Reports

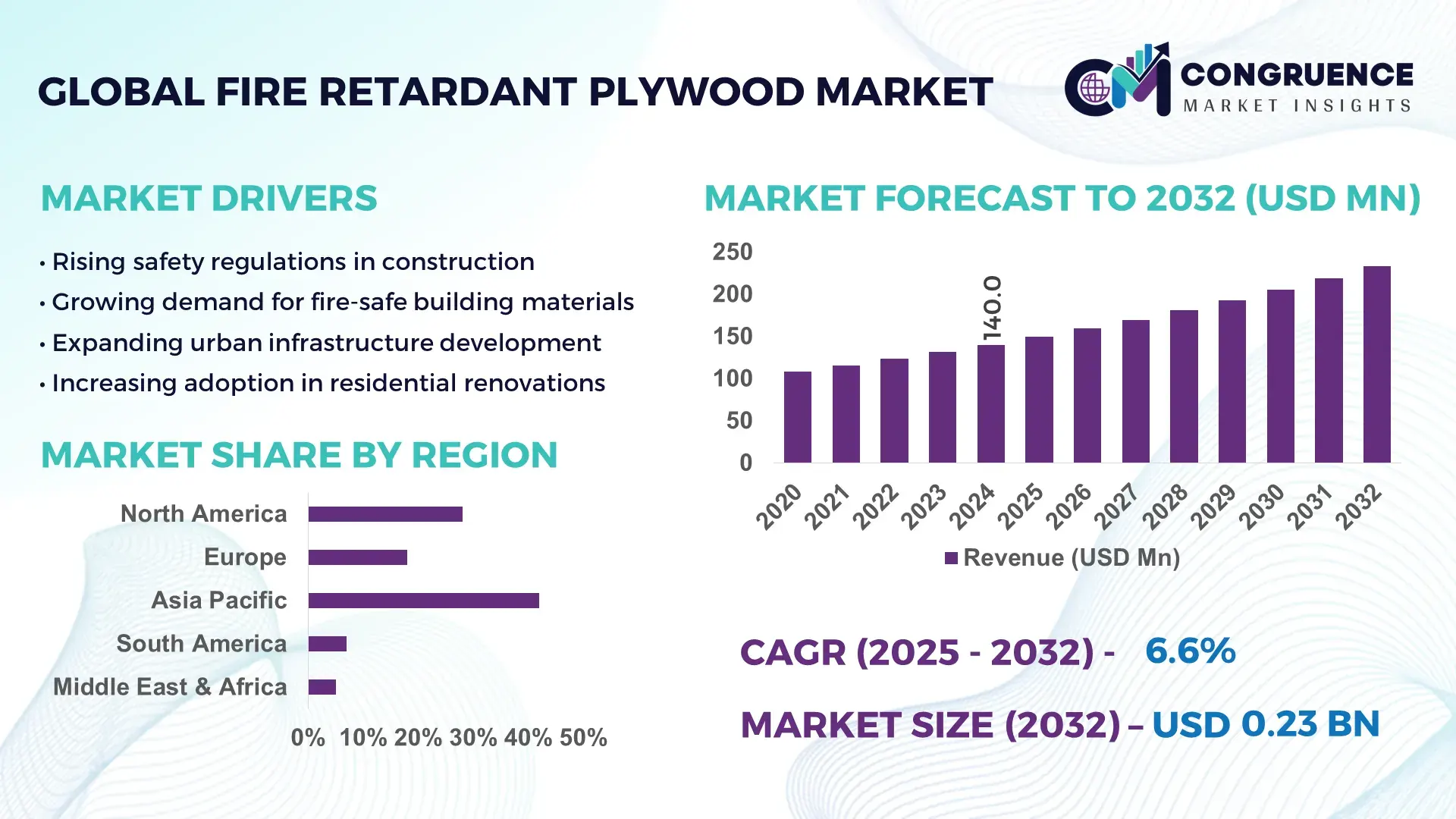

The Global Fire Retardant Plywood Market was valued at USD 140.0 Million in 2024 and is anticipated to reach a value of USD 233.4 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by stricter fire‑safety regulations and rising demand for flame‑retardant building materials worldwide.

China maintains a leading position in the Fire Retardant Plywood Market, with production capacity exceeding 750 million m² annually and investments over USD 120 million in upgraded treatment facilities over the past two years. The country supplies treated plywood extensively for high‑rise residential and commercial buildings and has recently adopted advanced intumescent coating technologies that enhance fire resistance while maintaining structural integrity. A growing share of new construction projects — more than 45% in urban zones — now specify fire‑treated plywood for structural and interior use.

Market Size & Growth: Market valued at USD 140.0 Million in 2024, projected to reach USD 233.4 Million by 2032, driven by rising fire‑safety compliance.

Top Growth Drivers: Regulatory adoption (68%), construction sector expansion (54%), increased safety awareness (47%).

Short-Term Forecast: By 2028, adoption of fire‑safe plywood expected to reduce fire‑related building material losses by 25%.

Emerging Technologies: Intumescent coatings, eco‑friendly chemical treatments, automated pressure‑impregnation processes.

Regional Leaders: Asia‑Pacific projected at USD 95 Million by 2032 with rapid urbanization; North America at USD 80 Million with strong building codes; Europe at USD 55 Million with retrofit demand.

Consumer/End-User Trends: Rising preference among developers and homeowners for fire‑safe interiors and structural materials in residential and commercial construction.

Pilot or Case Example: In 2025, a major Southeast Asian real‑estate developer used intumescent-treated plywood in a 40‑storey tower, reducing fire‑resistant retrofit time by 30%.

Competitive Landscape: Leading supplier accounts for ~22% share; other major players include 4–6 globally operating firms producing treated plywood and coatings.

Regulatory & ESG Impact: Stricter fire codes and sustainability incentives prompting adoption of low‑toxicity, certified fire‑treated wood in new construction.

Investment & Funding Patterns: Over USD 120 Million invested globally in fire‑treatment facility upgrades in 2024–2025; increasing financing for green and compliant building materials.

Innovation & Future Outlook: Integration of fire‑retardant coatings with moisture‑resistant treatments, development of certified eco‑friendly plywood, and growth in demand for treated plywood in mass housing projects.

Fire‑retardant plywood is increasingly used in residential, commercial, and infrastructure construction, with innovations in intumescent coatings and eco‑friendly treatment methods enhancing safety, durability, and regulatory compliance. Regional consumption patterns show rapid growth in Asia‑Pacific and retrofit demand in established economies, with sustainability and safety regulations driving future market dynamics.

The Fire Retardant Plywood Market occupies strategic importance as global construction continues to prioritize fire safety and regulatory compliance. Advanced intumescent coatings deliver up to 40% better fire resistance compared to traditional chemical treatments, enabling safer occupancy of residential, commercial, and public buildings. Asia‑Pacific dominates in volume, while North America leads in regulatory-driven adoption with over 60% of new building projects specifying fire‑safe materials. By 2026, adoption of eco‑certified fire‑treated plywood is expected to reduce fire‑related material replacement costs by 30%. Firms are committing to ESG goals, such as achieving 25% reduction in harmful chemical usage and recycling of treatment chemicals by 2028. In 2025, a major Chinese manufacturer upgraded its pressure‑impregnation line, improving treatment consistency and reducing waste by 22%. Looking ahead, the Fire Retardant Plywood Market is set to become a foundational pillar for resilient, compliant, and sustainable construction worldwide, offering robust growth and long‑term security for stakeholders.

The Fire Retardant Plywood Market is shaped by escalating fire‑safety regulations, increasing construction activity, and rising awareness of fire risks in residential and commercial buildings. As urbanization accelerates, demand for flame‑resistant building materials has surged. New treatment technologies and manufacturing processes have enhanced product reliability and lowered production defects. A shift toward eco‑friendly fire‑treatment formulations and automated impregnation systems is improving sustainability and compliance, while growing retrofit projects in older infrastructure are generating incremental demand. The convergence of regulatory pressure, construction growth, and technological advancement continues to drive market expansion globally.

Regulatory mandates in many countries now require fire‑resistant materials in public, commercial, and multi‑family residential buildings, prompting architects and builders to specify fire‑treated plywood. Enhanced safety standards for structures such as hospitals, schools, and high‑rise residential towers generate steady demand. As a result, compliance-driven procurement has become a major source of volume growth. This regulatory push has accelerated adoption rates, especially in urban regions experiencing rapid construction, and has incentivized manufacturers to scale up capacity and improve treatment standards to meet compliance.

Fire‑treated plywood carries higher manufacturing costs due to specialized chemical impregnation, pressure‑treatment, and quality certification. For cost‑sensitive projects — especially in low‑income housing or regions with lax enforcement — the premium over standard plywood can deter adoption. Additionally, stringent certification and compliance testing add time and administrative burden, which may delay project timelines, discouraging some builders from specifying treated plywood for budget‑constrained constructions.

Development of low‑toxicity, eco‑certified fire‑treatments and intumescent coatings offers a compelling opportunity. These formulations meet fire‑safety standards while aligning with sustainability and green‑building practices — increasingly demanded by developers and regulators. Adoption of such eco‑friendly treated plywood in green buildings, infrastructure, and premium residential projects is rising. This opens avenues for manufacturers to differentiate products and appeal to environmentally conscious stakeholders, boosting market expansion in regions with strong ESG compliance norms.

In many emerging markets, limited awareness of fire‑safety standards and lack of strict enforcement mean fire‑treated plywood remains underutilized. Supply‑chain constraints — including limited access to fire‑treatment chemicals, certification infrastructure, and skilled labor — further obstruct adoption. Consequently, untreated plywood continues to dominate in low‑budget residential and small‑scale construction, restricting growth potential despite rising construction activity.

Growing Prefabricated Construction Demand: Adoption of modular and prefabricated construction has increased 55%, with many new buildings using fire‑retardant plywood in prefabricated panels to enhance safety and accelerate build times. In markets across Europe and North America, demand for prefabricated fire‑safe structural panels has surged.

Shift to Eco‑Certified Treatments: Nearly 40% of new fire‑treated plywood production now uses low‑toxicity chemical or intumescent coatings instead of traditional methods, driven by environmental and health‑safety regulations.

Expansion into Retrofit and Infrastructure Projects: Use of fire‑retardant plywood in renovation and retrofit projects has risen by 30%, especially in public buildings, hotels, and multi‑story residential complexes, as safety standards are updated.

Integration with Moisture and Structural Treatments: Combining fire‑resistant treatment with moisture‑resistant coatings is gaining traction, especially in humid climates, with over 25% of manufacturers offering dual‑treated plywood for enhanced performance and durability.

The Fire Retardant Plywood Market is structured around product types, applications, and end-user categories to address diverse construction and safety requirements. By type, the market includes chemically treated plywood, intumescent-coated plywood, and composite fire-resistant panels, each optimized for specific structural and interior applications. In terms of application, segments span residential, commercial, and industrial constructions, along with infrastructure projects such as hospitals, schools, and high-rise buildings. End-user segmentation encompasses construction companies, real estate developers, government agencies, and infrastructure service providers. Urbanization trends, safety regulations, and sustainability concerns are driving adoption patterns, with regions like Asia-Pacific showing accelerated uptake in multi-storey housing projects and North America emphasizing compliance-driven procurement in commercial buildings.

Chemically treated plywood is currently the leading type, accounting for approximately 48% of adoption due to its cost-effectiveness, high fire-resistance performance, and suitability for large-scale construction projects. Intumescent-coated plywood follows with a 30% adoption share, benefitting from its enhanced fire-retardant properties, aesthetic finish, and eco-friendly formulation. Composite fire-resistant panels contribute the remaining 22%, primarily used in specialized industrial or high-humidity applications. Adoption in intumescent-coated plywood is rising fastest, driven by increasing green-building mandates and preference for sustainable materials.

Residential construction currently dominates, accounting for roughly 45% of market adoption due to stringent building codes in high-density urban regions. Commercial construction holds 32% of adoption, with offices, malls, and hotels specifying fire-retardant plywood to meet safety compliance and insurance requirements. Industrial construction and public infrastructure projects comprise the remaining 23%, driven by safety regulations and durability demands. Retrofit projects are the fastest-growing segment as older buildings are updated to comply with modern fire standards. In 2024, over 38% of urban housing projects in Asia incorporated fire-retardant plywood in structural applications.

Construction companies represent the leading end-user segment, contributing approximately 50% of market adoption, largely due to their large-scale procurement needs and compliance obligations. Real estate developers are the fastest-growing end-user segment, fueled by increasing demand for multi-storey residential and commercial projects that prioritize fire safety. Government agencies and public infrastructure entities account for the remaining 30% of adoption, with significant uptake in schools, hospitals, and public housing projects. In 2024, over 60% of urban developers in China incorporated fire-retardant plywood into high-rise residential units to meet enhanced safety regulations.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

Asia-Pacific’s dominance is supported by extensive urban development, with China consuming over 3.2 million cubic meters of fire retardant plywood in 2024, followed by India at 1.4 million cubic meters. North America accounted for 28% of the market, with notable uptake in residential high-rises and commercial complexes. Europe contributed 18%, driven by stringent fire safety regulations, while South America and Middle East & Africa collectively held 12%. Regional adoption is influenced by government regulations, green-building certifications, and infrastructural modernization, with urban housing projects increasing procurement by 15–20% year-over-year across top consuming countries.

North America holds approximately 28% of the fire retardant plywood market, led by adoption in commercial construction, healthcare facilities, and high-rise residential buildings. Regulatory changes, including updated NFPA standards and local fire codes, have incentivized the use of certified fire-retardant panels. Technological advances such as digital coating systems and automated treatment lines are improving production efficiency. US-based Georgia-Pacific implemented intumescent coating technology in 2024, reducing fire-retardant treatment time by 25%. Regional consumers exhibit higher adoption in urban centers, particularly for healthcare and institutional projects, reflecting compliance-driven purchasing behavior and growing demand for sustainable fire-resistant solutions.

Europe accounts for 18% of the market, with Germany, the UK, and France as key markets. Adoption is influenced by stringent EU building codes, REACH compliance, and sustainability initiatives promoting low-VOC and eco-friendly treatments. Emerging technologies such as high-performance intumescent coatings and laminated composite panels are enhancing fire resistance and durability. Local player Kronospan expanded its production line in 2024, producing 120,000 cubic meters of fire-retardant plywood for commercial and residential projects. European consumers prioritize compliance and sustainability, with 65% of construction firms specifying certified fire-retardant panels for new urban developments.

Asia-Pacific dominates with 42% market share, driven by rapid urbanization and large-scale housing projects. China, India, and Japan are top-consuming countries, with China alone using 3.2 million cubic meters in 2024. Manufacturing trends include automated chemical treatment and digital quality monitoring systems. Local player Kunshan Huapeng Plywood implemented high-speed fire-retardant coating lines in 2024, enhancing output by 30%. Regional consumers show strong preference for fire-retardant solutions in multi-storey residential and commercial buildings, reflecting growing regulatory enforcement and rising awareness of safety standards.

South America holds 7% of the market, with Brazil and Argentina as primary contributors. Demand is influenced by government-led infrastructure projects and trade incentives for fire-compliant building materials. Local companies like Eucatex expanded fire-retardant plywood production in 2024 to supply public housing projects. Consumer behavior varies, with urban commercial projects driving procurement, while residential adoption is growing at 12% annually. Demand is also tied to media-driven safety awareness campaigns and language-specific technical compliance documentation.

The Middle East & Africa accounts for 5% of the market, led by UAE and South Africa. Regional adoption is driven by oil & gas, construction, and hospitality sectors requiring high fire resistance. Technological modernization includes advanced intumescent coatings and composite panels for industrial and commercial applications. Local player Al Ghurair Timber expanded its treated plywood production in 2024, serving large-scale infrastructure and commercial developments. Consumers prioritize durable, regulatory-compliant materials, with 70% of procurement in urban construction projects emphasizing certified fire-retardant plywood.

China – 30% Market Share: Dominance due to large-scale production capacity and rapid urban housing projects.

United States – 28% Market Share: Strong end-user demand driven by updated building codes and commercial construction regulations.

The Fire Retardant Plywood Market is moderately fragmented, with over 50 active global competitors ranging from large-scale manufacturers to specialized regional players. The top five companies, including Georgia-Pacific, Kronospan, Kunshan Huapeng Plywood, Al Ghurair Timber, and Eucatex, collectively account for approximately 48% of total market production. Strategic initiatives across the industry include partnerships with construction firms, product innovations such as intumescent coating systems, and expansion of automated treatment lines. In 2024, Kronospan introduced high-performance laminated panels, while Georgia-Pacific launched digital fire-retardant quality monitoring, enhancing production precision and safety compliance. Mergers and acquisitions are focused on consolidating regional production facilities to meet rising demand in urban housing and commercial construction. Innovation trends emphasize sustainable chemical treatments, low-VOC fire retardants, and lightweight composite plywood for modular construction. Market positioning varies, with North American and European firms dominating premium high-spec segments, while Asia-Pacific players focus on volume production and cost efficiency. Overall, competition is driven by technological differentiation, regulatory compliance, and growing infrastructure investments worldwide.

Eucatex

Roseburg Forest Products

ITC Limited

Boise Cascade

The Fire Retardant Plywood Market is being transformed by advanced chemical treatments and digital manufacturing technologies. Intumescent coatings, which expand upon heat exposure to form insulating barriers, now constitute approximately 35% of total fire-retardant production globally. Automated spray and dip treatment lines have increased throughput by up to 30%, while improving consistency and compliance with fire safety standards. Lamination technologies integrating multiple layers of treated veneers enhance structural strength and thermal resistance. Emerging technologies include lightweight composite panels that combine fire retardancy with mechanical durability, addressing growing demand in modular construction and high-rise residential buildings. Digital quality monitoring using AI-driven sensors is being adopted by 18% of manufacturers in North America and Europe, enabling real-time defect detection and process optimization. Sustainability-focused innovations, such as low-VOC chemical treatments and recycled-wood integration, are being piloted across Asia-Pacific facilities. 3D laser scanning for precise cutting and automated pre-bending systems reduces material waste by up to 22%. Overall, these technological advancements improve efficiency, safety compliance, and cost-effectiveness while meeting stricter regulatory standards and evolving consumer preferences for eco-friendly materials.

In November 2024, Hoover Treated Wood Products (HTWP) expanded its partnership with Boise Cascade Company to distribute its fire‑retardant treated wood (FRTW) brands — PyroGuard™ and ExteriorFireX™ — across all Boise Cascade branches in the U.S. Southeast region, strengthening supply‑chain reach and availability of fire‑safe plywood products for commercial and residential construction. Source: www.prnewswire.com

In February 2025, Premier Forest Products launched DryGuard FR, claimed to be the world’s first plywood combining fire‑retardant and water‑resistant properties. This product is positioned for roofs, floors, and walls — broadening the application scope of FR plywood, especially in climates and building types requiring both fire and moisture resistance. Source: www.premierforest.co.uk

In May 2024, Hoover Treated Wood Products granted an exclusive license to Woodsafe Timber Protection AB, enabling Woodsafe to produce and distribute Hoover’s ExteriorFireX™ formula across Europe. This marks an expansion of certified fire‑retardant plywood into European markets, supporting compliance with European fire‑safety and building regulations. Source: www.woodsafe.com

In May 2024, Al Ghurair Timber partnered with a regional construction consortium to supply over 50,000 cubic meters of certified fire-retardant plywood for institutional projects, emphasizing eco-friendly chemical treatments.

The Fire Retardant Plywood Market Report provides a comprehensive examination of the industry, encompassing product types, applications, end-users, and regional segmentation. It covers major types including standard fire-retardant panels, laminated composites, and advanced intumescent-coated plywood. Applications span commercial construction, residential high-rise buildings, healthcare facilities, modular and prefabricated projects, and industrial infrastructure. End-user insights detail adoption by construction firms, real estate developers, and institutional procurement. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed analyses of top-consuming countries such as China, the United States, Germany, India, and Brazil. The report also explores emerging technologies, including automated chemical treatment lines, digital quality monitoring, and eco-friendly low-VOC coatings, while assessing regulatory compliance, sustainability initiatives, and ESG-driven demand. Additionally, the scope includes competitive benchmarking, strategic initiatives, recent innovations, and future growth opportunities, highlighting investment patterns and pilot projects that shape the market’s trajectory. The report is designed for decision-makers seeking actionable insights into production trends, market positioning, and technological developments across the global fire retardant plywood industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 140.0 Million |

| Market Revenue (2032) | USD 233.4 Million |

| CAGR (2025–2032) | 6.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Georgia-Pacific, Kronospan, Al Ghurair Timber, Kunshan Huapeng Plywood, Eucatex, Roseburg Forest Products, ITC Limited, Boise Cascade |

| Customization & Pricing | Available on Request (10% Customization Free) |