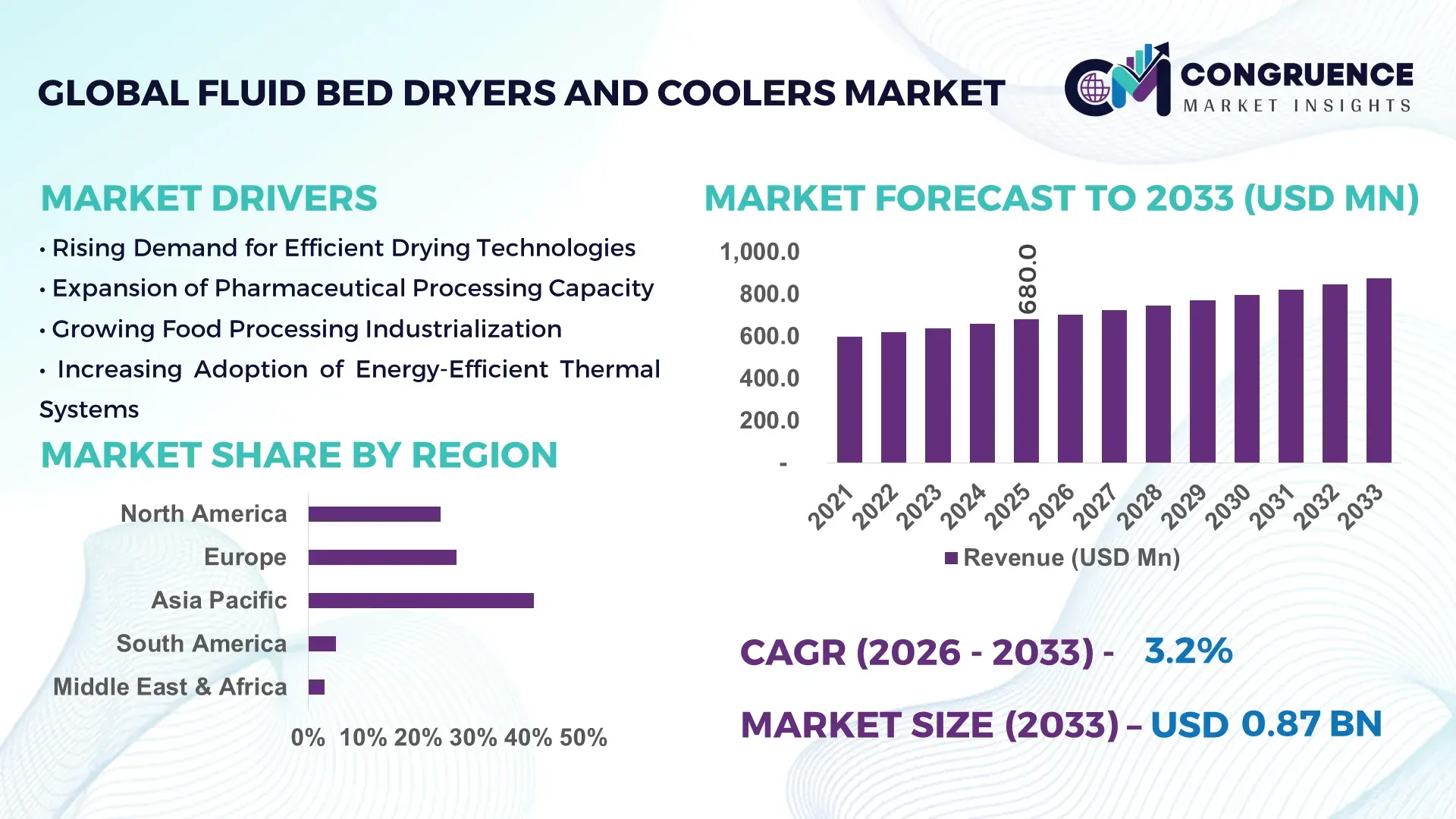

The Global Fluid Bed Dryers and Coolers Market was valued at USD 680 Million in 2025 and is anticipated to reach a value of USD 874.9 Million by 2033 expanding at a CAGR of 3.2% between 2026 and 2033.

The market is accelerating due to rising deployment of continuous processing systems in pharmaceuticals, food processing, and specialty chemicals, where fluid bed technologies improve thermal efficiency by over 22% compared to conventional tray drying systems while reducing processing time by nearly 30%. Between 2024 and 2026, industrial manufacturers are restructuring production lines amid European energy-efficiency mandates, China’s advanced process manufacturing push, and global supply-chain localization trends following Red Sea shipping disruptions and elevated industrial operating costs.

China dominates the global Fluid Bed Dryers and Coolers Market with approximately 31% production concentration, supported by large-scale pharmaceutical API manufacturing, expanding agrochemical processing capacity, and food ingredient exports exceeding 18% growth in 2025. More than 45% of newly installed industrial drying systems across major Chinese process industries now integrate automated airflow and heat-recovery technologies. Compared to North America, China operates nearly 2.4x higher industrial bulk material processing throughput, while Germany continues leading in precision thermal engineering adoption with over 38% of premium closed-loop system installations across Europe.

As industrial operators prioritize energy optimization, continuous processing, and emission-compliant thermal systems, competition is shifting toward automation-enabled, low-energy, high-throughput fluid bed platforms capable of supporting resilient and localized manufacturing ecosystems.

Market Size & Growth: USD 680 Million market in 2025 advancing toward USD 874.9 Million by 2033, driven by 22% higher thermal efficiency from advanced continuous drying systems.

Top Growth Drivers: Pharmaceutical processing demand rose 18%, food ingredient automation increased 21%, and industrial energy-efficiency upgrades expanded 24% globally.

Short-Term Forecast: By 2028, automated fluid bed systems are projected to reduce industrial drying energy consumption by 17% while improving processing throughput by 26%.

Emerging Technologies: AI-enabled airflow control, heat-recovery integration, and IoT-based predictive maintenance improved operational uptime by nearly 28%.

Regional Leaders: Asia-Pacific exceeds USD 320 Million demand, Europe surpasses USD 215 Million, and North America crosses USD 185 Million through advanced process automation adoption.

Consumer/End-User Trends: Nearly 48% of pharmaceutical manufacturers shifted toward continuous processing platforms to improve batch consistency and compliance efficiency.

Pilot/Case Example: In 2025, a German food processing facility achieved 31% lower thermal losses after deploying closed-loop fluid bed cooling systems.

Competitive Landscape: Top five players control nearly 42% market share, led by GEA Group, Glatt, Bühler, Andritz, and Carrier Vibrating Equipment.

Regulatory & ESG Impact: Industrial heat-recovery compliance initiatives reduced process emissions by 19% across high-energy manufacturing facilities in Europe.

Investment & Funding: More than USD 210 Million in industrial process modernization investments targeted automated drying and cooling infrastructure expansion during 2025.

Innovation & Future Outlook: High-capacity modular systems and digital twin monitoring platforms are redefining operational optimization across global process industries.

Pharmaceutical manufacturing contributes nearly 34% of global Fluid Bed Dryers and Coolers demand, followed by food processing at 29% and specialty chemicals at 21%, reflecting strong dependence on precision thermal processing. Automated airflow optimization systems improved drying consistency by 27% in 2025, while closed-loop heat recovery solutions reduced operational energy losses by 18% across advanced industrial facilities. Asia-Pacific continues dominating high-volume deployment, whereas Europe leads premium energy-efficient installations amid tightening industrial emission regulations. Increasing localization of industrial manufacturing and supply-chain diversification are accelerating investments in modular, digitally monitored drying platforms, positioning advanced thermal processing systems as a long-term strategic manufacturing priority.

The Fluid Bed Dryers and Coolers Market is rapidly transforming into a strategic industrial infrastructure segment as manufacturers prioritize energy-efficient continuous processing, production scalability, and process consistency across pharmaceuticals, chemicals, minerals, and food processing industries. Industrial operators are no longer competing only on production output; they are competing on thermal efficiency, processing speed, emission compliance, and operational resilience. This shift is accelerating capital allocation toward advanced fluid bed technologies capable of reducing production downtime while optimizing energy consumption across high-volume manufacturing ecosystems.

Global industrial supply-chain restructuring and tightening environmental regulations are forcing manufacturers to replace legacy batch drying systems with intelligent continuous thermal processing platforms. AI-enabled airflow optimization improves efficiency by 26% while reducing operating costs by nearly 18% compared to conventional static drying technologies. Europe currently leads in sustainability-focused innovation with over 39% adoption of closed-loop energy recovery systems, while Asia-Pacific dominates large-scale deployment volume due to aggressive pharmaceutical and agrochemical manufacturing expansion.

Over the next two to three years, industrial facilities deploying automated fluid bed platforms are expected to improve production throughput by nearly 24% while lowering maintenance interruptions by approximately 20%. ESG positioning is becoming a competitive advantage, particularly in Europe and North America, where energy-efficient thermal systems reduce industrial emissions by up to 19% and strengthen compliance access for export-oriented manufacturers.

A major pharmaceutical processing facility in India reported a 28% reduction in batch cycle time after integrating digitally monitored continuous fluid bed drying technology during a 2025 modernization program. Simultaneously, major equipment manufacturers are shifting investments toward modular systems, predictive maintenance platforms, and regionally localized manufacturing partnerships to secure long-term supply resilience and faster deployment capabilities. As industrial processing industries continue optimizing productivity, compliance, and operational continuity simultaneously, companies capable of integrating automation, energy efficiency, and scalable thermal processing infrastructure will secure a decisive competitive advantage in the next phase of industrial manufacturing transformation.

The Fluid Bed Dryers and Coolers Market is being reshaped by industrial automation, energy-efficiency mandates, and increasing demand for continuous material processing across pharmaceuticals, food ingredients, specialty chemicals, and mineral processing industries. Manufacturers are aggressively replacing conventional tray and rotary drying systems with fluidized thermal technologies that improve heat transfer efficiency, reduce processing time, and optimize production consistency. More than 46% of newly commissioned pharmaceutical production lines in 2025 integrated continuous processing systems, directly increasing demand for advanced fluid bed equipment. Operational efficiency pressures are intensifying across global industrial sectors due to rising energy prices, emission-reduction targets, and labor optimization requirements. Europe and North America are prioritizing closed-loop thermal systems and automated process monitoring, while Asia-Pacific continues expanding high-volume production infrastructure supported by lower manufacturing costs and localized equipment production. Simultaneously, supply-chain diversification strategies following geopolitical shipping disruptions are accelerating regional manufacturing investments. The market is also witnessing growing competition around smart automation, predictive maintenance integration, and modular system scalability, forcing manufacturers to balance cost competitiveness with technology differentiation and sustainability compliance.

The transition toward continuous industrial manufacturing is becoming the strongest structural growth engine for the Fluid Bed Dryers and Coolers Market. Pharmaceutical manufacturers increased continuous production integration by nearly 32% between 2024 and 2026 to improve batch consistency, reduce contamination risks, and accelerate production cycles. Advanced fluid bed systems are reducing drying time by approximately 28% while improving thermal utilization efficiency by over 22% compared to legacy batch-based systems. Global supply-chain restructuring and rising energy costs following Red Sea logistics disruptions forced manufacturers to localize production and optimize energy-intensive operations. As a result, food processing and specialty chemical producers accelerated deployment of automated thermal processing systems capable of reducing energy waste by nearly 18%. Industrial operators are responding through capacity expansion, automation investments, and strategic partnerships with equipment providers focused on predictive maintenance and intelligent airflow management. This demand shift is redefining competitive positioning. Companies investing in scalable modular systems and digital process monitoring are strengthening production resilience, improving operational continuity, and securing long-term cost advantages across highly regulated manufacturing environments.

Despite strong industrial adoption momentum, high installation costs and operational complexity remain major structural restraints in the Fluid Bed Dryers and Coolers Market. Advanced closed-loop systems require approximately 25% higher upfront capital investment compared to conventional thermal processing technologies, creating barriers for mid-sized manufacturers operating under limited modernization budgets. Additionally, integration of automated airflow controls and heat-recovery infrastructure increases commissioning complexity and extends deployment timelines by nearly 15%. Global volatility in stainless steel and industrial component pricing between 2024 and 2025 further intensified equipment manufacturing costs, while semiconductor shortages affected smart sensor availability for digitally controlled systems. Smaller processing facilities in South America and parts of Southeast Asia continue facing infrastructure limitations and limited access to skilled thermal processing engineers. Manufacturers are mitigating these risks through long-term supplier agreements, localized component sourcing, and hybrid retrofitting strategies that allow older systems to integrate selective automation features. Several equipment providers are also expanding modular product offerings to reduce installation complexity and improve deployment flexibility. However, companies unable to control operating costs and implementation timelines risk losing competitiveness as industrial buyers increasingly prioritize operational efficiency and rapid scalability.

The emergence of digitally integrated thermal processing platforms is opening significant high-impact opportunities across pharmaceuticals, nutraceuticals, battery materials, and specialty food processing industries. AI-driven process optimization systems improved operational throughput by approximately 24% in pilot installations during 2025, while predictive maintenance integration reduced unplanned downtime by nearly 21%. One major future signal is the rapid shift toward energy-recovery-enabled fluid bed technologies capable of lowering industrial heat losses by over 19%. This is becoming strategically critical as global manufacturers face tightening carbon reduction targets and rising industrial electricity costs. Simultaneously, demand for customized modular drying systems increased by 27% across emerging industrial hubs in India, Vietnam, and Mexico due to localized manufacturing expansion. Companies are aggressively positioning for long-term dominance through R&D investment, digital ecosystem integration, and regional manufacturing expansion. Equipment providers are partnering with industrial automation firms to deliver fully connected processing environments supporting remote monitoring and real-time optimization. The strongest upside lies not only in equipment sales but also in lifecycle service contracts, software integration, and energy-efficiency optimization platforms that create recurring industrial value streams.

Execution complexity and scalability limitations remain major challenges across the Fluid Bed Dryers and Coolers Market, particularly for industries requiring highly customized thermal processing conditions. Nearly 29% of industrial operators reported difficulties maintaining consistent airflow distribution and moisture control during large-scale continuous production operations. In high-volume pharmaceutical and food ingredient manufacturing, even minor process inconsistencies can reduce production efficiency by over 14%. Rising industrial electricity costs across Europe and parts of Asia continue pressuring thermal processing economics, while infrastructure constraints in emerging markets limit deployment of high-capacity automated systems. Simultaneously, stricter emission compliance regulations are forcing manufacturers to upgrade legacy equipment faster than some facilities can operationally absorb. To remain competitive, companies must solve system interoperability challenges, reduce maintenance complexity, and improve scalability for multi-product manufacturing environments. Major equipment providers are increasing investments in intelligent diagnostics, adaptive airflow technologies, and energy-recovery engineering partnerships to stabilize long-term operational performance. Firms capable of delivering scalable, low-energy, digitally optimized thermal processing ecosystems will define the next phase of sustainable industrial manufacturing leadership.

31% Rise in AI-Controlled Thermal Optimization Reshaping Industrial Drying Operations: Industrial manufacturers are rapidly deploying AI-enabled airflow and temperature management systems across pharmaceutical and food processing plants. Automated thermal optimization reduced drying inconsistencies by 26% while improving throughput efficiency by 22% during 2025 deployments. Companies are integrating predictive maintenance platforms to minimize downtime as labor shortages and energy-efficiency pressures continue reshaping industrial operations.

24% Expansion in Modular System Deployment Accelerating Localized Manufacturing Strategies: Manufacturers are shifting toward modular fluid bed systems capable of faster installation and flexible production scaling. Deployment timelines declined by nearly 18%, while localized production integration improved supply continuity across Asia-Pacific and North America. Companies are restructuring supply networks and expanding regional assembly operations to reduce exposure to shipping disruptions and industrial component shortages.

19% Increase in Closed-Loop Heat Recovery Adoption Redefining Energy Management: Industrial facilities are aggressively implementing closed-loop heat recovery systems to reduce thermal energy waste and comply with tightening emission regulations. Advanced systems lowered industrial heat losses by approximately 21% while improving operating efficiency by 17%. Equipment suppliers are prioritizing sustainability-focused retrofitting services as energy-intensive industries face growing compliance and operating cost pressures.

27% Growth in Continuous Pharmaceutical Processing Forcing Equipment Redesigns: Pharmaceutical manufacturers are accelerating continuous production adoption to improve batch consistency and reduce contamination risks. High-capacity fluid bed systems improved processing cycle speed by nearly 25% while supporting stricter regulatory compliance standards. Equipment providers are redesigning platforms for multi-product flexibility and digital process monitoring to capture rapidly expanding high-purity manufacturing demand.

The Fluid Bed Dryers and Coolers Market is segmented by type, application, and end-user industries, with demand strongly concentrated in high-volume industrial processing environments requiring efficient thermal management and continuous material handling. Continuous fluid bed systems account for nearly 58% of total deployment due to superior scalability, lower energy consumption, and faster processing performance compared to batch-based alternatives. Demand is increasingly shifting toward automated and closed-loop systems as industrial manufacturers prioritize operational efficiency, emission control, and production consistency.

Pharmaceutical and food processing applications collectively contribute over 63% of global demand, driven by stringent moisture-control requirements, hygiene compliance, and increasing production automation. Meanwhile, specialty chemicals and mineral processing industries are accelerating adoption of modular high-capacity systems to optimize throughput and reduce operational downtime. End-user strategies are also evolving, with large industrial manufacturers increasingly favoring digitally integrated thermal systems that support predictive maintenance, remote monitoring, and energy recovery. This segmentation trend highlights a broader transition toward intelligent, scalable, and sustainability-focused industrial processing infrastructure.

Continuous fluid bed dryers and coolers dominate the market with approximately 58% share due to their superior operational scalability, uninterrupted material processing capability, and nearly 24% lower energy consumption compared to conventional batch systems. These systems are heavily deployed across pharmaceutical APIs, food ingredients, and specialty chemicals where production continuity and process consistency are strategically critical. Manufacturers are prioritizing continuous platforms because they reduce cycle interruptions and improve throughput efficiency by over 26%. Batch fluid bed systems remain widely utilized in smaller-volume and highly customized production environments, particularly within specialty pharmaceutical and laboratory-scale applications. However, vibrating fluid bed systems are emerging as the fastest-growing segment, expanding adoption by nearly 19% due to enhanced material handling precision, improved cooling uniformity, and reduced product degradation risks during high-speed processing. Remaining specialized configurations, including static and hybrid fluidized systems, collectively account for approximately 23% of market demand, serving niche applications in minerals, agrochemicals, and heat-sensitive materials. Companies are responding to shifting demand by investing in modular continuous systems, automation-enabled airflow controls, and high-capacity vibrating platforms capable of supporting multi-product industrial environments. The strongest investment opportunities are concentrating around scalable, energy-efficient, digitally optimized system architectures.

• According to a 2025 report by the International Society for Pharmaceutical Engineering (ISPE), continuous fluid bed processing systems were adopted by over 52% of large pharmaceutical manufacturing facilities, resulting in nearly 27% improvement in batch consistency and thermal efficiency, reinforcing their growing strategic importance.

Pharmaceutical processing leads the Fluid Bed Dryers and Coolers Market with nearly 34% demand concentration due to strict moisture control requirements, contamination prevention standards, and rapid expansion of continuous manufacturing infrastructure. Large-scale API production facilities increasingly rely on advanced fluid bed systems to improve drying consistency, reduce production variability, and strengthen regulatory compliance across global supply chains. Food processing represents the fastest-growing application segment, expanding adoption by approximately 21% as manufacturers prioritize high-throughput ingredient drying, instant food production, and energy-efficient thermal processing. Compared to conventional rotary systems, fluid bed technologies improve product uniformity while reducing thermal degradation risks in sensitive food materials. Specialty chemicals and agrochemical applications collectively account for around 29% of total deployment, particularly in large-volume powder handling and granular material processing operations. Industrial usage patterns are shifting toward automated and closed-loop systems capable of supporting multi-product operations with lower operational downtime. Companies are increasingly deploying digitally monitored platforms to optimize production quality and reduce energy losses. As operational efficiency and sustainability targets intensify globally, investment is rapidly concentrating around high-capacity pharmaceutical and food-grade thermal processing systems that combine precision control with scalable industrial throughput.

• According to a 2025 report by the Food Processing Suppliers Association (FPSA), advanced fluid bed drying systems were deployed across more than 3,800 industrial food processing facilities, improving production efficiency by 24% and reducing product moisture variability by 19%, highlighting rapid operational adoption.

Large pharmaceutical manufacturers dominate end-user demand with approximately 36% market share due to heavy dependence on precision thermal processing, contamination-controlled production environments, and continuous manufacturing integration. These facilities operate high-volume production lines requiring stable airflow management, rapid moisture reduction, and automated process monitoring to maintain regulatory compliance and operational consistency. Food and beverage producers are emerging as the fastest-growing end-user segment, with adoption increasing by nearly 22% as companies accelerate automation and energy-efficiency upgrades across ingredient processing facilities. Compared to smaller processors, multinational food manufacturers are prioritizing modular high-throughput systems capable of reducing production interruptions while supporting flexible product portfolios. Chemical and specialty material manufacturers collectively contribute approximately 31% of global deployment, particularly in high-temperature powder and granular processing applications. Buying behavior is shifting toward integrated solutions combining predictive maintenance, energy recovery, and digital process analytics. Equipment manufacturers are responding through customized engineering partnerships, lifecycle service contracts, and scalable automation-focused product offerings. Future demand is increasingly concentrating around end-users capable of balancing production speed, sustainability compliance, and operational resilience, making digitally optimized thermal infrastructure a major competitive differentiator.

• According to a 2025 report by the International Federation of Pharmaceutical Manufacturers & Associations (IFPMA), adoption among pharmaceutical production facilities increased by 29%, with over 4,200 organizations implementing continuous thermal processing systems, leading to nearly 23% improvement in production efficiency and quality consistency, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 3.8% between 2026 and 2033.

Asia-Pacific dominates global demand due to large-scale pharmaceutical production, food ingredient manufacturing expansion, and lower-cost industrial processing infrastructure across China, India, and Southeast Asia. Europe holds approximately 27% share, driven by energy-efficiency regulations and strong adoption of closed-loop thermal systems in Germany and France. North America contributes nearly 24% demand concentration and leads automation integration, with over 46% of newly installed systems incorporating predictive maintenance and AI-enabled thermal monitoring technologies. Meanwhile, South America and the Middle East & Africa collectively account for 8% share, supported by expanding food processing, mining, and agrochemical sectors. Global supply-chain localization strategies and industrial energy optimization initiatives are increasingly shifting investment toward regional manufacturing expansion, modular deployment capabilities, and digitally integrated processing systems across high-growth industrial hubs.

North America accounts for nearly 24% of the global Fluid Bed Dryers and Coolers Market, supported by strong pharmaceutical manufacturing, processed food production, and specialty chemical processing demand across the United States and Canada. More than 46% of newly installed industrial drying systems now integrate predictive maintenance and AI-based thermal monitoring platforms to improve operational reliability and reduce maintenance interruptions by approximately 18%. Rising industrial energy costs and stricter emission compliance requirements are accelerating adoption of closed-loop and heat-recovery-enabled systems. Major manufacturers expanded modular processing capacity by nearly 21% during 2025 to support reshoring initiatives and supply-chain resilience strategies. Enterprise buyers increasingly prioritize automation-enabled, low-downtime systems capable of supporting multi-product operations with high process consistency. Companies are aggressively investing in this region because North America combines premium technology adoption, operational modernization, and high-margin industrial processing demand.

Europe contributes approximately 27% of global Fluid Bed Dryers and Coolers demand, led by Germany, France, and Italy where pharmaceutical, nutraceutical, and food processing industries are aggressively upgrading thermal infrastructure. Industrial emission-reduction mandates and EU energy-efficiency directives accelerated adoption of heat-recovery-enabled fluid bed systems by nearly 23% between 2024 and 2026. More than 38% of premium industrial thermal systems installed across Europe now integrate closed-loop airflow control and digital energy optimization platforms. Manufacturers are prioritizing low-emission, compliance-focused processing systems to reduce industrial heat losses and strengthen export competitiveness. European enterprise buyers remain strongly quality-focused and compliance-driven, favoring precision-engineered systems with advanced process monitoring capabilities. This region is forcing global equipment providers to innovate faster around energy optimization, sustainability compliance, and intelligent thermal processing efficiency.

Asia-Pacific leads the global Fluid Bed Dryers and Coolers Market with approximately 41% demand concentration, driven by large-scale pharmaceutical, agrochemical, and food ingredient manufacturing across China, India, Japan, and Southeast Asia. China alone accounts for nearly 31% of global production capacity, supported by aggressive industrial automation and expanding export-oriented processing infrastructure. Localized equipment manufacturing and lower production costs improved regional deployment speed by approximately 26% during 2025. Industrial operators are rapidly integrating automated airflow systems and modular thermal platforms to support high-volume continuous manufacturing operations. More than 45% of new pharmaceutical processing facilities in the region now deploy digitally monitored drying technologies to optimize throughput and quality consistency. Enterprise buyers prioritize scalability, cost efficiency, and rapid deployment over premium customization, forcing equipment suppliers to expand localized manufacturing partnerships and regional assembly operations. Asia-Pacific remains strategically critical because it combines unmatched production scale, accelerating industrial demand, and expanding global supply-chain influence.

South America represents nearly 5% of the global Fluid Bed Dryers and Coolers Market, led by Brazil and Argentina where food processing, mining, and agrochemical industries continue expanding thermal processing investments. Rising packaged food production and fertilizer processing demand increased industrial drying system deployment by approximately 14% during 2025. However, infrastructure limitations, import dependency, and currency volatility continue constraining large-scale modernization projects across several industrial sectors. Regional manufacturers are increasingly adopting mid-capacity modular systems that reduce upfront investment requirements while improving operational flexibility. Nearly 29% of industrial buyers now prioritize energy-efficient retrofitting solutions instead of full-system replacement strategies. Enterprise purchasing behavior remains highly price-sensitive, with strong preference for localized service support and lower-maintenance system configurations. The region presents attractive expansion opportunities for companies capable of balancing affordability, operational efficiency, and flexible deployment models within economically volatile industrial environments.

The Middle East & Africa account for approximately 3% of global Fluid Bed Dryers and Coolers demand, supported by expanding petrochemical, food processing, and mineral handling industries across Saudi Arabia, UAE, and South Africa. Industrial diversification initiatives and infrastructure modernization programs increased advanced thermal processing equipment deployment by nearly 16% during 2025. Governments and industrial operators are accelerating investments in automated production facilities and energy-efficient processing technologies to strengthen regional manufacturing capabilities. More than 22% of newly commissioned industrial processing projects integrated digitally monitored thermal systems to improve operational consistency and reduce maintenance interruptions. Enterprise buyers increasingly prioritize durable, low-maintenance systems capable of operating efficiently in high-temperature industrial environments. Strategic partnerships between international equipment suppliers and regional industrial groups are expanding localized deployment capabilities. This region is emerging as a long-term strategic market because industrial modernization and resource-processing expansion continue reshaping manufacturing priorities.

China – 31% market share: Leads due to massive pharmaceutical API production, food ingredient manufacturing scale, and localized industrial equipment capacity expansion.

United States – 18% market share: Dominates through advanced pharmaceutical processing infrastructure, high automation adoption, and strong investment in energy-efficient industrial thermal systems.

The Fluid Bed Dryers and Coolers Market is characterized by intense competition between global engineering leaders, automation-focused thermal processing specialists, and cost-competitive regional manufacturers. Major players including GEA Group, Glatt, Bühler, Andritz, and Carrier Vibrating Equipment collectively control approximately 42% of global market positioning through advanced engineering capabilities, global supply networks, and integrated process automation solutions.

Competition is increasingly centered around thermal efficiency, digital monitoring integration, modular scalability, and lifecycle operational cost reduction. Premium European manufacturers compete aggressively on energy optimization and compliance-focused engineering, while Asian manufacturers are strengthening position through lower-cost localized production and faster deployment cycles. Automated systems integrating predictive maintenance improved operational uptime by nearly 28%, forcing competitors to accelerate digital platform development and industrial software partnerships.

Companies are actively expanding regional assembly operations, pursuing strategic automation alliances, and investing in high-capacity modular system innovation to secure supply-chain resilience. Market consolidation pressure is increasing as industrial buyers prioritize full-service ecosystem providers capable of offering engineering customization, maintenance support, and long-term process optimization. Winning in this market now requires combining engineering precision, energy-efficiency leadership, scalable deployment capability, and integrated digital thermal processing intelligence.

Glatt GmbH

Bühler Group

Andritz AG

Carrier Vibrating Equipment Inc.

Ventilex BV

Thyssenkrupp Industrial Solutions

SPX FLOW Inc.

Tema Process BV

FLSmidth & Co. A/S

AVM Process Systems

Siddhi Vinayak Engineering

Shandong Tianli Energy Co., Ltd.

Syntegon Technology GmbH

Advanced automation and thermal optimization technologies are rapidly reshaping the Fluid Bed Dryers and Coolers Market. AI-enabled airflow control systems and IoT-integrated monitoring platforms are improving thermal consistency by nearly 26% while reducing unplanned maintenance downtime by approximately 21%. More than 44% of newly commissioned pharmaceutical processing facilities now integrate digitally monitored fluid bed systems capable of real-time process adjustment and predictive diagnostics. These technologies are becoming essential for maintaining production stability in high-volume industrial environments.

Closed-loop heat recovery systems are emerging as one of the most disruptive technologies across industrial thermal processing. Compared to conventional open-cycle systems, modern energy-recovery-enabled platforms reduce thermal energy losses by nearly 19% while lowering operating costs by approximately 17%. European manufacturers are aggressively deploying these systems to comply with tightening industrial emission standards, while North American operators are prioritizing them to optimize energy-intensive production operations.

Another major transformation involves modular and vibrating fluid bed technologies designed for flexible multi-product manufacturing. Compared to legacy static systems, modular platforms improve installation speed by nearly 23% and enhance operational scalability across pharmaceuticals, nutraceuticals, and specialty chemicals. Equipment providers with strong automation integration capabilities are securing competitive advantage as industrial buyers increasingly prioritize flexible, digitally connected production ecosystems.

Between 2026 and 2028, digital twin simulation platforms, adaptive airflow engineering, and smart thermal analytics are expected to redefine industrial process optimization. Companies acting early on automation, energy recovery, and predictive intelligence integration will strengthen operational resilience, reduce lifecycle costs, and capture premium industrial processing demand globally.

May 2026 – GEA Group introduced the meVap® technology platform focused on decarbonizing thermal processing industries through mechanical vapor recompression systems, significantly reducing industrial CO₂ emissions and operating costs across pharmaceutical and chemical processing applications. The launch strengthens GEA’s energy-transition positioning in advanced thermal processing markets. [Decarbonization Platform] Source: www.gea.com

March 2026 – GEA Group reported 9.1% organic order intake growth and confirmed accelerated expansion across its Pharma & Food Applications division, reflecting strong global demand for advanced industrial processing and thermal optimization systems. The company also achieved climate targets ahead of schedule, reinforcing its sustainability-led industrial strategy. [Climate Growth Acceleration]

September 2025 – Glatt GmbH expanded its fluid bed technology center capabilities with advanced solvent-based processing systems designed for GMP-compliant pharmaceutical and food applications. The upgraded infrastructure increased production capacity into the three-digit tonne range while supporting safer explosion-protected operations and enhanced bioavailability-focused processing. [Advanced GMP Expansion]

October 2025 – GEA Group accelerated organizational restructuring and operational streamlining initiatives ahead of 2026, strengthening focus on process technologies for food, pharmaceutical, and industrial applications. The strategic restructuring supports faster execution, higher-margin processing solutions, and long-term industrial automation expansion across global markets. [Strategic Restructuring Move]

The Fluid Bed Dryers and Coolers Market Report delivers comprehensive coverage of industrial thermal processing technologies, market segmentation structures, competitive positioning, and regional deployment dynamics across pharmaceuticals, food processing, chemicals, minerals, and specialty manufacturing industries. The report evaluates major system categories including continuous, batch, modular, and vibrating fluid bed technologies while assessing application-level demand distribution and end-user operational priorities. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with detailed country-level strategic insights.

The study analyzes more than 20 market variables including production concentration, automation adoption, energy-efficiency deployment, and industrial modernization trends. Over 44% of newly deployed industrial systems now integrate digital monitoring capabilities, while approximately 39% of premium installations include closed-loop energy recovery technologies. The report also examines emerging trends such as predictive maintenance, AI-enabled thermal optimization, modular scalability, and continuous pharmaceutical manufacturing integration.

Strategically, the report supports investment planning, technology benchmarking, competitive positioning, and regional expansion decision-making between 2026 and 2033. It highlights high-opportunity deployment environments, evolving buyer preferences, and emerging operational efficiency priorities shaping future industrial processing infrastructure. Decision-makers gain actionable intelligence around technology adoption shifts, demand concentration, and competitive transformation critical for long-term market positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 680 Million |

| Market Revenue (2033) | USD 874.9 Million |

| CAGR (2026–2033) | 3.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | GEA Group; Glatt GmbH; Bühler Group; Andritz AG; Carrier Vibrating Equipment Inc.; Ventilex BV; Thyssenkrupp Industrial Solutions; SPX FLOW Inc.; Tema Process BV; FLSmidth & Co. A/S; AVM Process Systems; Siddhi Vinayak Engineering; Shandong Tianli Energy Co., Ltd.; Syntegon Technology GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |