Reports

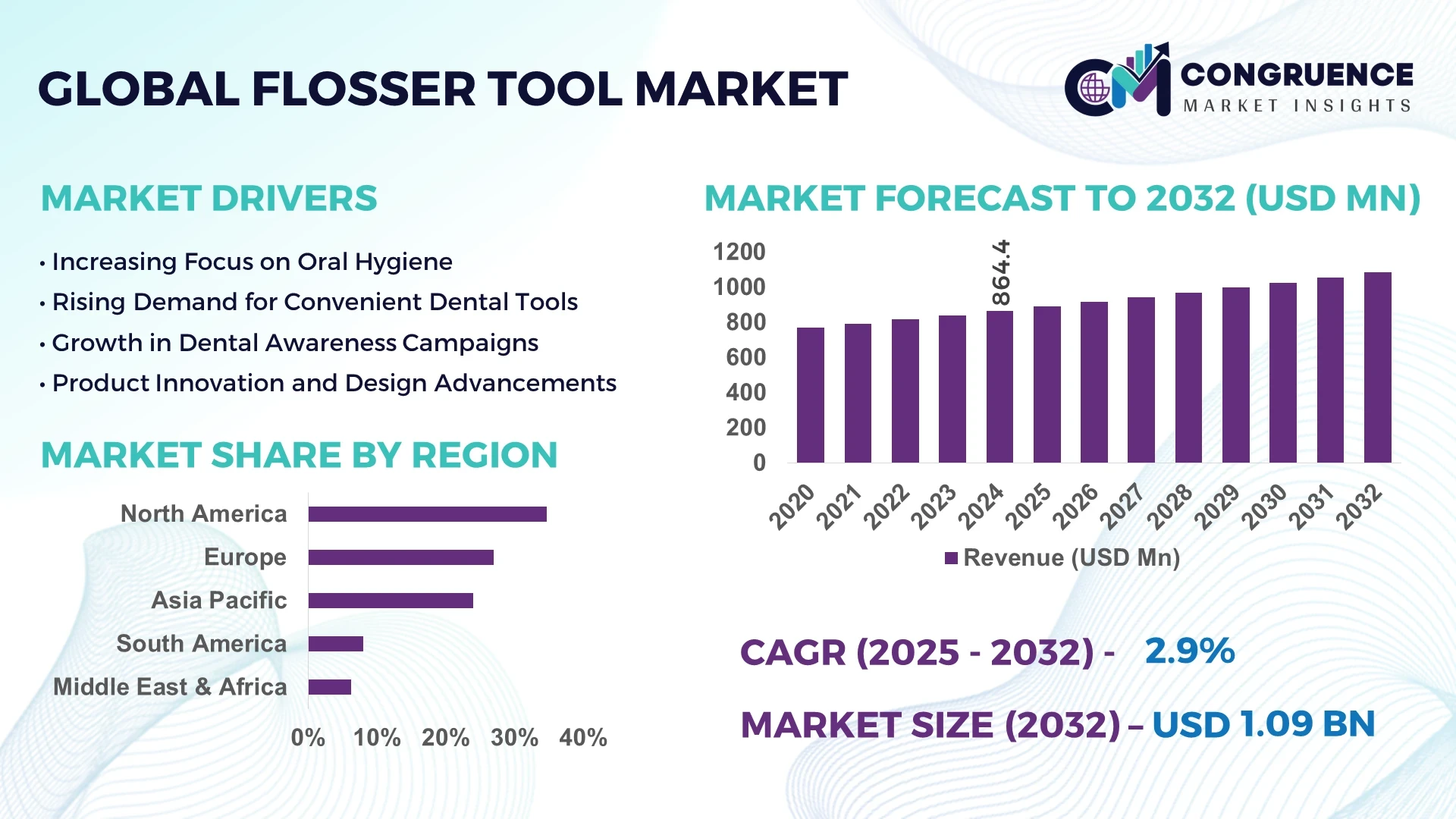

The Global Flosser Tool Market was valued at USD 864.4 Million in 2024 and is anticipated to reach a value of USD 1086.5 Million by 2032, expanding at a CAGR of 2.9% between 2025 and 2032.

North America, particularly the United States, dominates the global Flosser Tool Market. In 2023, the North American market was valued at approximately USD 250 million, with the United States accounting for the majority share. The high adoption of advanced technology and the presence of major industry players contribute significantly to this dominance.

The Flosser Tool Market is segmented by type into F Shape and Y Shape, and by application into Household and Hospital & Dental Clinic. The Household segment held the largest market share in 2024, driven by increasing consumer awareness about dental hygiene and the convenience of at-home oral care solutions.

Artificial Intelligence (AI) is playing a pivotal role in transforming the Flosser Tool Market by enhancing product functionalities and user experiences. AI-driven features such as real-time feedback, personalized care, and smart flossing solutions are becoming increasingly prevalent. These innovations cater to individual user needs more effectively, thereby improving oral hygiene outcomes.

The integration of AI and automation technologies is also streamlining manufacturing processes, reducing production costs, and enhancing overall product reliability. AI algorithms optimize the design and functionality of flossing tools, allowing for improved performance and adaptability to different dental conditions. With growing consumer interest in smart health devices, manufacturers are investing in AI-enabled flossers that can sync with mobile apps to track user habits and suggest improvements. This trend is leading to increased consumer engagement and better oral health compliance.

“In 2024, a leading oral care company introduced an AI-powered flosser that utilizes machine learning algorithms to adapt to users' flossing habits, providing personalized recommendations and improving overall dental health outcomes.”

The growing consumer preference for oral care products equipped with advanced comfort and safety features is a significant driver of the Flosser Tool Market. Manufacturers are responding by developing flossers with ergonomic designs, adjustable pressure settings, and smart features that reduce user effort and enhance the flossing experience. Additionally, the incorporation of safety features such as pressure sensors and automatic shut-off mechanisms is becoming standard, driven by stringent safety regulations and consumer awareness. This trend is particularly prominent in the premium and luxury segments, where consumers are willing to invest in superior oral care experiences.

The presence of substitute products such as wax flossers, non-wax tapes, and traditional dental floss poses a significant restraint to the Flosser Tool Market. These alternatives often come at a lower cost and are widely available, making them accessible to a broader consumer base. Additionally, some consumers may prefer traditional flossing methods due to familiarity or skepticism towards newer technologies. This preference can hinder the adoption of advanced flosser tools, particularly in price-sensitive markets.

The increasing consumer demand for personalized oral care solutions presents a significant opportunity for the Flosser Tool Market. Advancements in technology enable the development of flossers that cater to individual dental needs, such as adjustable pressure settings, interchangeable tips, and smart features that track and analyze flossing habits. These personalized solutions enhance user engagement and satisfaction, leading to increased adoption rates. Furthermore, the integration of AI and machine learning can provide users with real-time feedback and tailored recommendations, further personalizing the oral care experience.

The development and integration of advanced technologies in flosser tools lead to increased production costs, which are often passed on to consumers in the form of higher prices. This price increase can be a barrier to adoption, especially in developing regions where consumers may be more price-sensitive. Additionally, the need for regular maintenance and replacement parts for advanced flossers can add to the overall cost of ownership, potentially deterring long-term use. Manufacturers must find a balance between incorporating innovative features and maintaining affordability to ensure widespread adoption.

Rise in Portable and Rechargeable Devices: The market is witnessing a surge in demand for portable and rechargeable flosser tools. Consumers prefer devices that offer convenience and ease of use, especially those with USB charging options and compact designs suitable for travel. This trend is driven by the increasing need for on-the-go oral care solutions.

Integration of Smart Features: Modern flosser tools are increasingly incorporating smart features such as Bluetooth connectivity, app-based tracking, and real-time feedback. These innovations enhance user engagement and allow for personalized oral care routines, aligning with the growing consumer interest in health and wellness technology.

Emphasis on Sustainable and Eco-friendly Designs: Manufacturers are focusing on developing flosser tools with eco-friendly materials and water-saving modes. This shift caters to the environmentally conscious consumer base and aligns with global sustainability goals. Products with recyclable components and biodegradable packaging are also gaining traction.

Expansion in Emerging Markets: The Flosser Tool Market is expanding rapidly in emerging economies, particularly in the Asia-Pacific region. Factors such as increasing disposable incomes, growing awareness about oral health, and the rising prevalence of dental issues contribute to this growth. Urbanization and improvements in healthcare infrastructure are further accelerating market penetration.

The Flosser Tool Market is segmented based on type, application, and end-user insights. Each of these segments plays a critical role in shaping the market landscape and determining the direction of growth. By understanding these segments in detail, businesses can tailor their strategies to target high-growth areas. The market has shown notable diversification across different product types and user applications, with rapid advancements driven by both technological innovation and consumer demand. The segmentation analysis helps identify which product forms and user categories are leading in adoption and where future expansion is most likely to occur.

The Flosser Tool Market is primarily divided into two major types: F-Shape and Y-Shape flossers. Among these, the F-Shape segment accounted for the largest market share in 2024, contributing over 55% of the global volume. This dominance is attributed to the widespread preference for the ergonomic and user-friendly design of F-Shape flossers, especially for individuals with limited dexterity or for children. They are easier to handle, offer better grip, and provide a precise cleaning experience, making them more appealing to households.

However, the Y-Shape segment is the fastest-growing type and is expected to exhibit the highest growth rate through 2032. The increased adoption is largely driven by professional and clinical use, as the Y-Shape design enables access to difficult-to-reach interdental areas. This type is also gaining popularity among users with braces or other dental devices due to its angled design. The continuous improvement in Y-Shape design, combined with better material quality and comfort, is contributing to its accelerating demand.

The Flosser Tool Market is segmented into two main application areas: Household and Hospital & Dental Clinic. The Household segment leads the market, accounting for nearly 65% of total usage in 2024. This is primarily due to rising consumer awareness regarding preventive dental care and the convenience offered by at-home oral hygiene solutions. Increasing disposable income, along with the growing trend of investing in personal wellness, has significantly boosted sales in this category.

On the other hand, the Hospital & Dental Clinic segment is emerging as the fastest-growing application area. Clinics and dental professionals are increasingly adopting advanced flosser tools for pre-treatment cleaning, patient demonstrations, and post-operative care. The demand for high-precision and effective flossing solutions in clinical settings is pushing innovation in this segment. Moreover, professional endorsement of specific products often influences consumer preferences in the household segment, creating a positive feedback loop for market growth.

End-users in the Flosser Tool Market are broadly categorized into Adults, Children, and Geriatric Populations. The Adult segment dominated the market in 2024, comprising over 60% of the total user base. This dominance stems from the higher purchasing power, greater awareness of oral hygiene, and lifestyle trends among adults. Adults are also more likely to adopt technologically advanced products such as smart flossers that offer app integration and real-time feedback.

The fastest-growing end-user segment is the Geriatric population. With a rising global aging demographic and increased prevalence of dental conditions such as gum disease, tooth sensitivity, and dental implants, elderly consumers are seeking effective and gentle flossing solutions. Flosser tools with pressure control, ergonomic handles, and soft bristles are gaining traction among this group. Meanwhile, the Children segment also shows healthy growth due to increasing parental focus on pediatric oral care and the availability of colorful, fun, and safe flosser designs specifically tailored to younger users.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

The North American market’s dominance is largely driven by advanced oral care infrastructure, high consumer spending, and the presence of leading market players. Meanwhile, Asia-Pacific’s rapid growth can be attributed to rising awareness about dental hygiene, increasing disposable incomes, and significant expansion of retail and online sales channels in countries like China and India. Additionally, government initiatives and improved healthcare access are contributing to higher adoption of flosser tools across urban and semi-urban areas.

Surging Adoption of Smart Oral Care Devices

North America continues to lead in adopting smart oral care technologies, with over 38 million households using electronic flossers in 2024. The U.S. alone represented approximately USD 210 million in market value, driven by consumer inclination towards convenience, hygiene awareness, and integration of AI-enabled oral health devices. Technological advancements such as Bluetooth-enabled flossers and app-based performance tracking are gaining popularity, especially among millennials and tech-savvy consumers. Retailers are offering product bundles and subscription-based refills, further boosting long-term usage and customer retention.

Increasing Focus on Preventive Dental Care

In 2024, Europe accounted for 27.3% of the global flosser tool market, with Germany, the UK, and France contributing the highest shares. The region has seen increased demand for preventive dental care tools, driven by a strong emphasis on oral hygiene education and dental insurance coverage that encourages routine home care. Over 45% of adults in Western Europe now report using oral irrigators or electric flossers. Eco-friendly and sustainable flosser products, such as biodegradable floss heads and refillable cartridges, are gaining traction, particularly in Nordic countries. The trend toward minimalist and ergonomic designs also influences purchasing behavior.

Expanding Middle-Class Driving Market Penetration

Asia-Pacific held 22.8% of the global flosser tool market in 2024 but is projected to experience the fastest expansion by 2032. China and India are leading the charge with increasing consumer awareness and growing health consciousness. China alone contributed over USD 85 million in sales, while India saw a 12% year-over-year increase in electric flosser adoption. The growing middle class, urbanization, and e-commerce boom are crucial factors boosting market penetration. In addition, local manufacturers are entering the market with cost-effective, feature-rich products, making flossers more accessible to a wider audience.

Steady Growth Amid Rising Oral Health Campaigns

South America contributed 6.2% to the global market in 2024, with Brazil holding the largest share in the region at USD 35 million. The region is experiencing steady growth due to increased government-backed oral health awareness campaigns and a growing young population seeking preventive care solutions. Despite economic challenges, urban centers in countries like Argentina and Chile are witnessing rising demand for affordable flosser tools. Market penetration is being supported by the expansion of e-commerce platforms and supermarket chains offering imported and domestic oral care brands.

Low Penetration with Emerging Growth Opportunities

Middle East & Africa held 4.5% of the global market share in 2024. The United Arab Emirates and South Africa led the region, collectively accounting for USD 28 million. These markets are benefiting from rising dental tourism, greater healthcare spending, and higher exposure to international product standards. While penetration remains low compared to other regions, the growing availability of flosser tools in urban pharmacies and online marketplaces presents strong potential. Increasing oral health awareness campaigns and collaborations with dental clinics are expected to boost future adoption rates, especially in Gulf Cooperation Council (GCC) countries.

United States – USD 210 Million

Strong consumer spending, advanced healthcare infrastructure, and early technology adoption drive the U.S. market leadership.

China – USD 85 Million

Rapid urbanization, increased health awareness, and a growing middle-class population fuel demand in China.

The global Flosser Tool Market is characterized by a dynamic and competitive landscape, featuring a mix of established multinational corporations and emerging regional players. In 2024, the top five companies collectively accounted for approximately 42% of the global market share, reflecting a moderately consolidated market structure. Leading companies are investing heavily in research and development to introduce innovative products that cater to evolving consumer preferences, such as eco-friendly materials and smart technology integration. For instance, the introduction of biodegradable flossers and app-connected devices has gained significant traction among environmentally conscious and tech-savvy consumers.

Emerging players, particularly in the Asia-Pacific region, are leveraging cost-effective manufacturing and localized marketing strategies to capture market share. These companies are focusing on affordability and accessibility, introducing products that meet the needs of a broader consumer base. Additionally, the rise of e-commerce platforms has enabled smaller brands to reach a global audience, intensifying competition across all regions. Strategic partnerships, mergers, and acquisitions are also prevalent, as companies seek to expand their product portfolios and geographic presence. The competitive landscape is expected to remain dynamic, driven by continuous innovation and shifting consumer demands.

Colgate-Palmolive

The Procter & Gamble Company

GSK plc

Johnson & Johnson

Koninklijke Philips N.V.

Yunnan Baiyao Group Co., Ltd.

Lion Corporation

Sunstar Inc.

Perrigo

Church & Dwight Co. Inc.

Weimeizi (Guangdong) Co., Ltd.

LG H&H Co., Ltd.

Dencare (Chongqing) Oral Care Co., Ltd.

Dentaid SL

Technological advancements are significantly influencing the Flosser Tool Market, enhancing usability, hygiene, and consumer satisfaction. One major innovation is the integration of smart connectivity features. Bluetooth-enabled flosser tools can track user habits, offer usage insights, and synchronize with mobile applications for personalized oral hygiene plans. These features appeal particularly to younger demographics and health-conscious users who appreciate real-time feedback and gamified hygiene tracking.

Water flosser technology has also advanced with multi-pressure settings, adaptive pulsation, and noise reduction enhancements. These improvements support the effectiveness of plaque removal and offer gentler care for users with sensitive gums or orthodontic appliances. The miniaturization of components now allows for travel-sized models with near full-sized functionality, expanding consumer adoption across different lifestyle segments.

Sustainability is another driving force behind recent developments. Many manufacturers are switching to recyclable and biodegradable materials in response to environmental concerns. Rechargeable batteries with longer life spans and USB-C compatibility are becoming standard, reducing waste and offering more convenience. The convergence of digital health technologies, environmental awareness, and product customization is likely to shape the next phase of innovation in this market.

In May 2023, a leading brand launched a new cordless water flosser with a sliding compact design, focusing on portability and ergonomic improvements to enhance user experience.

In December 2023, a notable collaboration between a lifestyle dental brand and a celebrity influencer led to the release of a designer water flosser featuring dual cleaning modes, tailored for younger consumers.

In November 2023, a new product launch through a major retail chain introduced a cost-effective, ergonomically designed water flosser aimed at increasing accessibility to advanced oral care tools.

In 2023, a premium homecare brand released a high-efficiency flosser with quieter operation and advanced nozzle control, targeting consumers seeking comfort and customization in their hygiene routines.

The Flosser Tool Market Report provides a comprehensive overview of the global industry landscape, covering key market indicators, segmentation, technological innovations, and strategic insights. It offers detailed coverage of the types of flosser tools available, including traditional string flossers, electric flossers, and water flossers. The report explores various application areas such as individual oral care, dental clinics, and orthodontic use, and offers an in-depth assessment of consumer behavior and demand trends across regions.

Furthermore, the report highlights emerging developments in technology, including smart and eco-friendly innovations, which are reshaping product portfolios. It also addresses the competitive dynamics of the market, identifying top players and outlining their strategic initiatives in product development, market expansion, and mergers and acquisitions.

Regional analysis reveals differing growth trajectories, with Asia-Pacific showing strong momentum and North America maintaining dominance. The report is intended for manufacturers, distributors, policymakers, investors, and stakeholders who seek actionable insights into market opportunities, challenges, and future trajectories of the Flosser Tool Market globally.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Flosser Tool Market |

| Market Revenue (2024) | USD 864.4 Million |

| Market Revenue (2032) | USD 1,086.5 Million |

| CAGR (2025–2032) | 2.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Colgate-Palmolive, The Procter & Gamble Company, GSK plc, Johnson & Johnson, Koninklijke Philips N.V., Yunnan Baiyao Group Co., Ltd., Lion Corporation, Sunstar Inc., Perrigo, Church & Dwight Co. Inc., Weimeizi (Guangdong) Co., Ltd., LG H&H Co., Ltd., Dencare (Chongqing) Oral Care Co., Ltd., Dentaid SL, Jordan Oral Care (Orkla ASA), Prestige Consumer Healthcare Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |