Reports

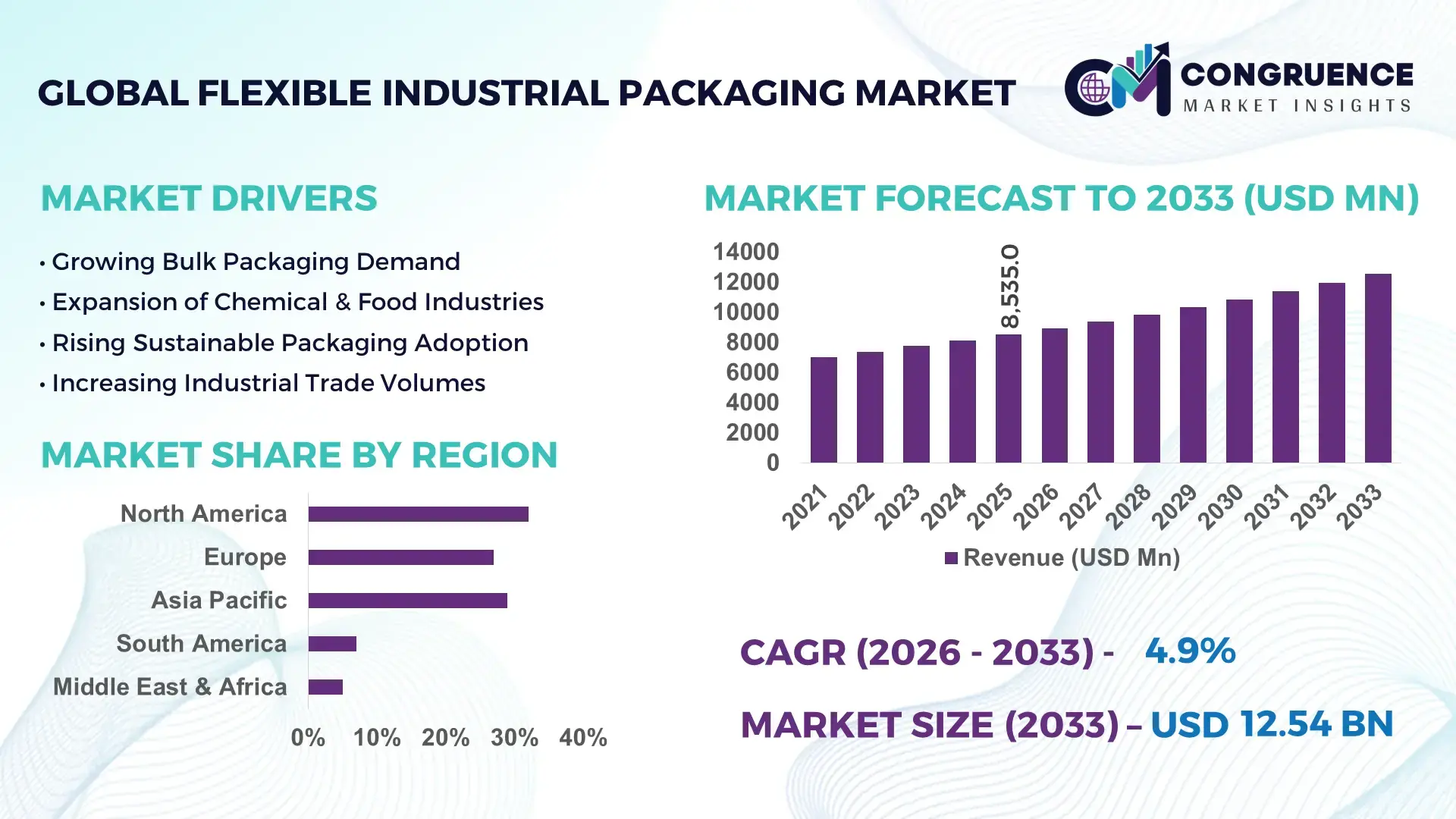

The Global Flexible Industrial Packaging Market was valued at USD 8,535.0 Million in 2025 and is anticipated to reach a value of USD 12,543.0 Million by 2033 expanding at a CAGR of 4.93% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is primarily driven by rising demand for cost-efficient bulk packaging solutions across chemicals, food processing, agriculture, and construction sectors.

The United States represents the dominant country in the Flexible Industrial Packaging Market, supported by advanced manufacturing infrastructure and strong end-use industrial demand. The U.S. produces over 36 million tons of plastic resins annually, a critical raw material for FIBCs, industrial liners, and flexible intermediate bulk containers. More than 65% of industrial chemical shipments in the country utilize flexible packaging formats due to weight reduction and storage efficiency advantages. Capital investment in sustainable packaging technologies exceeded USD 2 billion in 2024, focusing on recyclable polypropylene and high-barrier film innovations. Additionally, automation penetration in industrial packaging facilities has surpassed 58%, enabling higher throughput and reduced material wastage.

Market Size & Growth: Valued at USD 8,535.0 Million in 2025, projected to reach USD 12,543.0 Million by 2033, expanding at 4.93% CAGR; growth is supported by increasing bulk material handling efficiency across industrial sectors.

Top Growth Drivers: 62% adoption in chemical bulk transport, 48% cost reduction versus rigid packaging, 35% improvement in logistics efficiency.

Short-Term Forecast: By 2028, automation integration is expected to improve packaging line productivity by 22% and reduce material waste by 15%.

Emerging Technologies: AI-driven quality inspection, recyclable mono-material polypropylene films, smart FIBC tracking with RFID integration.

Regional Leaders: North America projected above USD 4,200 Million by 2033 with high automation adoption; Asia-Pacific nearing USD 3,800 Million driven by industrial exports; Europe exceeding USD 2,900 Million supported by circular packaging mandates.

Consumer/End-User Trends: Over 57% of chemical manufacturers prefer FIBCs for bulk storage, while 44% of food processors are shifting toward recyclable liners.

Pilot Example: In 2024, a U.S. chemical plant reduced packaging downtime by 18% through AI-enabled defect detection systems.

Competitive Landscape: Berry Global (~14%), Amcor, Mondi Group, Greif, and Sonoco Products Company dominate the landscape.

Regulatory & ESG Impact: 70% of industrial buyers now prioritize recyclable or reusable bulk packaging formats aligned with circular economy targets.

Investment & Funding: Over USD 3.1 Billion invested globally since 2023 in sustainable flexible packaging manufacturing upgrades.

Innovation & Outlook: Lightweight multilayer films and reusable bulk container systems are expected to improve lifecycle efficiency by 25% by 2030.

Flexible Industrial Packaging serves chemicals (34%), food & beverages (27%), agriculture (18%), and construction (12%), with the remainder distributed across pharmaceuticals and mining. Recyclable polypropylene FIBCs and high-barrier multilayer films are gaining traction due to regulatory pressure and carbon-reduction targets. Asia-Pacific accounts for over 40% of production volume, supported by export-oriented manufacturing. Sustainability mandates and automation investments are reshaping product innovation, positioning reusable and RFID-enabled packaging as future growth pillars.

The Flexible Industrial Packaging Market holds strategic importance in global supply chains, particularly for bulk material handling in chemicals, agriculture, food ingredients, and construction materials. With over 60% of industrial bulk goods transported in flexible intermediate bulk containers (FIBCs) and liners, the market plays a pivotal role in reducing logistics costs and enhancing storage optimization. Advanced multilayer polypropylene systems deliver 28% higher load stability compared to conventional woven sacks, improving transport safety and warehouse efficiency.

Technological integration is accelerating competitiveness. AI-driven inspection systems deliver 20% defect detection improvement compared to manual quality checks. North America dominates in production volume, while Europe leads in sustainable adoption with over 68% of enterprises implementing recyclable bulk packaging formats. By 2028, smart packaging integration with IoT tracking is expected to cut inventory mismanagement by 17%.

Firms are committing to ESG improvements such as 30% recycled content integration by 2030 and 25% carbon footprint reduction in packaging operations. In 2024, a U.S.-based manufacturer achieved a 19% energy efficiency improvement through automation upgrades in FIBC production lines.

Looking ahead, the Flexible Industrial Packaging Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable industrial growth, driven by innovation in lightweight materials, digital traceability, and circular packaging frameworks.

The Flexible Industrial Packaging Market is influenced by increasing industrial output, expanding global trade flows, and sustainability-driven material innovation. Demand for flexible bulk containers, liners, and industrial films continues to rise as manufacturers prioritize lightweight packaging that reduces logistics costs by up to 30% compared to rigid alternatives. Automation penetration in packaging plants has crossed 50% in developed economies, enhancing throughput and minimizing defects. Environmental regulations encouraging recyclable polypropylene and mono-material solutions are reshaping product design standards. Additionally, cross-border chemical and agricultural exports have grown by over 12% in recent years, strengthening demand for high-durability and contamination-resistant flexible packaging formats.

Global chemical production exceeds 4 billion metric tons annually, with over 60% transported in bulk formats requiring durable flexible packaging. Flexible intermediate bulk containers reduce shipping weight by nearly 40% compared to rigid drums, improving transport efficiency. Agricultural commodity exports, including grains and fertilizers, have expanded by over 10% in Asia-Pacific, increasing demand for moisture-resistant liners. Additionally, 55% of industrial exporters now prefer flexible bulk packaging due to stackability and warehouse optimization benefits. The growing emphasis on contamination prevention and tamper-proof designs further accelerates adoption across cross-border trade networks.

Polypropylene and polyethylene resin prices fluctuate by 15–25% annually due to crude oil volatility, impacting manufacturing margins. Since raw materials account for nearly 65% of total production costs in FIBC manufacturing, price instability reduces profitability and planning accuracy. Supply chain disruptions have extended resin lead times by 20% in certain regions. Additionally, environmental regulations restricting single-use plastics have increased compliance costs by approximately 12% for manufacturers transitioning to recyclable alternatives. These financial pressures may delay capital investments in capacity expansion.

Over 70% of industrial buyers have committed to circular packaging targets, creating demand for mono-material and reusable FIBCs. Recyclable polypropylene content integration has improved by 25% in the past three years. Bio-based flexible films are gaining traction, with pilot adoption rising by 18% in Europe. Smart packaging with RFID tracking improves inventory accuracy by 16%, enhancing operational transparency. Increasing adoption of reusable bulk containers in chemical supply chains presents scalable opportunities for manufacturers offering lifecycle-optimized solutions.

While 68% of enterprises aim for recyclable packaging, global recycling rates for industrial plastics remain below 30%. Limited collection infrastructure in emerging economies restricts circular adoption. Compliance with cross-border packaging waste directives increases documentation and operational costs by nearly 14%. Additionally, certification requirements for food-grade flexible packaging involve rigorous testing protocols that extend product launch timelines by 6–9 months. Addressing infrastructure and regulatory harmonization remains critical for sustained growth.

Expansion of Recyclable Mono-Material FIBCs: Over 45% of new industrial packaging product launches in 2025 focus on mono-material polypropylene structures, improving recyclability rates by 30%. Industrial buyers report 22% reduction in disposal costs after switching to recyclable bulk containers. Europe leads with 60% enterprise-level adoption of recyclable FIBCs.

Automation in Bulk Packaging Production: Automation deployment in flexible packaging plants has surpassed 58% in developed economies. AI-enabled inspection systems reduce defect rates by 20% and improve line efficiency by 18%. Robotics integration has cut manual labor dependency by 25% in high-volume facilities.

Growth in Smart and RFID-Enabled Packaging: RFID integration in FIBCs has increased by 26% since 2023, improving inventory accuracy by 16% and reducing shipment loss by 12%. Chemical exporters report 14% faster turnaround time using digitally tracked bulk containers.

Lightweight High-Barrier Film Innovation: Advanced multilayer films reduce packaging weight by 35% while maintaining tensile strength standards. Adoption in food ingredient transport has grown by 21%, improving shelf stability and reducing contamination incidents by 15%.

The Flexible Industrial Packaging Market is segmented by type, application, and end-user industry. Flexible intermediate bulk containers (FIBCs) account for a substantial share due to widespread usage in bulk chemical and agricultural transport. Industrial liners and sacks are gaining traction for moisture-sensitive goods. Applications span chemical storage, food ingredient transport, agricultural commodities, and construction materials. Chemicals represent the leading segment, followed by food processing and agriculture. End-user demand is strongest among chemical manufacturers and agri-exporters, while pharmaceutical and mining sectors contribute niche but high-value requirements due to regulatory standards and contamination control needs.

Flexible Intermediate Bulk Containers (FIBCs) hold approximately 46% of total adoption due to high load-bearing capacity and reusability. Industrial flexible liners account for 28%, offering contamination resistance for chemicals and food ingredients. Woven sacks and multilayer films collectively contribute around 26%. FIBCs remain the leading type because they support up to 2,000 kg load capacity and reduce storage space requirements by nearly 30%. While FIBCs dominate, recyclable mono-material FIBCs are the fastest-growing segment, expanding at approximately 6.2% CAGR due to sustainability mandates. High-barrier multilayer films are also witnessing increased demand in food and pharmaceutical logistics.

Chemicals account for nearly 34% of application demand, followed by food & beverages at 27% and agriculture at 18%. Construction materials contribute 12%, with pharmaceuticals and mining covering the remaining 9%. Chemical applications lead due to high bulk transport frequency and hazardous material handling requirements. Agriculture is the fastest-growing application, expanding at approximately 5.8% CAGR, driven by rising fertilizer and grain exports. Over 52% of agricultural exporters in Asia-Pacific now utilize moisture-resistant flexible liners. In 2025, more than 40% of mid-sized chemical manufacturers reported piloting RFID-enabled FIBCs for improved tracking accuracy.

Chemical manufacturers represent approximately 38% of end-user adoption, followed by food processors at 25% and agricultural producers at 20%. Construction and mining collectively account for 17%. Chemical companies lead due to strict safety and contamination control standards. Food processing is the fastest-growing end-user segment, expanding at nearly 6.1% CAGR due to hygiene compliance and shelf-life optimization needs. Around 44% of food processors globally are transitioning toward recyclable flexible liners. In 2025, over 36% of large enterprises reported integrating automation in flexible packaging handling systems.

North America accounted for the largest market share at 32% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of5.8% between 2026 and 2033.

North America’s leadership is supported by high automation penetration exceeding 58% in industrial packaging plants and strong chemical bulk exports surpassing 900 million metric tons annually. Europe follows with approximately 27% share, driven by strict sustainability mandates and over 60% adoption of recyclable industrial packaging formats. Asia-Pacific holds nearly 29% share, supported by manufacturing output representing over 45% of global industrial production volume. South America contributes around 7%, largely influenced by agricultural commodity exports exceeding 180 million metric tons annually. The Middle East & Africa region accounts for roughly 5%, with demand tied to petrochemical exports and infrastructure projects valued above USD 300 billion collectively. Increasing industrial trade volumes, growing export-oriented economies, and regulatory mandates for recyclable materials are shaping regional growth trajectories across all five major regions.

North America accounts for approximately 32% of global market volume, supported by strong chemical, food processing, and agricultural export industries. The U.S. leads regional demand, representing over 75% of total North American consumption, followed by Canada at nearly 15%. Chemical manufacturing contributes more than 35% of regional packaging utilization. Regulatory frameworks encouraging recyclable materials and waste reduction targets have accelerated the adoption of mono-material polypropylene FIBCs, now used by over 60% of large exporters. Automation integration exceeds 58% in packaging plants, improving throughput by 20%. Berry Global, a major regional player, expanded its sustainable flexible packaging portfolio in 2024, focusing on high-strength recyclable bulk containers. Enterprise buyers in this region prioritize compliance, traceability, and digital inventory tracking, with over 48% implementing RFID-enabled packaging systems.

Europe holds nearly 27% of the global market share, with Germany, the UK, and France collectively contributing over 60% of regional demand. Germany leads in industrial output, accounting for nearly 25% of Europe’s chemical production volume. EU circular economy directives require increased recycled plastic content targets of at least 30% by 2030, driving rapid shifts toward recyclable FIBCs and liners. Over 68% of European enterprises report integrating sustainable packaging policies into procurement strategies. Automation and digital inspection technologies have penetrated nearly 50% of industrial packaging facilities. Mondi Group has introduced recyclable bulk packaging solutions with enhanced tensile strength, reducing material usage by 15%. European buyers show strong preference for certified, traceable packaging solutions aligned with ESG compliance frameworks.

Asia-Pacific represents approximately 29% of global consumption volume and ranks first in industrial output. China accounts for over 45% of regional demand, followed by India at 18% and Japan at 12%. The region handles more than 40% of global agricultural exports and 35% of chemical shipments. Infrastructure investments exceeding USD 1 trillion across major economies support construction-related packaging demand. Automation adoption is increasing, with 42% of large packaging facilities integrating robotic handling systems. Indian manufacturer UFlex has expanded high-barrier flexible packaging production capacity to support export markets. Regional buyers prioritize cost efficiency, lightweight materials, and scalability, particularly in export-driven industries.

South America contributes roughly 7% of global market volume, led by Brazil and Argentina, which together account for nearly 70% of regional demand. Brazil’s agricultural exports exceed 150 million metric tons annually, creating sustained demand for moisture-resistant flexible liners. Infrastructure modernization projects valued at over USD 120 billion are stimulating construction material packaging needs. Trade agreements facilitating cross-border commodity movement have enhanced bulk container usage by 14% over the past two years. Local producers are increasing capacity for woven polypropylene sacks to support fertilizer distribution networks. Buyers emphasize durability and cost optimization, with nearly 52% preferring reusable FIBC systems for grain and chemical exports.

The Middle East & Africa region accounts for nearly 5% of global demand, driven by oil & gas and petrochemical exports exceeding 500 million metric tons annually. The UAE and Saudi Arabia represent over 60% of regional consumption, supported by downstream petrochemical production. Construction projects valued above USD 400 billion are increasing demand for cement and mineral bulk packaging. Automation modernization initiatives in UAE industrial zones have raised packaging efficiency by 18%. South Africa leads sub-Saharan Africa in chemical and mining-related packaging adoption. Buyers increasingly demand heat-resistant and UV-stabilized FIBCs suited for extreme climatic conditions, with 37% of enterprises investing in advanced high-barrier flexible materials.

United States – 24% Market Share: Strong chemical manufacturing base, over 900 million metric tons bulk transport annually, and high automation penetration in packaging facilities.

China – 21% Market Share: Extensive manufacturing capacity, handling over 40% of Asia-Pacific industrial output and significant agricultural and chemical export volumes.

The Flexible Industrial Packaging Market is moderately fragmented, with over 120 active global and regional competitors. The top five companies collectively hold approximately 48% of total market share, reflecting a semi-consolidated structure. Leading players compete through product innovation, sustainable material integration, and automation upgrades. Around 35% of competitive strategies announced in 2024–2025 focused on recyclable mono-material packaging development. Mergers and acquisitions increased by 12% year-over-year, targeting regional capacity expansion and sustainable technology portfolios. Strategic partnerships with chemical and agricultural exporters account for nearly 28% of supply contracts among top-tier manufacturers. Automation investment among leading companies exceeds 20% of annual capital expenditure budgets, enhancing defect reduction rates by up to 20%. Competitive differentiation increasingly centers on ESG compliance, digital traceability solutions, and lightweight high-strength material innovations designed to reduce logistics costs by nearly 30%.

Greif Inc.

Sonoco Products Company

Sealed Air Corporation

UFlex Ltd.

LC Packaging

Global-Pak Inc.

Intertape Polymer Group

ProAmpac

Coveris

Bischof + Klein

RKW Group

Technological transformation in the Flexible Industrial Packaging Market centers on automation, material science innovation, and digital traceability. Over 58% of large-scale manufacturing plants have integrated robotic palletizing and automated stitching systems, improving production efficiency by 18–22%. AI-powered defect detection systems reduce quality inspection time by 25% and decrease product rejection rates by 15%.

Material innovation is focused on mono-material polypropylene structures, improving recyclability rates by nearly 30%. High-barrier multilayer films enhance moisture resistance by 20%, critical for agricultural exports. Bio-based polymer integration has increased by 17% in pilot projects targeting carbon reduction.

Digitalization through RFID-enabled FIBCs improves inventory accuracy by 16% and reduces shipment discrepancies by 12%. IoT-enabled tracking solutions allow real-time monitoring of bulk container utilization cycles, extending lifecycle performance by 25%. Additionally, advanced extrusion technologies enable 35% reduction in packaging weight while maintaining tensile strength standards. Collectively, these technologies strengthen operational efficiency, regulatory compliance, and lifecycle sustainability.

• In March 2025, Berry Global Group, Inc. released its 2024 Sustainability Report, detailing substantial progress in circular economy initiatives including a 43% year-over-year increase in post-consumer resin purchases (from 3.6% to 5.1%), enhancements to recyclability in key products (e.g., mono-material polypropylene closures), and a reduction of Scope 1 & 2 emissions by 28.3% compared to its 2019 baseline—surpassing 2025 targets early, alongside an MSCI rating upgrade to AA reflecting strong ESG performance. Source: www.businesswire.com

• In April 2025, Berry Global announced its second quarter 2025 financial results, reporting $2.50 billion in net sales, $391 million operating income, and 2% organic volume growth across segments; the company highlighted continued flexible packaging volume growth while progressing strategic portfolio actions including divestitures and integration of sustainability goals. Source: www.businesswire.com

• In April 2025, Amcor plc confirmed the successful completion of its all-stock combination with Berry Global, strengthening its global leadership in consumer and healthcare packaging solutions and unlocking synergies estimated at $650 million by fiscal 2028; the completed combination expands its flexible packaging innovation capabilities and global scale. Source: www.amcor.com

• In November 2025, Amcor announced an expansion of its North American flexible packaging production, committing to install new state-of-the-art equipment through the first half of 2026 to increase capacity—particularly to support protein packaging demand—and bolster its AmPrima flexible packaging product lines and overall market responsiveness. Source: www.packagingdive.com

The Flexible Industrial Packaging Market Report provides comprehensive coverage of product types including FIBCs, industrial liners, woven sacks, and high-barrier multilayer films, collectively serving bulk loads up to 2,000 kg capacity. The report evaluates applications across chemicals (34%), food & beverages (27%), agriculture (18%), construction (12%), and niche sectors including pharmaceuticals and mining.

Geographic coverage spans North America (32%), Europe (27%), Asia-Pacific (29%), South America (7%), and Middle East & Africa (5%), analyzing production capacity, trade volumes exceeding 4 billion metric tons of industrial goods annually, and automation penetration rates above 50% in developed economies.

Technology analysis includes AI-based inspection systems, RFID-enabled bulk containers, recyclable mono-material polypropylene solutions, and high-barrier film advancements reducing material weight by 35%. The report further assesses ESG integration trends, including 30% recycled content targets and carbon reduction initiatives.

Additionally, the scope encompasses competitive benchmarking of over 120 global players, sustainability-driven investments exceeding USD 3 billion since 2023, and digital transformation initiatives improving operational efficiency by up to 22%. The analysis delivers actionable insights for manufacturers, investors, distributors, and procurement leaders seeking long-term resilience, regulatory compliance, and innovation-driven growth within the Flexible Industrial Packaging Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 8,535.0 Million |

| Market Revenue (2033) | USD 12,543.0 Million |

| CAGR (2026–2033) | 4.93% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Berry Global; Amcor plc; Mondi Group; Greif Inc.; Sonoco Products Company; Sealed Air Corporation; UFlex Ltd.; LC Packaging; Global-Pak Inc.; Intertape Polymer Group; ProAmpac; Coveris; Bischof + Klein; RKW Group |

| Customization & Pricing | Available on Request (10% Customization Free) |