Reports

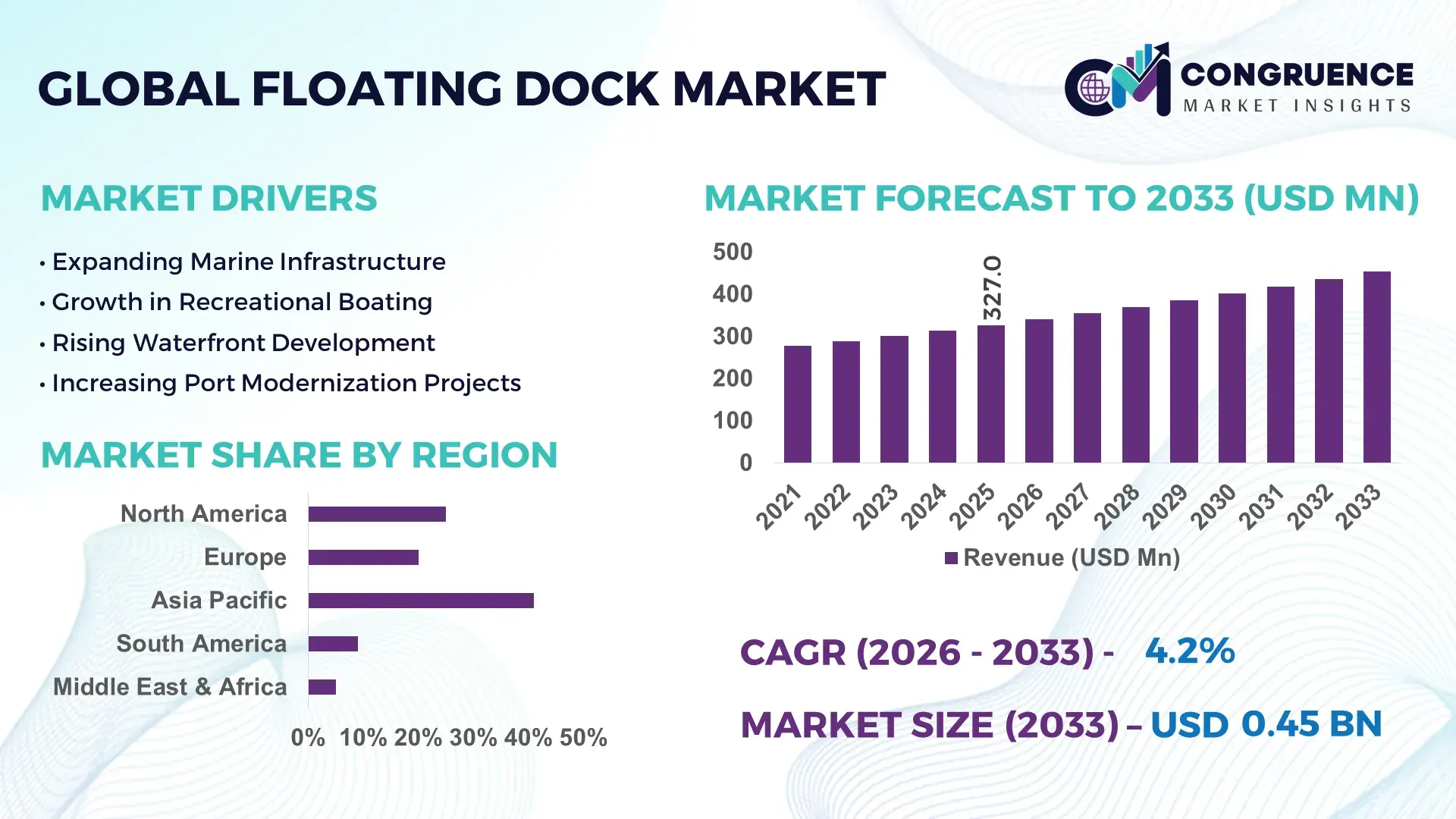

The Global Floating Dock Market was valued at USD 327 Million in 2025 and is anticipated to reach a value of USD 454.45 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033.

Growth is being accelerated by rising investments in modular marina infrastructure, offshore vessel maintenance facilities, and defense-grade floating dock systems, with automated ballast control technologies improving docking efficiency by nearly 18% compared to conventional systems. Between 2024 and 2026, Red Sea shipping disruptions, stricter coastal infrastructure regulations, and expanding naval modernization programs across Asia-Pacific and Europe reshaped procurement priorities toward durable, corrosion-resistant floating dock platforms with faster deployment cycles.

China remains the dominant country in the global floating dock market, accounting for approximately 31% of global production capacity in 2026, supported by aggressive shipbuilding expansion, port modernization spending exceeding USD 14 billion, and strong integration of smart monitoring systems across commercial dockyards. Over 45% of newly commissioned floating dock installations in East Asia now incorporate IoT-enabled structural monitoring and automated load-balancing systems, compared to below 20% adoption in 2021. The country’s large-scale maritime logistics, offshore energy servicing, and naval infrastructure programs provide a substantial competitive advantage over smaller regional manufacturing hubs in Southeast Asia and Europe.

Market participants prioritizing lightweight composite materials, rapid-installation dock designs, and digitally monitored maintenance ecosystems are positioned to secure higher-value contracts across commercial marine, defense, and offshore energy applications.

Market Size & Growth: USD 327 Million in 2025 rising to USD 454.45 Million by 2033 at 4.2% CAGR, driven by smart marina expansion and naval infrastructure modernization.

Top Growth Drivers: Automated dock systems improve operational efficiency by 18%, corrosion-resistant materials extend lifecycle by 22%, and modular deployment cuts installation time by 30%.

Short-Term Forecast: By 2027, advanced floating dock operators are projected to reduce maintenance downtime by 16% through predictive monitoring integration.

Emerging Technologies: AI-enabled ballast systems, composite floating platforms, and IoT-based structural diagnostics are integrated in over 41% of new projects globally.

Regional Leaders: Asia-Pacific exceeds USD 170 Million with shipyard expansion, Europe crosses USD 108 Million through marina redevelopment, and North America surpasses USD 92 Million via defense dock upgrades.

Consumer/End-User Trends: Nearly 52% of commercial marina operators prioritize modular floating docks for scalability and lower operational disruption.

Pilot/Case Example: In 2025, a Scandinavian smart-port deployment improved docking turnaround efficiency by 21% using automated stabilization systems.

Competitive Landscape: Top manufacturers collectively control nearly 38% market share, with competition centered on durability, rapid assembly, and digital maintenance platforms.

Regulatory & ESG Impact: Advanced recycled-polymer dock systems reduce maintenance-related emissions by 14% while supporting stricter coastal sustainability mandates.

Investment & Funding: More than USD 1.2 billion in global marine infrastructure investments supported floating dock expansion projects between 2024 and 2026.

Innovation & Future Outlook: Hybrid floating dock ecosystems integrating renewable shore-power connectivity and autonomous vessel support are reshaping high-growth maritime infrastructure strategies.

Commercial marine operations contribute nearly 46% of global floating dock demand, followed by defense and naval infrastructure at approximately 28%, reflecting sustained investment in vessel servicing capacity and port modernization. Advanced composite dock systems with IoT-enabled monitoring now represent over 35% of new installations, improving structural lifespan and reducing maintenance cycles. Asia-Pacific continues leading procurement activity due to shipyard expansion and coastal logistics upgrades, while Europe benefits from stricter waterfront sustainability regulations. Increasing localization of marine infrastructure supply chains and rapid adoption of smart docking ecosystems are setting the foundation for next-generation strategic maritime development.

The floating dock market is rapidly transforming into a strategic maritime infrastructure segment as ports, naval facilities, offshore energy operators, and commercial marinas prioritize flexible, scalable docking ecosystems. Accelerating vessel traffic, rising coastal redevelopment investments, and growing defense modernization programs are intensifying competition among manufacturers focused on advanced modular dock systems. Between 2024 and 2026, supply chain restructuring across Asian shipbuilding corridors and stricter coastal sustainability regulations forced operators to shift toward lightweight composite docks and digitally monitored maintenance platforms. Smart floating dock installations increased by 34% globally in 2025 as operators optimized operational uptime and reduced lifecycle maintenance exposure.

AI-enabled ballast stabilization systems improve docking efficiency by 22% while reducing maintenance cost by 17% compared to legacy hydraulic platforms. Asia-Pacific leads in deployment volume due to large-scale shipyard expansion, while Northern Europe leads in innovation adoption with nearly 48% integration of automated structural monitoring systems. Over the next three years, predictive maintenance integration is projected to reduce operational downtime by 19% across commercial marine infrastructure. ESG-driven floating dock designs using recycled polymer composites lower corrosion-related maintenance requirements by 14%, creating both compliance advantages and long-term operating savings.

In 2025, a modular floating marina redevelopment project in the Middle East improved berth utilization efficiency by 24% through sensor-enabled dock management systems. Capital allocation is increasingly shifting toward smart-port partnerships, offshore servicing hubs, and rapid-installation dock technologies as manufacturers expand regional assembly capacity and digital service capabilities. Companies optimizing automation, sustainability performance, and modular scalability are securing stronger positioning across high-value maritime infrastructure contracts and long-term coastal development programs.

Global maritime infrastructure modernization is accelerating floating dock demand as ports, naval operators, and marina developers prioritize scalable docking systems with lower installation timelines and higher operational flexibility. Automated ballast management and IoT-enabled structural monitoring technologies improve dock efficiency by 18% while reducing maintenance interruptions by 15%. More than 42% of newly developed waterfront projects in 2025 integrated modular floating dock platforms due to faster deployment advantages over fixed concrete structures. Red Sea shipping disruptions and expanding Indo-Pacific naval activity forced governments and logistics operators to accelerate coastal infrastructure investments. In response, manufacturers are expanding composite-material production capacity, forming regional engineering partnerships, and investing in digitally optimized dock systems to strengthen project execution speed, durability performance, and long-term infrastructure competitiveness.

Rising raw material volatility and uneven coastal infrastructure readiness are constraining large-scale floating dock deployment across several emerging marine economies. Composite polymers and marine-grade aluminum prices increased by nearly 19% between 2024 and 2025, while specialized corrosion-resistant steel procurement lead times expanded by 27%, directly pressuring project margins and installation schedules. Limited deepwater servicing infrastructure across parts of Africa and Southeast Asia is restricting deployment efficiency for larger modular dock systems. These constraints are increasing capital exposure and slowing multi-site expansion strategies for marina operators and offshore maintenance providers. To reduce operational risk, companies are diversifying supplier networks, securing long-term material contracts, and accelerating adoption of hybrid composite alternatives that improve durability while lowering dependence on volatile metal-intensive manufacturing cycles.

Next-generation floating dock ecosystems are creating high-value opportunities across commercial marinas, offshore wind servicing, and defense logistics infrastructure. Smart dock platforms integrated with AI-driven maintenance analytics improve operational efficiency by 21% and reduce emergency repair incidents by nearly 16%, strengthening long-term asset performance. More than 38% of planned waterfront redevelopment projects in emerging coastal economies now prioritize modular floating infrastructure due to lower civil engineering requirements and faster deployment capabilities. The expansion of offshore renewable energy servicing corridors is generating new demand pockets for heavy-duty floating maintenance platforms. Companies are responding through targeted R&D investment, regional manufacturing expansion, and integrated digital service ecosystems that combine predictive monitoring, energy-efficient materials, and automated docking optimization to secure future infrastructure dominance and recurring service-based revenue streams.

Execution complexity, environmental exposure, and long-term maintenance reliability remain critical challenges reshaping competitive positioning in the floating dock market. Severe coastal weather events increased floating infrastructure repair costs by approximately 18% in 2025, while inconsistent marine engineering standards across regions delayed nearly 23% of cross-border dock projects. High-performance automated systems also require specialized technical servicing capabilities, creating operational bottlenecks for smaller infrastructure operators. Increasing environmental compliance pressure is forcing manufacturers to redesign anchoring systems, buoyancy structures, and corrosion-control technologies without compromising deployment speed or structural durability. Companies unable to scale advanced engineering support, localized manufacturing partnerships, and predictive maintenance ecosystems face growing pressure from integrated marine infrastructure providers that are optimizing lifecycle reliability, regulatory alignment, and long-term operational resilience simultaneously.

34% increase in modular dock deployments is reshaping installation timelines and operational flexibility. Marina developers and commercial waterfront operators are replacing fixed infrastructure with modular floating systems that reduce installation time by 28% and lower site disruption by 19%. Companies are restructuring manufacturing around pre-engineered dock components and regional assembly hubs to accelerate project execution amid ongoing coastal redevelopment pressure and labor shortages.

41% adoption of IoT-enabled monitoring systems is redefining dock maintenance operations. Smart sensors tracking buoyancy balance, corrosion exposure, and structural stress reduced unscheduled maintenance incidents by 17% across newly upgraded marine facilities in 2025. Operators are integrating predictive maintenance dashboards into port management workflows, while manufacturers are forming software partnerships to optimize long-term service contracts and reduce lifecycle maintenance costs.

26% growth in recycled composite dock usage is shifting material procurement strategies globally. Rising marine-grade steel volatility and tightening environmental regulations are forcing manufacturers to expand polymer-based dock production with lighter, corrosion-resistant structures. Composite platforms now extend average maintenance cycles by 21% compared to conventional metal-intensive systems, creating a non-obvious advantage in regions facing aggressive saltwater degradation and escalating repair labor costs.

31% rise in defense-linked floating infrastructure projects is accelerating specialized dock customization. Naval modernization programs and offshore security expansion are increasing demand for high-load floating maintenance platforms with automated stabilization capabilities. Companies are scaling hybrid dock configurations supporting rapid vessel turnaround, while strategic partnerships between marine engineering firms and defense contractors are optimizing deployment speed by nearly 18% across critical coastal infrastructure networks.

The floating dock market is segmented by type, application, and end-user, with demand increasingly shifting toward modular and digitally monitored infrastructure systems. Metal and modular docks collectively account for nearly 58% of installations due to durability and deployment flexibility, while commercial ports and marina operations represent over 49% of application demand driven by vessel traffic expansion and waterfront redevelopment. Marine industry and government-linked projects continue dominating procurement activity, although tourism-focused waterfront investments are accelerating adoption of lightweight composite dock systems. Demand distribution is increasingly influenced by maintenance efficiency, installation speed, and sustainability compliance, forcing manufacturers to reposition product portfolios toward scalable, low-maintenance floating infrastructure ecosystems.

Metal floating docks dominate the market with approximately 34% share due to superior structural strength, heavy-load handling capability, and long operational lifespan across commercial ports and defense-linked marine infrastructure. Their integration advantage in high-traffic docking environments continues reinforcing demand despite rising material costs. Modular floating docks are the fastest-growing segment, expanding by nearly 16% annually as marina developers and waterfront operators prioritize rapid deployment, scalability, and reduced installation disruption. Compared to traditional concrete systems, modular platforms lower installation timelines by approximately 28% while improving expansion flexibility for multi-site marine projects.

Concrete docks maintain strategic relevance in permanent waterfront infrastructure due to stability and weather resistance, while plastic and wood docks collectively account for nearly 24% of installations, primarily serving recreational marinas and residential waterfront applications. Wood demand is gradually declining because of higher maintenance exposure, whereas advanced plastic composite systems are gaining traction through corrosion resistance and lower lifecycle servicing costs. Companies are increasingly expanding modular and hybrid composite production capacity while reducing dependency on maintenance-intensive legacy materials. Investment focus is clearly shifting toward scalable, lightweight, digitally adaptable dock systems capable of supporting long-term marine infrastructure modernization.

“According to a 2025 report by the International Marina Institute, modular floating dock systems were adopted by over 43% of newly developed marina projects, resulting in nearly 22% faster installation efficiency and lower long-term maintenance exposure, reinforcing their growing strategic importance.”

Commercial ports lead the floating dock market with approximately 32% share as expanding cargo throughput, vessel servicing demand, and port modernization programs intensify infrastructure utilization. High operational dependency on scalable docking systems continues concentrating investment within cargo handling and marine logistics facilities. Ship maintenance is the fastest-growing application segment, advancing by nearly 15% due to increasing offshore vessel repair activity and naval fleet servicing requirements. Compared to mature marina operations focused on leisure infrastructure, ship maintenance applications require higher-load floating systems with automated stabilization and integrated maintenance support capabilities.

Marina operations and boat mooring collectively represent nearly 37% of application demand, driven by waterfront redevelopment and premium coastal tourism expansion. Ferry services are also gaining deployment traction as regional governments prioritize flexible transport infrastructure supporting coastal connectivity projects. Waterfront recreation remains strategically relevant for urban waterfront revitalization programs integrating floating leisure ecosystems and modular docking expansion. Companies are repositioning product portfolios toward application-specific dock configurations, including heavy-duty commercial platforms and digitally monitored marina systems. Demand is increasingly shifting toward infrastructure capable of reducing turnaround delays, improving berth utilization, and supporting faster operational scaling across marine transportation networks.

“According to a 2025 report by the International Association of Ports and Harbors, floating dock systems for ship maintenance were deployed across more than 620 commercial marine facilities, improving vessel servicing efficiency by 19%, highlighting their rapid operational adoption.”

The marine industry remains the dominant end-user segment with approximately 36% market share due to continuous dependence on floating infrastructure for vessel docking, servicing, logistics support, and offshore operations. High-frequency utilization and infrastructure modernization requirements continue concentrating procurement activity within commercial marine ecosystems. The defense sector is the fastest-growing end-user group, expanding by nearly 17% as naval modernization programs and coastal security investments accelerate deployment of specialized floating maintenance platforms. Compared to residential waterfront owners focused on low-maintenance recreational docks, defense buyers prioritize high-load durability, rapid deployment capability, and integrated stabilization technologies.

Commercial ports and government authorities collectively account for nearly 33% of total demand as port expansion projects and coastal redevelopment initiatives intensify globally. Tourism and hospitality operators are increasingly adopting modular floating systems supporting waterfront recreation, marina hospitality, and premium docking experiences. Companies are strategically targeting these segments through customized dock configurations, long-term maintenance partnerships, and region-specific engineering support models. Procurement behavior is shifting toward scalable, digitally monitored dock systems capable of reducing maintenance cycles and improving operational resilience, forcing manufacturers to prioritize modular engineering, sustainability compliance, and lifecycle service integration to capture future demand concentration.

“According to a 2025 report by the International Maritime Organization, adoption among defense sector operators increased by 21%, with over 340 naval infrastructure facilities implementing advanced floating dock systems, leading to nearly 18% improvement in vessel maintenance efficiency, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Asia-Pacific dominates global floating dock demand through large-scale shipbuilding activity, coastal infrastructure expansion, and cost-efficient manufacturing ecosystems, while Europe captures nearly 27% share through advanced marina modernization and sustainability-driven dock replacement programs. North America maintains approximately 22% of market demand, supported by defense infrastructure upgrades and smart-port integration initiatives. The Middle East & Africa region is accelerating deployment through offshore energy servicing and waterfront megaproject investments, with floating marina installations rising by 24% in 2025. Supply chain regionalization and stricter coastal resilience policies are reshaping procurement strategies globally. Companies are increasingly focusing on Asia-Pacific for manufacturing scale, Europe for innovation-led engineering, and the Middle East for high-value infrastructure expansion opportunities.

North America represents nearly 22% of global floating dock demand, driven by marina redevelopment, naval modernization programs, and expanding coastal logistics infrastructure. Commercial ports and defense-linked marine facilities account for over 48% of regional deployment activity as operators prioritize operational resilience and faster vessel servicing capabilities. Stricter coastal infrastructure standards and rising maintenance costs are accelerating adoption of modular composite dock systems that reduce lifecycle servicing requirements by approximately 16%. Smart dock monitoring integration increased by 29% across newly upgraded facilities in 2025, reflecting rapid operational digitization. Manufacturers are expanding localized assembly operations and engineering partnerships to shorten delivery cycles. Enterprise buyers increasingly prioritize scalability, predictive maintenance capability, and compliance-ready dock platforms, reinforcing North America as a strategic region for premium infrastructure investment and technology-led deployment expansion.

Europe accounts for approximately 27% of the floating dock market, led by waterfront modernization projects across Germany, Norway, and the Netherlands. Stringent coastal sustainability regulations and marine emission reduction mandates are forcing operators to replace aging steel-intensive infrastructure with recyclable composite dock systems that lower corrosion-related maintenance by nearly 21%. More than 44% of newly commissioned marina projects in 2025 integrated digitally monitored floating platforms to improve compliance tracking and operational efficiency. Enterprise procurement behavior remains strongly quality-focused, with buyers prioritizing long-lifecycle infrastructure and ESG-aligned engineering standards over low-cost alternatives. Regional manufacturers are accelerating investment in lightweight modular dock technologies and energy-efficient fabrication methods, making Europe a critical market for innovation-driven adaptation and premium marine infrastructure differentiation.

Asia-Pacific leads the floating dock market with nearly 41% global demand concentration, supported by large-scale shipbuilding capacity, port modernization programs, and rapidly expanding waterfront infrastructure projects across China, South Korea, and Singapore. The region benefits from integrated marine supply chains and cost-efficient manufacturing ecosystems capable of reducing dock production timelines by approximately 24%. More than 46% of newly deployed floating dock systems in 2025 incorporated modular configurations supporting faster installation and scalable expansion. Manufacturers are increasingly localizing advanced composite production and digital monitoring integration to support mass deployment requirements. Enterprise buyers prioritize cost efficiency, rapid execution, and infrastructure scalability, forcing suppliers to optimize regional assembly networks and engineering capabilities. Asia-Pacific remains strategically critical for manufacturing scale, export expansion, and high-volume commercial marine infrastructure deployment.

South America contributes approximately 6% of global floating dock demand, with Brazil and Chile leading deployment activity through expanding coastal logistics infrastructure and marina redevelopment investments. Commercial fishing operations, tourism-linked waterfront projects, and regional ferry transportation upgrades are driving adoption of modular floating systems capable of reducing installation disruption by nearly 18%. However, inconsistent infrastructure financing and high imported material costs continue constraining large-scale deployment efficiency across several coastal economies. Localized demand for low-maintenance composite docks increased by 22% in 2025 as operators prioritized durability and reduced servicing exposure. Buyers remain highly price-sensitive, favoring scalable systems with lower lifecycle maintenance requirements. The region presents strong long-term expansion potential, although companies must balance growth opportunities against infrastructure funding limitations and supply chain volatility.

Middle East & Africa accounts for approximately 9% of global floating dock demand, driven by offshore energy servicing, waterfront tourism expansion, and large-scale coastal infrastructure modernization projects across the UAE, Saudi Arabia, and South Africa. Marina and offshore support deployments increased by nearly 24% in 2025 as governments accelerated smart coastal development initiatives and logistics diversification strategies. Strategic partnerships between marine infrastructure developers and regional engineering firms are improving project execution speed by approximately 17%. Operators increasingly prefer modular heavy-duty dock systems capable of supporting rapid deployment and harsh marine conditions with lower maintenance exposure. Investment-led procurement behavior and expanding waterfront megaproject pipelines are transforming the region into a high-value marine infrastructure market where scalability, durability, and execution speed determine competitive positioning.

China – 31% market share in the Floating Dock market due to dominant shipbuilding capacity, integrated marine manufacturing ecosystems, and aggressive coastal infrastructure expansion.

United States – 18% market share in the Floating Dock market driven by strong defense-linked marine infrastructure demand, smart-port modernization, and advanced marina redevelopment activity.

The floating dock market is defined by competition between global marine infrastructure leaders, regional fabrication specialists, and modular dock technology innovators including Bellingham Marine, Marinetek, SF Marina, EZ Dock, and Meeco Sullivan. The top five players collectively control approximately 39% of global market activity, competing aggressively on customization capability, deployment speed, corrosion resistance, and integrated digital monitoring systems. Advanced modular dock platforms reduce installation timelines by nearly 28%, while composite-based systems lower lifecycle maintenance exposure by approximately 19%, forcing traditional steel-focused manufacturers to accelerate material innovation. Companies are expanding regional manufacturing hubs, strengthening engineering partnerships, and vertically integrating supply chains to secure faster execution capacity amid ongoing coastal infrastructure investment cycles. Technology-driven product differentiation and localized servicing networks are increasingly reshaping competitive positioning, while high marine engineering costs and certification requirements continue limiting new market entry. Winning requires scalable manufacturing, digitally optimized dock ecosystems, and rapid-response project execution capabilities.

Bellingham Marine

Marinetek Group

SF Marina Systems

EZ Dock

Meeco Sullivan

Walcon Marine

AccuDock

Candock

Ingemar

Technomarine Manufacturing

Poralu Marine

Jetfloat International

MARTINI ALFREDO S.p.A.

Flotation Systems Inc.

Advanced modular floating dock systems are becoming the operational standard across commercial marinas, defense facilities, and waterfront infrastructure projects. Composite-reinforced dock platforms improve corrosion resistance by nearly 24% while reducing lifecycle maintenance costs by 18% compared to traditional steel-intensive systems. More than 46% of newly deployed floating docks in 2026 integrated modular construction designs supporting faster assembly and scalable expansion. Manufacturers are optimizing prefabricated production lines and regional assembly networks to reduce deployment delays, creating stronger competitive positioning in high-volume coastal infrastructure projects.

IoT-enabled monitoring and AI-driven ballast stabilization technologies are accelerating operational transformation across smart-port ecosystems. Predictive maintenance systems reduce unplanned dock servicing incidents by approximately 17%, while automated load-balancing platforms improve docking efficiency by 21%. Adoption of digitally monitored floating infrastructure surpassed 39% across newly modernized marine facilities in 2025 as operators prioritized uptime optimization and structural reliability. Companies integrating software analytics with dock engineering platforms are securing long-term maintenance contracts and differentiating through data-driven operational support capabilities.

Between 2026 and 2028, inductive charging docks, hybrid renewable-powered marina systems, and autonomous vessel-compatible floating platforms will redefine premium infrastructure deployment. Smart charging-enabled docks improve vessel turnaround efficiency by nearly 26% compared to legacy fueling systems while lowering waterfront energy dependency. Innovation leaders with integrated automation, sustainable materials, and digitally scalable dock ecosystems will capture higher-value defense, offshore energy, and smart-port infrastructure contracts as marine operators accelerate infrastructure modernization cycles.

April 2025 – Bellingham Marine expanded turnkey marina infrastructure deployment capabilities through the St George Motor Boat Club marina expansion project in Australia, integrating modular floating dock systems designed to improve berth optimization and reduce installation timelines by approximately 20%. The expansion strengthened the company’s regional marine contracting footprint. [Marina Expansion Push] Source: domain — Bellingham Marine

September 2024 – SF Marina installed a 460-meter arc-shaped floating breakwater system at Waiheke Island Marina in New Zealand using 23 floating concrete pontoons to improve docking protection and wave-energy reduction. The deployment enhanced marina resilience against severe marine conditions while strengthening sustainable waterfront infrastructure positioning. [Wave Protection Upgrade] Source: domain — Marina World

January 2024 – Bellingham Marine announced executive leadership restructuring with the appointment of a new company president to accelerate global marine infrastructure execution and waterfront engineering expansion initiatives. The strategic shift aligned with rising demand for integrated floating dock systems and large-scale coastal redevelopment contracts. [Leadership Realignment Strategy] Source: domain — Bellingham Marine )

2024 – SF Marina advanced smart waterfront infrastructure deployment through its floating fuel dock solution developed with Malte Group AB, integrating automated leakage detection systems and compliance-ready fuel management technology. The system enabled environmentally controlled fueling operations while supporting stricter marine safety regulations across sensitive waterfront locations. [Smart Fueling Integration] Source: domain — SF Marina

The Floating Dock Market Report delivers comprehensive analysis across dock types including concrete, plastic, wood, metal, and modular systems, alongside application segments such as marina operations, commercial ports, ferry services, waterfront recreation, boat mooring, and ship maintenance. The report evaluates demand trends across six major end-user categories and covers key geographic regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Advanced technologies assessed include IoT-enabled structural monitoring, AI-driven ballast systems, composite-reinforced dock platforms, modular floating infrastructure, and smart energy-integrated marina systems shaping marine infrastructure modernization between 2026 and 2033.

The study analyzes more than 10 leading companies and identifies operational trends influencing procurement, deployment speed, maintenance optimization, and lifecycle performance. Modular dock systems account for nearly 46% of new marine infrastructure installations, while digitally monitored floating platforms exceeded 39% adoption across upgraded commercial waterfront projects in 2025. The report provides strategic benchmarking on regional production capacity, infrastructure investment direction, technology integration, and competitive positioning. It supports decision-makers evaluating expansion opportunities, product innovation priorities, regional manufacturing strategies, partnership models, and long-term infrastructure modernization pathways across evolving global marine ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 327 Million |

|

Market Revenue in 2033 |

USD 454.45 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bellingham Marine, Marinetek Group, SF Marina Systems, EZ Dock, Meeco Sullivan, Walcon Marine, AccuDock, Candock, Ingemar, Technomarine Manufacturing, Poralu Marine, Jetfloat International, MARTINI ALFREDO S.p.A., Flotation Systems Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |