Reports

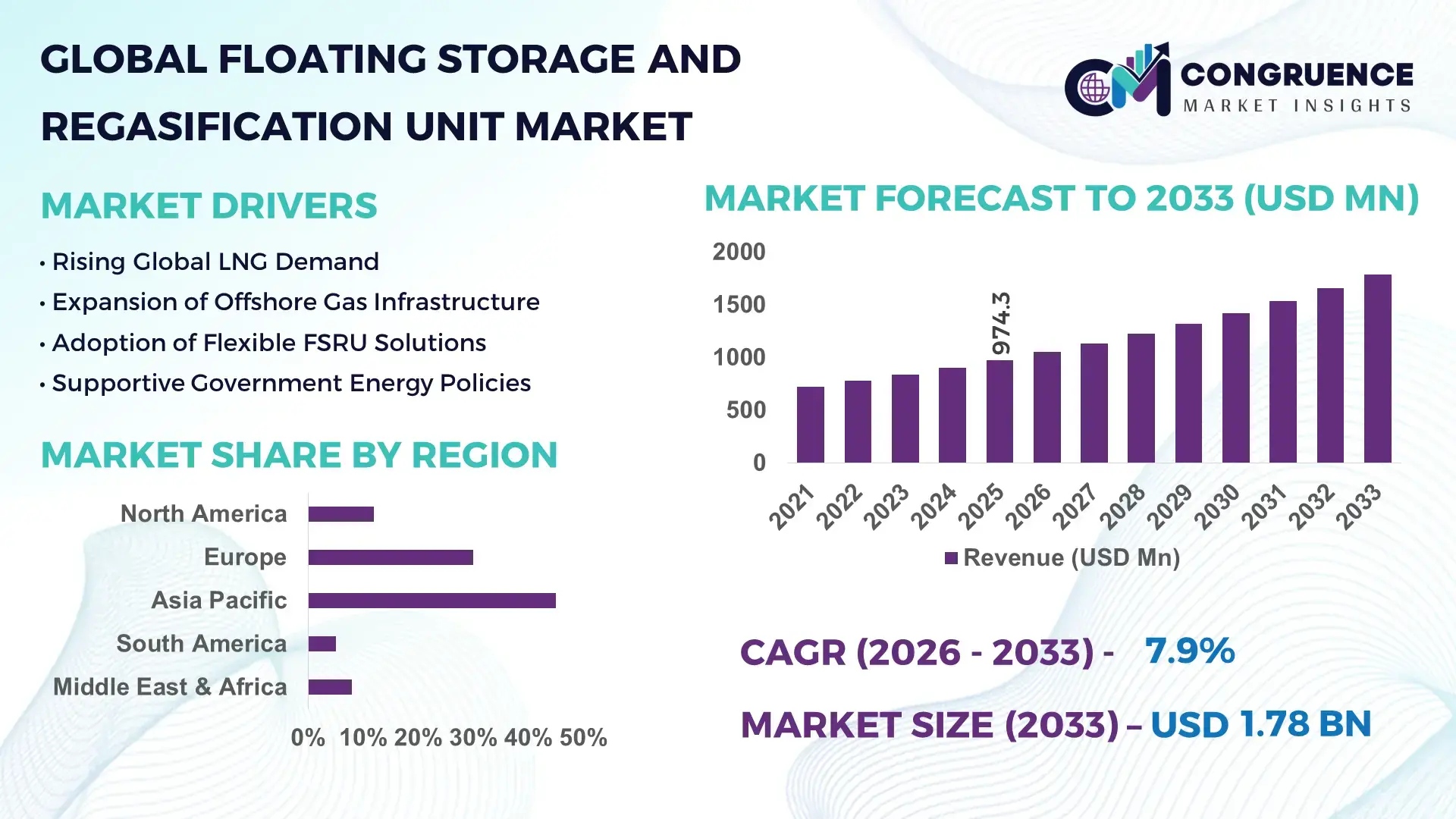

The Global Floating Storage and Regasification Unit Market was valued at USD 974.3 Million in 2025 and is anticipated to reach a value of USD 1,783.4 Million by 2033 expanding at a CAGR of 7.85% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising LNG import demand, faster deployment timelines compared to onshore terminals, and increasing energy security initiatives across gas-importing nations.

China represents the most influential country-level market in the Floating Storage and Regasification Unit Market, supported by aggressive LNG infrastructure expansion. As of 2025, China operates more than 10 FSRU-linked LNG receiving terminals, contributing to a national regasification capacity exceeding 120 million tonnes per annum (MTPA). State-owned enterprises have invested over USD 15 billion in LNG import and floating terminal infrastructure since 2020. FSRUs in China primarily support power generation (accounting for nearly 45% of imported LNG utilization), city gas distribution (around 35%), and industrial feedstock applications (20%). Advanced cryogenic regasification systems and digital monitoring platforms have improved regasification efficiency by nearly 18% over the past five years, reinforcing large-scale deployment.

Market Size & Growth: Valued at USD 974.3 Million in 2025, projected to reach USD 1,783.4 Million by 2033 at 7.85% CAGR, driven by rapid LNG import infrastructure deployment and energy diversification strategies.

Top Growth Drivers: LNG trade expansion (+12%), faster project commissioning timelines (+40%), lower upfront capex versus onshore terminals (+25%).

Short-Term Forecast: By 2028, floating regasification deployment is expected to reduce terminal commissioning time by 30% compared to land-based alternatives.

Emerging Technologies: Closed-loop regasification systems, AI-enabled asset monitoring, hybrid FSRU-to-power integration platforms.

Regional Leaders: Asia Pacific projected above USD 780 Million by 2033 with strong LNG imports; Europe exceeding USD 520 Million amid energy diversification; Middle East & Africa nearing USD 210 Million with new gas-to-power projects.

Consumer/End-User Trends: Power utilities account for nearly 48% usage, followed by city gas distributors at 32%, and industrial users at 20%.

Pilot or Case Example: In 2024, a European FSRU deployment reduced gas supply disruption risk by 35% through rapid-grid integration.

Competitive Landscape:Höegh LNG holds approximately 18% share, followed by Excelerate Energy, BW LNG, Mitsui O.S.K. Lines, and Golar LNG.

Regulatory & ESG Impact: Stricter EU methane reduction targets aim for 30% emission cuts by 2030, accelerating cleaner regasification technologies.

Investment & Funding Patterns: Over USD 20 billion committed globally since 2021 in floating LNG infrastructure and FSRU conversions.

Innovation & Future Outlook: Integration with floating power plants, carbon capture-ready modules, and digital twin technologies are shaping next-generation FSRU deployments.

The Floating Storage and Regasification Unit Market is primarily driven by the power generation sector (~48%), followed by city gas distribution (~32%) and industrial applications (~20%). Technological upgrades such as closed-loop vaporization systems and digital asset monitoring have improved operational efficiency by nearly 15%. Environmental mandates targeting 30% methane reduction by 2030 are influencing procurement decisions, while Asia-Pacific accounts for over 45% of LNG import-linked FSRU deployments. Future growth is expected from hybrid LNG-to-power solutions and modular offshore terminal expansion.

The Floating Storage and Regasification Unit Market has emerged as a strategic pillar for nations seeking rapid energy security, diversification of gas supply, and reduced infrastructure risk. Compared to traditional onshore LNG terminals that require 4–5 years for development, modular FSRU deployment can be completed within 18–24 months, delivering nearly 40% faster commissioning timelines. Closed-loop regasification systems deliver 22% lower thermal losses compared to conventional open-loop vaporization methods, enhancing operational efficiency and environmental compliance.

Asia Pacific dominates in LNG import volume, while Europe leads in rapid FSRU adoption, with over 60% of newly commissioned LNG import facilities in 2023–2025 utilizing floating infrastructure. By 2028, AI-driven predictive maintenance systems are expected to cut unplanned downtime by 25%, optimizing asset utilization and reducing lifecycle costs.

From an ESG perspective, operators are committing to 30% methane emission reductions by 2030 and integrating shore-power connectivity to lower auxiliary emissions by 15%. In 2024, Germany achieved a 35% improvement in gas import turnaround time through accelerated FSRU grid-integration initiatives, strengthening winter energy resilience.

Strategically, the Floating Storage and Regasification Unit Market is transitioning toward hybrid LNG-to-power hubs, carbon capture-ready regasification modules, and digital twin-enabled asset management. As global LNG trade volumes expand beyond 550 million tonnes annually, floating infrastructure provides scalable, lower-risk entry into gas markets. Looking ahead, the Floating Storage and Regasification Unit Market stands as a cornerstone of energy resilience, regulatory compliance, and sustainable growth in the global gas ecosystem.

The Floating Storage and Regasification Unit Market is shaped by expanding global LNG trade flows, geopolitical energy diversification strategies, and the increasing preference for flexible gas infrastructure. With global LNG demand surpassing 400 million tonnes annually, importing nations are prioritizing floating regasification solutions due to faster deployment cycles and reduced land acquisition constraints. The market is further influenced by volatility in pipeline gas supply, growing electricity demand in emerging economies, and the expansion of gas-fired power generation capacity. Technological advancements, including digital monitoring platforms and energy-efficient vaporization systems, are improving regasification throughput by up to 20%. Additionally, regulatory focus on methane emission reductions and decarbonization targets is accelerating modernization of floating infrastructure, reshaping procurement and investment decisions across regions.

Global LNG trade volumes exceeded 400 million tonnes in recent years, with Asia accounting for nearly 70% of total imports. Many emerging economies have expanded gas-fired power capacity by over 15% in the past five years, increasing reliance on imported LNG. FSRUs provide import capacities ranging from 3 to 7 MTPA per unit, enabling rapid response to peak seasonal demand. Compared to land-based terminals requiring multi-year construction, floating units reduce deployment timelines by approximately 40%, supporting urgent supply diversification. In regions facing pipeline disruptions, FSRUs have increased short-term gas availability by nearly 30%, stabilizing domestic power grids and industrial gas supply chains.

FSRU conversion costs can exceed USD 250 million per vessel, while newbuild units may require investments above USD 300 million. Charter rates have increased by nearly 20% during periods of heightened LNG demand, placing financial pressure on smaller importing nations. Infrastructure integration, including subsea pipelines and port modifications, can account for an additional 15–25% of total project expenditure. Furthermore, regulatory approvals and environmental impact assessments can delay commissioning by 6–12 months. These financial and operational constraints limit entry for countries with constrained budgets or underdeveloped port infrastructure.

The integration of FSRUs with floating power plants offers scalable electricity generation for island nations and emerging markets. Gas-to-power projects linked to floating regasification units can generate between 300 MW and 1,000 MW per installation, supporting grid expansion in underserved regions. Africa and Southeast Asia collectively represent over 40 GW of planned gas-fired capacity additions through 2030. Hybrid LNG-to-power configurations reduce transmission losses by up to 18% compared to imported electricity alternatives. Additionally, repurposing aging LNG carriers into FSRUs extends vessel lifecycle by 15–20 years, creating cost-effective expansion pathways.

Port congestion, limited berth availability, and insufficient pipeline connectivity can restrict FSRU utilization rates by up to 25%. Environmental concerns related to seawater intake in open-loop systems have led several countries to impose stricter discharge temperature regulations. Compliance upgrades can increase retrofit costs by nearly 12%. Additionally, fluctuations in global LNG prices impact import affordability, influencing capacity utilization levels. Workforce skill gaps in offshore regasification operations also pose operational risks, with specialized training requirements increasing project preparation timelines by 6–9 months.

45% Increase in Rapid-Deployment LNG Terminals: Between 2022 and 2025, over 45% of newly commissioned LNG import terminals globally utilized floating regasification models. Deployment timelines averaging 18–24 months have improved project turnaround efficiency by nearly 40% compared to land-based facilities, particularly in Europe and Asia.

30% Efficiency Gains Through Closed-Loop Systems: Adoption of closed-loop vaporization technology has grown by approximately 30% across new FSRU installations, reducing seawater dependency and lowering thermal discharge impact. These systems enhance energy efficiency by up to 22% and reduce operational environmental risks.

25% Reduction in Unplanned Downtime via Digital Monitoring: AI-enabled predictive maintenance platforms implemented across major FSRU fleets have reduced unexpected outages by nearly 25%. Digital twin integration has improved asset lifecycle optimization by approximately 18%, enhancing fleet reliability.

35% Growth in LNG-to-Power Hybrid Projects: Hybrid floating LNG-to-power projects expanded by nearly 35% between 2023 and 2025, with individual installations generating up to 1,000 MW. These configurations reduce fuel switching time by 20% and improve grid stability in high-demand regions.

The Floating Storage and Regasification Unit Market is segmented by type, application, and end-user, reflecting diverse operational models and consumption patterns across global LNG-importing regions. By type, the market includes newly built FSRUs and converted LNG carriers, each addressing distinct capital and deployment requirements. Application-wise, floating regasification supports power generation, city gas distribution, and industrial feedstock supply, with power utilities accounting for nearly half of global regasified LNG utilization. End-user segmentation highlights utilities, energy traders, and government-backed infrastructure agencies as primary stakeholders. Increasing electrification, urban gas penetration programs, and industrial fuel switching initiatives are strengthening demand across these segments. Technological integration—such as digital asset monitoring and closed-loop vaporization—further differentiates deployment preferences within each category, offering measurable efficiency gains and environmental compliance advantages for operators and policymakers.

The Floating Storage and Regasification Unit Market by type comprises Newbuild FSRUs and Converted FSRUs (LNG carrier conversions). Converted FSRUs currently account for approximately 58% of operational deployments, as vessel retrofitting reduces capital expenditure by nearly 25% compared to newbuild alternatives and shortens delivery timelines by 12–18 months. In contrast, newbuild FSRUs hold around 42% of installations but are expanding steadily due to enhanced storage capacities exceeding 180,000 cubic meters and integrated regasification modules offering 20% higher operational efficiency. Converted FSRUs remain the leading segment due to flexibility and cost optimization. However, newbuild FSRUs are the fastest-growing type, expanding at an estimated 8.6% annual growth rate, driven by demand for higher send-out capacities exceeding 750 million standard cubic feet per day and compatibility with closed-loop systems. Other niche configurations, including hybrid floating LNG-to-power units, collectively represent under 10% of installations but are gaining relevance in island economies and remote regions.

In 2024, the International Gas Union reported that more than 35 LNG carriers were under evaluation globally for potential FSRU conversion, reflecting growing preference for retrofit-based expansion strategies.

Power generation is the dominant application, accounting for approximately 48% of total FSRU utilization, as gas-fired plants increasingly replace coal and oil-based generation. City gas distribution represents nearly 32%, supporting urban residential and commercial heating demand. Industrial applications—including petrochemicals, fertilizers, and manufacturing—contribute around 20%. While power generation leads in adoption, city gas distribution is expanding rapidly, supported by urbanization and cleaner fuel mandates. Industrial use is the fastest-growing application, projected to grow at approximately 9.1% annually, driven by fuel-switching initiatives and feedstock diversification in emerging economies. In 2025, nearly 41% of LNG-importing utilities reported prioritizing floating regasification to stabilize grid operations during peak demand. Additionally, over 36% of large industrial gas consumers in Asia indicated plans to increase LNG procurement via floating terminals within the next three years.

In 2024, Germany’s Federal Network Agency confirmed that newly deployed FSRU-linked terminals significantly enhanced winter gas supply resilience, increasing national import flexibility by over 30%.

Utilities represent the leading end-user segment, accounting for nearly 50% of total FSRU-linked LNG offtake due to direct integration with national power grids and gas distribution networks. National oil and gas companies follow with approximately 30%, leveraging floating infrastructure for strategic import diversification. Independent power producers and large industrial operators collectively contribute around 20%. While utilities dominate current utilization, independent power producers (IPPs) are the fastest-growing end-user category, expanding at an estimated 9.4% annually, supported by decentralized gas-to-power projects ranging from 300 MW to 1,000 MW per installation. In 2025, approximately 44% of gas-importing governments prioritized floating regasification within national energy security frameworks. Additionally, nearly 38% of LNG trading companies increased short-term charter agreements to optimize seasonal procurement strategies.

In 2024, the European Commission reported that floating LNG infrastructure additions improved regional gas storage flexibility by more than 25%, directly supporting utility-led energy transition programs.

Asia-Pacific accounted for the largest market share at 45% in 2025; however, Europe is expected to register the fastest growth, expanding at a CAGR of8.9% between 2026 and 2033.

Asia-Pacific’s leadership is supported by LNG import volumes exceeding 280 million tonnes annually, with more than 20 active floating regasification terminals across China, India, Japan, and Southeast Asia. Europe holds approximately 30% share, driven by the rapid commissioning of over 10 FSRUs between 2022 and 2025, significantly increasing regasification capacity by more than 60 billion cubic meters per year. North America contributes around 12%, primarily through LNG export-linked floating infrastructure and strategic import balancing. The Middle East & Africa represent nearly 8%, supported by gas-to-power projects exceeding 15 GW in planning or development. South America accounts for roughly 5%, with Brazil and Argentina leading regional floating LNG adoption. Increasing electrification, industrial gas demand growth of over 6% annually in emerging markets, and diversification from pipeline gas remain central regional growth catalysts.

North America holds approximately 12% of the global Floating Storage and Regasification Unit Market share, supported by strategic LNG balancing, export-import arbitrage, and energy security initiatives. While the United States is a major LNG exporter exceeding 80 million tonnes annually, floating regasification plays a niche yet strategic role in seasonal supply balancing and offshore power integration. Canada is evaluating floating LNG import options to support eastern provinces, where pipeline connectivity constraints exist. Regulatory frameworks emphasize methane emission reductions of 30% by 2030, prompting adoption of closed-loop vaporization systems and digital emissions tracking. Advanced digital twin integration has improved asset monitoring efficiency by nearly 20% across LNG infrastructure. Regional adoption patterns show higher enterprise demand in power utilities and industrial gas consumers, with nearly 40% of large-scale utilities evaluating floating infrastructure for grid resilience strategies.

Europe accounts for nearly 30% of the global Floating Storage and Regasification Unit Market share, with Germany, the United Kingdom, France, Italy, and the Netherlands emerging as key LNG-importing economies. Since 2022, more than 10 FSRUs have been deployed, increasing regional regasification capacity by over 60 bcm annually. Germany alone commissioned multiple floating terminals within 12–18 months to stabilize winter supply. European regulatory bodies emphasize methane reduction targets of 30% by 2030 and carbon intensity disclosures, accelerating adoption of environmentally compliant regasification systems. Hybrid grid-integration technologies have improved send-out reliability by approximately 25%. Consumer behavior reflects regulatory-driven procurement, with over 55% of new LNG capacity additions favoring floating systems for rapid deployment and flexibility.

Asia-Pacific leads the Floating Storage and Regasification Unit Market with approximately 45% global share, supported by LNG import demand exceeding 280 million tonnes annually. China, India, and Japan represent the top consuming countries, collectively accounting for over 65% of regional LNG imports. China’s regasification capacity surpasses 120 MTPA, while India has expanded floating terminal infrastructure to support gas-based power and fertilizer production. Infrastructure expansion includes port modernization and floating terminal installations capable of 5–7 MTPA per unit. Regional digitalization initiatives have improved regasification operational efficiency by nearly 18%. Regional adoption patterns are driven by urban gas penetration and industrial fuel-switching, with over 42% of new gas-fired power additions relying on LNG-linked supply chains.

South America represents approximately 5% of the global Floating Storage and Regasification Unit Market. Brazil and Argentina are the primary markets, with Brazil operating multiple floating LNG terminals supporting thermal power plants exceeding 3 GW capacity. Argentina has expanded floating regasification to stabilize seasonal gas shortages. Infrastructure trends include integration with offshore production hubs and diversification from hydroelectric volatility. Government energy diversification programs aim to increase gas-fired generation by nearly 15% over five years. Regional procurement emphasizes flexible charter agreements, with over 35% of LNG imports tied to floating regasification during peak demand seasons. Consumer demand is closely linked to industrial and utility-scale energy consumption patterns.

The Middle East & Africa account for approximately 8% of the Floating Storage and Regasification Unit Market. Key growth countries include the UAE, Egypt, Pakistan, and South Africa, where gas-to-power projects exceeding 15 GW are planned or operational. LNG imports supplement domestic production, particularly during peak electricity demand. Technological modernization includes adoption of hybrid floating LNG-to-power units capable of generating up to 1,000 MW. Regulatory reforms in several African economies encourage private-sector LNG participation, improving port infrastructure efficiency by nearly 20%. Regional adoption is strongly tied to electricity demand growth exceeding 6% annually in several African markets. Floating solutions provide rapid grid connectivity, reducing fuel-switching timelines by approximately 30%.

China – 22% Market Share: High LNG import capacity exceeding 120 MTPA and large-scale deployment of floating regasification terminals supporting power and industrial sectors.

Germany – 15% Market Share: Accelerated FSRU commissioning since 2022, expanding regasification capacity by over 20 bcm annually to strengthen national energy security.

The Floating Storage and Regasification Unit Market exhibits a moderately consolidated competitive environment with more than 40 active global players operating across vessel conversion, newbuild FSRUs, and hybrid LNG-to-power units. The top 5 companies, including Höegh LNG, Excelerate Energy, BW LNG, Mitsui O.S.K. Lines, and Golar LNG, collectively account for approximately 65% of total deployed capacity, reflecting significant market influence. Competition is driven by strategic initiatives such as long-term charter agreements, technological partnerships for closed-loop regasification systems, and fleet modernization programs. Over the past three years, more than 15 new FSRU contracts have been signed globally, demonstrating the rapid pace of adoption in Asia-Pacific, Europe, and emerging African markets. Companies are investing in digital twin technologies, AI-enabled predictive maintenance, and hybrid LNG-to-power configurations, improving operational efficiency by 18–25% and reducing unplanned downtime. The market is characterized by high entry barriers due to substantial capital requirements (USD 250–300 million per vessel) and technical expertise, resulting in fewer but highly specialized competitors. Innovation trends include modular FSRU designs, carbon capture-ready units, and advanced cryogenic systems capable of handling up to 7 MTPA of LNG per vessel. Overall, strategic alliances, fleet expansions, and technology-driven differentiation are defining competitive positioning for market leadership.

Mitsui O.S.K. Lines

Golar LNG

Teekay LNG Partners

K Line LNG Shipping

NYK LNG Shipping

MOL LNG Transport

Yamal LNG Offshore

Qatar Gas Transport

Gaztransport & Technigaz (GTT)

Samsung Heavy Industries LNG Division

Daewoo Shipbuilding & Marine Engineering LNG Division

Technological advancements are reshaping the Floating Storage and Regasification Unit Market, enhancing operational efficiency, environmental compliance, and scalability. Closed-loop regasification systems are increasingly deployed to reduce seawater dependency, minimize thermal discharge, and improve energy efficiency by approximately 22% compared to conventional open-loop designs. Digital twin technologies are integrated into FSRU operations, providing real-time monitoring of cryogenic storage tanks, vaporization modules, and pipeline connectivity, reducing unplanned downtime by nearly 25%. AI-enabled predictive maintenance platforms allow operators to identify potential failures, optimizing scheduling and extending vessel lifecycle by 15–20 years. Emerging trends include hybrid LNG-to-power units, capable of generating 300–1,000 MW, enabling decentralized electricity production for island nations and industrial zones. Modular FSRU designs facilitate faster deployment, with pre-fabricated regasification and storage modules reducing construction timelines by up to 40%. Companies are also exploring carbon capture-ready units, enabling future integration with decarbonization initiatives and compliance with methane emission reduction targets. Advanced cryogenic materials and high-capacity storage tanks exceeding 180,000 cubic meters improve LNG throughput while reducing boil-off gas losses. Overall, these innovations are accelerating deployment flexibility, reducing operational risk, and positioning FSRUs as pivotal infrastructure in global LNG supply chains.

In October 2025, Excelerate Energy announced it had signed a definitive commercial agreement with a subsidiary of Iraq’s Ministry of Electricity to develop the country’s first fully integrated floating LNG import terminal at the Port of Khor Al Zubair. The integrated project includes a five‑year regasification services and LNG supply agreement with extension options and minimum contracted offtake of 250 MMscf/d, deploying its newest FSRU, Hull 3407, with 170,000 m³ storage and ~1 billion scf/d regasification capacity, planned for 2026 operations. Source: www.excelerateenergy.com

In January 2026, Excelerate Energy’s Hull 3407 FSRU completed sea trials ahead of its deployment for the integrated LNG import terminal project in Iraq, marking a major construction milestone as the vessel advances toward performance and safety certification before gas trials. Source: www.offshore‑energy.biz

In June 2025, Wärtsilä Gas Solutions was contracted to supply a high‑capacity regasification module for Höegh LNG’s conversion of the LNG carrier Hoegh Gandria into a floating storage and regasification unit (FSRU). The converted vessel will support up to 1,000 mmscf/day regasification capacity when deployed, reinforcing long‑standing technological collaboration. Source: www.wartsila.com

In April–May 2025, Excelerate Energy reported record quarterly results (Q3 2025), including strong Adjusted EBITDA of USD 129.3 million, execution of the Iraq FSRU project agreement, and support for operational momentum in Jamaica, along with approval of a quarterly cash dividend of USD 0.08 per share for shareholders. Source: www.excelerateenergy.com

The Floating Storage and Regasification Unit Market Report provides a comprehensive assessment of global market segments, technologies, and regional dynamics. It covers product types, including newbuild FSRUs, converted LNG carriers, and hybrid LNG-to-power units, detailing operational capacity, storage volumes, and deployment flexibility. Application coverage includes power generation, city gas distribution, and industrial feedstock supply, with insights into infrastructure requirements, technological integration, and consumption patterns. The report analyzes end-user segments, focusing on utilities, national oil and gas companies, independent power producers, and industrial operators, providing adoption statistics and sector-specific trends. Geographically, it examines Asia-Pacific, Europe, North America, South America, and Middle East & Africa, highlighting terminal capacity, project timelines, regulatory frameworks, and government incentives. Technological coverage includes closed-loop regasification systems, digital twin integration, AI predictive maintenance, modular construction, and carbon capture-ready FSRUs, emphasizing deployment efficiency, environmental compliance, and lifecycle optimization. Additionally, the report evaluates emerging and niche opportunities, such as island LNG-to-power projects, hybrid vessels, and retrofitting programs, offering decision-makers actionable insights into fleet optimization, strategic investments, and operational planning. This scope ensures stakeholders gain a detailed understanding of market dynamics, competitive positioning, and future-ready technologies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 974.3 Million |

| Market Revenue (2033) | USD 1,783.4 Million |

| CAGR (2026–2033) | 7.85% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Höegh LNG; Excelerate Energy; BW LNG; Mitsui O.S.K. Lines; Golar LNG; Teekay LNG Partners; K Line LNG Shipping; NYK LNG Shipping; MOL LNG Transport; Yamal LNG Offshore; Qatar Gas Transport; Gaztransport & Technigaz (GTT); Samsung Heavy Industries LNG Division; Daewoo Shipbuilding & Marine Engineering LNG Division |

| Customization & Pricing | Available on Request (10% Customization Free) |