Reports

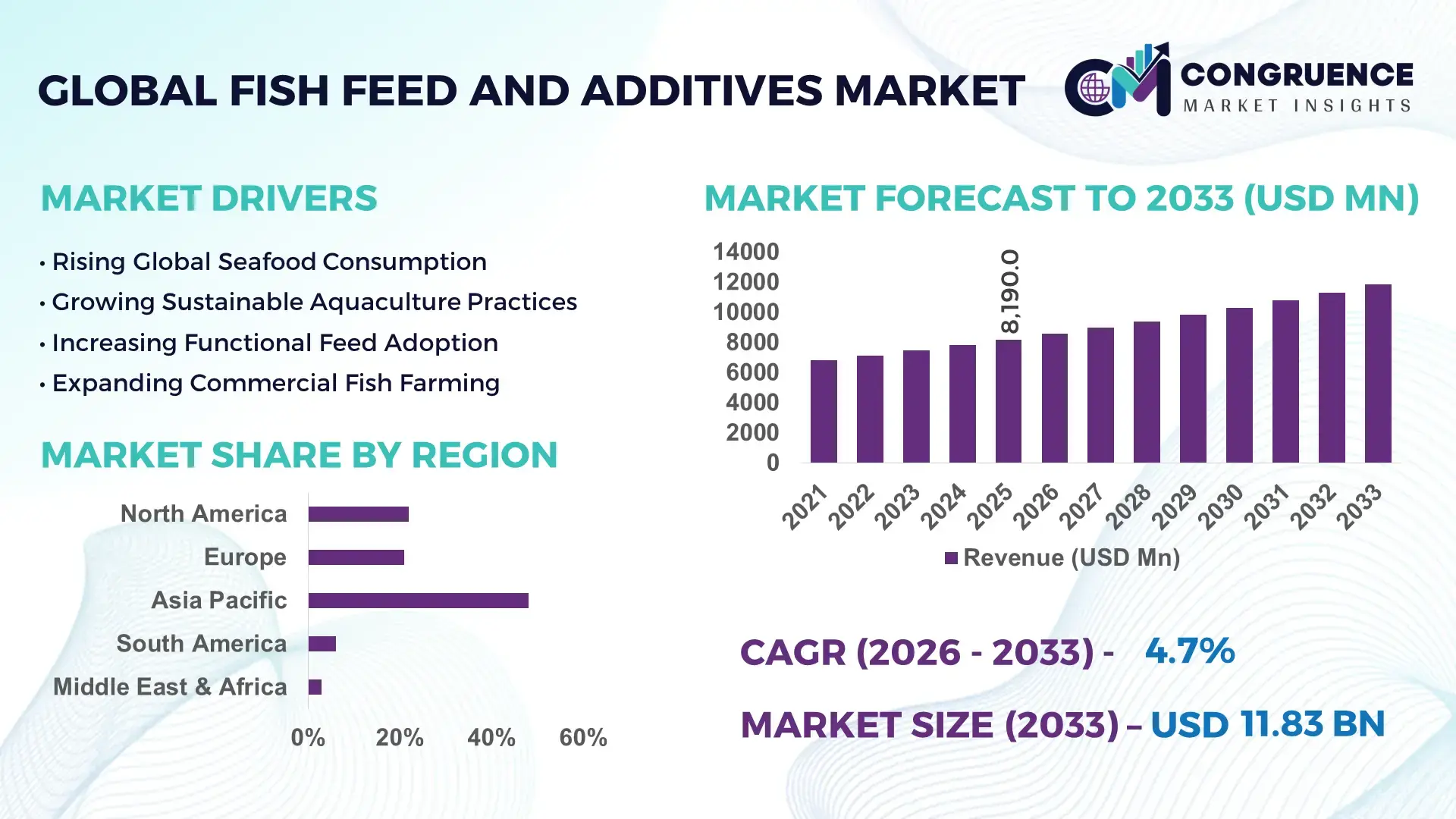

The Global Fish Feed and Additives Market was valued at USD 8,190.0 Million in 2025 and is anticipated to reach a value of USD 11,826.5 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. The market is accelerating due to precision aquaculture expansion, rising protein conversion optimization, and rapid adoption of functional feed additives that improve feed efficiency by over 18% while reducing fish mortality rates across intensive farming systems. Between 2024 and 2026, tightening marine ingredient supply chains, growing restrictions on antibiotic feed usage, and increasing investment in sustainable aquafeed production are reshaping procurement strategies across Asia-Pacific and Europe.

China continues to dominate the global Fish Feed and Additives Market with nearly 34% production share, supported by over 52 million metric tons of aquaculture output and aggressive modernization across inland farming systems. More than 46% of large-scale Chinese aquaculture operators have integrated enzyme-based and probiotic feed formulations to improve yield consistency and disease resistance. Compared with conventional fishmeal-heavy diets, advanced plant-protein and additive-enriched formulations reduce feed conversion ratios by nearly 15%, strengthening operational efficiency amid volatile raw material pricing. Rising seafood security concerns following Red Sea shipping disruptions and global fishmeal supply fluctuations are further accelerating regional feed localization investments.

Aquaculture production accounts for nearly 71% of total market demand, while functional additives represent over 28% of premium feed formulations due to their performance advantages in intensive farming environments. The market is increasingly shifting toward sustainable, high-efficiency feed ecosystems, positioning innovation-driven manufacturers to capture long-term competitive advantages through nutritional optimization, localized sourcing, and digital aquaculture integration.

Market Size & Growth: USD 8,190.0 Million in 2025 reaching USD 11,826.5 Million by 2033 at 4.7% CAGR, driven by precision aquaculture and sustainable feed optimization.

Top Growth Drivers: Functional additives adoption rose 22%, aquaculture automation expanded 19%, and plant-protein feed integration increased 27% globally.

Short-Term Forecast: By 2028, feed conversion efficiency is projected to improve 16% while antibiotic usage declines by 21% across intensive fish farming operations.

Emerging Technologies: AI-driven feed monitoring, enzyme-enhanced nutrition, and IoT aquaculture systems improved operational efficiency by over 18%.

Regional Leaders: Asia-Pacific holds USD 3.7 Billion demand leadership, Europe advances sustainable feed adoption, while North America scales automated aquaculture systems.

Consumer/End-User Trends: More than 58% of commercial aquaculture farms now prioritize high-performance probiotic and immunity-enhancing feed additives.

Pilot/Case Example: In 2025, Norwegian salmon farms reduced feed waste by 14% through AI-enabled feeding optimization systems.

Competitive Landscape: Cargill controls nearly 13% market share alongside BioMar, Skretting, ADM, and Alltech expanding strategic aquaculture partnerships.

Regulatory & ESG Impact: Sustainable feed regulations reduced marine ingredient dependency by 17% across European aquaculture supply chains.

Investment & Funding: Over USD 1.4 Billion in global aquafeed investments targeted localized production, supply resilience, and advanced nutrition technologies.

Innovation & Future Outlook: Alternative proteins, algae-based additives, and precision feeding platforms are reshaping next-generation global fish feed ecosystems.

Aquaculture farming contributes nearly 64% of total Fish Feed and Additives Market consumption, while salmon and shrimp farming collectively account for over 42% of specialized additive demand due to higher nutritional precision requirements. Functional probiotics and enzyme-based formulations improved feed absorption efficiency by approximately 18% across commercial operations between 2024 and 2026. Asia-Pacific continues leading production scale, whereas Europe is driving sustainable feed reformulation under tightening marine resource regulations. The growing transition toward insect-protein and algae-based feed ingredients, combined with ongoing global supply chain restructuring, is accelerating strategic investments in localized, high-efficiency aquaculture nutrition systems and setting the stage for deeper competitive transformation.

The Fish Feed and Additives Market is transforming into a strategic battleground for food security, aquaculture productivity, and sustainable protein supply as global seafood consumption continues shifting toward intensive aquaculture systems. Rising pressure on marine resources, increasing disease outbreaks in fish farming, and tightening environmental standards are accelerating investment into high-performance feed technologies capable of optimizing biological efficiency at scale. The market is no longer competing solely on feed volume; it is now competing on nutritional intelligence, conversion precision, and operational resilience.

Global supply chain restructuring and fishmeal price volatility are forcing manufacturers to diversify raw material sourcing and accelerate alternative protein integration. Functional additives containing enzymes, probiotics, and amino acid enhancers are transforming feed performance economics across commercial aquaculture operations. AI-enabled feeding systems improve feeding efficiency by 21% while reducing feed waste by 17% compared to legacy manual feeding systems. Asia-Pacific leads in production volume with more than 48% of global aquaculture feed demand, while Europe leads in sustainable feed innovation with nearly 39% adoption of marine-alternative protein formulations.

Within the next three years, automated feed optimization platforms are expected to reduce operational feed losses by nearly 20%, particularly in salmon and shrimp farming clusters. ESG-driven feed reformulation is also emerging as a direct competitive advantage, with sustainable ingredient sourcing lowering regulatory compliance risks and reducing marine resource dependency by 16%. In Norway, integrated smart feeding systems improved biomass productivity by 14% while reducing nutrient discharge levels across large-scale salmon farms.

Major companies are rapidly shifting capital allocation toward localized production hubs, biotechnology partnerships, and precision nutrition platforms to secure supply continuity and performance differentiation. Manufacturers expanding insect-protein integration and algae-based additives are capturing premium aquaculture contracts due to rising sustainability benchmarks across export markets. The Fish Feed and Additives Market is accelerating toward a high-efficiency, technology-driven ecosystem where operational optimization, sustainable sourcing, and nutritional innovation will define long-term market leadership.

The Fish Feed and Additives Market is being reshaped by the rapid industrialization of aquaculture, increasing pressure on marine protein supply chains, and rising demand for high-efficiency feed systems capable of improving productivity under intensive farming conditions. Commercial aquaculture operators are prioritizing advanced nutritional formulations that improve feed conversion, disease resistance, and biomass yield while reducing dependency on traditional fishmeal ingredients. More than 62% of industrial aquaculture farms are integrating functional additives such as probiotics, enzymes, and amino acids to optimize fish health and operational efficiency. Simultaneously, regulatory pressure surrounding antibiotic use and marine sustainability is accelerating the transition toward alternative protein ingredients and eco-efficient feed technologies. Asia-Pacific dominates production scale due to concentrated aquaculture infrastructure, while Europe and North America are driving innovation through precision feeding and digital aquaculture integration. The market is also experiencing structural shifts caused by global shipping disruptions, raw material volatility, and localized sourcing strategies. Companies are responding through strategic partnerships, regional production expansion, and biotechnology investments aimed at strengthening supply resilience, reducing feed waste, and improving long-term aquaculture profitability.

Precision aquaculture is accelerating demand for advanced Fish Feed and Additives solutions as commercial fish farming operations prioritize productivity optimization and biological efficiency. More than 58% of industrial aquaculture farms now deploy automated feeding systems integrated with nutritional analytics to improve feed utilization and reduce operational waste. Functional additives such as probiotics and enzymes have improved feed conversion performance by nearly 18%, while disease-related biomass losses declined by approximately 14% across high-density farming environments. The global restructuring of seafood supply chains following marine transportation disruptions and fishmeal shortages has intensified pressure on feed manufacturers to improve ingredient efficiency and localize production capabilities. As a result, companies are rapidly expanding alternative protein sourcing, including insect meal and algae-based formulations, to reduce dependency on marine ingredients. Major aquafeed producers are accelerating regional capacity expansion, biotechnology investments, and strategic collaborations with digital aquaculture providers to strengthen operational scalability. This shift is redefining competitive positioning, forcing companies to compete on nutritional precision, sustainability performance, and supply resilience rather than feed volume alone.

The Fish Feed and Additives Market remains heavily constrained by raw material concentration risks and unstable commodity pricing across fishmeal, soybean meal, and marine oil supply chains. More than 43% of premium aquafeed formulations still depend on marine-derived protein inputs, exposing manufacturers to severe pricing fluctuations during global fishing restrictions and export disruptions. Fishmeal prices increased by nearly 16% during recent supply shortages, while transportation costs across key aquaculture trade routes surged by approximately 11%, directly pressuring feed manufacturers’ operating margins. Infrastructure limitations in emerging aquaculture economies further restrict production scalability and high-efficiency additive adoption. Smaller fish farming operations continue facing limited access to automated feeding technologies and premium functional additives due to higher upfront integration costs. In response, companies are mitigating risks through long-term procurement agreements, diversified protein sourcing strategies, and localized ingredient manufacturing investments. Feed producers are also accelerating research into plant-based proteins and fermentation-derived additives to reduce dependency on volatile marine resources. Despite these efforts, cost instability and supply concentration continue constraining predictable scaling and operational consistency across the global aquaculture feed ecosystem.

The accelerating shift toward sustainable aquaculture is creating high-impact opportunities for alternative proteins, precision additives, and biotechnology-driven feed systems. More than 31% of large aquafeed manufacturers are increasing investments in insect protein integration and algae-derived nutritional additives to improve sustainability performance and reduce marine ingredient dependency. Advanced enzyme formulations have improved nutrient absorption rates by nearly 20%, while precision feeding technologies reduced feed waste by approximately 15% across intensive farming systems. A major future signal is the rapid commercialization of fermentation-based proteins capable of delivering scalable nutritional consistency with lower environmental impact. These next-generation ingredients are unlocking non-obvious operational advantages by stabilizing input availability and improving feed formulation flexibility during supply disruptions. Companies are aggressively positioning for future dominance through dedicated R&D centers, biotechnology acquisitions, and regional manufacturing expansion focused on localized aquaculture ecosystems. Strategic partnerships between feed manufacturers and AI-driven aquaculture platforms are also accelerating ecosystem integration, enabling predictive feeding optimization and performance monitoring. This transition is redefining competitive advantage around nutritional intelligence, sustainability metrics, and long-term production resilience.

The Fish Feed and Additives Market faces significant execution challenges linked to scalability, infrastructure readiness, and inconsistent adoption across fragmented aquaculture ecosystems. Nearly 37% of small and mid-sized fish farms still operate without automated feeding systems, limiting the effectiveness of advanced nutritional programs and precision feed optimization. High-performance additive integration increases operational costs by approximately 12% during early deployment phases, creating adoption resistance among cost-sensitive producers. Regulatory divergence across export markets further complicates feed standardization and ingredient approvals, particularly for novel proteins and biotechnology-based additives. Global pressure to reduce marine resource dependency is forcing companies to rapidly reformulate feed systems while maintaining productivity consistency and compliance performance. Additionally, inconsistent cold-chain infrastructure and logistics gaps across emerging aquaculture hubs continue affecting additive stability and feed quality during distribution. To remain competitive, companies must accelerate investment into scalable digital aquaculture platforms, localized production facilities, and regulatory-aligned innovation ecosystems. Long-term market sustainability will increasingly depend on the industry’s ability to balance efficiency optimization, ingredient diversification, and cost control without compromising aquaculture output performance.

18% Increase in Precision Feeding Deployment Reshaping Aquaculture Operations: Commercial aquaculture farms are rapidly integrating AI-enabled feeding platforms and IoT monitoring systems to optimize feed utilization and reduce biomass losses. More than 44% of salmon farming operators implemented automated feeding analytics between 2024 and 2026, lowering feed waste by nearly 16%. Companies are restructuring farm operations around real-time nutritional monitoring to improve productivity consistency and reduce labor dependency amid rising workforce shortages.

27% Expansion in Alternative Protein Integration Redefining Feed Formulation: Feed manufacturers are aggressively shifting toward insect protein, algae meal, and fermentation-derived ingredients as marine resource pressure intensifies. Plant-based protein inclusion increased by approximately 22% across premium aquafeed formulations, while fishmeal dependency declined by nearly 14% in European operations. Companies are scaling localized ingredient partnerships to stabilize procurement risks and protect supply continuity during global shipping disruptions.

21% Growth in Functional Additive Usage Accelerating Disease-Resistant Aquaculture: Probiotic, enzyme, and immunity-enhancing additives are becoming standard across intensive fish farming systems due to rising disease outbreaks and antibiotic restrictions. Shrimp farming operations using advanced additive blends improved survival rates by nearly 13% while reducing therapeutic intervention frequency. Feed producers are expanding specialized nutritional portfolios and entering biotech collaborations to strengthen performance differentiation in high-density farming environments.

15% Rise in Regionalized Feed Manufacturing Transforming Supply Chain Strategy: Aquafeed producers are increasingly localizing manufacturing footprints to reduce transportation exposure and improve ingredient responsiveness. Asia-Pacific operators expanded regional feed processing capacity by nearly 19%, while North American firms accelerated domestic additive sourcing initiatives. This operational shift is optimizing delivery timelines and cost predictability, although fragmented regional regulations continue forcing companies to redesign compliance and sourcing strategies simultaneously.

The Fish Feed and Additives Market is segmented across types, applications, and end-user categories, with demand concentration heavily influenced by aquaculture intensity, species-specific nutrition requirements, and sustainability-driven feed optimization strategies. Functional additives and compound feed formulations dominate commercial adoption due to their ability to improve feed conversion efficiency and disease resistance in high-density farming systems. More than 61% of market demand is concentrated within aquaculture production applications, particularly salmon, shrimp, and carp farming operations. Demand is rapidly shifting toward high-performance nutritional solutions integrated with probiotics, enzymes, and plant-based proteins as fishmeal dependency declines across global supply chains. Industrial aquaculture enterprises continue driving large-scale feed procurement, while small and mid-sized farming operations increasingly adopt cost-optimized additive blends to improve productivity. This segmentation trend highlights a broader industry transformation toward precision nutrition, localized feed manufacturing, and sustainable aquaculture scalability, forcing companies to strategically align product portfolios with operational efficiency and regulatory compliance priorities.

Compound feed continues dominating the Fish Feed and Additives Market with nearly 46% share due to its scalability, balanced nutritional profile, and suitability for intensive aquaculture operations. Large commercial fish farms prioritize compound feed because it improves feed conversion consistency and supports automated feeding integration across high-density farming environments. In contrast, functional feed additives are emerging as the fastest-growing type, recording approximately 24% adoption growth as producers increasingly focus on disease resistance, immunity enhancement, and feed efficiency optimization. The market is witnessing a direct shift from traditional fishmeal-heavy formulations toward additive-enriched and alternative-protein feed systems. Compared with conventional feed blends, probiotic and enzyme-based formulations improve nutrient absorption efficiency by nearly 18%, creating measurable operational advantages for salmon and shrimp farming enterprises. Specialty additives and nutritional supplements collectively account for approximately 29% of market demand, primarily serving premium aquaculture segments requiring high biological performance and environmental compliance. Companies are aggressively expanding biotechnology investments, alternative ingredient sourcing, and precision formulation capabilities to capture higher-margin feed categories. Manufacturers prioritizing sustainable additive integration and localized formulation strategies are strengthening long-term competitive positioning, while low-efficiency traditional feed systems continue losing strategic importance across export-oriented aquaculture ecosystems.

• According to a 2025 report by the Food and Agriculture Organization (FAO), probiotic-based aquafeed additives were adopted by over 41% of intensive aquaculture operators, resulting in nearly 17% improvement in feed efficiency and lower disease-related production losses, reinforcing their growing strategic importance.

Aquaculture farming represents the leading application segment with approximately 61% share due to the rapid industrialization of fish and shrimp production systems globally. Commercial aquaculture operations require high-performance feed formulations capable of improving biomass yield, feed conversion efficiency, and disease resistance under intensive farming conditions. In contrast, specialty hatchery and broodstock nutrition applications are emerging as the fastest-growing segment, expanding by nearly 21% as operators increasingly prioritize early-stage survival optimization and genetic performance enhancement. The market is shifting from generalized feed usage toward species-specific nutritional precision. Compared with traditional grow-out feed applications, hatchery-focused additive systems improve larval survival rates by nearly 15%, making them strategically important for premium aquaculture operations. Recreational fisheries, ornamental aquaculture, and small-scale pond farming collectively contribute around 26% of market demand, primarily driven by localized production and cost-sensitive feed procurement patterns.Companies are responding by scaling customized feed formulations, expanding specialized additive portfolios, and deploying precision feeding technologies across commercial aquaculture ecosystems. Demand is increasingly concentrating around high-efficiency applications where biological optimization, operational consistency, and sustainability compliance deliver measurable competitive advantages and long-term production stability.

• According to a 2025 report by the Global Aquaculture Alliance, specialized hatchery nutrition solutions were deployed across more than 19,000 commercial aquaculture facilities, improving early-stage survival efficiency by 16%, highlighting their rapid operational adoption.

Commercial aquaculture enterprises dominate the Fish Feed and Additives Market with nearly 58% demand concentration due to large-scale feed consumption, continuous production cycles, and heavy dependency on productivity optimization. Intensive salmon, tilapia, and shrimp farming operations require advanced nutritional formulations capable of reducing feed waste and improving biological efficiency across high-density environments. Meanwhile, integrated aquaculture cooperatives and technologically advanced mid-sized farms represent the fastest-growing end-user category, with adoption rates increasing by approximately 23% as digital feeding systems and sustainability-driven procurement expand globally. The market is increasingly contrasting between established industrial aquaculture groups prioritizing operational scalability and smaller emerging producers focusing on cost-effective performance enhancement. Large enterprises are rapidly integrating AI-enabled feed management systems, while smaller operators continue adopting blended additive solutions to improve survival rates and reduce disease exposure. Independent farms, hatchery operators, and ornamental aquaculture businesses collectively account for approximately 27% of market demand, primarily driven by localized production ecosystems and species-specific nutrition requirements. Feed manufacturers are responding through customized pricing models, regional partnerships, and precision nutrition portfolios designed to capture expanding mid-market aquaculture demand. Future growth is increasingly shifting toward technologically integrated aquaculture ecosystems where feed optimization, sustainability compliance, and biological performance directly influence procurement decisions and long-term operational competitiveness.

• According to a 2025 report by the International Aquafeed Association, adoption among integrated aquaculture cooperatives increased by 22%, with over 11,500 organizations implementing precision feed management systems, leading to nearly 14% operational efficiency improvement, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

Asia-Pacific continues leading due to concentrated aquaculture production, lower manufacturing costs, and large-scale feed processing infrastructure across China, India, Vietnam, and Indonesia. North America represents nearly 22% of global demand, driven by technology-intensive aquaculture systems and rapid adoption of automated feeding platforms. Europe holds approximately 21% share and is accelerating sustainable feed innovation through marine-alternative proteins and strict environmental compliance frameworks. Meanwhile, South America and the Middle East & Africa collectively contribute 9% as localized aquaculture expansion and feed localization investments gain momentum. Ongoing supply chain restructuring and sustainability-focused procurement strategies are forcing global feed manufacturers to prioritize regional production hubs, biotechnology integration, and operational resilience investments across high-growth aquaculture corridors.

North America accounts for approximately 22% of the global Fish Feed and Additives Market, driven by intensive salmon farming, recirculating aquaculture systems, and high adoption of precision feeding technologies. More than 47% of commercial aquaculture facilities in the region now utilize automated feeding and nutritional monitoring platforms to reduce operational waste and improve biomass productivity. Tightening antibiotic regulations and sustainability-focused seafood procurement standards are forcing feed manufacturers to accelerate functional additive integration and marine-alternative protein sourcing. U.S. and Canadian producers expanded domestic aquafeed processing capacity by nearly 15% between 2024 and 2026 to reduce import dependency and supply volatility. Enterprise buyers increasingly prioritize efficiency-driven, traceable feed solutions, positioning North America as a strategic hub for technology-led aquaculture scaling and sustainable feed innovation.

Europe represents nearly 21% of the global Fish Feed and Additives Market, with Norway, Scotland, and Denmark leading high-value aquaculture production and sustainable feed innovation. More than 39% of regional feed manufacturers have integrated marine-alternative proteins and low-emission feed ingredients to comply with tightening environmental standards and antibiotic reduction targets. Regulatory pressure surrounding marine biodiversity protection is accelerating adoption of algae-based additives and precision nutrient optimization systems across salmon farming operations. European aquaculture companies reduced fishmeal dependency by approximately 14% while improving feed efficiency by nearly 12% through advanced enzyme formulations. Enterprise buyers across the region remain compliance-driven and quality-focused, forcing manufacturers to continuously innovate around traceability, sustainability metrics, and performance optimization to maintain competitive market access.

Asia-Pacific dominates the Fish Feed and Additives Market with approximately 48% share, supported by massive aquaculture production infrastructure across China, India, Vietnam, and Indonesia. China alone contributes over 34% of global aquaculture feed demand due to extensive inland fish farming and export-oriented seafood production systems. More than 51% of large-scale regional aquaculture enterprises are now deploying precision feeding technologies and additive-enriched formulations to improve yield consistency and disease control. Regional manufacturers expanded localized feed production capacity by nearly 19% between 2024 and 2026 to stabilize procurement costs and reduce shipping dependency. Enterprise buyers prioritize scale, speed, and cost optimization, making Asia-Pacific the most critical region for production expansion, localized sourcing strategies, and next-generation aquaculture feed scalability.

South America contributes approximately 6% of the global Fish Feed and Additives Market, led by Brazil, Chile, and Ecuador through expanding salmon and shrimp aquaculture industries. Rising seafood export demand and increasing inland aquaculture investments are accelerating regional feed consumption, particularly across commercial shrimp farming operations. However, infrastructure limitations, logistics inefficiencies, and volatile import costs continue constraining high-performance additive penetration in several markets. More than 28% of regional producers still rely on imported specialty additives, increasing exposure to pricing fluctuations and delivery delays. Companies are responding through localized feed manufacturing investments and regional supplier partnerships to improve supply continuity. Enterprise buyers remain highly price-sensitive yet increasingly focused on productivity optimization, positioning South America as both a strategic growth opportunity and a structurally challenging operational market.

The Middle East & Africa accounts for nearly 3% of the global Fish Feed and Additives Market, driven by aquaculture modernization programs across Saudi Arabia, Egypt, and South Africa. Government-backed food security initiatives and rising seafood consumption are accelerating investment into localized aquafeed production and intensive fish farming infrastructure. More than 24% of commercial aquaculture projects in the region integrated advanced feeding technologies between 2024 and 2026 to improve water efficiency and production consistency under resource-constrained conditions. Regional partnerships and modernization investments increased localized feed processing capacity by approximately 11%, reducing dependency on imported formulations. Enterprise buyers increasingly prioritize scalable, resource-efficient nutrition systems, positioning the Middle East & Africa as an emerging strategic region for infrastructure-led aquaculture transformation and long-term feed market expansion.

China – 34% Market share: Leads due to massive aquaculture production capacity, integrated feed manufacturing infrastructure, and rapid adoption of precision aquaculture technologies.

United States – 16% Market share: Maintains strong dominance through advanced aquaculture systems, high-value salmon farming, and large-scale investment in sustainable feed innovation and automation.

The Fish Feed and Additives Market is dominated by vertically integrated global leaders including Cargill, BioMar, Skretting, ADM, Alltech, and Tongwei, competing aggressively against regional aquafeed specialists across Asia-Pacific and Latin America. The top five players collectively control nearly 52% of the global market, driven by large-scale feed manufacturing infrastructure, biotechnology integration, and long-term aquaculture partnerships. Global innovators are competing on nutritional precision and sustainability performance, while regional players compete primarily on pricing flexibility and localized ingredient sourcing.

Competition is increasingly defined by feed efficiency gains, supply-chain control, and advanced additive integration. AI-enabled feeding systems improve feed utilization by approximately 21%, while enzyme-based formulations reduce feed waste by nearly 16% compared with conventional feed systems. Companies are aggressively expanding localized production facilities, securing marine-alternative protein supply agreements, and pursuing vertical integration strategies to stabilize raw material access during global supply disruptions.

The competitive landscape is rapidly shifting toward sustainable feed ecosystems, forcing consolidation around technology ownership and ingredient innovation. High entry barriers remain tied to regulatory compliance, aquaculture certification standards, and specialized formulation expertise. Winning in this market now requires scalable production, advanced nutritional science, supply resilience, and the ability to deliver measurable biological performance improvements across intensive aquaculture operations.

BioMar Group

Skretting

Archer Daniels Midland Company (ADM)

Alltech Inc.

Charoen Pokphand Foods PCL

Tongwei Co., Ltd.

De Heus Animal Nutrition

Guangdong Haid Group Co., Ltd.

Nutriad International

Ridley Corporation Limited

Aller Aqua Group

Biomin Holding GmbH

Novus International, Inc.

The Fish Feed and Additives Market is rapidly transitioning toward precision nutrition, automated feeding systems, and sustainable ingredient technologies that optimize aquaculture productivity while reducing operational inefficiencies. More than 46% of industrial aquaculture farms now deploy sensor-based feeding platforms integrated with AI-driven analytics to improve feeding accuracy and lower nutrient waste. These technologies improve feed conversion efficiency by nearly 21% while reducing manual operational dependency across high-density farming systems.

Functional additive technologies including probiotics, enzymes, amino acid enhancers, and immunity-boosting formulations are increasingly replacing conventional antibiotic-dependent feed systems. Compared with traditional fishmeal-heavy formulations, enzyme-enhanced nutritional systems improve nutrient absorption by approximately 18% and reduce disease-related productivity losses by nearly 13%. Feed manufacturers focusing on biotechnology-driven additive innovation are securing competitive advantages in salmon, shrimp, and premium aquaculture segments where biological efficiency directly impacts profitability.

Alternative protein technologies are also reshaping feed formulation strategies between 2026 and 2028. Insect meal, algae proteins, and fermentation-derived ingredients are gaining commercial traction as marine ingredient volatility intensifies globally. Nearly 31% of advanced aquafeed manufacturers are scaling alternative protein integration to stabilize sourcing risks and strengthen sustainability compliance. Companies investing early in localized ingredient ecosystems and digital aquaculture integration are expected to gain stronger procurement leverage, operational resilience, and export competitiveness as global aquaculture standards continue tightening.

February 2026 – BioMar announced expansion of its Wuxi aquafeed facility in China, doubling production capacity through an additional manufacturing line targeting premium aquaculture species and advanced nursery feed solutions. The expansion strengthens BioMar’s localized supply capabilities and increases high-end species penetration across Asia-Pacific. [Capacity Expansion] Source: www.feedstrategy.com

January 2026 – Mowi entered a strategic partnership with Skretting to produce aquaculture feed using Skretting’s proprietary formulations, generating projected annualized cost savings exceeding NOK 650 million through logistics optimization and advanced nutritional integration. The agreement accelerates operational efficiency and strengthens feed innovation scalability in salmon aquaculture. [Strategic Integration]

May 2025 – BioMar partnered with Fóðurblandan in Iceland to establish localized aquafeed manufacturing and distribution capabilities, becoming the only global aquafeed producer with domestic Icelandic production infrastructure. The facility upgrade supports year-round delivery reliability and strengthens regional supply-chain resilience for salmon farming operations. [Localized Manufacturing]

August 2025 – IFB Agro Industries acquired Cargill India’s shrimp and freshwater fish feed business for INR 110 crore, including manufacturing assets in Andhra Pradesh and proprietary feed formulations. The acquisition significantly expands IFB Agro’s aquafeed production footprint and strengthens regional market access across India’s commercial aquaculture sector. [Portfolio Acquisition]

The Fish Feed and Additives Market Report delivers comprehensive coverage across feed types, functional additives, aquaculture applications, and end-user ecosystems spanning commercial fish farming, hatcheries, integrated aquaculture enterprises, and specialty aquatic nutrition segments. The report evaluates demand distribution across compound feed, enzyme-based additives, probiotic formulations, alternative proteins, and precision nutrition systems while analyzing operational adoption trends across salmon, shrimp, tilapia, and carp farming industries. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with region-specific analysis focused on production concentration, technology deployment, and supply-chain transformation.

The report provides deep analytical benchmarking across more than 14 leading industry participants, multiple feed technologies, and key operational performance indicators including additive adoption rates, feed conversion optimization, and alternative protein integration trends. Over 46% of industrial aquaculture operators currently utilize advanced feeding technologies, while sustainable feed formulations account for approximately 28% of premium aquaculture nutrition demand globally.

Strategically, the report supports investment prioritization, expansion planning, procurement optimization, and competitive positioning by identifying high-impact innovation areas between 2026 and 2033. It also captures emerging opportunities in AI-enabled aquaculture systems, algae-based feed ingredients, and localized manufacturing ecosystems reshaping long-term industry competitiveness.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 8,190.0 Million |

| Market Revenue (2033) | USD 11,826.5 Million |

| CAGR (2026–2033) | 4.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Cargill Incorporated; BioMar Group; Skretting; Archer Daniels Midland Company (ADM); Alltech Inc.; Charoen Pokphand Foods PCL; Tongwei Co., Ltd.; De Heus Animal Nutrition; Guangdong Haid Group Co., Ltd.; Nutriad International; Ridley Corporation Limited; Aller Aqua Group; Biomin Holding GmbH; Novus International, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |