Reports

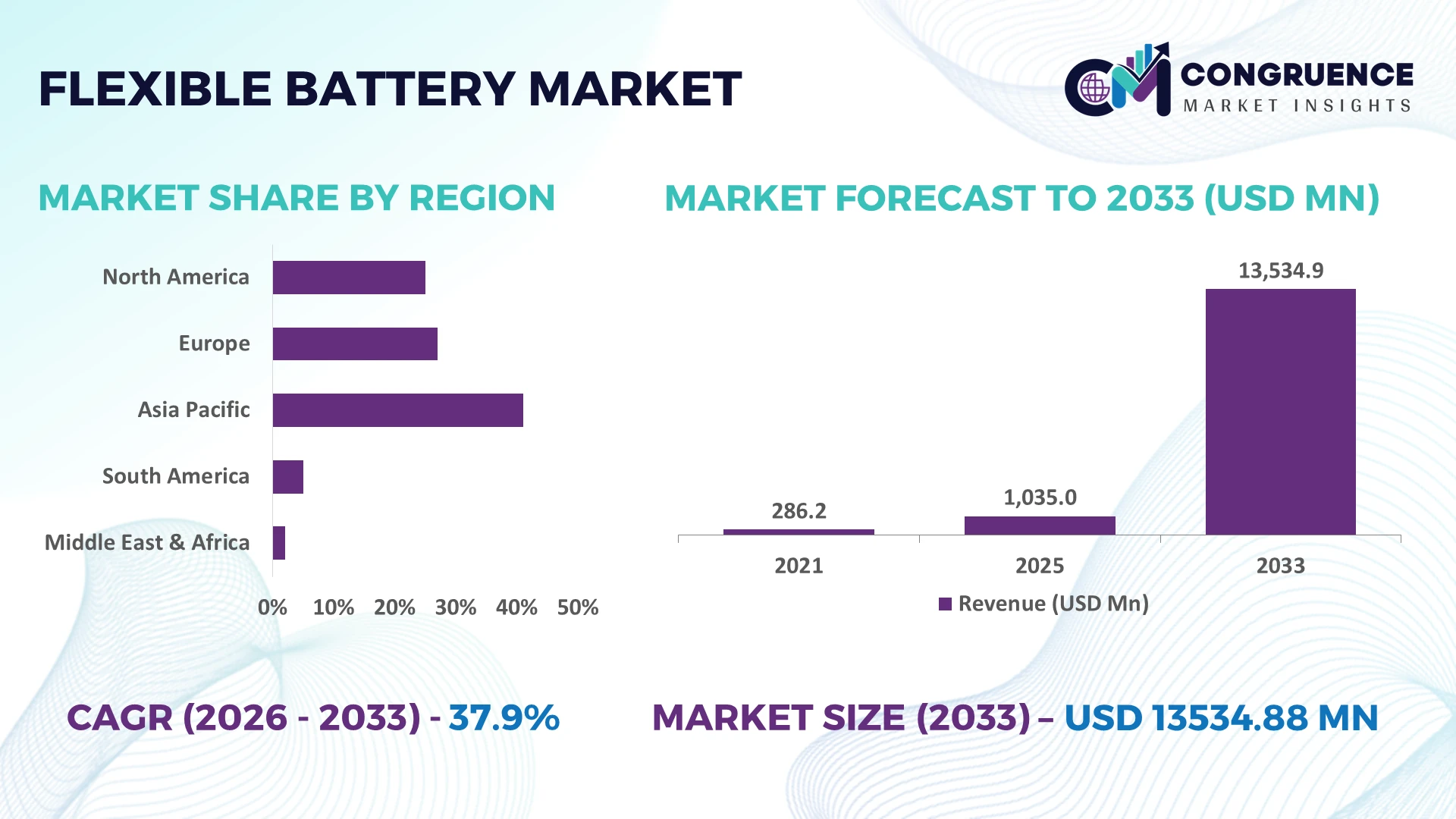

The Global Flexible Battery Market was valued at USD 1035 Million in 2025 and is anticipated to reach a value of USD 13534.88 Million by 2033 expanding at a CAGR of 37.9% between 2026 and 2033. Growth is driven by rapid integration of ultra-thin energy storage into wearable electronics, smart medical devices, electronic skin, and IoT sensors requiring lightweight, bendable, and high-cycle-performance battery technologies.

China remains the dominant manufacturing hub, accounting for approximately 48% of global flexible battery production capacity, supported by strong investments in advanced electronics, electric mobility components, and battery materials. South Korea follows with nearly 16% capacity, leveraging high-value display and semiconductor industries for next-generation battery integration. Continued supply-chain diversification beyond East Asia after geopolitical trade realignments has accelerated localized production strategies while improving component resilience.

Manufacturers investing in scalable production, advanced materials, and diversified regional supply networks are positioned to secure long-term competitive advantages across high-growth application segments.

Market Size & Growth: USD 1,035 million in 2025 reaching USD 13,534.88 million by 2033 at 37.9% CAGR, driven by expanding wearable electronics and printed medical device integration.

Top Growth Drivers: Wearable electronics demand exceeds 30%, medical sensor deployment grows over 24%, and IoT device integration expands above 28% globally.

Short-Term Forecast: By 2028, manufacturing costs decline nearly 18% through automated production and improved thin-film material utilization.

Emerging Technologies: AI-enabled battery management, solid-state flexible cells, and printable energy storage improve cycle life by more than 25%.

Regional Leaders: Asia-Pacific surpasses USD 7 billion, North America exceeds USD 3 billion, Europe approaches USD 2 billion, supported by regional manufacturing expansion and electronics innovation.

Consumer/End-User Trends: More than 40% of next-generation wearable device designs incorporate flexible power solutions for thinner and lighter products.

Pilot/Case Example: In 2026, flexible healthcare monitoring deployments improved continuous device operating efficiency by approximately 22% using ultra-thin rechargeable batteries.

Competitive Landscape: Leading manufacturers collectively control around 42% market share alongside Panasonic, Samsung SDI, Enfucell, Blue Spark Technologies, and LG Energy Solution.

Regulatory & ESG Impact: Manufacturing waste reductions exceeding 15% support cleaner battery production while regional localization strengthens supply-chain resilience.

Investment & Funding: More than USD 2 billion supports manufacturing expansion, strategic partnerships, and advanced material commercialization amid global production shifts.

Innovation & Future Outlook: Stretchable batteries, graphene-enhanced electrodes, and scalable printed manufacturing accelerate commercialization across medical, industrial, and smart packaging applications.

Flexible Battery Market continues expanding across wearable healthcare, smart packaging, connected sensors, and flexible consumer electronics where lightweight power solutions deliver greater design freedom. Recent advances in printable solid-state architectures and high-energy-density materials have improved energy efficiency by approximately 20%, while regional manufacturing diversification and evolving battery compliance standards strengthen supply resilience, setting the stage for broader strategic market evaluation.

Flexible batteries are becoming a strategic technology platform as manufacturers compete to deliver thinner, lighter, and connected electronic products across healthcare, industrial IoT, consumer electronics, and smart packaging. The market is benefiting from supply-chain restructuring that encourages localized battery manufacturing and material sourcing, reducing dependence on single-country suppliers while strengthening production resilience. This shift is accelerating investment decisions for companies seeking secure component availability and faster product commercialization.

Compared with conventional rigid lithium-ion cells, advanced flexible batteries reduce device thickness by nearly 40% and improve space utilization by approximately 30% in compact electronics, enabling new product designs without compromising portability. China leads high-volume manufacturing through integrated battery and electronics ecosystems, while Japan and South Korea concentrate on premium materials and next-generation flexible cell innovation. During the next two to three years, automated roll-to-roll production is expected to increase manufacturing throughput by roughly 20%, improving consistency for medical wearables and industrial sensor applications.

A practical example is continuous patient-monitoring patches, where flexible batteries enable uninterrupted operation while improving user comfort and device durability. Companies are expanding material partnerships, investing in printable battery technologies, and establishing localized production capabilities to strengthen commercialization. Organizations that integrate scalable manufacturing, advanced materials, and diversified supply networks will achieve stronger competitive positioning as flexible energy storage becomes a core enabler of connected electronic ecosystems.

The rapid expansion of wearable electronics, connected medical devices, and industrial IoT platforms remains the primary catalyst for flexible battery adoption. More than 35% of new wearable product designs now prioritize ultra-thin power solutions, while printed electronics manufacturing efficiency has improved by approximately 22% through automated production processes. China continues expanding flexible electronics manufacturing capacity, supported by industrial policies encouraging advanced battery materials and localized supply chains. This combination of technology adoption and manufacturing scale is prompting battery producers to increase production capacity, establish development partnerships with device manufacturers, and accelerate commercialization of high-energy-density flexible cells, creating faster product development cycles and stronger supply reliability.

Commercial deployment continues to face pressure from volatile prices for specialty polymers, conductive materials, and advanced electrode components. Raw material costs for certain flexible battery inputs have fluctuated by nearly 18% in recent procurement cycles, while imported specialty materials account for over 50% of selected production requirements in several manufacturing hubs. South Korean and Japanese producers continue facing supply concentration risks for premium functional materials, affecting production planning and inventory management. Companies are responding through supplier diversification, localized procurement agreements, and alternative electrode chemistry development, improving procurement stability while protecting manufacturing margins and supporting consistent product availability.

Printable battery technology is creating new commercial opportunities beyond traditional consumer electronics. Flexible power systems improve manufacturing efficiency by approximately 25% in smart labels and disposable medical devices while enabling product miniaturization for next-generation healthcare monitoring. India and Singapore are strengthening innovation ecosystems supporting printed electronics research and advanced medical technology manufacturing. Companies are increasing R&D investments, forming partnerships with healthcare device developers, and expanding pilot production for printable solid-state batteries. A notable strategic advantage lies in integrating flexible energy storage directly into product substrates, reducing assembly complexity while enabling differentiated product performance across emerging industrial applications.

Maintaining consistent electrochemical performance during mass production remains a significant execution challenge as commercial volumes increase. Manufacturing yield variations of approximately 12% continue affecting production efficiency, while flexible battery durability requirements have increased by nearly 30% for medical and industrial applications. Germany and Japan continue tightening quality standards for advanced electronic components, requiring higher manufacturing precision and extensive validation procedures. Companies must expand automated quality inspection, invest in advanced coating technologies, and strengthen collaborative testing with device manufacturers. Successfully achieving large-scale production consistency will determine long-term competitiveness, product reliability, and qualification across regulated, high-value application markets.

Advanced Manufacturing Automation Roll-to-roll production lines are increasing manufacturing throughput by approximately 20% while reducing material waste by nearly 15%, enabling higher-volume flexible battery fabrication with consistent quality. Labor shortages and production localization initiatives in China and South Korea are accelerating factory automation, prompting manufacturers to scale digital quality inspection and automated coating technologies that shorten production cycles and improve operational efficiency.

Medical Wearables Redefine Design Flexible battery integration in healthcare devices has expanded by nearly 28%, while ultra-thin rechargeable cells reduce device thickness by around 35% compared with conventional battery configurations. Stricter medical device performance requirements are encouraging battery suppliers to collaborate directly with healthcare equipment manufacturers, strengthening product validation processes and accelerating customized energy-storage development for continuous patient monitoring.

Localized Material Supply Networks Battery manufacturers have reduced dependence on single-country sourcing by approximately 18% through supplier diversification and regional material qualification programs. Geopolitical trade adjustments and critical material security concerns are driving procurement restructuring, leading companies to establish long-term supply agreements, expand localized component processing, and improve production continuity across advanced electronics manufacturing ecosystems.

Printable Energy Storage Expansion Printed flexible batteries now improve production efficiency by nearly 22% in smart labels and disposable electronics while lowering assembly complexity by approximately 17%. Japan and Singapore continue advancing printed electronics ecosystems through collaborative research, encouraging battery developers to expand pilot manufacturing, strengthen material partnerships, and commercialize scalable integrated power solutions for industrial sensing and intelligent packaging.

Lithium-Ion batteries remain the leading segment because they combine high energy density, established manufacturing ecosystems, and broad compatibility with wearable electronics, medical devices, and consumer products. Nearly 55% of commercial flexible battery deployments continue using lithium-ion chemistry due to proven reliability and scalable production. Printed Batteries are expanding steadily across smart packaging and disposable electronics, while Thin-Film batteries maintain strategic importance in compact sensors requiring ultra-thin profiles. Zinc-Based batteries remain relevant for safe, low-power applications where environmental considerations and simplified disposal provide operational advantages.

Solid-State Batteries represent the fastest-growing segment as manufacturers target improved safety, higher energy density, and longer operational life. Prototype commercialization has increased by approximately 30%, while energy density improvements exceeding 20% are supporting broader investment. Companies are expanding pilot production, collaborating with advanced material developers, and strengthening intellectual property portfolios to accelerate commercialization. Investment priorities are increasingly shifting toward solid-state architectures capable of supporting next-generation medical wearables and industrial electronics.

Wearable Devices remain the largest application segment as fitness trackers, smartwatches, electronic textiles, and continuous health-monitoring products require lightweight, flexible energy storage. More than 45% of flexible battery deployments support wearable platforms, where compact form factors and mechanical durability are essential. Consumer Electronics continues representing a mature demand base through foldable products and compact accessories, while Smart Cards maintain stable adoption in secure identification and financial applications requiring thin integrated power sources.

Medical Devices are emerging as the fastest-growing application as remote patient monitoring and disposable diagnostic systems expand globally. Flexible battery integration within connected healthcare equipment has increased by approximately 27%, while IoT Devices continue recording deployment growth above 24% through industrial sensing and asset monitoring. Manufacturers are strengthening automation, expanding production partnerships, and developing customized battery formats to meet application-specific requirements, ensuring greater reliability across connected device ecosystems.

Electronics remains the dominant end-user segment due to sustained demand from wearable devices, foldable displays, wireless accessories, and connected consumer products. Approximately 58% of flexible battery utilization originates from electronics manufacturing, supported by continuous product miniaturization and integration requirements. Consumer Goods continue adopting flexible batteries in intelligent packaging and premium connected products, while Industrial users deploy them within wireless monitoring equipment and predictive maintenance systems where compact energy storage improves installation flexibility.

Healthcare is the fastest-growing end-user as digital diagnostics, remote monitoring, and smart therapeutic devices become operational priorities. Flexible battery adoption within healthcare equipment has expanded by nearly 29%, while Automotive manufacturers are increasing evaluation of flexible energy storage for intelligent interiors and advanced sensing systems. Companies are responding through sector-specific product customization, strategic partnerships with original equipment manufacturers, and ecosystem-focused development strategies that strengthen competitive differentiation across specialized application environments.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 40.8% between 2026 and 2033.

Strategic Innovation Driven by Advanced Healthcare and Wearable Manufacturing

North America maintains its leadership through strong commercialization of wearable electronics, digital healthcare platforms, and high-value flexible electronics manufacturing. The region contributes nearly 37% of global demand, supported by established semiconductor ecosystems, advanced battery research, and strong enterprise investment in connected medical technologies. More than 45% of next-generation wearable product launches integrate flexible power solutions to achieve thinner device architectures and extended operating performance. Battery developers are expanding pilot-scale manufacturing, strengthening partnerships with healthcare technology firms, and increasing automated production capabilities to improve product consistency. Ongoing investment in printed electronics and advanced materials continues enhancing commercialization while reducing development timelines for flexible battery-enabled devices.

United States Market Outlook: The United States leads regional deployment through its strong ecosystem of medical device manufacturers, wearable technology companies, and advanced battery innovators. More than 60% of North America's flexible battery research programs originate in the country, supported by extensive university-industry collaboration and private-sector investment. Companies continue expanding prototype manufacturing, accelerating product validation, and strengthening domestic battery supply capabilities to improve commercialization speed across healthcare and consumer electronics applications.

Sustainability Standards Accelerate Advanced Battery Integration

Europe continues strengthening its position through sustainable battery manufacturing, advanced material innovation, and strict product quality standards. The region accounts for approximately 25% of global market activity, supported by strong electronics engineering capabilities and expanding investments in environmentally responsible battery technologies. Manufacturers have improved material recovery efficiency by nearly 18% through circular production initiatives, while collaborative development projects continue advancing solid-state and printable battery platforms. Industrial modernization and battery compliance requirements are encouraging companies to redesign manufacturing workflows, improve traceability, and establish strategic partnerships across the electronics value chain for long-term operational resilience.

Germany Market Outlook: Germany remains the region's technological leader through its advanced industrial automation capabilities and precision manufacturing expertise. Around 35% of Europe's advanced battery pilot manufacturing initiatives are concentrated in Germany, supported by strong collaboration between industrial equipment suppliers, research institutes, and electronics manufacturers. Companies continue investing in automated production systems and high-performance battery materials to strengthen manufacturing competitiveness and support premium electronics applications.

Manufacturing Scale Powers Global Expansion

Asia-Pacific serves as the world's manufacturing center for flexible batteries through integrated electronics production, material processing, and large-scale battery fabrication. The region accounts for nearly 43% of global production capacity, supported by established supply networks and expanding investments in advanced manufacturing infrastructure. Production efficiency has improved by approximately 21% through automated roll-to-roll manufacturing and digital quality control systems. Leading manufacturers continue increasing export capacity, expanding strategic partnerships, and investing in next-generation battery materials to meet growing demand from wearable electronics, healthcare devices, and industrial IoT applications.

China Market Outlook: China dominates global flexible battery manufacturing through integrated supply chains, large-scale electronics production, and extensive battery material processing capabilities. Nearly 48% of worldwide flexible battery manufacturing capacity is concentrated in China, supported by continuous factory modernization and domestic component availability. Manufacturers continue expanding production facilities, increasing automation, and strengthening partnerships with consumer electronics and medical device companies to maintain global manufacturing leadership.

Industrial Digitalization Supports Emerging Adoption

South America is steadily increasing flexible battery adoption through industrial digitalization, connected healthcare expansion, and growing consumer electronics demand. The region contributes approximately 7% of global deployment, with adoption concentrated in industrial monitoring, logistics tracking, and healthcare applications. Deployment of connected industrial sensors has increased by nearly 19%, encouraging battery suppliers to strengthen regional distribution and technical support capabilities. Infrastructure limitations remain a constraint for large-scale manufacturing, yet companies are responding through localized partnerships, product customization, and expanded technical collaboration to improve market accessibility and operational efficiency.

Brazil Market Outlook: Brazil leads regional demand through its expanding electronics assembly industry, healthcare modernization initiatives, and industrial automation investments. More than 45% of South America's flexible battery deployments are concentrated within Brazil, supported by increasing adoption of connected medical equipment and industrial monitoring systems. Companies continue expanding distribution partnerships and localized service capabilities to strengthen market penetration while supporting growing domestic demand for advanced electronic devices.

Technology Investment Strengthens Digital Infrastructure

The Middle East & Africa market is advancing through digital infrastructure investments, healthcare modernization, and smart city development programs that increasingly require compact energy storage solutions. The region represents approximately 5% of global market activity, with deployment focused on connected healthcare equipment, intelligent identification systems, and industrial monitoring technologies. Smart infrastructure projects have increased advanced electronics deployment by nearly 17%, encouraging battery suppliers to establish regional partnerships and technical support networks. Companies are prioritizing localized distribution, technology collaboration, and specialized product offerings to improve deployment efficiency while supporting emerging digital ecosystems.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's primary innovation hub through substantial investment in smart infrastructure, healthcare technology, and advanced digital services. Approximately 30% of regional pilot deployments for flexible electronic solutions are concentrated in the country, supported by technology partnerships and innovation-focused industrial policies. Companies continue expanding demonstration projects, enterprise collaborations, and regional distribution operations to accelerate commercialization of flexible battery-enabled solutions.

Competition in the Flexible Battery Market is led by Panasonic, Samsung SDI, LG Energy Solution, Enfucell, and Blue Spark Technologies, while specialized printed-battery developers compete against large lithium-ion manufacturers and regional material suppliers. The top five participants collectively account for approximately 46% of market activity, creating a moderately concentrated structure where technology leadership outweighs pricing alone. Premium manufacturers compete through higher energy density, flexible form factors, and product reliability, whereas cost-focused suppliers emphasize manufacturing efficiency and localized sourcing. Automated production has reduced manufacturing costs by nearly 18%, while advanced material optimization improves energy density by approximately 22%, strengthening competitive differentiation. Companies are expanding pilot manufacturing, forming joint development partnerships with wearable and medical device manufacturers, and increasing vertical integration across electrode materials and flexible substrates to secure supply continuity. Competition is shifting toward proprietary materials and scalable production rather than commodity pricing. High qualification requirements, intellectual property portfolios, and precision manufacturing create significant entry barriers. Winning requires scalable manufacturing, advanced material innovation, dependable supply networks, and rapid commercialization with application-specific customization.

Panasonic Corporation

Samsung SDI Co., Ltd.

LG Energy Solution Ltd.

Enfucell Oy

Blue Spark Technologies, Inc.

BrightVolt, Inc.

Ultralife Corporation

STMicroelectronics N.V.

Molex LLC

Jenax Inc.

Imprint Energy, Inc.

Ilika plc

Flexible battery technology is advancing through solid-state electrolytes, printable battery architectures, and ultra-thin lithium-ion cell designs that support compact electronics without sacrificing performance. Solid-state flexible cells improve safety while increasing energy density by approximately 20%, and printable battery manufacturing reduces material waste by nearly 15%. Around 40% of new wearable device development programs now evaluate flexible energy-storage integration during early product design, enabling manufacturers to shorten development cycles and improve product differentiation across healthcare and consumer electronics.

Emerging manufacturing technologies are replacing conventional batch production with automated roll-to-roll fabrication and AI-enabled quality inspection. Compared with legacy production methods, automated manufacturing improves throughput by approximately 25% while reducing defect rates by nearly 18%. Companies with integrated production capabilities gain stronger supply-chain control and faster commercialization, whereas specialized battery innovators benefit from licensing advanced materials and customized cell architectures for niche medical and industrial applications.

Between 2026 and 2028, graphene-enhanced electrodes, stretchable conductive materials, and hybrid solid-state battery platforms are expected to reshape competitive positioning. Adoption of digital manufacturing systems is projected to exceed 50% among leading producers, enabling faster process optimization and consistent product quality. Organizations investing early in advanced materials, automated production, and collaborative product development will strengthen operational resilience, accelerate qualification with original equipment manufacturers, and secure long-term advantages in high-value flexible electronics markets.

January 2024 BrightVolt introduced next-generation flexible lithium-ion batteries for IoT and wearable applications, emphasizing reduced weight and higher energy capacity to improve compact device performance and extend operating life across connected electronics. Source: brightvolt.com

March 2024 Jenax unveiled its J.Flex flexible battery featuring higher energy density and enhanced mechanical flexibility, enabling improved performance for smart textiles and electronic skin applications while expanding commercialization opportunities in wearable electronics. Source: jenax.com

May 2024 Imprint Energy launched the ZT flexible battery for medical and wearable devices, delivering a lightweight, low-profile architecture that improves device integration while supporting greater design flexibility for next-generation healthcare products.

July 2025 Panasonic commenced operations at its Kansas battery facility capable of producing approximately 66 battery cells per second, strengthening manufacturing scale, supply resilience, and advanced battery production capabilities supporting global electronics and energy-storage markets.

This report provides a comprehensive assessment of the Flexible Battery Market by evaluating technology evolution, competitive positioning, manufacturing developments, and deployment patterns across the value chain. It analyzes five major battery types, five application categories, and five primary end-user industries while examining operational trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of current deployments remain concentrated in wearable electronics and connected healthcare, highlighting the market's transition toward high-value, application-specific energy storage.

The report delivers strategic intelligence covering advanced materials, printable batteries, solid-state innovation, manufacturing automation, and supply-chain localization between 2026 and 2033. It benchmarks leading companies, assesses regional production capabilities, and identifies shifting investment priorities, partnership strategies, and commercialization pathways. Business stakeholders can leverage these insights to evaluate expansion opportunities, strengthen competitive positioning, prioritize technology investments, and align product development with emerging demand across medical, industrial, consumer, and IoT ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1035 Million |

Market Revenue in 2033 | USD 13534.88 Million |

CAGR (2026 - 2033) | 37.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Panasonic Corporation, Samsung SDI Co., Ltd., LG Energy Solution Ltd., Enfucell Oy, Blue Spark Technologies, Inc., BrightVolt, Inc., Ultralife Corporation, STMicroelectronics N.V., Molex LLC, Jenax Inc., Imprint Energy, Inc., Ilika plc |

Customization & Pricing | Available on Request (10% Customization is Free) |