Reports

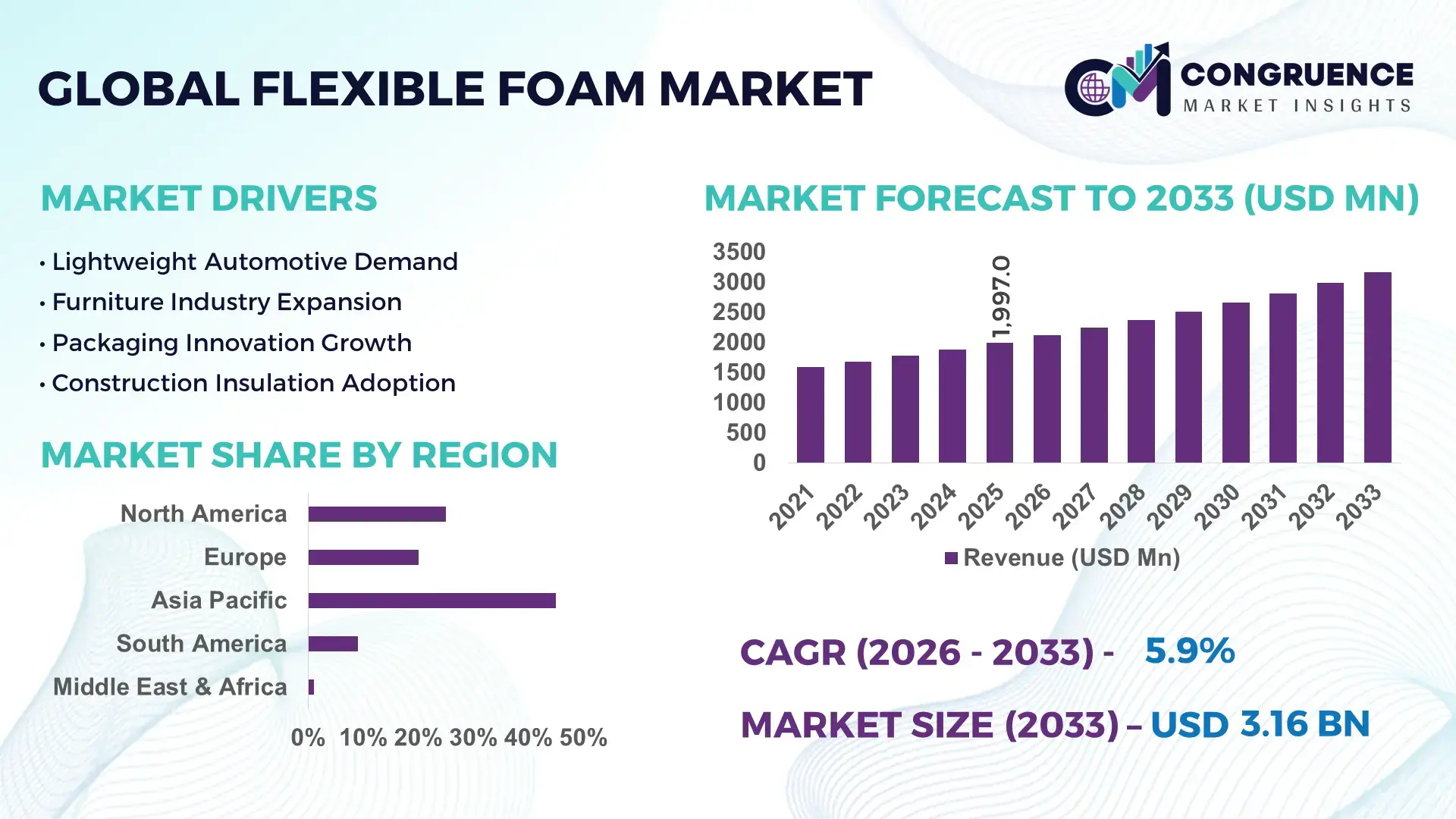

The Global Flexible Foam Market was valued at USD 1997 Million in 2025 and is anticipated to reach a value of USD 3158.97 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033.

The market is advancing through accelerated adoption of lightweight polyurethane and bio-based flexible foam materials across automotive seating, bedding, insulation, and packaging applications, where manufacturers are reducing component weight by nearly 18% while improving thermal and acoustic efficiency. Rising automation in foam cutting and molding lines has also lowered production waste by over 12%, strengthening operating margins across high-volume manufacturing facilities. Between 2024 and 2026, global supply chain restructuring and stricter emissions compliance in Europe and North America reshaped raw material sourcing strategies, particularly after volatility in petrochemical feedstock pricing linked to Red Sea shipping disruptions and energy-market instability. Producers increasingly shifted toward regional manufacturing hubs and recycled polyol integration to stabilize procurement costs and maintain delivery reliability.

China remains the dominant country in the global flexible foam market, accounting for nearly 34% of global production capacity in 2026, supported by strong downstream demand from furniture, automotive, and electronics industries. The country added more than 1.8 million metric tons of flexible polyurethane foam processing capacity between 2023 and 2025, while smart manufacturing adoption in tier-one industrial clusters exceeded 46%. Compared with several European producers, Chinese manufacturers operate at approximately 15% lower conversion costs due to scale efficiency and integrated chemical supply chains. India and Southeast Asia are also emerging as strategic expansion zones, with automotive interior foam demand increasing above 9% annually due to electric vehicle production growth.

The market is transitioning from volume-driven competition toward technology-led differentiation, making regional capacity positioning, sustainable material innovation, and supply chain resilience critical strategic priorities for manufacturers and investors.

Global market value rises from USD 1997 Million in 2025 to USD 3158.97 Million by 2033, driven by lightweight automotive and advanced bedding applications.

Automotive interior demand contributes over 31% of market consumption, while furniture and bedding account for nearly 42% combined globally.

Bio-based foam adoption increases 18% as manufacturers reduce petroleum-derived content amid tightening environmental compliance standards.

By 2027, automated foam conversion systems improve production efficiency by 14% and reduce material waste by approximately 11%.

AI-enabled process monitoring, robotic cutting systems, and advanced low-VOC polyurethane technologies reshape high-growth flexible foam manufacturing.

Asia-Pacific surpasses USD 1280 Million by 2030, Europe exceeds USD 760 Million, and North America crosses USD 690 Million through EV and furniture demand expansion.

Over 57% of premium mattress manufacturers integrate pressure-relief flexible foam layers to improve comfort performance and product durability.

A 2025 industrial foam modernization project in East Asia reduced energy consumption by 16% and shortened production cycle times by 13%.

Top manufacturers collectively control nearly 38% market share, with competition centered on product innovation, recycling capability, and regional capacity expansion.

ESG regulations and low-emission material mandates lowered volatile organic compound output by nearly 21% across advanced production facilities.

Global investments exceeded USD 2.4 Billion between 2024 and 2026, focused on recycled polyols, regional supply chain expansion, and next-generation sustainable foam solutions.

Flexible foam demand remains concentrated in furniture, bedding, automotive, and packaging industries, which collectively contribute more than 72% of total global consumption. Manufacturers are accelerating adoption of low-VOC formulations, recycled polyols, and digitally controlled foaming systems that improve material consistency by nearly 15%. Asia-Pacific continues leading regional demand with over 48% market share, while North America is expanding high-performance automotive foam applications. Growing localization strategies following global logistics disruptions are strengthening regional production networks, and bio-based flexible foam innovation is emerging as a long-term competitive differentiator shaping future strategic investments.

The flexible foam market is transforming into a high-priority investment arena as automotive lightweighting, premium bedding demand, and sustainable material transitions accelerate simultaneously across global manufacturing networks. Advanced flexible polyurethane systems are optimizing thermal insulation, acoustic control, and cushioning efficiency while reducing component weight by nearly 20% across mobility and furniture applications. Regulatory pressure on emissions and waste generation is forcing manufacturers to shift toward recyclable polyols and low-VOC production technologies, particularly across Europe and North America where compliance-linked procurement standards tightened sharply between 2024 and 2026.

AI-enabled foam processing and precision robotic cutting systems are redefining operational economics. Automated digital foaming technology improves production efficiency by 17% while reducing conversion costs by 13% compared to legacy batch-based systems. Asia-Pacific leads in production volume with more than 48% market share, while Europe leads in sustainable foam innovation, where bio-based flexible foam penetration exceeded 26% in advanced furniture manufacturing clusters. Over the next three years, smart manufacturing integration is projected to lower raw material waste by 14% and reduce production downtime by nearly 11%. A 2025 automotive seating modernization project in South Korea improved foam durability performance by 19% through advanced cell-structure optimization and automated density control.

ESG positioning is becoming a measurable competitive advantage as recycled-content flexible foam lowers compliance costs and improves supplier access across export-oriented industries. Global manufacturers are accelerating capital allocation toward regional production hubs, recycled feedstock integration, and high-performance specialty foam portfolios to strengthen supply resilience after recent logistics disruptions. Companies that control sustainable material innovation, automation capability, and regional manufacturing flexibility will define long-term competitive leadership in the evolving global flexible foam market.

The accelerating shift toward lightweight and energy-efficient manufacturing is forcing flexible foam producers to expand advanced polyurethane and specialty foam capacity across automotive, furniture, and insulation sectors. Automotive interior manufacturers reduced average seating system weight by nearly 18% between 2023 and 2026 through high-resilience flexible foam integration, directly improving electric vehicle range efficiency and cabin acoustics. Simultaneously, premium bedding demand increased more than 21% globally as consumers shifted toward pressure-relief and ergonomic comfort solutions with higher durability cycles. Supply chain restructuring following Asia-Europe logistics disruptions pushed manufacturers to regionalize production and secure localized raw material partnerships to reduce lead-time exposure by approximately 15%. This structural demand expansion is accelerating investment into automated foam conversion technologies and low-emission production systems. Advanced digital foaming platforms improved output consistency by 16% while reducing scrap generation by nearly 12% compared to conventional production lines. In response, companies are expanding regional manufacturing footprints, entering strategic chemical supply partnerships, and increasing recycled polyol integration to stabilize procurement costs and strengthen long-term operational resilience. The market is no longer competing solely on production scale; it is increasingly defined by material performance, sustainability compliance, and supply chain agility.

Flexible foam manufacturers remain heavily exposed to petrochemical feedstock volatility, particularly in polyurethane precursor materials where pricing fluctuations exceeded 22% during recent global energy-market instability. Dependence on concentrated supply networks for isocyanates and polyols continues constraining production predictability, especially after shipping disruptions across critical trade corridors increased procurement lead times by nearly 17%. At the same time, stricter VOC emission regulations across Europe and North America are forcing costly production upgrades, adding compliance-related operating expenses of approximately 9% for mid-sized manufacturers lacking advanced processing infrastructure. These structural pressures are directly affecting scalability, margin consistency, and long-term investment planning. Smaller producers face increasing difficulty securing stable raw material contracts, while export-focused manufacturers encounter tighter sustainability certification requirements for international market access. In response, companies are diversifying supplier bases, accelerating recycled-content material development, and negotiating long-term procurement agreements to reduce pricing exposure. Several manufacturers are also investing in bio-based foam technologies and localized sourcing models to minimize dependence on volatile petrochemical supply chains. The competitive gap is widening between technologically integrated producers and cost-sensitive manufacturers operating with legacy infrastructure.

The transition toward sustainable and performance-optimized flexible foam systems is creating high-impact growth opportunities across automotive, healthcare, packaging, and smart furniture applications. Bio-based flexible foam adoption increased more than 18% globally between 2024 and 2026 as manufacturers prioritized lower-emission materials and circular production models. Simultaneously, smart manufacturing systems integrating AI-driven density control and robotic foam cutting improved material utilization efficiency by nearly 15%, reducing conversion waste and enhancing production precision. Emerging markets in India, Vietnam, and Mexico are also generating new demand pockets as localized furniture and EV manufacturing ecosystems expand rapidly. A major future signal is the rise of recyclable mono-material foam systems designed for easier post-consumer recovery and lower compliance costs. Advanced open-cell foam technologies are improving airflow efficiency by approximately 20% in premium bedding applications while extending product durability cycles. Companies are positioning aggressively through R&D expansion, recycled polyol partnerships, and vertically integrated manufacturing ecosystems that combine raw material processing with downstream customization capabilities. The market is increasingly rewarding manufacturers that can simultaneously deliver sustainability compliance, operational efficiency, and premium product differentiation at industrial scale.

Despite strong demand momentum, the market faces significant execution barriers linked to infrastructure modernization, sustainability compliance, and performance standardization. More than 34% of existing flexible foam production facilities still rely on aging processing systems with limited automation capability, constraining scalability and quality consistency. High energy consumption in foam curing and chemical processing operations continues pressuring manufacturers as industrial electricity costs increased by nearly 12% across several major production regions between 2024 and 2026. In parallel, stricter environmental regulations are forcing rapid transitions toward low-emission formulations that often require costly reformulation and testing cycles. The challenge extends beyond cost pressure into long-term competitive sustainability. Manufacturers must balance lightweight performance, recyclability, durability, and fire-safety compliance without compromising production efficiency. Adoption barriers remain particularly high in emerging markets where advanced recycling infrastructure and skilled automation talent are still developing. Companies unable to modernize operations risk slower production cycles, reduced export competitiveness, and weaker supplier positioning. To remain competitive, industry leaders are accelerating investment into digital production systems, regional technical partnerships, and next-generation sustainable chemistry platforms capable of supporting both regulatory compliance and high-volume industrial scalability.

15% Reduction in Foam Waste Through AI-Driven Manufacturing Optimization Flexible foam producers are rapidly deploying AI-enabled density monitoring, robotic cutting systems, and automated mixing platforms to improve precision across high-volume production lines. Smart process integration reduced material waste by nearly 15% while improving batch consistency by 13% across automotive and bedding applications. Manufacturers are restructuring legacy operations and scaling digitally controlled foaming systems to offset labor shortages and rising energy costs. The shift is reshaping factory economics by shortening production cycles and lowering defect-related reprocessing costs.

22% Increase in Recycled Polyol Integration Across Global Production Networks Sustainability execution has moved from pilot stage to large-scale deployment as producers accelerate recycled-content integration into mainstream foam manufacturing. Recycled polyol utilization increased by 22% between 2024 and 2026, particularly in Europe where low-emission compliance requirements tightened across furniture and packaging sectors. Companies are forming regional feedstock partnerships and redesigning procurement models to stabilize raw material access following petrochemical supply disruptions. A non-obvious shift is emerging where recycled-content certification is becoming a procurement requirement rather than a branding advantage.

18% Expansion in Automotive Foam Customization for Electric Vehicle Platforms Automotive manufacturers are demanding application-specific flexible foam systems optimized for lightweighting, vibration control, and thermal insulation in EV interiors. Customized foam deployment increased by 18% as automakers shifted toward modular seating and noise-reduction architectures. Suppliers are responding through rapid prototyping partnerships and localized production expansion to reduce delivery lead times by approximately 12%. The market is redefining supplier competitiveness around engineering flexibility rather than production scale alone.

14% Growth in Regionalized Manufacturing and Short-Cycle Supply Models Flexible foam manufacturers are accelerating regional production restructuring to reduce logistics exposure and improve delivery responsiveness after recent shipping instability across global trade corridors. Regional sourcing adoption increased by 14%, while localized conversion facilities improved order fulfillment speed by nearly 16% in furniture and packaging applications. Companies are optimizing near-market manufacturing strategies, particularly across India, Mexico, and Southeast Asia, where demand visibility and lower transportation dependency are strengthening operational resilience and margin protection.

The flexible foam market is segmented by type, application, and end-user industries, with demand strongly concentrated in polyurethane-based products and high-volume furniture and bedding applications. Polyurethane foam continues dominating due to its cost efficiency, lightweight properties, and large-scale integration across automotive interiors, mattresses, and insulation systems. Automotive and packaging applications are also gaining strategic importance as manufacturers prioritize lightweighting and protective material efficiency. More than 42% of total demand remains tied to furniture and bedding sectors, while automotive-related consumption increased by approximately 11% due to electric vehicle production expansion. Demand distribution is shifting toward recyclable and high-resilience foam solutions as regulatory compliance and operational efficiency become purchasing priorities. Companies are increasingly aligning product portfolios around application-specific performance, regional supply flexibility, and sustainable material integration to capture evolving industrial demand patterns.

Polyurethane Foam dominates the flexible foam market with approximately 58% share due to its superior cushioning performance, scalability, low conversion cost, and broad integration across furniture, bedding, automotive, and insulation industries. Its structural dominance is reinforced by high production flexibility and compatibility with automated foaming systems that improve manufacturing efficiency by nearly 14%. Manufacturers continue expanding polyurethane processing capacity and investing in low-VOC and recycled-content formulations to maintain competitive positioning amid tightening environmental standards. EVA Foam is emerging as the fastest-growing segment, with adoption increasing by nearly 16% due to rising demand for lightweight, durable, and impact-resistant materials in automotive interiors and specialty packaging. Compared to Polyurethane Foam, EVA Foam offers stronger moisture resistance and higher dimensional stability, making it increasingly attractive for premium and technical applications despite higher production costs. Polyethylene Foam and PVC Foam collectively account for nearly 27% of market demand, serving niche requirements in protective packaging, insulation, and industrial cushioning where chemical resistance and structural rigidity remain critical.

Demand is shifting toward performance-engineered and sustainable foam materials, forcing companies to optimize specialty foam portfolios, expand regional production capacity, and accelerate advanced material innovation. Investment momentum remains strongest in recyclable polyurethane systems and high-performance EVA solutions where long-term industrial adoption is accelerating.

Furniture remains the leading application segment, accounting for nearly 34% of total flexible foam demand due to large-scale usage in sofas, chairs, and modular seating systems where comfort, lightweight structure, and durability are critical purchasing factors. High-volume residential and commercial furniture manufacturing continues driving consumption concentration, particularly across Asia-Pacific production hubs. Manufacturers are increasingly deploying automated foam shaping and high-resilience formulations to improve product lifespan and reduce material waste by approximately 12%. Automotive is the fastest-growing application segment, with demand increasing by nearly 15% as electric vehicle manufacturers prioritize lightweight interiors, acoustic insulation, and advanced seating comfort systems. Compared to the mature furniture segment, automotive applications are shifting toward engineered foam customization with stricter performance specifications and thermal management requirements. Bedding, Packaging, and Construction collectively contribute around 46% of market demand, supported by rising premium mattress consumption, protective packaging optimization, and energy-efficient insulation deployment.

Usage patterns are rapidly evolving toward specialized and recyclable foam applications, forcing manufacturers to reposition portfolios around application-specific performance and regional delivery responsiveness. Companies are scaling localized production facilities, strengthening OEM partnerships, and investing in sustainable material technologies to capture shifting demand across high-value industrial segments.

The Furniture Industry remains the leading end-user segment, contributing approximately 39% of global flexible foam consumption due to continuous demand for ergonomic seating, modular furniture systems, and premium comfort products. Large-scale dependency on flexible polyurethane foam across residential and commercial furniture manufacturing reinforces this concentration, particularly in China, Vietnam, and India where export-oriented production remains strong. Buyers are increasingly prioritizing durability, low-emission materials, and supply consistency, pushing manufacturers toward automated production systems and recycled-content integration. The Automotive Industry is the fastest-growing end-user segment, with demand expanding by nearly 14% as electric vehicle production accelerates globally. Compared to the mature furniture sector, automotive buyers are demanding highly customized foam systems optimized for lightweighting, thermal insulation, and vibration reduction. Packaging Industry and Construction Industry collectively represent around 37% of market demand, driven by protective logistics solutions and rising adoption of insulation materials in energy-efficient building projects.

Purchasing behavior is shifting toward long-term supply agreements, sustainable sourcing standards, and application-specific customization. Companies are responding through strategic OEM partnerships, regional manufacturing expansion, and advanced material R&D focused on recyclable and performance-engineered foam solutions. Future demand concentration is increasingly moving toward technically specialized and compliance-ready foam systems where operational reliability and sustainability alignment define competitive advantage.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Asia-Pacific continues leading in production scale and downstream manufacturing demand, supported by strong furniture, bedding, and automotive supply chains across China, India, and Southeast Asia. Europe holds nearly 24% market share and leads in sustainable foam innovation, where recycled polyol integration exceeded 26% across industrial foam manufacturing systems. North America contributes approximately 21% of global demand and is accelerating adoption of automated foam processing technologies that improved production efficiency by nearly 15%. Regional supply chain restructuring and stricter environmental compliance standards are reshaping sourcing strategies and manufacturing localization decisions globally. Companies are increasingly prioritizing Asia-Pacific for scale, Europe for advanced sustainable technologies, and North America for high-margin specialty foam deployment and automation-driven operational optimization.

North America accounts for nearly 21% of global flexible foam demand, driven primarily by automotive interiors, premium bedding, and high-performance furniture manufacturing. The United States dominates regional consumption due to strong electric vehicle production and rising adoption of ergonomic consumer products. Tightening emissions standards and increasing freight costs are forcing manufacturers to regionalize production and accelerate recycled-content foam integration. Automated foam conversion systems improved operational efficiency by approximately 15%, while smart density-control technologies reduced material waste by nearly 11% across major manufacturing facilities. Several producers expanded localized specialty foam capacity between 2024 and 2026 to reduce import dependency and improve delivery responsiveness. Enterprise buyers increasingly prioritize durability, compliance-ready materials, and stable regional sourcing, making North America a strategic market for high-value product innovation and advanced manufacturing investment.

Europe represents approximately 24% of the global flexible foam market, with Germany, Italy, and Poland serving as key production and innovation centers for automotive, furniture, and insulation applications. Strict low-VOC emission regulations and circular economy mandates are accelerating adoption of recyclable polyurethane systems and bio-based polyols across regional manufacturing networks. Recycled-content foam utilization increased by nearly 22% between 2024 and 2026, while automated low-emission production systems improved energy efficiency by approximately 13%. Manufacturers are restructuring operations around compliance-driven production and advanced material traceability to secure long-term procurement contracts with automotive and furniture OEMs. Enterprise buyers increasingly favor certified sustainable foam products despite higher initial costs, reinforcing Europe’s role as a technology and compliance-driven market where innovation speed directly influences competitive positioning and export access.

Asia-Pacific leads the global flexible foam market with nearly 48% demand share and the highest production concentration, supported by large-scale manufacturing ecosystems in China, India, Japan, and Vietnam. The region benefits from integrated chemical supply chains, lower conversion costs, and rapidly expanding automotive and furniture industries. Localized production adoption increased by approximately 18% as manufacturers optimized near-market supply models to improve export responsiveness and reduce logistics exposure after recent shipping disruptions. China alone accounts for over one-third of global flexible foam processing capacity, while India is emerging as a high-growth hub for bedding and automotive foam demand. Producers are scaling automated manufacturing systems and expanding specialty foam exports to capture rising international demand. Enterprise buyers continue prioritizing speed, cost efficiency, and scalable production, making Asia-Pacific critical for long-term manufacturing expansion and supply chain dominance.

South America contributes nearly 5% of global flexible foam demand, with Brazil and Argentina leading regional consumption through furniture manufacturing, automotive assembly, and packaging applications. Growing urban housing demand and expansion in localized consumer goods production are supporting increased foam utilization across residential and industrial sectors. However, volatile raw material pricing and infrastructure limitations continue constraining large-scale manufacturing modernization, particularly for smaller regional producers. Flexible foam adoption in packaging and bedding applications increased by approximately 12% between 2024 and 2026 as local manufacturers shifted toward cost-efficient cushioning materials. Several companies expanded domestic conversion operations to reduce import dependence and shorten product delivery cycles by nearly 10%. Enterprise buyers remain highly price-sensitive, prioritizing durability and affordability, positioning South America as a market with strong expansion potential but elevated operational and supply-chain execution risks.

The Middle East & Africa region accounts for approximately 7% of global flexible foam demand, supported by expanding construction, hospitality, automotive, and industrial packaging sectors across Saudi Arabia, the UAE, and South Africa. Large-scale infrastructure development and industrial diversification programs are accelerating deployment of insulation and cushioning materials across commercial and residential projects. Regional manufacturing modernization increased by nearly 14% between 2024 and 2026 as producers adopted automated foam conversion technologies to improve production efficiency and reduce import reliance. Several Gulf-based manufacturers expanded specialty foam processing capacity to support rising domestic demand and export opportunities. Enterprise procurement behavior increasingly favors durable, heat-resistant, and cost-efficient foam solutions tailored for climate-intensive operating environments. The region is emerging as a strategic growth zone where infrastructure investment, industrial localization, and manufacturing partnerships are reshaping long-term market positioning.

China – 34% market share in the Flexible Foam market due to its massive production capacity, integrated chemical supply chains, and dominant furniture and automotive manufacturing ecosystem.

United States – 19% market share in the Flexible Foam market driven by advanced automotive applications, premium bedding demand, and rapid adoption of automated foam manufacturing technologies.

The flexible foam market is dominated by competition between global polyurethane leaders, specialty material innovators, and regional cost-efficient manufacturers focused on automotive, furniture, bedding, and industrial applications. Major players including BASF SE, Covestro AG, Huntsman Corporation, Recticel, and Carpenter Co. collectively control nearly 38% of the market, competing aggressively on material performance, supply chain integration, and sustainable foam innovation. Global leaders are differentiating through low-VOC formulations, recycled polyol integration, and automated processing systems that improve production efficiency by approximately 15% while reducing material waste by nearly 12%.

Regional manufacturers compete primarily on conversion cost, localized supply responsiveness, and customized foam solutions for high-volume industrial buyers. Competitive intensity is increasing as companies expand regional manufacturing facilities, secure long-term chemical feedstock agreements, and accelerate strategic partnerships with automotive and furniture OEMs. Vertical integration is becoming a critical competitive shift, particularly as raw material volatility and compliance costs continue pressuring margins. Entry barriers remain high due to capital-intensive processing infrastructure, regulatory requirements, and advanced formulation expertise. Winning in this market increasingly depends on balancing scalable production, sustainability compliance, automation capability, and rapid application-specific customization.

BASF SE

Covestro AG

Huntsman Corporation

Carpenter Co.

Recticel

Rogers Corporation

Armacell International S.A.

Zotefoams plc

JSP Corporation

INOAC Corporation

Sekisui Chemical Co., Ltd.

Woodbridge Foam Corporation

UFP Technologies, Inc.

FoamPartner Group

Advanced automated foaming systems, AI-driven density control, and robotic cutting technologies are currently reshaping flexible foam manufacturing efficiency across automotive, bedding, and furniture applications. Smart process automation improved production consistency by nearly 17% while reducing material waste by approximately 14% compared to conventional batch-controlled systems. More than 46% of large-scale foam manufacturers integrated digitally monitored conversion systems by 2026 to optimize throughput and reduce operational downtime. Compared with legacy manual production environments, automated foam processing lowered defect-related rework costs by nearly 12%, strengthening supply reliability and margin stability for high-volume producers.

Emerging technologies are increasingly focused on recyclable polyurethane systems, bio-based polyols, and closed-loop foam recovery processes. Recycled-content integration increased by nearly 22% across advanced production facilities as manufacturers accelerated adoption of chemical recycling technologies capable of recovering reusable polyols from post-consumer foam waste. New-generation recyclable polyurethane formulations improve lifecycle material recovery efficiency by approximately 30% compared to conventional non-recyclable foam structures. Companies with vertically integrated recycling capabilities are gaining competitive advantage through compliance readiness, lower raw material dependency, and stronger procurement positioning with automotive and furniture OEMs.

Disruptive innovation between 2026 and 2028 will center on circular foam chemistry, lightweight engineered structures, and precision-customized foam performance systems. Open-cell advanced comfort foams improved airflow efficiency by nearly 20% in premium bedding applications, while modular EV seating systems accelerated demand for lightweight acoustic insulation materials. Manufacturers are increasingly deploying AI-enabled predictive quality systems and digital twin production models to shorten development cycles and improve scalability. Companies acting now on sustainable material integration, automation expansion, and recycling infrastructure development will secure long-term operational advantages as compliance pressure and application-specific performance standards intensify globally.

March 2025 – BASF introduced biomass balance flexible polyurethane foam systems for the North American furniture sector, enabling up to 75% reduction in product carbon footprint compared to conventional systems. The launch strengthens BASF’s sustainable foam positioning while helping furniture manufacturers meet tightening low-emission procurement standards. [Carbon Shift]

April 2025 – BASF presented its “Loop” polyurethane recycling technology at CHINAPLAS 2025, enabling recycled polyol incorporation of up to 20 wt% into new flexible foam formulations. The development advances closed-loop foam manufacturing and strengthens recycled-content scalability across automotive and furniture applications. [Closed-Loop Scaling]

April 2024 – Covestro expanded circular polyurethane initiatives at UTECH Europe 2024, highlighting lower-carbon foam technologies and recyclable material systems for insulation and mattress applications. The initiative accelerated industry adoption of circular raw materials while improving sustainability integration across high-volume foam manufacturing sectors. [Circular Materials Push]

April 2024 – BASF introduced mechanically recyclable flexible PU foams at UTECH 2024, enabling 100% recyclability through thermoplastic recovery processes. The innovation supports end-of-life foam reuse in furniture manufacturing while reducing dependence on virgin petrochemical feedstocks and improving long-term circularity economics. [Recyclable Foam Breakthrough]

The Flexible Foam Market Report delivers comprehensive analysis across product types including Polyurethane Foam, Polyethylene Foam, EVA Foam, and PVC Foam, alongside key applications such as Furniture, Bedding, Automotive, Packaging, and Construction. The study evaluates demand patterns across major end-user industries including furniture manufacturing, automotive production, packaging operations, and infrastructure development. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic country-level assessment focused on manufacturing concentration, technology deployment, and regional supply-chain positioning. The report also covers emerging technologies including recyclable polyurethane systems, AI-enabled foam processing, automated cutting systems, and bio-based polyol integration.

The analysis incorporates more than 25 strategic market indicators covering adoption rates, material transition trends, production optimization, sustainability integration, and application-specific performance demand. Polyurethane foam currently accounts for nearly 58% of product adoption, while recycled-content foam integration exceeded 22% across advanced industrial manufacturing facilities between 2024 and 2026. The report profiles major global manufacturers, evaluates competitive positioning, and tracks operational shifts including regionalized production expansion and circular manufacturing initiatives.

From 2026 to 2033, the report provides forward-looking insights into specialty foam innovation, lightweight automotive applications, sustainable material adoption, and advanced manufacturing transformation. It supports investment planning, capacity expansion decisions, procurement strategy, competitive benchmarking, and long-term market positioning for manufacturers, suppliers, investors, and industrial decision-makers operating across the global flexible foam ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1997 Million |

|

Market Revenue in 2033 |

USD 3158.97 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Covestro AG, Huntsman Corporation, Carpenter Co., Recticel, Rogers Corporation, Armacell International S.A., Zotefoams plc, JSP Corporation, INOAC Corporation, Sekisui Chemical Co., Ltd., Woodbridge Foam Corporation, UFP Technologies, Inc., FoamPartner Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |