Reports

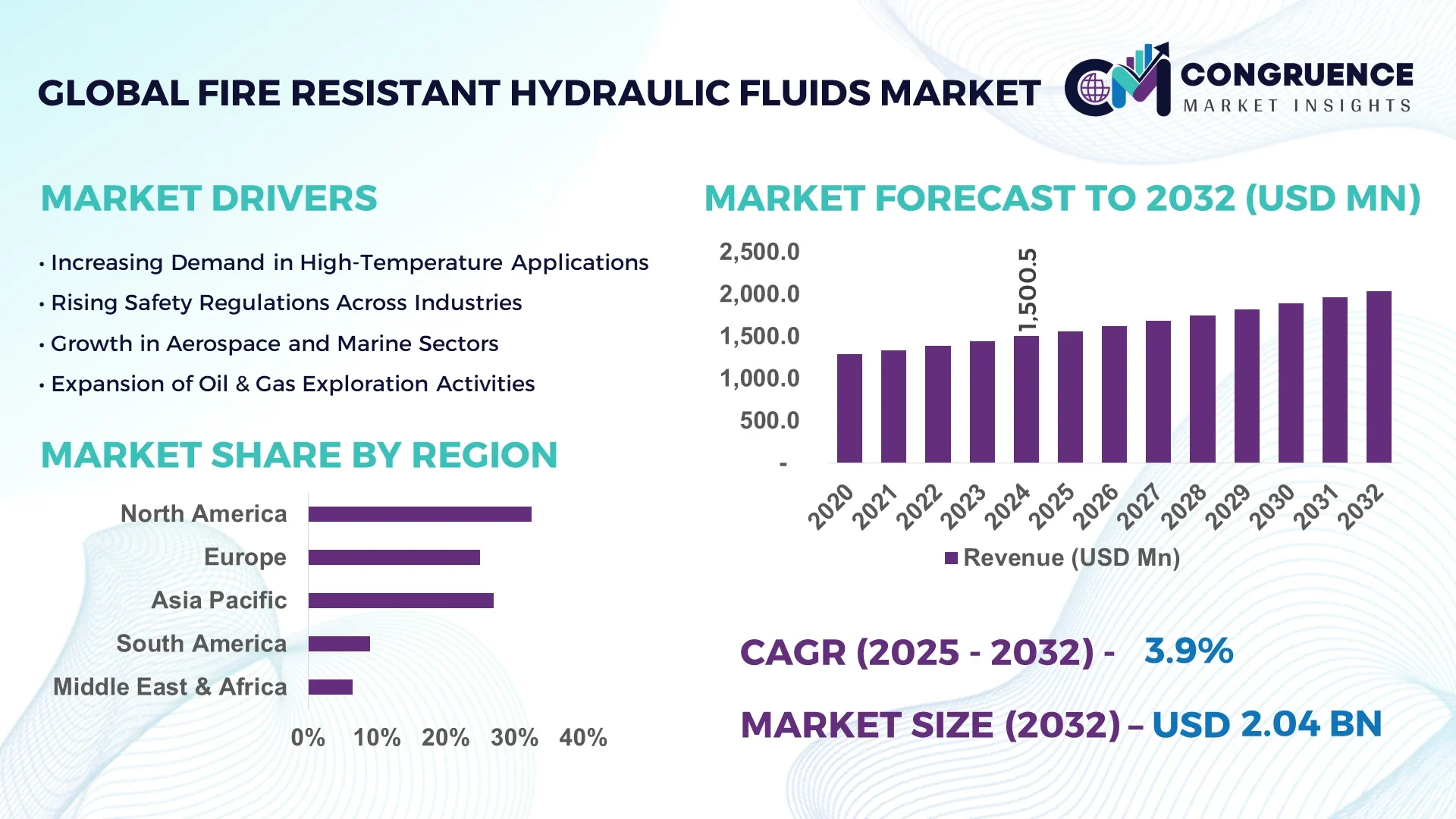

The Global Fire Resistant Hydraulic Fluids Market was valued at USD 1.56 Billion in 2024 and is anticipated to reach a value of USD 2.01 Billion by 2032, expanding at a CAGR of 3.9% between 2025 and 2032.

South Korea has emerged as a dominant player in the fire-resistant hydraulic fluids market, driven by its robust industrial base and stringent safety regulations. The country's advanced manufacturing sectors, including automotive and electronics, have significantly increased the adoption of fire-resistant hydraulic fluids to ensure operational safety and compliance with international standards.

The global market is witnessing a steady shift towards environmentally friendly and high-performance fire-resistant hydraulic fluids. Industries such as metal processing, aviation, and mining are increasingly adopting these fluids to enhance safety and reduce environmental impact. Technological advancements have led to the development of fluids with improved thermal stability and biodegradability, catering to the evolving needs of various end-use sectors.

Artificial Intelligence (AI) is playing a pivotal role in revolutionizing the fire-resistant hydraulic fluids market by enhancing product development, optimizing manufacturing processes, and improving predictive maintenance.

In product development, AI algorithms analyze vast datasets to identify optimal formulations that balance fire resistance, environmental compliance, and cost-effectiveness. This accelerates the R&D process, enabling companies to bring innovative products to market more swiftly.

Manufacturing processes benefit from AI through real-time monitoring and control systems that ensure consistent product quality and reduce waste. AI-driven analytics help in identifying process inefficiencies and implementing corrective measures promptly.

Predictive maintenance, powered by AI, allows for the early detection of equipment anomalies, minimizing downtime and extending the lifespan of hydraulic systems. By analyzing patterns and trends, AI systems can forecast potential failures and schedule maintenance activities proactively.

Furthermore, AI aids in supply chain optimization by forecasting demand, managing inventory levels, and streamlining logistics, ensuring timely delivery of fire-resistant hydraulic fluids to various industries.

"In 2024, a leading chemical company implemented an AI-driven formulation system that reduced the development time of new fire-resistant hydraulic fluids by 30%, enhancing their competitive edge in the market."

The increasing focus on workplace safety and stringent environmental regulations are significant drivers of the fire-resistant hydraulic fluids market. Industries are mandated to use fluids that minimize fire hazards and environmental impact. For instance, the European Union's REACH regulation and OSHA standards in the United States have compelled manufacturers to adopt fire-resistant and eco-friendly hydraulic fluids. This trend is particularly prominent in sectors like mining, steel production, and aviation, where the risk of fire is substantial.

The higher cost of fire-resistant hydraulic fluids compared to conventional fluids poses a restraint to market growth. Small and medium-sized enterprises (SMEs) may find it challenging to invest in these premium products, especially in developing regions where cost sensitivity is high. Additionally, the need for specialized equipment and training for handling these fluids adds to the overall operational costs, potentially hindering widespread adoption.

Technological innovations present significant opportunities in the fire-resistant hydraulic fluids market. Advances in fluid chemistry have led to the development of biodegradable and high-performance fluids that meet both safety and environmental standards. The integration of nanotechnology and advanced additives enhances fluid properties, such as thermal stability and wear resistance. These innovations open new avenues for application in emerging industries and geographies, expanding the market potential.

The fire-resistant hydraulic fluids market faces challenges related to supply chain disruptions and raw material price volatility. Geopolitical tensions, trade restrictions, and global events like pandemics can disrupt the supply of essential raw materials, affecting production schedules and costs. Manufacturers need to develop resilient supply chains and explore alternative sourcing strategies to mitigate these risks and ensure consistent product availability.

Shift Towards Biodegradable Fluids: There is a growing trend towards the adoption of biodegradable fire-resistant hydraulic fluids, driven by environmental concerns and regulatory pressures. These fluids offer the dual benefits of fire resistance and reduced ecological impact, making them increasingly popular in industries like agriculture and forestry.

Integration of IoT for Predictive Maintenance: The integration of Internet of Things (IoT) technologies in hydraulic systems enables real-time monitoring and predictive maintenance. Sensors collect data on fluid condition and system performance, allowing for timely interventions and reducing the risk of system failures. This trend enhances operational efficiency and safety across various industries.

Expansion in Emerging Markets: Emerging economies in Asia-Pacific and Latin America are witnessing rapid industrialization, leading to increased demand for fire-resistant hydraulic fluids. Government initiatives to improve industrial safety standards are further propelling market growth in these regions. Companies are expanding their presence and distribution networks to capitalize on these opportunities.

Development of Multi-Functional Fluids: Manufacturers are focusing on developing multi-functional fire-resistant hydraulic fluids that offer additional benefits such as anti-wear properties, corrosion resistance, and extended service life. These advanced fluids cater to the evolving needs of modern hydraulic systems, providing cost savings and improved performance for end-users.

The fire resistant hydraulic fluids market is segmented into various types, applications, and end-user industries, each playing a unique role in shaping overall market dynamics. These segments help in identifying demand concentrations and areas of rapid growth, offering valuable insights to manufacturers and stakeholders. The segmentation reveals clear preferences for certain fluid types in safety-critical applications, with specific industries driving high-volume demand. Additionally, end-user insights indicate a rising inclination towards technologically advanced and environmentally friendly fluid options, particularly in sectors that operate under stringent safety and environmental regulations.

The fire resistant hydraulic fluids market is primarily segmented into water-based (HFA, HFB), water-glycol-based (HFC), and synthetic-based fluids (HFD types including HFD-U, HFD-R, and HFD-S). Among these, synthetic-based fluids (HFD types) dominate the market due to their superior fire resistance, thermal stability, and longer service life. These fluids are widely used in high-risk environments like steel and metal production plants. In 2024, HFD fluids accounted for over 45% of the market share.

The fastest growing segment is the water-glycol-based (HFC) fluids, owing to their non-toxicity and environmental benefits. With increasing emphasis on sustainability and lower disposal costs, HFC fluids are gaining popularity across industries such as food processing and pharmaceutical manufacturing. Additionally, advancements in fluid formulations are improving their compatibility with various hydraulic systems, boosting their adoption.

The key application segments of fire resistant hydraulic fluids include metal processing, aviation, mining, marine, construction, and power generation. Metal processing holds the largest share of the application segment, driven by the constant exposure to high temperatures and potential ignition sources in rolling mills and forging operations. The ability of fire-resistant fluids to reduce fire hazards has made them a standard in this industry.

Mining emerges as the fastest growing application segment, supported by increasing automation and mechanization in underground and surface mining operations. The need to enhance equipment safety and reliability in flammable and high-pressure conditions is pushing demand for specialized hydraulic fluids. In 2024, mining applications grew by over 6% year-on-year, as companies aimed to reduce equipment downtime and ensure operational safety.

Other applications such as aviation and power generation also show steady growth, primarily due to stringent regulations and the criticality of operations that cannot risk hydraulic fluid fires.

The primary end-users in the fire resistant hydraulic fluids market are segmented into manufacturing, construction, mining, aerospace, marine, and energy sectors. Manufacturing continues to be the largest end-user segment, accounting for over 30% of the total demand in 2024. This dominance is attributed to the widespread use of hydraulic systems in automated processes, presses, and machining equipment across global manufacturing facilities. These environments often operate under high heat, pressure, and the presence of ignition sources, necessitating the use of fire-resistant fluids.

The aerospace sector is the fastest growing end-user segment due to an increased emphasis on in-flight safety, ground support equipment reliability, and military-grade performance standards. Fire-resistant hydraulic fluids are being increasingly adopted in aircraft systems, where hydraulic fluid leaks pose significant risks. Additionally, with rising aircraft production and defense investments worldwide, demand from the aerospace industry is expected to surge.

Other sectors like mining and energy are also adopting these fluids at a growing rate, supported by regulatory compliance mandates and increasing awareness of operational risks.

North America accounted for the largest market share at 32.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2025 and 2032.

This regional trend is shaped by industrial maturity in North America and emerging industrialization and infrastructure development across Asia-Pacific. Europe followed closely behind, driven by strict safety standards and a mature manufacturing base. Meanwhile, the Middle East & Africa and South America are showing a steady increase in demand, supported by investments in mining, oil, and heavy industries. Each region has distinct drivers, but the overarching factors include rising awareness about workplace safety, environmental sustainability, and the need for fluid performance under extreme conditions.

Technological Leadership and Stringent Safety Standards Driving Adoption

North America maintains its dominance in the global fire resistant hydraulic fluids market due to strong industrial adoption and rigorous safety regulations enforced by agencies such as OSHA. In 2024, the region generated over USD 500 million in revenue, with the United States alone contributing more than 70%. Sectors like metal processing, aerospace, and defense remain the primary consumers. Moreover, the incorporation of AI and IoT technologies in hydraulic systems has increased fluid monitoring and maintenance efficiency. Canadian mining operations and U.S. steel production have witnessed a surge in demand for HFD and HFC fluids to mitigate fire risks and ensure compliance.

Sustainability-Driven Market Acceleration in Industrial Hubs

Europe’s fire resistant hydraulic fluids market is fueled by its focus on environmental sustainability and workplace safety. In 2024, Germany, France, and Italy were the largest contributors, together accounting for over 60% of the regional market. Europe has a high preference for biodegradable and synthetic fluids, such as HFD-U and HFD-S, used across manufacturing, rail transport, and power generation. Renewable energy infrastructure, including wind and hydroelectric plants, increasingly integrates fire resistant fluids for equipment safety. Additionally, the EU's REACH compliance framework has accelerated the phasing out of conventional fluids in favor of fire-resistant alternatives.

Rapid Industrialization and Urbanization Fueling Regional Growth

Asia-Pacific is the fastest-growing region in the fire resistant hydraulic fluids market, led by China, India, South Korea, and Japan. In 2024, China held over 40% of the regional market share due to its massive industrial sector and ongoing infrastructure projects. India is emerging rapidly with increased demand from construction and mining. Local manufacturers are investing in advanced fluid technologies to cater to the high-temperature and high-load demands of steel plants and automotive manufacturing. Moreover, the region’s rise in renewable energy projects and emphasis on operational safety are contributing to a growing preference for synthetic and biodegradable hydraulic fluids.

Mining and Oil & Gas Investments Accelerating Demand

South America’s fire resistant hydraulic fluids market is gaining momentum, primarily driven by mining and oil exploration activities in Brazil, Chile, and Peru. Brazil accounted for more than 45% of the regional revenue in 2024. With the expansion of open-pit and underground mining operations, there is a rising demand for fire-resistant fluids in hydraulic drilling and excavation equipment. Chile’s copper mining sector and Venezuela’s oil industry also contribute to the increasing need for safer and high-performance hydraulic fluids. The market is witnessing a shift towards water-glycol-based fluids due to their better cooling properties in high-heat environments.

Infrastructure Growth and Industrial Safety Enhancing Market Penetration

The Middle East & Africa region is seeing steady growth in the fire resistant hydraulic fluids market, driven by construction, oil & gas, and mining sectors. The UAE and Saudi Arabia collectively contributed to more than 55% of the regional revenue in 2024. The ongoing mega infrastructure projects such as NEOM in Saudi Arabia are pushing demand for fire-safe fluid systems. In Africa, South Africa and Nigeria are leading in adoption due to mining activities and industrial expansions. Regional industries are progressively replacing traditional fluids with synthetic and HFC alternatives to improve equipment longevity and safety compliance in high-risk environments.

United States: USD 350 million in 2024 – driven by extensive adoption in aerospace, defense, and industrial machinery sectors.

China: USD 240 million in 2024 – fueled by rapid industrialization, infrastructure expansion, and manufacturing sector growth.

The global fire-resistant hydraulic fluids market is characterized by intense competition, driven by technological advancements and stringent safety regulations across industries. Major players are focusing on developing innovative, eco-friendly formulations to meet the evolving demands of various sectors such as aerospace, marine, and manufacturing. The market is witnessing a surge in demand for biodegradable and synthetic fluids, prompting companies to invest heavily in research and development. Strategic collaborations and mergers are also prevalent, enabling firms to expand their product portfolios and global reach. For instance, in March 2024, Kodiak acquired Aztech Lubricants to strengthen its position in the specialty chemical sector, specifically in fire-resistant hydraulic fluids. Similarly, Shell's acquisition of MIDEL and MIVOLT brands in January 2024 bolstered its offerings in synthetic and natural ester-based transformer fluids, enhancing fire safety and environmental friendliness. These developments underscore the dynamic nature of the market, with companies striving to gain a competitive edge through innovation and strategic partnerships.

ExxonMobil Corporation

BASF SE

Castrol Limited

American Chemical Technologies, Inc.

Dow Inc.

Quaker Houghton

Southwestern Petroleum Corporation

Eastman Chemical Company

TotalEnergies SE

SINOPEC

MORESCO Corporation

Idemitsu Kosan Co., Ltd.

Chevron Corporation

Fuchs Petrolub SE

BP plc

Royal Dutch Shell

LANXESS AG

Sasol Limited

Lubrication Engineers, Inc.

Zeller+Gmelin GmbH & Co. KG

Technological advancements are playing a pivotal role in shaping the fire-resistant hydraulic fluids market. The integration of smart technologies into hydraulic systems is driving the demand for advanced fluid properties that can respond dynamically to operational changes. For instance, the rise of Industrial Internet of Things (IIoT) technology allows for real-time monitoring of hydraulic systems, providing early warnings of potential fluid-related issues, enhancing safety, and optimizing fluid usage.

Moreover, the industry is witnessing a shift towards synthetic and biodegradable fluids due to their superior performance characteristics and lower environmental impact. These fluids are often preferred in regions with stringent environmental regulations. Companies are focusing on developing customized fire-resistant fluids tailored to the specific needs of different industries, including fluids optimized for temperature extremes, high-pressure systems, and specific environmental conditions.

Additionally, advancements in fluid formulations are improving compatibility with various hydraulic systems, boosting their adoption. The development of bio-based fire-resistant hydraulic fluids that are less polluting while providing the same performance characteristics as conventional mineral oil-based fluids is gaining traction. These innovations not only enhance environmental sustainability but also deliver cost efficiencies and reduce the risk of property damage and injuries associated with industrial fires.

In March 2024, Kodiak announced its acquisition of Aztech Lubricants, aiming to bolster its presence in the specialty chemical sector, specifically in fire-resistant hydraulic fluids. This strategic move allows Kodiak to expand its product portfolio and market reach, enhancing its capabilities in providing advanced fluid solutions for industries requiring safety and reliability.

In January 2024, Bosch Rexroth, in collaboration with TotalEnergies, embarked on an innovative venture to engineer a water-based, biodegradable hydraulic fluid that maintains the performance standards of conventional mineral oils while mitigating environmental impact. It is envisioned to enhance environmental sustainability, deliver cost efficiencies, and reduce the risk of property damage and injuries associated with industrial fires.

In January 2024, Shell U.K. Limited announced the acquisition of the highly esteemed MIDEL and MIVOLT brands from M&I Materials Ltd., positioning them at the forefront of the fire-resistant hydraulic fluids industry. The integration of MIDEL's synthetic and natural ester-based transformer fluids into Shell's diverse lubricants portfolio bolsters their standings with a product suite characterized by enhanced fire safety and environmental friendliness.

In July 2022, Quaker Houghton entered into a collaboration to combine SKF RecondOil’s Double Separation Technology (DST) with Quaker Houghton’s industrial oils and application expertise to enable the industry to more efficiently utilize its resources by reducing the unsustainable linear use of oil.

The fire-resistant hydraulic fluids market report provides a comprehensive analysis of market trends, dynamics, and growth opportunities from 2024 to 2032. It delves into various segments, including product types, applications, and end-user industries, offering insights into market drivers, restraints, and challenges. The report highlights the increasing demand for environmentally friendly and high-performance fluids across industries such as aerospace, marine, manufacturing, and mining.

It examines the impact of technological advancements, such as the integration of smart technologies and the development of biodegradable fluids, on market growth. The report also explores regional market trends, identifying North America as the largest market in 2024 and Asia-Pacific as the fastest-growing region, driven by rapid industrialization and infrastructure development.

Furthermore, the report profiles key market players, analyzing their strategies, product portfolios, and recent developments. It underscores the importance of innovation, strategic partnerships, and mergers in gaining a competitive edge. The report serves as a valuable resource for stakeholders, providing actionable insights to navigate the evolving landscape of the fire-resistant hydraulic fluids market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Fire Resistant Hydraulic Fluids Market |

| Market Revenue (2024) | USD 1.56 Billion |

| Market Revenue (2032) | USD 2.01 Billion |

| CAGR (2025–2032) | 3.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ExxonMobil Corporation, BASF SE, Castrol Limited, American Chemical Technologies, Inc., Dow Inc., Quaker Houghton, Southwestern Petroleum Corporation, Eastman Chemical Company, TotalEnergies SE, SINOPEC, MORESCO Corporation, Idemitsu Kosan Co., Ltd., Chevron Corporation, Fuchs Petrolub SE, BP plc, Royal Dutch Shell, LANXESS AG, Sasol Limited, Lubrication Engineers, Inc., Zeller+Gmelin GmbH & Co. KG |

| Customization & Pricing | Available on Request (10% Customization is Free) |