Reports

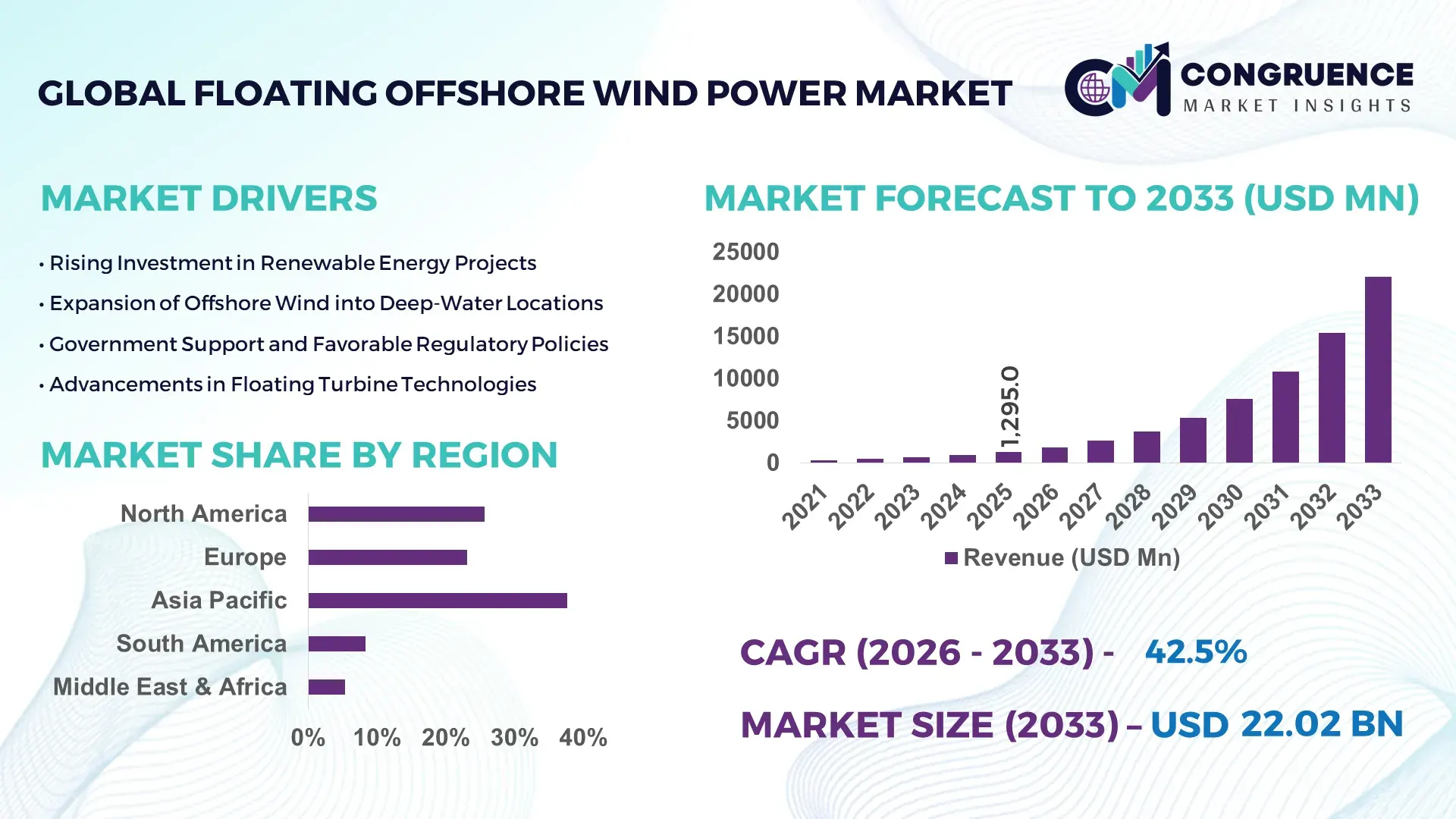

The Global Floating Offshore Wind Power Market was valued at USD 1295 Million in 2025 and is anticipated to reach a value of USD 22018.54 Million by 2033 expanding at a CAGR of 42.5% between 2026 and 2033. This accelerated growth is primarily driven by the increasing deployment of advanced floating wind turbines in deep-water zones, enabling higher energy capture and expanding offshore renewable capacity.

The United Kingdom continues to play a central role in the floating offshore wind power market, supported by more than 30 GW of installed offshore wind capacity and a rapidly expanding floating segment. The country has allocated over USD 5 billion toward floating wind project development, particularly through large-scale leasing programs such as ScotWind. Industrial utilization spans grid-scale electricity generation, offshore oil platform electrification, and green hydrogen production. Technological innovations including semi-submersible platforms and dynamic cable systems have improved installation efficiency by over 20% while reducing operational risks. Offshore wind currently contributes over 25% of national electricity generation, reflecting strong adoption across utility-scale energy providers and industrial consumers.

Market Size & Growth: USD 1295 Million in 2025, projected to reach USD 22018.54 Million by 2033, expanding at a CAGR of 42.5%, driven by deep-water wind resource utilization and clean energy transition initiatives

Top Growth Drivers: Offshore capacity expansion +38%, turbine efficiency improvements +25%, renewable adoption acceleration +40%

Short-Term Forecast: By 2028, installation and deployment costs are expected to decrease by 18% due to modular floating platform advancements

Emerging Technologies: AI-based predictive maintenance systems, next-generation floating substructures, and advanced mooring stabilization technologies

Regional Leaders: Europe projected to reach USD 11000 Million by 2033 with strong regulatory backing; Asia-Pacific USD 7000 Million with aggressive coastal expansion; North America USD 4000 Million driven by pilot-scale commercialization

Consumer/End-User Trends: Utilities contribute over 65% of demand, followed by hydrogen production facilities and offshore oil & gas electrification projects

Pilot or Case Example: In 2024, a Norway-based floating wind project achieved a 30% reduction in maintenance downtime through real-time digital monitoring systems

Competitive Landscape: Leading player holds approximately 28% share, followed by major companies including Equinor, Siemens Gamesa, Vestas, and Principle Power

Regulatory & ESG Impact: Governments targeting up to 50% offshore renewable integration by 2035, supported by carbon neutrality mandates and sustainability frameworks

Investment & Funding Patterns: Over USD 15 billion in global investments driven by institutional funding, public-private partnerships, and green financing models

Innovation & Future Outlook: Hybrid offshore wind-to-hydrogen systems, floating substations, and grid integration technologies shaping next-generation deployment strategies

The floating offshore wind power market is supported by diverse end-use sectors including utilities, oil & gas, and green hydrogen, contributing approximately 60%, 20%, and 15% respectively to overall demand. Technological advancements such as turbines exceeding 15 MW capacity, digital twin integration, and floating substations are improving efficiency and reducing lifecycle costs. Regulatory frameworks across Europe and Asia-Pacific are accelerating permitting and incentivizing renewable energy investments. Regional consumption trends highlight strong adoption in deep-water coastal economies, while emerging markets are advancing pilot deployments. The market is witnessing increased collaboration between energy companies and technology providers, reinforcing long-term growth potential and innovation-driven expansion.

Floating offshore wind power market development is strategically aligned with global decarbonization targets and energy security initiatives, particularly in regions with limited shallow seabeds. Advanced floating turbine technology delivers 35% higher energy yield compared to traditional fixed-bottom offshore systems due to access to high-wind-speed zones. Europe dominates in volume deployment, while Asia-Pacific leads in adoption with over 45% of new offshore energy developers investing in floating technologies.

By 2028, AI-enabled predictive analytics and autonomous maintenance systems are expected to reduce operational costs by 22% while improving turbine uptime by 18%. Governments and corporations are committing to ESG benchmarks, targeting up to 60% carbon emission reduction in offshore energy portfolios by 2030. Additionally, floating wind farms are increasingly integrated with green hydrogen production facilities, creating multi-output energy ecosystems.

In 2024, Norway achieved a 28% increase in turbine efficiency through the integration of real-time digital monitoring and adaptive blade pitch control systems. Such measurable advancements demonstrate the scalability and resilience of floating offshore wind infrastructure. Regulatory frameworks, including offshore leasing reforms and carbon pricing mechanisms, are further strengthening market expansion. The floating offshore wind power market is positioned as a critical pillar of sustainable energy transformation, offering resilience against energy supply disruptions, ensuring regulatory compliance, and enabling long-term industrial decarbonization strategies across global markets.

The ability to harness deep-water wind resources is a major driver of floating offshore wind power market growth, as approximately 80% of offshore wind potential lies in waters deeper than 60 meters. Floating turbines can access wind speeds that are 20–30% higher than nearshore locations, significantly improving energy output and capacity factors. Countries with limited shallow coastal areas, such as Japan and Norway, are increasingly investing in floating wind technologies to expand renewable energy generation. Additionally, advancements in turbine size, exceeding 15 MW capacity, are enhancing power generation efficiency by over 25%. These developments are supported by favorable government policies, including subsidies and long-term power purchase agreements, which encourage large-scale deployment. The ability to deploy turbines further offshore also reduces visual and environmental impact concerns, improving public acceptance and accelerating project approvals.

High capital expenditure remains a significant restraint in the floating offshore wind power market, with installation costs estimated to be 2–3 times higher than fixed-bottom offshore wind systems. Complex engineering requirements, including advanced mooring systems, dynamic cables, and specialized installation vessels, contribute to elevated project costs. Additionally, limited port infrastructure capable of assembling large floating platforms restricts scalability in several regions. Supply chain constraints, particularly for high-capacity turbines and subsea components, further increase project timelines and expenses. Maintenance operations in deep-water environments are also more challenging, leading to higher operational costs. Financing large-scale projects requires substantial upfront investment, which can deter smaller developers and slow down market penetration despite strong long-term potential.

The integration of floating offshore wind power with green hydrogen production presents a significant growth opportunity, enabling the conversion of excess electricity into hydrogen for storage and industrial use. Offshore hydrogen production can improve energy utilization efficiency by up to 30%, reducing curtailment during periods of low grid demand. Countries such as Germany and the Netherlands are investing in offshore hydrogen hubs, combining floating wind farms with electrolysis facilities. This approach supports decarbonization in hard-to-abate sectors including steel, chemicals, and heavy transport. Additionally, floating wind systems can power offshore oil and gas platforms, reducing emissions by up to 40%. The development of hybrid energy systems, including wind-to-hydrogen and wind-to-ammonia, is expected to unlock new revenue streams and enhance the economic viability of floating offshore wind projects.

Regulatory complexities and grid integration challenges pose significant obstacles to the floating offshore wind power market. Offshore permitting processes often involve multiple regulatory bodies, leading to approval timelines extending beyond 5–7 years in some regions. Environmental impact assessments, maritime zoning regulations, and cross-border energy policies add layers of complexity to project development. Furthermore, integrating large-scale floating wind capacity into existing grid infrastructure requires significant upgrades, including high-voltage subsea transmission systems. Grid congestion and limited interconnection capacity can result in energy curtailment, reducing project efficiency. The lack of standardized regulations across regions also creates uncertainty for investors and developers. Addressing these challenges requires coordinated policy frameworks, investment in grid modernization, and streamlined approval processes to support large-scale deployment.

Expansion of High-Capacity Floating Turbines Beyond 15 MW: The floating offshore wind power market is witnessing rapid adoption of next-generation turbines exceeding 15 MW capacity, improving energy output by over 30% compared to earlier 8–10 MW systems. More than 40% of new project pipelines in Europe and Asia-Pacific are now designed around high-capacity turbines to maximize efficiency in deep-water environments. Larger rotor diameters, often exceeding 220 meters, are enabling higher capacity factors above 55%, significantly improving power generation consistency. This trend is also reducing the number of turbines required per project by nearly 20%, optimizing installation logistics and long-term operational efficiency.

Rise in Modular and Prefabricated Floating Platform Construction: Modular construction techniques are transforming project execution, with approximately 55% of newly commissioned floating wind projects reporting reduced installation timelines by up to 25%. Prefabricated components, including pre-assembled floating hulls and turbine sections, are increasingly manufactured off-site using automated fabrication systems. This has lowered labor dependency by nearly 30% and improved quality consistency. Regions such as Europe and North America are leading adoption, with over 60% of new floating wind projects integrating modular assembly processes to enhance scalability and reduce offshore construction risks.

Integration of Digital Monitoring and AI-Based Predictive Maintenance: Digitalization is reshaping operational efficiency, with over 70% of floating wind operators deploying AI-driven monitoring systems to optimize turbine performance. Predictive maintenance technologies have reduced unplanned downtime by 25–35%, while increasing asset lifespan by approximately 15%. Advanced sensors and real-time data analytics are enabling early fault detection and automated performance adjustments. This trend is particularly prominent in Norway and the United Kingdom, where digital twin technologies are being implemented in more than 50% of operational floating wind farms to enhance reliability and reduce maintenance costs.

Hybridization with Offshore Hydrogen and Energy Storage Systems: The integration of floating offshore wind with hydrogen production and energy storage is emerging as a key trend, with over 35% of upcoming projects incorporating hybrid energy systems. Offshore electrolysis powered by floating wind is improving energy utilization efficiency by nearly 30%, reducing curtailment during low grid demand periods. Additionally, floating wind-to-hydrogen systems are supporting decarbonization in industrial sectors, with pilot projects demonstrating emission reductions exceeding 40%. Energy storage integration, including battery and subsea storage systems, is further stabilizing power output and enhancing grid compatibility across large-scale offshore deployments.

The floating offshore wind power market is segmented based on type, application, and end-user, reflecting a diverse and rapidly evolving industry landscape. By type, the market includes spar-buoy, semi-submersible, and tension-leg platform systems, each offering unique structural and operational advantages. In terms of application, floating wind is primarily deployed for utility-scale electricity generation, offshore oil and gas electrification, and green hydrogen production. End-user segmentation highlights utilities, energy companies, and industrial operators as key stakeholders. Approximately 60% of installations are driven by large-scale utilities, while emerging applications such as hydrogen production are gaining traction, contributing nearly 15% of demand. The segmentation structure demonstrates a clear shift toward integrated energy systems and advanced floating technologies, enabling broader adoption across regions with deep-water access and strong renewable energy policies.

The floating offshore wind power market is categorized into spar-buoy, semi-submersible, and tension-leg platform systems. Semi-submersible platforms currently dominate the market, accounting for approximately 48% of total installations due to their stability, ease of assembly, and suitability for a wide range of water depths. Spar-buoy systems hold around 32% share, offering high stability in deep-water conditions exceeding 100 meters, while tension-leg platforms account for nearly 20%, providing reduced motion and enhanced turbine efficiency.

Semi-submersible systems are widely preferred because they can be assembled at port and towed to offshore locations, reducing installation complexity by nearly 25%. However, spar-buoy platforms are gaining traction due to their superior performance in harsh marine environments, particularly in regions like the North Sea.

The fastest-growing segment is tension-leg platforms, expanding at an estimated CAGR of over 45%, driven by their ability to minimize vertical motion and improve energy capture efficiency by approximately 20%. These systems are increasingly being adopted in pilot-scale projects where precision and stability are critical.

The floating offshore wind power market applications include utility-scale power generation, offshore oil and gas electrification, and green hydrogen production. Utility-scale electricity generation dominates the segment, accounting for nearly 62% of total deployment, driven by increasing demand for renewable energy integration into national grids. Offshore oil and gas electrification contributes around 23%, enabling emission reductions of up to 40% by replacing diesel-based power systems on platforms.

Green hydrogen production currently holds approximately 15% share but is rapidly emerging as a transformative application. While utility-scale generation leads in adoption, hydrogen-based applications are growing fastest, with an expected CAGR exceeding 48%, supported by rising investments in offshore electrolysis infrastructure and industrial decarbonization initiatives.

Other niche applications, including offshore desalination and hybrid energy systems, collectively contribute around 10% of the market, reflecting growing diversification.

End-users in the floating offshore wind power market include utilities, oil & gas companies, and industrial energy consumers. Utilities dominate the market with approximately 60% share, driven by large-scale offshore wind farm development and grid integration requirements. Oil and gas companies account for around 25%, leveraging floating wind systems to electrify offshore operations and reduce carbon emissions by up to 40%.

Industrial users, including hydrogen producers and heavy manufacturing sectors, represent nearly 15% of the market and are emerging as the fastest-growing segment, with an estimated CAGR exceeding 50%. These industries are increasingly adopting floating wind power to secure stable, low-carbon energy supply for energy-intensive processes.

Other smaller end-users, including research institutions and government pilot projects, collectively contribute around 10%, supporting innovation and early-stage deployment.

Region Europe accounted for the largest market share at 52% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 46% between 2026 and 2033.

Europe leads due to its mature offshore wind infrastructure, with over 30 GW installed offshore capacity and more than 5 GW allocated to floating wind development pipelines. The region has committed over 70 GW of future offshore wind capacity, with nearly 15% expected to be floating-based installations. Asia-Pacific is rapidly scaling, with countries like Japan and South Korea targeting over 20 GW of floating wind capacity combined by 2035. North America holds approximately 18% share, supported by over 10 GW of planned offshore projects, while South America and the Middle East & Africa collectively account for less than 10% but show increasing project announcements exceeding 8 GW. Increasing investments in deep-water energy projects, regulatory support, and technological advancements are reshaping regional deployment patterns, with global floating wind installations expected to surpass 25 GW by 2033.

North America accounts for approximately 18% of the floating offshore wind power market, driven by strong policy frameworks and increasing offshore leasing activities. The United States leads the region with over 10 GW of planned offshore wind capacity, including floating wind pilot projects along the West Coast where water depths exceed 800 meters. Key industries driving demand include utilities, offshore oil & gas electrification, and green hydrogen production. Government initiatives such as federal leasing auctions and tax incentives are accelerating project development, with over 70% of offshore wind areas already leased for future exploration. Technological advancements include the adoption of digital twin systems and AI-based monitoring, improving turbine efficiency by nearly 20%. A notable regional player, Principle Power, has deployed advanced floating platform technology that reduces installation costs by approximately 15%. Consumer behavior in the region reflects high enterprise-level adoption, particularly among utility providers seeking long-term renewable energy contracts and grid stability solutions.

Europe dominates the floating offshore wind power market with a 52% share, supported by strong regulatory frameworks and aggressive renewable energy targets. Key markets such as the United Kingdom, Norway, and France are leading installations, with the UK alone targeting over 5 GW of floating wind capacity by 2030. Regulatory bodies have introduced streamlined permitting processes and financial incentives, enabling faster project approvals. Approximately 65% of new offshore wind projects in Europe now incorporate floating technology to expand into deeper waters. Advanced technologies such as semi-submersible platforms and digital monitoring systems are widely adopted, improving operational efficiency by over 25%. Equinor, a leading regional player, has implemented floating wind farms that achieve capacity factors above 50%. Consumer behavior is strongly influenced by regulatory pressure and sustainability mandates, with energy providers prioritizing transparent and efficient renewable energy solutions to meet carbon neutrality goals.

Asia-Pacific ranks as the fastest-growing region in the floating offshore wind power market, accounting for approximately 22% of global installations while rapidly expanding its project pipeline. Countries such as Japan, South Korea, and China are leading demand, with combined floating wind targets exceeding 20 GW by 2035. Infrastructure development is accelerating, with over 15 specialized offshore assembly ports under construction to support large-scale turbine deployment. The region is also emerging as a manufacturing hub, producing more than 40% of global offshore wind components. Technological innovation is concentrated in coastal industrial zones, where advanced floating platform designs and hybrid energy systems are being tested. A key regional player, Mitsubishi Heavy Industries, is developing floating turbines optimized for typhoon-prone conditions, improving structural resilience by 30%. Consumer behavior in the region is driven by rapid industrialization and energy demand, with governments prioritizing scalable and cost-efficient offshore energy solutions.

South America holds approximately 5% of the floating offshore wind power market, with Brazil and Argentina emerging as key contributors. Brazil alone has announced over 6 GW of offshore wind projects, many of which are being evaluated for floating technology due to deep coastal waters. The region’s energy sector is undergoing transformation, with increasing diversification toward renewable sources to reduce dependence on hydropower. Government incentives, including tax benefits and streamlined licensing, are encouraging foreign investments in offshore wind infrastructure. Technological adoption remains in early stages, with pilot projects focusing on semi-submersible platforms and hybrid energy systems. A regional energy company has initiated a floating wind pilot project aiming to reduce offshore oil platform emissions by 25%. Consumer behavior reflects growing interest in sustainable energy, particularly among industrial users seeking stable power supply and reduced carbon footprints.

The Middle East & Africa region accounts for nearly 3% of the floating offshore wind power market but is gaining momentum due to energy diversification strategies. Countries such as the UAE and South Africa are exploring floating wind as part of their renewable energy portfolios, with combined project pipelines exceeding 4 GW. Demand is primarily driven by the oil & gas sector, which is integrating floating wind systems to reduce offshore operational emissions by up to 35%. Technological modernization includes the adoption of advanced monitoring systems and hybrid energy integration, improving efficiency by nearly 20%. Trade partnerships with European technology providers are accelerating knowledge transfer and project development. A regional energy firm has initiated a pilot floating wind project designed to power offshore facilities, demonstrating early-stage adoption. Consumer behavior in the region is influenced by industrial energy demand and government-led sustainability initiatives aimed at reducing carbon intensity.

United Kingdom – 28% share in the floating offshore wind power market, driven by large-scale offshore capacity expansion and strong regulatory support for renewable energy deployment

Norway – 18% share in the floating offshore wind power market, supported by advanced technological innovation and extensive deep-water offshore project development

The floating offshore wind power market is moderately consolidated, with approximately 25–30 active global competitors driving innovation and large-scale deployment. The top five companies collectively account for nearly 55% of the market, reflecting a competitive yet innovation-driven landscape. Leading players are focusing on strategic partnerships, joint ventures, and technology licensing agreements to strengthen their market positions. For instance, collaborations between turbine manufacturers and floating platform developers have improved installation efficiency by over 20% and reduced operational risks.

Innovation remains a key competitive factor, with companies investing heavily in high-capacity turbines exceeding 15 MW, advanced mooring systems, and AI-driven predictive maintenance technologies. Over 60% of major players are actively involved in pilot projects integrating floating wind with hydrogen production, highlighting a shift toward hybrid energy solutions. Mergers and acquisitions are also shaping the competitive environment, enabling companies to expand their technological capabilities and geographic presence.

Additionally, regional expansion strategies are prominent, with companies targeting emerging markets in Asia-Pacific and South America, where project pipelines exceed 25 GW combined. The competitive landscape is further influenced by government policies, financial incentives, and sustainability mandates, encouraging continuous innovation and long-term investment in floating offshore wind infrastructure.

Equinor

Siemens Gamesa Renewable Energy

Vestas Wind Systems

Principle Power

Mitsubishi Heavy Industries

General Electric Renewable Energy

SBM Offshore

Aker Solutions

Ideol

Hexicon

BW Ideol

Naval Energies

Technological innovation is at the core of the floating offshore wind power market, with advancements focused on improving efficiency, reducing operational complexity, and enabling large-scale deployment in deep-water environments. One of the most significant developments is the scaling of turbine capacity, with next-generation floating wind turbines exceeding 15 MW and rotor diameters surpassing 220 meters. These turbines can generate over 80 GWh annually per unit under optimal offshore conditions, increasing energy output by more than 30% compared to earlier models. Floating platform technologies are also evolving rapidly, with semi-submersible structures accounting for nearly 48% of installations due to their adaptability and stability across varying sea depths. Tension-leg platforms and spar-buoy systems are being optimized with advanced mooring solutions, reducing structural motion by up to 40% and improving turbine efficiency. The use of high-strength composite materials and corrosion-resistant alloys is extending platform lifespan beyond 25 years while lowering maintenance requirements by approximately 20%.

Digital transformation is another critical driver, with over 70% of operational floating wind projects integrating AI-based predictive maintenance and digital twin technologies. These systems enable real-time monitoring of turbine performance, reducing unplanned downtime by 25–35% and increasing asset utilization rates. Advanced sensors and edge computing are enhancing data processing capabilities, allowing for faster fault detection and automated performance adjustments. Grid integration technologies are also advancing, including high-voltage dynamic cables capable of operating at depths exceeding 1000 meters. Floating substations are being developed to support power transmission efficiency improvements of up to 15%. Additionally, hybrid systems combining floating wind with offshore hydrogen production and energy storage are gaining traction, improving energy utilization efficiency by nearly 30% and enabling multi-output offshore energy systems.

• In March 2025, Equinor advanced its Hywind Tampen floating wind project in Norway to full operational capacity, supplying renewable electricity to offshore oil and gas platforms. The project features 11 turbines with a total capacity of 88 MW, reducing offshore emissions by approximately 200,000 tonnes annually. Source: www.equinor.com

• In September 2024, Siemens Gamesa completed the installation of its SG 14-236 DD offshore wind turbine prototype, one of the largest in the industry, designed for floating applications. The turbine features a rotor diameter of 236 meters and is capable of generating over 30% more energy compared to previous models. Source: www.siemensgamesa.com

• In June 2025, Principle Power deployed its WindFloat® Atlantic floating platform enhancements, improving structural stability and reducing installation time by nearly 20%. The upgraded system incorporates advanced mooring configurations and digital monitoring tools to optimize performance in deep-water conditions. Source: www.principlepower.com

• In November 2024, Mitsubishi Heavy Industries initiated testing of a next-generation floating offshore wind turbine system in Japan, designed to withstand typhoon conditions. The system demonstrated a 30% increase in structural resilience and improved operational reliability in extreme weather environments. Source: www.mhi.com

The floating offshore wind power market report provides a comprehensive analysis of key industry segments, technologies, applications, and regional developments shaping the global landscape. The report covers multiple platform types, including semi-submersible systems, spar-buoy structures, and tension-leg platforms, which collectively account for 100% of floating wind installations, with semi-submersible platforms leading at approximately 48% share. It also evaluates turbine technologies exceeding 15 MW capacity, reflecting a growing trend toward high-efficiency power generation systems.

From an application perspective, the report examines utility-scale electricity generation, offshore oil and gas electrification, and green hydrogen production, with utilities contributing nearly 60% of total demand. Emerging applications such as offshore hydrogen production and hybrid energy systems are also analyzed, accounting for approximately 15% of new project pipelines. The report further explores end-user segments, including utilities, energy companies, and industrial operators, highlighting their respective adoption patterns and energy consumption requirements.

Geographically, the report provides in-depth coverage of Europe, North America, Asia-Pacific, South America, and the Middle East & Africa, with Europe leading global deployment at over 50% share and Asia-Pacific emerging as the fastest-growing region with more than 20 GW of planned capacity. Additionally, the report examines key technological trends such as AI-driven predictive maintenance, digital twin integration, advanced mooring systems, and floating substations, which are collectively improving operational efficiency by up to 30%.

The scope also includes analysis of investment trends, regulatory frameworks, supply chain dynamics, and infrastructure development, offering a holistic view of the market. It highlights niche segments such as offshore energy storage and wind-to-hydrogen integration, providing decision-makers with actionable insights into future growth opportunities and strategic planning considerations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

42.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Equinor, Siemens Gamesa Renewable Energy, Vestas Wind Systems, Principle Power, Mitsubishi Heavy Industries, General Electric Renewable Energy, SBM Offshore, Aker Solutions, Ideol, Hexicon, BW Ideol, Naval Energies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |