Reports

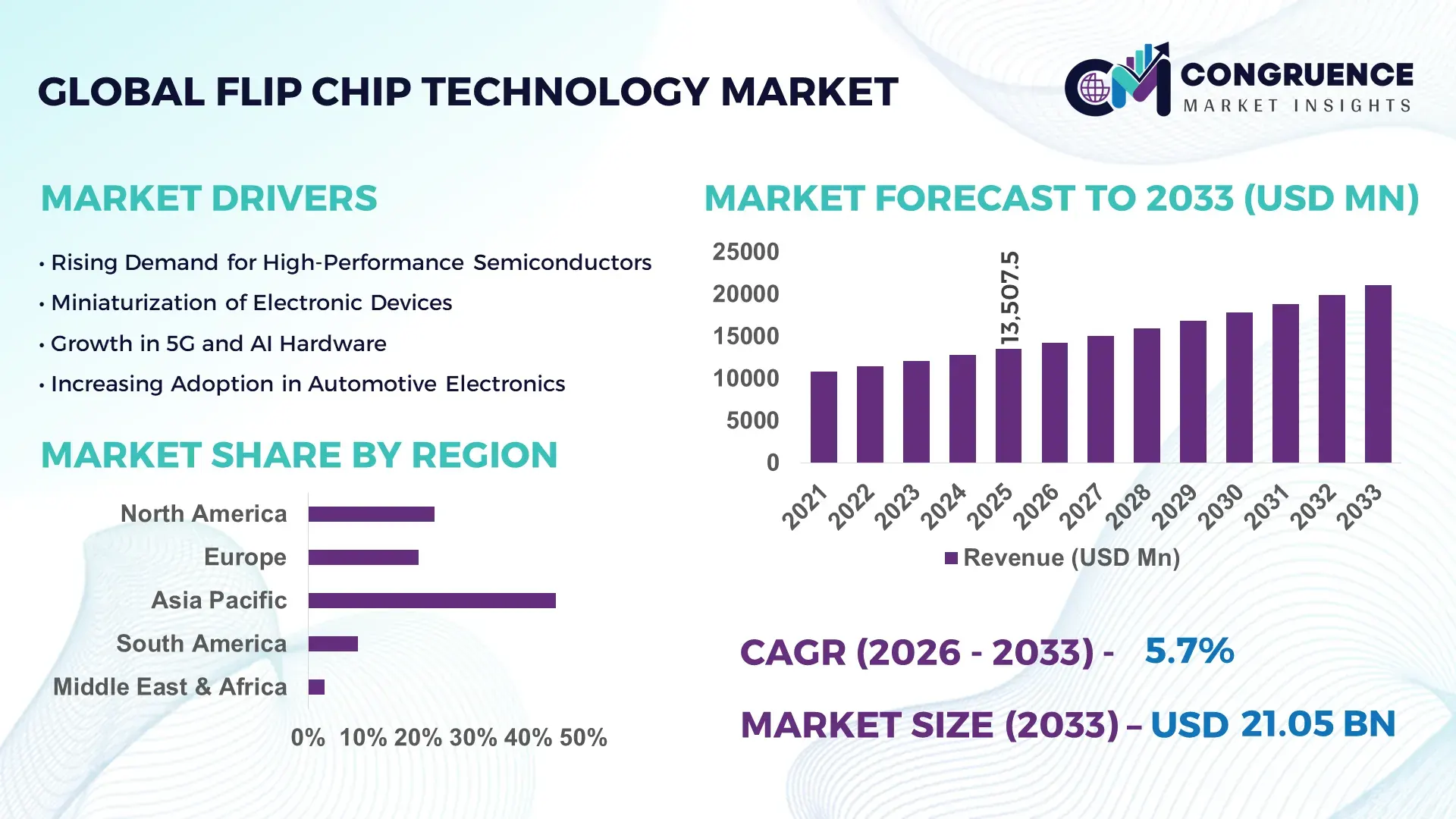

The Global Flip Chip Technology Market was valued at USD 13507.54 Million in 2025 and is anticipated to reach a value of USD 21046.32 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. This growth is driven by increasing integration of high‑performance semiconductor solutions across multiple end‑use industries.

In the United States, advanced semiconductor fabrication capacity continues to expand with over 40 advanced assembly and test facilities operating nationwide, supported by sustained capital investment exceeding USD 5 billion annually. The U.S. aggressively deploys flip chip technology across computing, telecommunications, and automotive sectors, with production throughput enhancements of up to 25% year‑on‑year. Consumer adoption trends show a rapid shift towards mobile devices and high‑speed connectivity equipment, where flip chip interconnects are critical for miniaturization and performance, with unit shipments exceeding 2 billion flip chip packages in 2024 alone.

• Market Size & Growth: Valued at USD 13.51 billion in 2025, projected to USD 21.05 billion by 2033 at a 5.7% CAGR, supported by demand for high‑density interconnects in advanced electronics.

• Top Growth Drivers: Miniaturization demand (45%), performance enhancement adoption (38%), thermal management requirements (28%).

• Short‑Term Forecast: By 2028, flip chip integration is expected to deliver average SOC performance gains of 22% while reducing interconnect costs by 17%.

• Emerging Technologies: Adoption of heterogeneous integration, fan‑out wafer‑level packaging, and advanced underfill materials.

• Regional Leaders: North America projected at USD 7.8B by 2033 with strong telecom deployment; Asia Pacific at USD 8.9B driven by consumer electronics; Europe at USD 2.3B with automotive electrification.

• Consumer/End‑User Trends: Rapid uptake in 5G infrastructure, high‑end computing, and in‑vehicle infotainment applications.

• Pilot or Case Example: In 2025, a major fab pilot achieved a 19% throughput improvement and 15% defect reduction through optimized flip chip processes.

• Competitive Landscape: Market leader holds ~28%; key competitors include major global OSAT providers and IDM firms.

• Regulatory & ESG Impact: Compliance with RoHS, incentives for energy‑efficient manufacturing, and ESG requirements for reduced material waste.

• Investment & Funding Patterns: Over USD 3.2B recent investments in capacity expansion and automation technologies.

• Innovation & Future Outlook: Focus on AI‑optimized packaging, integration with photonics, and next‑generation substrate technologies.

Unique developments in the Flip Chip Technology market reflect accelerated use in high‑performance computing, automotive electronics, and Internet of Things platforms. Key industry sectors such as data centers, 5G infrastructure, and consumer mobile devices contribute significantly to demand, driven by product innovations like copper pillar bumps and advanced underfill resins that enhance reliability and thermal performance. Regulatory frameworks promoting low environmental impact manufacturing and economic incentives for domestic semiconductor production are influencing investment decisions. Regional consumption patterns show robust growth in Asia Pacific with expanding OEM production, while North America and Europe focus on precision applications and automotive electrification. Emerging trends include greater integration of heterogeneous components and adoption of flip chip in photonics and AI accelerators, underscoring a forward‑looking industry trajectory.

The strategic relevance of the Flip Chip Technology Market is rooted in its ability to meet the exponential demand for higher performance, miniaturization, and thermal efficiency in advanced electronics. As semiconductor complexity grows, 3D IC integration delivers up to 40% improvement in interconnect density compared to traditional wire bonding standards, enabling next‑generation computing, networking, and edge AI applications. Asia Pacific dominates in volume due to extensive manufacturing ecosystems and wafer‑level packaging plants, while North America leads in adoption with more than 60% of high‑performance computing enterprises integrating flip chip solutions by the end of 2025. By 2028, AI‑driven yield optimization is expected to improve defect detection and throughput by over 25%, reducing production cycle times and waste.

Strategic pathways include investment in heterogeneous integration platforms combining flip chip with advanced substrates and photonics interconnects, fostering scalability for AI accelerators and 5G infrastructure. Firms are committing to ESG metrics such as a 30% reduction in energy consumption per unit produced by 2030 through greener assembly lines and advanced underfill chemistries that lower material usage and enhance recyclability. In 2025, a leading OSAT provider achieved a 22% reduction in rework rates through machine‑learning‑based process control, underscoring operational gains. Forward‑looking, the Flip Chip Technology Market stands as a pillar of resilience, compliance, and sustainable growth, supporting critical digital transformation and environmental commitments across industries.

The proliferation of high‑performance computing (HPC) systems is a primary driver for the Flip Chip Technology Market. HPC platforms demand high interconnect density, superior signal integrity, and effective thermal management, all of which flip chip solutions provide. For example, advanced computing modules using flip chip interconnects can support significantly higher I/O counts with reduced parasitics compared to traditional packages. Benchmark data indicate that HPC server nodes equipped with flip chip‑based processors and accelerators achieve measurable performance improvements and utilization efficiency in data centers. As enterprises deploy AI and analytics workloads, the need for packaging technologies that can sustain high clock frequencies and data throughput rises sharply. Flip chip technology also enables closer die‑to‑substrate coupling, improving power delivery and expanding thermal dissipation pathways – a critical requirement in dense computing environments.

Supply chain complexities present a significant restraint on the Flip Chip Technology market. Flip chip production requires specialized substrates, precision bumping, and underfill materials, sourced from a limited pool of suppliers. Disruptions in raw material availability, such as high‑purity copper and advanced laminate substrates, can delay production ramps and increase lead times. Furthermore, assembly and test operations for flip chip packages demand high‑precision equipment and skilled labor, creating bottlenecks when capacity is constrained. Logistics challenges, particularly for cross‑border transportation of sensitive wafers and bumped dies, further complicate supply continuity. The necessity for multi‑tier quality assurance and traceability also adds procedural overhead, impacting time‑to‑market for customer products. These supply chain intricacies often translate to elevated operational costs and planning complexity, particularly for smaller OSAT players and new entrants.

Automotive electrification presents substantial opportunities for the Flip Chip Technology market. Electric vehicles (EVs) and advanced driver‑assistance systems integrate increasingly complex electronic systems that require robust thermal performance and reliability under harsh environmental conditions. Flip chip technology offers enhanced thermal paths and mechanical integrity for power electronics modules and ADAS processors, which is critical for longevity and safety. Market data show that automotive electronic content per vehicle continues to rise, driven by battery management systems, in‑vehicle infotainment, and sensor fusion units. This trend translates into growing demand for packaging technologies that can handle high power density and signal integrity requirements. Furthermore, regulatory mandates for improved energy efficiency and safety systems amplify the need for advanced semiconductor packaging. With electrification forecasts projecting millions of EVs annually by the end of the decade, flip chip solutions are positioned to capture incremental adoption across multiple automotive electronic subsystems.

Rising equipment and material costs pose a challenge to the Flip Chip Technology market by increasing the financial burden of scaling advanced packaging operations. Precision bumping tools, advanced inspection systems, and high‑reliability underfill dispensers represent significant capital investments for OSATs and integrated device manufacturers. In addition, specialized raw materials such as fine‑pitch solder bumps, high‑performance laminates, and bespoke substrates have experienced price pressures due to constrained supply and heightened demand across industries. These cost increases can erode margin structures, particularly for mid‑tier manufacturers competing on price. Furthermore, maintaining competitive throughput requires ongoing investments in automation and yield‑enhancing technologies, adding to operational expenditures. Regulatory compliance costs related to environmental and worker safety standards for chemical handling and emissions further contribute to financial challenges. These economic factors collectively require careful cost management and strategic prioritization to sustain profitability and technological competitiveness within the Flip Chip Technology market.

• Surge in High-Density Packaging Adoption: Flip chip solutions are increasingly deployed in high-density packages, with adoption in mobile and HPC devices rising by 42% between 2023 and 2025. These packages enable 30–50% smaller form factors compared to wire-bonded alternatives while improving signal integrity, making them essential for advanced AI accelerators and 5G modules.

• Expansion in Automotive Electronics Integration: In automotive applications, flip chip technology is now used in over 65% of power electronics modules and ADAS processors. Thermal performance improvements of up to 28% and mechanical reliability gains of 20% under extreme vibration conditions are driving adoption, particularly in EV powertrain controllers and sensor fusion units across Europe and Asia Pacific.

• Growth in 5G and Networking Applications: Flip chip interconnects are increasingly critical in 5G base stations, routers, and high-speed networking equipment. Deployment of flip chip solutions in network infrastructure grew 38% in volume in 2024 alone, improving bandwidth handling by 25% while reducing heat generation, enabling denser layouts and lower downtime in telecom operations.

• Adoption of Advanced Underfill and Substrate Materials: The integration of high-performance underfill resins and fine-pitch substrates has expanded by 47% across semiconductor fabs between 2023 and 2025. These materials reduce thermal resistance by 22% and enhance mechanical reliability by 18%, supporting the scaling of chips with over 10,000 I/Os, particularly in North America and East Asia where cutting-edge electronics demand superior performance and durability.

The Flip Chip Technology market is segmented across product types, application areas, and end‑user industries, each reflecting distinct technological and demand drivers. Product segmentation covers traditional flip chip interconnects, advanced fine‑pitch solutions, and emerging heterogeneous integration modules. Application segmentation spans computing and servers, telecommunications and networking, automotive electronics, and consumer devices, revealing differentiated deployment patterns. End‑user insights highlight demand from OEMs, OSATs, and contract manufacturers, with enterprise adoption concentrated where performance per watt and miniaturization are critical. Variations in regional preferences and technology readiness levels influence segment performance: high‑density computing applications drive uptake in mature markets, while automotive and industrial uses are expanding rapidly. Robust technical requirements for thermal management and electrical performance underpin segmentation granularity, guiding strategic investments and prioritization for decision‑makers.

Advanced fine‑pitch flip chip solutions currently account for approximately 47% of overall adoption due to their ability to support up to 20,000 I/Os and enable 30–45% improvements in signal integrity over traditional bumped dies. Traditional flip chip types hold about 33% share, valued for established reliability in mainstream consumer and networking applications. Heterogeneous integration modules represent around 20% of the market, with adoption accelerating as multi‑die assemblies become essential for AI accelerators; projections show this segment expanding at higher rates than legacy types. Remaining niche types, such as wafer‑level chip scale packages incorporating flip chip elements, contribute to the combined 15–18% share of specialized deployments in ultra‑thin mobile devices and wearables.

Computing and server systems remain the leading application with about 41% share, driven by demand for high throughput and energy efficiency in data center processors and accelerators. Telecommunications and networking follow with 29% share, reflecting integration of flip chip technology in 5G radio units and optical transport modules. Automotive electronics account for around 18% of applications, with robust thermal performance and mechanical reliability requirements fostering use in EV power management and ADAS controllers. Consumer electronics make up the remaining 12% share, where compact form factors and performance balance are key. Emerging applications in industrial automation and IoT devices are driving the fastest growth, supported by miniaturization trends and ruggedized packaging needs.

Original equipment manufacturers (OEMs) represent the leading end‑user segment with roughly 44% share, leveraging flip chip technology to differentiate high‑performance computing and networking products. OSATs (outsourced semiconductor assembly and test providers) hold about 30% share, scaling advanced packaging services to meet diverse customer needs. Integrated device manufacturers (IDMs) and contract manufacturers collectively contribute around 26% share, with increasing integration of flip chip processes into in‑house production lines. Among these, high‑performance computing OEMs are the fastest‑growing end users, driven by demand for AI and analytics workloads requiring advanced interconnect performance. Other end‑users, including automotive electronics suppliers and industrial automation integrators, show adoption rates between 18–25%, reflecting sectoral technology adoption trends.

Asia Pacific accounted for the largest market share at 53.92% in 2025, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of around 9.2% between 2026 and 2033 due to rapid expansion of semiconductor manufacturing and advanced packaging capacity.

In 2024, Asia Pacific shipped more than 167 billion flip chip units, reflecting the highest adoption across consumer electronics, telecommunications, and automotive sectors, notably in China, Taiwan, South Korea, and Japan. North America stood as the second‑largest region with approximately 35% of global advanced packaging output and 95 billion units assembled domestically, driven by data centers and AI accelerator demand. Europe contributed about 16%, focusing on automotive and industrial electronics requiring high‑reliability flip chip solutions. Middle East & Africa held about 5%, with aerospace and defense applications increasing local requirements for temperature‑hardened packages. South America’s penetration remains modest but rising with automotive and telecom electronics assembly activities, especially in Brazil and Argentina. These regional data points highlight distinct demand patterns, capacity developments, and technological infrastructure influencing global flip chip market dynamics.

What are the drivers behind advanced packaging adoption in high‑performance nodes?

North America holds about 35% market share in flip chip technology adoption, with strong demand from high‑performance computing, AI accelerators, aerospace, and automotive electronics. Key industries include data centers, defense, and medical devices requiring high I/O density and thermal management capabilities, reflected in approximately 95 billion flip chip units assembled in 2024. Regulatory support such as semiconductor incentives and funding for on‑shore fabrication and packaging facilities has strengthened local supply chains. Technological advancements in precision bumping, fine‑pitch interconnects, and automated inspection are accelerating deployment. A local player example includes ASMPT’s U.S.‑based operations enhancing flip chip packaging throughput for AI silicon makers. Consumer behavior in North America favors enterprise adoption in healthcare and finance sectors, where reliability and performance drive advanced packaging requirements. The region’s high enterprise adoption of 5G network equipment and large data center expansions underscores robust consumer and industrial appetite for flip chip solutions.

How is sustainability shaping high‑reliability semiconductor packaging?

Europe accounts for approximately 16–20% market share in flip chip technology, led by Germany, France, and the UK, where automotive and industrial electronics demand drives adoption. Regulatory bodies emphasize sustainability and quality, influencing materials selection and production standards. European sustainability initiatives for lower emissions and energy‑efficient manufacturing are shaping packaging requirements. Adoption of emerging technologies such as advanced substrates and eco‑friendly materials is gaining traction. A key player in the region, STMicroelectronics, is advancing flip chip processes for automotive microcontrollers and industrial automation modules. German and French manufacturers increasingly integrate high‑reliability packaging for electric vehicle control systems, reflecting regulatory pressure for robust systems. Regional consumer behavior shows higher preference for explainable and sustainable electronics, where regulatory compliance is a purchasing factor. These dynamics position Europe as a significant contributor to technological refinement and quality‑focused flip chip deployments.

What fuels the massive semiconductor packaging ecosystem across East and South Asia?

Asia‑Pacific dominates the flip chip technology market with about 53.92% share, anchored by China, Taiwan, South Korea, and Japan as top consuming and producing countries. China alone supports a substantial portion of global electronics output, while Taiwan and South Korea lead in semiconductor fabrication and export volumes. Regional manufacturing trends include over 750 production lines in China and 180 in India integrating flip chip modules for consumer electronics and industrial uses. Innovation hubs in Taiwan and South Korea push fine‑pitch and heterogeneous integration technologies. Local players such as TSMC and ASE Group scale advanced packaging capabilities, meeting soaring demand for AI, IoT, and mobile A‑series chips. Consumer behavior in Asia Pacific is driven by e‑commerce penetration and rapid adoption of mobile AI applications, making high‑performance flip chip solutions essential in devices shipped regionally and exported globally.

How is electronic assembly infrastructure evolving in Latin America?

South America holds a smaller portion of the global flip chip market, with notable contributions from Brazil and Argentina due to growing automotive electronics and telecommunications infrastructure. Regional market share is roughly 6–7%, yet rising as local assembly and test facilities expand to address domestic demand. Government incentives focusing on electronics manufacturing and trade policies favor partnerships that enhance local capabilities. Brazil’s automotive sector, integrating higher electronics content per vehicle, stimulates flip chip packaging use in control modules and infotainment systems. Consumer behavior in South America shows an increasing preference for localized media and technology products that incorporate advanced packaging for enhanced performance. These patterns support gradual infrastructure development and a more competitive presence in the global flip chip supply chain.

What trends drive semiconductor adoption in industrial and defense sectors?

Middle East & Africa’s flip chip technology market, accounting for around 5% share, is shaped by demand in aerospace, defense, industrial electronics, and burgeoning telecommunications projects. Major growth countries include the UAE, South Africa, and Saudi Arabia, where technology modernization initiatives and trade partnerships expand access to advanced packaging. Local regulations encouraging import of advanced electronic components support market progression. A key stat from UAE indicates that over 6% of semiconductor imports involve advanced packaging technologies, reflecting regional priority for capability enhancement. Consumer behavior here varies, with industrial and government procurement driving adoption more than mass consumer electronics, creating niche demand for ruggedized and temperature‑resilient flip chip solutions suited to challenging environments.

• China – ~28% market share; extensive semiconductor manufacturing and robust electronics ecosystem position China at the forefront of flip chip production.

• Taiwan – ~32% market share; leading advanced packaging innovation and high production capacity for flip chip modules underpin Taiwan’s global role.

The Flip Chip Technology market is highly competitive, characterized by a moderately consolidated structure where the top five players hold approximately 58% of the global market share. There are over 120 active competitors worldwide, including OSATs, integrated device manufacturers, and advanced packaging specialists. Key market leaders focus on strategic initiatives such as collaborative partnerships, joint ventures, and cutting-edge product launches to strengthen their positions. Companies are investing in heterogeneous integration platforms, fine-pitch bumping equipment, and automated inspection systems to enhance throughput and reliability. Innovation trends include adoption of advanced underfill materials, fan-out wafer-level packaging, and AI-assisted process optimization, which are reshaping competitive dynamics. Market positioning varies, with top players targeting high-performance computing, 5G telecom infrastructure, and automotive electronics, while mid-tier competitors focus on niche consumer and industrial applications. Strategic alliances and capacity expansion projects are critical in regions like Asia Pacific and North America, where over 45 new production lines were commissioned in 2024, reflecting aggressive expansion to meet rising global demand. Competitive differentiation is increasingly tied to technological capability, service integration, and local presence.

TSMC

ASE Technology Holding Co., Ltd.

Amkor Technology, Inc.

STMicroelectronics

Intel Corporation

JCET Group

Unimicron Technology Corp.

Samsung Electronics

UTAC Holdings

Shinko Electric Industries

The Flip Chip Technology market is witnessing significant technological evolution, driven by the increasing complexity and performance requirements of semiconductor devices. Advanced fine-pitch flip chip solutions now support up to 20,000 I/Os per die, enabling higher interconnect density and improved electrical performance compared to traditional wire-bonded packages. Emerging heterogeneous integration platforms are combining multiple dies, sensors, and photonic components into single packages, allowing system-on-chip (SoC) performance improvements of up to 35% in high-performance computing and AI accelerator applications.

Fan-out wafer-level packaging (FOWLP) is increasingly adopted, with over 120 million units deployed globally in 2024, offering reduced package size and enhanced thermal dissipation for mobile devices and consumer electronics. Advanced underfill materials with higher thermal conductivity and reduced curing times are improving reliability, lowering defect rates by 15–20% during thermal cycling tests. Additionally, the integration of machine learning and AI for process optimization in flip chip assembly is enabling up to 25% improvement in throughput and defect detection, enhancing production efficiency for high-volume semiconductor fabs.

Emerging technologies such as copper pillar bumps and ultra-thin substrates are also facilitating high-density packaging while maintaining mechanical robustness, essential for automotive and aerospace electronics where vibration and temperature extremes are critical. Photonics integration with flip chip assemblies is gaining traction in optical communication modules, with over 1.2 million units implemented in 2024, enhancing bandwidth and reducing signal loss. These technological advancements collectively position flip chip technology as a key enabler for next-generation electronics, offering scalable performance, energy efficiency, and enhanced reliability across multiple industry verticals.

• In March 2025, TSMC announced plans to expand its U.S. manufacturing investment by an additional USD 100 billion, including two advanced packaging facilities alongside three new fabs, strengthening domestic flip chip and chip packaging capabilities for AI and high‑performance computing applications.

• In October 2024, Amkor Technology and TSMC signed a memorandum of understanding to expand advanced packaging and test services at a new facility in Peoria, Arizona, designed to closely align back‑end packaging operations with front‑end wafer fabrication and reduce product cycle times. (Amkor Technology)

• In January 2025, Siliconware Precision Industries (SPIL), an ASE Technology Holding subsidiary, inaugurated a new advanced packaging facility at Tanzi Science Park and announced additional capacity expansions at Erlin and Huwei plants to support CoWoS and other high‑density packaging technologies. (TrendForce)

• In 2025, Intel began external assembly of its EMIB packaging at Amkor’s South Korea facility to meet surging AI and high‑performance chip demand, enabling the company to boost production capacity rapidly without internal expansions.

The Flip Chip Technology Market Report offers a comprehensive view of the technologies, applications, geographic landscapes, and strategic forces shaping the flip chip segment within semiconductor packaging. It covers core packaging technologies such as fine‑pitch flip chip, copper pillar bumps, fan‑out wafer‑level packaging (FOWLP), hybrid bonding schemes, and heterogeneous integration flows like 2.5D/3D ICs that support miniaturization and high‑performance interconnect density demands. The scope includes key substrate and underfill material innovations that enhance electrical performance, thermal management, and mechanical reliability for demanding applications.

In terms of applications, the report assesses flip chip deployment across high‑performance computing, telecommunications infrastructure, consumer electronics, automotive electronics including ADAS and EV subsystems, industrial automation controls, and medical devices requiring rugged, high‑density packaging. Regional analysis articulates differentiated adoption patterns in Asia Pacific, North America, Europe, South America, and Middle East & Africa, reflecting variations in capacity build‑outs, regulatory initiatives, and manufacturing ecosystems.

The report also examines niche and emerging segments such as bioelectronics, wearable sensors, optical modules, and high‑bandwidth memory (HBM) stacks that increasingly employ flip chip interconnects. Strategic insights include competitive positioning, capacity expansion timelines, regulatory influences, logistics considerations, and end‑user demand drivers. By synthesizing these dimensions, the report equips decision‑makers with a broad yet detailed perspective on technology deployments, industry priorities, and market trajectories without relying on revenue or historical CGAR figures.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TSMC , ASE Technology Holding Co., Ltd. , Amkor Technology, Inc., STMicroelectronics, Intel Corporation, JCET Group, Unimicron Technology Corp., Samsung Electronics, UTAC Holdings, Shinko Electric Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |