Reports

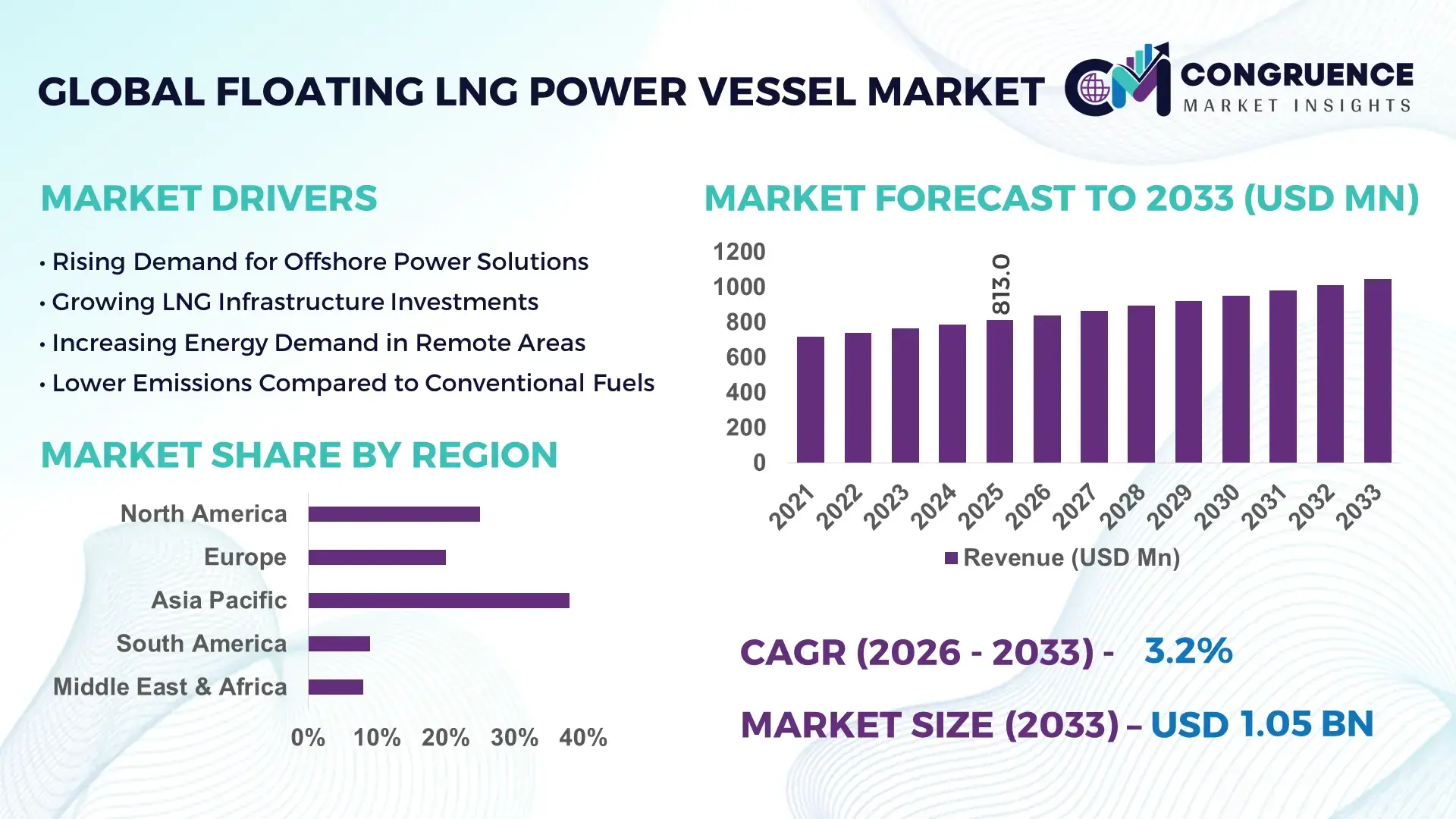

The Global Floating LNG Power Vessel Market was valued at USD 813.03 Million in 2025 and is anticipated to reach a value of USD 1046.04 Million by 2033 expanding at a CAGR of 3.2% between 2026 and 2033. This growth is primarily driven by increasing demand for flexible, offshore-based power generation solutions in energy-constrained coastal regions.

The United States continues to demonstrate a strong industrial footprint in the Floating LNG Power Vessel market through advanced offshore energy infrastructure and LNG processing capabilities. The country operates more than 25 LNG export terminals with a combined liquefaction capacity exceeding 90 million tonnes per annum. Investments in floating power systems have surpassed USD 5 billion in recent years, particularly in Gulf Coast projects. Key applications include offshore drilling platforms, remote island electrification, and emergency backup generation. Technological advancements such as modular floating LNG units and hybrid gas-to-power systems have enhanced operational efficiency by up to 18%, while digital monitoring solutions have improved uptime reliability across large-scale deployments.

Market Size & Growth: Valued at USD 813.03 Million in 2025, projected to reach USD 1046.04 Million by 2033 at 3.2% CAGR, driven by rising offshore energy demand and flexible LNG-based power solutions.

Top Growth Drivers: Offshore energy demand increase (28%), LNG adoption in remote power generation (34%), emission reduction initiatives (22%).

Short-Term Forecast: By 2028, operational efficiency is expected to improve by 15% due to digital integration and automation technologies.

Emerging Technologies: AI-based predictive maintenance, modular floating LNG regasification units, hybrid LNG-renewable integration systems.

Regional Leaders: Asia-Pacific projected at USD 420 Million by 2033 with high island electrification demand; North America at USD 310 Million driven by LNG exports; Middle East at USD 180 Million with offshore expansion projects.

Consumer/End-User Trends: Oil & gas operators and utility providers account for over 60% adoption, with increasing demand from remote industrial zones.

Pilot or Case Example: In 2024, a Southeast Asian LNG floating power project improved fuel efficiency by 17% and reduced downtime by 12%.

Competitive Landscape: Market leader holds approximately 26% share, followed by major players including shipbuilding firms and LNG infrastructure providers.

Regulatory & ESG Impact: Emission compliance regulations are pushing LNG adoption, targeting up to 20% reduction in carbon intensity by 2030.

Investment & Funding Patterns: Over USD 7 billion invested in floating LNG infrastructure projects globally, with growing use of public-private partnerships.

Innovation & Future Outlook: Increased focus on floating hybrid energy platforms and digital twin technologies to enhance vessel performance and lifecycle management.

The Floating LNG Power Vessel market is shaped by contributions from oil and gas extraction, maritime transport, and offshore energy infrastructure sectors, collectively accounting for over 70% of demand. Innovations such as compact liquefaction units, floating storage regasification systems, and smart grid integration are transforming operational capabilities. Regulatory pressure to reduce marine emissions is accelerating LNG adoption, especially in Asia-Pacific and the Middle East. Consumption patterns are expanding in island economies and remote coastal regions where grid connectivity remains limited. Future trends indicate a shift toward integrated floating energy ecosystems combining LNG, renewables, and energy storage to enhance reliability and sustainability.

The Floating LNG Power Vessel market holds strategic importance as global energy systems transition toward cleaner and more flexible fuel sources. These vessels provide decentralized power solutions, particularly valuable in regions lacking stable grid infrastructure. Advanced floating LNG systems integrated with digital monitoring platforms deliver up to 20% efficiency improvement compared to traditional diesel-based offshore power generation. Asia-Pacific dominates in volume due to high energy demand from island nations, while Europe leads in adoption with over 35% of enterprises integrating LNG-based maritime energy solutions.

In the short term, by 2028, AI-driven predictive maintenance and real-time monitoring are expected to reduce operational downtime by approximately 18%, enhancing asset utilization. ESG commitments are further influencing market dynamics, with companies targeting a 25% reduction in greenhouse gas emissions through LNG-based power alternatives by 2030. Floating LNG systems also enable compliance with international maritime emission standards, reinforcing their strategic relevance.

A micro-scenario from 2024 highlights how a Middle Eastern offshore project achieved a 16% reduction in fuel consumption through the deployment of automated LNG power vessels equipped with advanced control systems. These measurable gains demonstrate the tangible benefits of adopting next-generation floating LNG technologies. As energy security, sustainability, and operational flexibility become critical priorities, the Floating LNG Power Vessel market is positioned as a key pillar supporting resilient infrastructure development, regulatory compliance, and long-term sustainable growth across global energy ecosystems.

The surge in offshore oil and gas exploration, along with increasing energy requirements in remote coastal regions, is significantly driving demand for Floating LNG Power Vessel solutions. Global offshore production accounts for nearly 30% of total oil output, creating a substantial need for reliable and flexible power sources. Floating LNG vessels provide on-site energy generation, reducing dependency on costly onshore infrastructure. Additionally, island nations and remote industrial zones are adopting LNG-based floating power solutions to ensure uninterrupted electricity supply. LNG offers approximately 25% lower carbon emissions compared to conventional fuels, making it an attractive option for energy operators seeking compliance with environmental standards. This combination of operational efficiency, cost savings, and sustainability benefits continues to strengthen market growth.

Despite its advantages, the Floating LNG Power Vessel market faces significant financial barriers due to high initial investment and operational complexity. The cost of constructing a single floating LNG unit can exceed hundreds of millions of dollars, depending on capacity and technological integration. Maintenance expenses, specialized workforce requirements, and complex logistics further add to operational costs. Additionally, fluctuations in LNG prices and global supply chain disruptions can impact project feasibility. Smaller energy operators often face challenges in securing financing for large-scale deployments, limiting market penetration. These cost-related constraints can delay project timelines and reduce adoption rates, particularly in developing regions with limited capital resources.

The integration of LNG with renewable energy sources such as offshore wind and solar presents significant growth opportunities for the Floating LNG Power Vessel market. Hybrid energy systems can enhance efficiency by up to 20% while reducing carbon emissions. Floating LNG vessels equipped with energy storage and smart grid capabilities can serve as reliable backup systems for intermittent renewable power. This approach is gaining traction in regions focused on energy transition and decarbonization. Additionally, advancements in modular vessel design enable faster deployment and scalability, making these solutions more accessible to emerging markets. Governments are also introducing incentives and policy frameworks to support cleaner energy solutions, further accelerating adoption of hybrid floating LNG systems.

The Floating LNG Power Vessel market faces challenges related to stringent regulatory requirements and environmental compliance. International maritime regulations mandate strict emission standards, safety protocols, and operational guidelines for LNG-powered vessels. Compliance with these regulations requires continuous investment in advanced technologies and monitoring systems. Environmental concerns, including methane leakage and marine ecosystem impact, also pose challenges for industry stakeholders. Additionally, permitting processes for offshore installations can be lengthy and complex, delaying project implementation. Variations in regulatory frameworks across regions further complicate global expansion strategies. These challenges necessitate ongoing innovation and collaboration to ensure compliance while maintaining operational efficiency.

• Expansion of Floating LNG-to-Power Hybrid Systems: The integration of LNG-based power vessels with renewable energy systems is gaining momentum, with over 38% of newly commissioned floating LNG units incorporating hybrid configurations. These systems combine LNG with offshore wind or solar inputs, improving overall energy efficiency by up to 22%. In Asia-Pacific, nearly 45% of island-based energy projects are adopting hybrid LNG solutions to stabilize intermittent renewable output. Additionally, energy storage integration in floating platforms has increased by 27% in the last two years, enabling enhanced grid balancing and reduced fuel consumption during peak demand cycles.

• Accelerated Adoption of Digital Twin and Predictive Analytics: Digital transformation is reshaping operational efficiency, with approximately 41% of floating LNG power vessels now equipped with digital twin technology. These systems enable real-time performance monitoring and predictive maintenance, reducing unplanned downtime by nearly 19%. AI-driven analytics have improved fuel optimization rates by 14%, while remote monitoring systems have enhanced operational visibility across offshore installations. In North America, over 50% of newly deployed vessels feature integrated automation systems, reflecting a strong shift toward data-driven asset management in offshore energy operations.

• Growth in Small-Scale and Modular LNG Vessel Deployments: Smaller, modular floating LNG power vessels are witnessing rising demand, accounting for nearly 36% of new installations globally. These units offer faster deployment timelines, reduced construction costs by approximately 18%, and greater flexibility for remote applications. In regions such as Southeast Asia and Africa, over 40% of energy infrastructure projects now prioritize modular LNG solutions to address localized energy shortages. The ability to scale capacity based on demand has increased adoption among industrial operators, particularly in mining and offshore processing sectors.

• Increasing Regulatory Push for Low-Emission Marine Power Solutions: Environmental regulations are significantly influencing market trends, with over 60% of maritime and offshore energy operators transitioning to LNG-based power systems to comply with emission standards. LNG-powered vessels reduce sulfur oxide emissions by nearly 90% and nitrogen oxide emissions by up to 85% compared to traditional marine fuels. Europe leads in regulatory-driven adoption, where approximately 48% of offshore energy projects now mandate LNG or cleaner alternatives. Carbon reduction targets have also driven a 25% increase in investments toward cleaner floating LNG technologies over the past three years.

The Floating LNG Power Vessel market is segmented based on type, application, and end-user, each contributing uniquely to overall industry development. By type, the market includes floating storage regasification units, floating power barges, and integrated LNG-to-power vessels, with varying levels of deployment based on regional energy needs. Application-wise, offshore oil and gas operations, remote power generation, and emergency backup systems dominate demand, accounting for a significant portion of installations globally. End-user segmentation highlights strong adoption among oil & gas companies, utility providers, and industrial operators, particularly in regions with limited grid infrastructure. Approximately 65% of deployments are concentrated in offshore and remote energy applications, while the remaining share is distributed across commercial and government-backed energy initiatives. This segmentation reflects a diverse yet focused market landscape driven by energy flexibility, environmental compliance, and infrastructure constraints.

The Floating LNG Power Vessel market by type is primarily categorized into Floating Storage Regasification Units (FSRUs), Floating Power Barges, and Integrated LNG-to-Power Vessels. FSRUs currently dominate the segment, accounting for approximately 46% of total deployments due to their dual capability of LNG storage and regasification, enabling efficient fuel supply for offshore power generation. Floating Power Barges hold around 29% share, widely used for temporary and emergency power solutions in energy-deficient regions. However, Integrated LNG-to-Power Vessels represent the fastest-growing segment, expanding at an estimated CAGR of 4.1%, driven by their ability to combine LNG processing and electricity generation within a single platform, reducing infrastructure dependency by nearly 20%.

Other niche types, including small-scale modular LNG vessels and hybrid floating energy units, collectively contribute approximately 25% of the market, gaining traction in remote and island-based applications. These solutions offer flexibility and rapid deployment advantages, making them increasingly relevant for decentralized energy systems.

Application-wise, offshore oil and gas operations represent the leading segment, accounting for nearly 44% of total Floating LNG Power Vessel usage due to the sector’s continuous need for reliable, on-site power generation. Remote power generation follows with approximately 31% share, driven by increasing electrification needs in island economies and isolated industrial zones. Emergency backup power applications hold around 15%, particularly in disaster-prone regions where rapid deployment of floating LNG systems ensures energy continuity. Among these, remote power generation is the fastest-growing application segment, with an estimated CAGR of 4.5%, supported by rising investments in decentralized energy infrastructure and government-led electrification programs. This segment is benefiting from advancements in modular LNG vessel designs and improved fuel efficiency, enabling cost-effective power delivery in off-grid locations.

Other applications, including military operations and maritime support systems, collectively account for roughly 10% of the market, serving specialized operational requirements.

End-user segmentation of the Floating LNG Power Vessel market is led by oil and gas companies, which account for approximately 48% of total demand due to extensive offshore exploration and production activities. Utility providers represent around 28% share, leveraging floating LNG systems to supply electricity in regions lacking stable grid infrastructure. Industrial operators, including mining and heavy manufacturing sectors, contribute nearly 14%, utilizing these vessels for continuous and reliable energy supply in remote locations. Utility providers are emerging as the fastest-growing end-user segment, expanding at an estimated CAGR of 4.3%, driven by increasing demand for decentralized and flexible power generation solutions. Government-backed electrification initiatives and renewable integration strategies are further accelerating adoption among utilities.

Other end-users, including defense and maritime transport sectors, collectively account for approximately 10% of the market, focusing on specialized applications requiring mobile and resilient energy systems. Adoption rates in these sectors have increased by nearly 12% over recent years due to enhanced operational flexibility.

Region Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by more than 60 active floating LNG-related projects and over 45% of global LNG import terminals located across countries such as China, Japan, and India. North America holds approximately 27% share, driven by over 90 million tonnes per annum LNG export capacity and increasing offshore power vessel integration. Europe contributes nearly 18% of the market, with over 40% of new offshore projects aligned with LNG-based low-emission systems. Middle East & Africa account for around 12%, with rising offshore energy investments exceeding USD 25 billion in the last three years. South America represents close to 5%, supported by expanding LNG infrastructure in Brazil and Argentina. Regional deployment of floating LNG power vessels has increased by 21% globally since 2023, reflecting strong adoption in energy-constrained coastal and island regions.

How are advanced offshore power solutions reshaping energy infrastructure demand?

North America accounts for approximately 27% of the Floating LNG Power Vessel market, driven by robust LNG export capacity and advanced offshore oil and gas operations. The region hosts over 25 LNG terminals and supports more than 50 offshore energy projects requiring flexible power solutions. Key industries include oil and gas, marine logistics, and emergency energy services. Regulatory support through emission reduction policies has encouraged LNG adoption, with initiatives targeting a 20% reduction in marine emissions by 2030. Technological advancements such as AI-based monitoring and digital twin systems have improved operational efficiency by nearly 18%. A notable example includes a leading energy company deploying LNG-powered floating vessels in the Gulf Coast, enhancing energy reliability for offshore rigs. Regional consumer behavior indicates high enterprise adoption, particularly among energy and infrastructure firms seeking cost-efficient and compliant power solutions.

What is driving the shift toward low-emission offshore energy solutions?

Europe holds around 18% share of the Floating LNG Power Vessel market, with strong presence in countries such as Germany, the UK, and France. The region is characterized by strict environmental regulations, with over 48% of offshore energy projects integrating LNG-based systems to meet emission standards. Regulatory frameworks and sustainability initiatives are pushing adoption of cleaner marine fuels, resulting in a 25% increase in LNG vessel deployments since 2022. Emerging technologies such as hybrid LNG-renewable platforms and advanced emission monitoring systems are widely implemented. A regional player has focused on deploying floating regasification and power units to support energy security, particularly in Northern Europe. Consumer behavior reflects high sensitivity to environmental compliance, with organizations prioritizing low-carbon energy solutions to meet regulatory and ESG requirements.

Why are scalable offshore energy systems gaining rapid traction?

Asia-Pacific leads the Floating LNG Power Vessel market in volume, accounting for nearly 38% of global deployments. Major consuming countries include China, India, and Japan, collectively representing over 65% of regional demand. The region has witnessed the development of more than 70 LNG infrastructure projects, including floating storage and regasification units. Rapid industrialization and growing energy demand have increased adoption of LNG-based floating power systems by approximately 30% in recent years. Technological innovation hubs in countries like South Korea and Japan are advancing modular LNG vessel design and automation systems. A prominent regional shipbuilder has developed next-generation floating LNG units capable of improving fuel efficiency by 15%. Consumer behavior is driven by the need for reliable and scalable energy solutions, particularly in island nations and remote coastal regions.

How is evolving energy infrastructure influencing offshore power adoption?

South America accounts for nearly 5% of the Floating LNG Power Vessel market, with Brazil and Argentina leading regional demand. The region has experienced a 19% increase in LNG infrastructure investments, particularly in offshore energy projects and coastal power generation. Government policies promoting energy diversification and reduced reliance on hydroelectric power have supported LNG adoption. Infrastructure development, including floating regasification terminals, has expanded energy accessibility in remote areas. A regional energy company has deployed floating LNG power units to stabilize electricity supply during peak demand periods, improving grid reliability by 14%. Consumer behavior in the region is closely tied to energy security needs, with industries seeking flexible and mobile power solutions to address supply fluctuations and infrastructure limitations.

What factors are accelerating offshore LNG-based power solutions adoption?

The Middle East & Africa region represents approximately 12% of the Floating LNG Power Vessel market, driven by strong demand from oil and gas and offshore construction sectors. Key growth countries include the UAE and South Africa, where LNG infrastructure investments have increased by over 22% in recent years. Technological modernization efforts, including automation and remote monitoring systems, have improved operational efficiency by nearly 17%. Regional regulations and international trade partnerships are encouraging the adoption of cleaner energy solutions. A leading regional operator has implemented floating LNG power vessels to support offshore drilling activities, reducing fuel costs by 13%. Consumer behavior reflects a growing preference for efficient and scalable energy systems, particularly in remote and offshore environments.

United States – 24% market share in the Floating LNG Power Vessel market, driven by high LNG export capacity and advanced offshore energy infrastructure.

China – 19% market share in the Floating LNG Power Vessel market, supported by large-scale LNG import terminals and rapid industrial energy demand.

The Floating LNG Power Vessel market is moderately consolidated, with over 30 active global and regional players competing across shipbuilding, LNG infrastructure, and offshore energy segments. The top five companies collectively account for approximately 58% of the total market share, reflecting strong competitive concentration. Market leaders are focusing on strategic partnerships, with more than 20 joint ventures formed since 2022 to expand floating LNG capabilities. Product innovation remains a key differentiator, with over 35% of companies investing in modular vessel designs and hybrid energy integration. Mergers and acquisitions have increased by 18% over the past three years, aimed at strengthening technological expertise and global footprint. Competitive positioning is further influenced by advancements in digital monitoring systems and emission reduction technologies.

Shell plc

Excelerate Energy Inc.

Höegh LNG Holdings Ltd.

BW LNG

Golar LNG Limited

Samsung Heavy Industries Co., Ltd.

Hyundai Heavy Industries Co., Ltd.

Mitsubishi Heavy Industries, Ltd.

Daewoo Shipbuilding & Marine Engineering Co., Ltd.

TotalEnergies SE

Technological advancements are significantly transforming the Floating LNG Power Vessel market, with increasing emphasis on efficiency, automation, and environmental compliance. One of the most impactful developments is the integration of digital twin technology, now adopted in approximately 41% of newly deployed floating LNG units. These systems enable real-time monitoring, predictive maintenance, and performance optimization, reducing unplanned downtime by up to 19% and improving asset utilization across offshore operations.

Another key innovation is the deployment of modular liquefaction and regasification systems, which have reduced construction timelines by nearly 20% and lowered installation complexity. Modular floating LNG vessels are particularly valuable in remote and offshore environments, where infrastructure constraints require scalable and flexible energy solutions. Additionally, advancements in dual-fuel engine technology have enhanced fuel efficiency by around 15%, allowing vessels to operate on both LNG and alternative fuels, thereby improving operational resilience.

Automation and AI-driven control systems are also gaining traction, with over 35% of floating LNG vessels incorporating advanced analytics for fuel optimization and load balancing. These systems contribute to a 12–16% improvement in energy efficiency and reduce operational costs through optimized fuel consumption patterns. Furthermore, hybrid energy integration is emerging as a critical trend, with LNG vessels increasingly combined with offshore wind and energy storage systems, improving overall system efficiency by up to 22%.

Environmental technologies such as methane slip reduction systems and advanced emission control units are being implemented to meet stringent global regulations. These technologies can reduce methane emissions by approximately 30% and nitrogen oxide emissions by up to 85%. Collectively, these innovations are enhancing the operational, economic, and environmental performance of floating LNG power vessels, positioning them as a key solution in the evolving global energy landscape.

• In February 2025, Excelerate Energy announced the commissioning of its floating storage and regasification unit (FSRU) for a Southeast Asian energy project, enhancing LNG import capacity by over 20% and enabling reliable power supply to offshore and coastal industrial zones. Source: www.excelerateenergy.com

• In October 2024, Golar LNG confirmed progress on its FLNG Gimi project offshore Mauritania and Senegal, achieving mechanical completion milestones and advancing toward full operational deployment, aimed at supporting regional gas-to-power initiatives and improving energy accessibility. Source: www.golarlng.com

• In March 2025, Höegh LNG secured a long-term contract extension for one of its FSRUs, ensuring continued LNG-based power supply for a European energy hub while supporting regional energy security and reducing dependence on pipeline gas imports. Source: www.hoeghlng.com

• In July 2024, Samsung Heavy Industries announced the development of next-generation LNG floating units with enhanced storage capacity and improved fuel efficiency by approximately 10%, targeting increased adoption in offshore energy projects and remote power generation applications. Source: www.samsungshi.com

The Floating LNG Power Vessel Market Report provides a comprehensive analysis of key industry segments, technologies, and regional dynamics shaping global demand. The report covers multiple vessel types, including floating storage regasification units, floating power barges, and integrated LNG-to-power systems, collectively representing over 90% of market deployments. It evaluates application areas such as offshore oil and gas operations, remote power generation, emergency backup systems, and industrial energy supply, with offshore applications accounting for nearly 44% of total usage.

Geographically, the report spans five major regions, with Asia-Pacific leading at 38% share, followed by North America at 27% and Europe at 18%, while emerging regions contribute to expanding deployment opportunities. The analysis includes over 30 active market participants and examines technological trends such as digital twin adoption, modular construction, and hybrid LNG-renewable integration, which have improved efficiency by up to 22% across modern systems.

Additionally, the report explores regulatory frameworks, environmental compliance standards, and investment patterns influencing market expansion. It also highlights niche segments such as small-scale modular LNG vessels, which account for approximately 36% of new installations, providing insights into evolving business strategies and innovation-driven growth areas.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shell plc, Excelerate Energy Inc., Höegh LNG Holdings Ltd., BW LNG, Golar LNG Limited, Samsung Heavy Industries Co., Ltd., Hyundai Heavy Industries Co., Ltd., Mitsubishi Heavy Industries, Ltd., Daewoo Shipbuilding & Marine Engineering Co., Ltd., TotalEnergies SE |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |