Global Fire-resistant Adhesives Market Report Overview

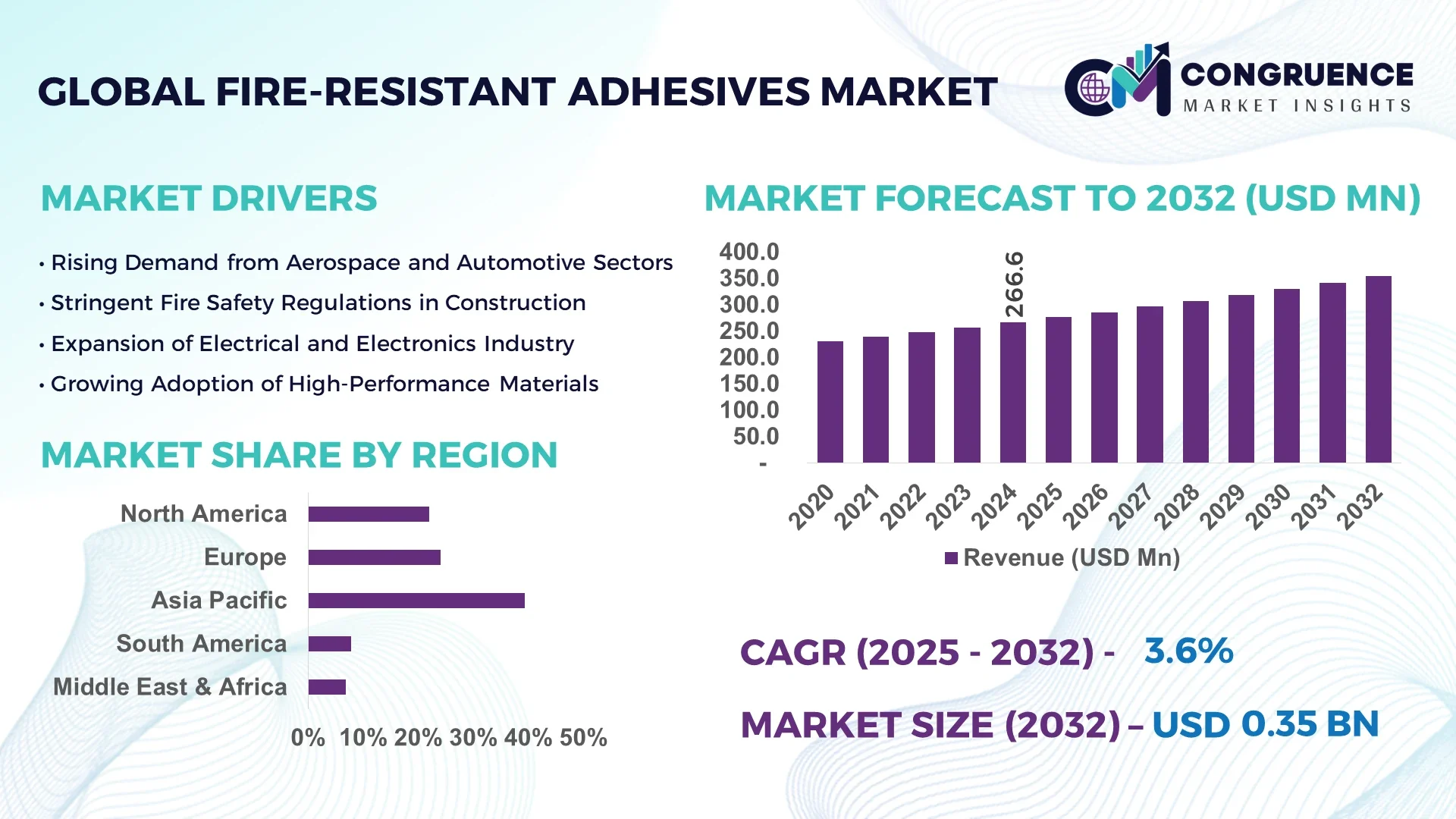

The Global Fire-resistant Adhesives Market was valued at USD 266.56 Million in 2024 and is anticipated to reach a value of USD 353.734 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032.

The United States accounted for the largest share of the global fire-resistant adhesives market in 2024, with widespread utilization in construction composites, aerospace insulation panels, electric vehicle battery enclosures, and industrial fireproofing solutions.

The fire-resistant adhesives market is evolving rapidly, driven by the growing need for materials that can withstand extreme temperatures and fire exposure across sectors like construction, automotive, aerospace, and electronics. Silicone-based fire-resistant adhesives led the market with over 45% market share due to their superior performance in high-temperature conditions. The construction sector represented approximately 40% of the total demand, propelled by increasing global infrastructure development and fire safety mandates. Automotive and aerospace industries are also major contributors, leveraging these adhesives for engine compartments, cabin interiors, and fuselage components. Stringent safety regulations across the U.S., EU, and Asia-Pacific have further boosted the use of certified fire-resistant bonding solutions. Advancements in adhesive technologies are creating more versatile and durable products suitable for multi-substrate bonding under high thermal stress. This steady growth pattern is expected to continue, supported by R&D innovations and adoption across fire-sensitive applications.

How is AI Transforming Fire-resistant Adhesives Market?

Artificial Intelligence is transforming the fire-resistant adhesives market by revolutionizing how adhesives are researched, developed, and manufactured. AI and machine learning algorithms are being used to create smarter formulations by analyzing massive datasets to discover optimal chemical structures for fire resistance, thermal stability, and bonding strength. These AI-driven models can predict adhesive performance in high-temperature environments without the need for physical testing, thereby accelerating R&D cycles.

AI is also reshaping manufacturing by enabling real-time process control and predictive maintenance. Smart sensors paired with AI algorithms help detect viscosity changes, curing quality, or bonding anomalies, ensuring consistent product performance. In automated production lines, AI systems optimize adhesive mixing ratios and monitor application precision to prevent bonding failures in critical safety environments like aircraft cabins or electrical enclosures. Moreover, AI aids regulatory compliance by simulating how formulations respond under fire conditions, aligning development with fire safety standards such as ASTM E84 or UL 94. AI is becoming indispensable in achieving quality, safety, and speed in the development and production of fire-resistant adhesives, giving manufacturers a technological edge in a highly regulated and competitive landscape.

"In 2025, researchers introduced a machine learning platform that predicts flammability metrics such as heat release rate and ignition time in polymers. The tool, integrated into the MatVerse cloud interface, uses advanced algorithms to simulate and design new fire-resistant materials, enhancing the formulation of safer adhesives without lengthy physical testing."

Fire-resistant Adhesives Market Dynamics

The fire-resistant adhesives market is shaped by a range of factors including material innovation, application expansion across industries, and regulatory requirements for fire safety. As industries like automotive, construction, aerospace, and electronics demand reliable bonding under high-temperature conditions, the role of fire-resistant adhesives continues to grow. The increasing adoption of lightweight materials, electric vehicles, and composite structures has made flame-retardant bonding essential. While innovation and demand are propelling the market forward, certain regulatory, cost, and material compatibility factors continue to act as constraints. However, with the growth of smart manufacturing and rising awareness of fire protection, new opportunities are emerging.

DRIVER:

Expanding Infrastructure and Construction Projects

The global construction industry is experiencing strong growth, particularly in high-rise buildings, tunnels, and public infrastructure that require stringent fire safety measures. Fire-resistant adhesives are being increasingly adopted for bonding insulation materials, panels, and structural components. As of 2024, over 40% of the total fire-resistant adhesive demand was attributed to construction-related applications. Countries like China, India, and the UAE have introduced new fire compliance codes for commercial and residential buildings, accelerating product deployment. Additionally, the use of flame-retardant adhesives in sealing HVAC ducts and fire doors is rising. This sector-wide need for flame-safe infrastructure is significantly boosting market momentum.

RESTRAINT:

High Formulation Costs and Performance Trade-offs

Fire-resistant adhesives, especially those based on silicone, epoxy, and polyimide chemistries, often come with high raw material and processing costs. Manufacturers face difficulties in balancing fire retardancy, adhesion strength, and flexibility, making it challenging to create universal formulations. In 2024, silicone-based fire-resistant adhesives cost up to 35% more than standard industrial adhesives. Additionally, performance limitations such as longer curing times and substrate compatibility issues restrict their widespread adoption in budget-sensitive applications. These cost-performance trade-offs discourage smaller manufacturers and OEMs from transitioning to high-grade fire-resistant adhesive systems, slowing market penetration in certain segments.

OPPORTUNITY:

Integration of Fire-resistant Adhesives in EV Battery Packs

The rise of electric vehicles (EVs) is opening a major avenue for fire-resistant adhesives. Battery packs, which are sensitive to thermal runaway and combustion risks, are increasingly being designed with non-combustible enclosures using fire-retardant bonding materials. In 2024, over 30% of premium EV models included some form of flame-retardant adhesive for internal battery components, fire barriers, or sensor modules. This trend is expected to intensify with the growing demand for enhanced EV safety standards globally. OEMs are investing in low-VOC, thermally resistant adhesives that can sustain battery heat loads while improving structural strength—making this a prime opportunity for adhesive innovation and market expansion.

CHALLENGE:

Regulatory Compliance and Certification Complexities

One of the most pressing challenges in the fire-resistant adhesives market is the need to meet varying international fire safety standards. Regulations such as UL 94, NFPA 285, ASTM E84, and EN 13501-1 differ across regions, requiring extensive testing, third-party certifications, and reformulations. Adhesive manufacturers are often compelled to create region-specific variants, increasing R&D costs and time-to-market. In 2024, nearly 25% of new product launches in this space were delayed due to compliance bottlenecks. These certification challenges hinder global scalability and complicate cross-border trade, especially for small and medium-sized enterprises (SMEs) that lack the resources for repeated regulatory processes.

Fire-resistant Adhesives Market Trends

• Rise in Sustainable Construction Materials: The growing demand for sustainable and energy-efficient buildings is influencing material choices, including the use of fire-resistant adhesives with low VOC content and halogen-free formulations. Construction companies are integrating these adhesives into insulation panels, cladding systems, and structural glazing. In 2024, over 55% of green-certified commercial buildings in North America utilized flame-retardant adhesives to meet LEED and fire compliance standards. As green building certifications become mandatory in more regions, this trend is expected to intensify, supporting the steady adoption of eco-friendly adhesive solutions.

• Expansion of Aerospace Interior Applications: Fire-resistant adhesives are being increasingly adopted in aerospace interiors to bond floor panels, overhead bins, insulation blankets, and seating systems. With the aviation sector recovering steadily post-pandemic, OEMs are prioritizing lightweight and fireproof bonding solutions for passenger safety. In 2024, approximately 70% of newly manufactured narrow-body aircraft integrated fire-rated adhesives for cabin interior assemblies. Europe and the U.S. are the leading regions for such adoption due to stringent FAA and EASA flammability requirements.

• Growing Integration in Electronics Assembly: The electronics industry is witnessing growing demand for fire-resistant adhesives to ensure device safety, particularly in high-performance devices and lithium-ion battery enclosures. These adhesives are used for PCB encapsulation, wire insulation, and thermal interface bonding. In 2024, over 40% of fire incidents in consumer electronics were linked to inadequate fire insulation, prompting OEMs to adopt high-temperature-resistant adhesives. Asia-Pacific leads in manufacturing adoption, especially in China, Japan, and South Korea.

• Increased Usage in Mass Transit Systems: Urban transit networks, including metros and high-speed rail, are incorporating fire-resistant adhesives in panel bonding, flooring systems, and electrical cable management to ensure passenger safety. The rail industry has introduced stricter fire compliance protocols, especially for interior applications. In 2024, fire-rated adhesives were used in over 65% of newly commissioned metro trains in Asia and Europe. These adhesives help maintain structural integrity during fire events and reduce toxic smoke generation, aligning with evolving safety norms in public transportation infrastructure.

Segmentation Analysis

The global fire-resistant adhesives market is segmented by type, application, and end-user insights. Each segment plays a vital role in determining the growth trajectory and demand across industrial, commercial, and infrastructure verticals. Different adhesive types cater to unique performance requirements across sectors such as construction, automotive, electronics, and aerospace. Applications range from structural bonding to insulation, while end-user insights reveal deeper adoption trends in sectors demanding stringent fire safety protocols. With increasing regulatory pressures and safety standards across geographies, manufacturers are diversifying their offerings by focusing on high-temperature performance, smoke suppression, and compatibility with a variety of substrates to target niche growth pockets within each segment.

By Type

The fire-resistant adhesives market is categorized into epoxy adhesives, silicone adhesives, polyurethane adhesives, acrylic adhesives, and otherssuch as phenolic-based and polyimide adhesives. Among these, epoxy adhesivesaccounted for the largest market share in 2024, with over 38% share globally, owing to their superior heat resistance, high tensile strength, and excellent bonding with metals and composites. These adhesives are widely used in the construction and aerospace sectors. Meanwhile, silicone adhesivesare emerging as the fastest-growing segment, projected to expand significantly between 2025 and 2032, driven by their excellent flexibility and durability under fluctuating thermal environments. Silicone adhesives are particularly preferred in electronics and electric vehicles (EVs), where components are exposed to constant heating and cooling cycles. Polyurethane adhesiveshold notable traction in transportation and insulation applications due to their low-smoke formulation and strong adhesion to plastics. Acrylic adhesives remain niche, mainly in lightweight assembly solutions. The diversification across types allows manufacturers to target a broader array of heat-resilient bonding requirements.

By Application

The primary applications for fire-resistant adhesives include building & construction, automotive & transportation, aerospace, electronics, and otherssuch as marine and energy systems. In 2024, building & constructionemerged as the dominant application segment, capturing over 41% of the market share, due to the surge in demand for non-combustible bonding materials in façades, cladding systems, HVAC insulation, and structural panel bonding. The segment is also being driven by stringent fire safety building codes globally. Automotive & transportationis the second-largest segment, where adhesives are used in thermal insulation panels, battery components, and vehicle interiors. However, the aerospaceapplication segment is projected to witness the fastest growth during the forecast period due to increased usage of lightweight flame-retardant adhesives in aircraft interiors and composite bonding. The electronicssegment continues to see growing adoption of fire-resistant adhesives in PCBs and battery packs, especially with the rise in consumer electronics and EV production. Each application drives a different demand dynamic based on material performance under heat stress and regulatory compliance.

By End-User Insights

Fire-resistant adhesives are utilized across a variety of end-user sectors, including construction companies, automotive manufacturers, aerospace OEMs, electronics and electrical equipment producers, and otherssuch as defense and marine. In 2024, construction companiesled the market with over 44% share, primarily due to their extensive usage of flame-retardant adhesives in both residential and commercial infrastructure projects. The increasing global emphasis on fire-safe building envelopes and eco-friendly adhesives is bolstering demand in this segment. Meanwhile, aerospace OEMsare the fastest-growing end-user segment, driven by the recovery in global air travel and rising production of new-generation aircraft that require advanced flame-resistant bonding materials. Automotive manufacturerscontinue to adopt such adhesives for fireproofing EV battery housings and under-the-hood components. Electronics producersare also ramping up adoption due to the rising concern over thermal events and circuit overheating. The demand pattern reflects a shift toward high-reliability bonding solutions across increasingly complex industrial environments.

Region-Wise Market Insights

Asia-Pacific accounted for the largest market share at 39.4% in 2024; however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.3% between 2025 and 2032.

The Asia-Pacific region has maintained its leadership position due to rapid urbanization, stringent fire safety regulations in the construction industry, and the large-scale presence of manufacturing facilities using fire-resistant adhesives. Countries like China, India, and Japan have shown a steep rise in demand across automotive, electronics, and industrial applications. Meanwhile, the Middle East & Africa is witnessing a strong uptick in adoption, particularly in large-scale infrastructure projects, airport expansions, and smart city developments across the UAE, Saudi Arabia, and South Africa. Increasing awareness and government mandates around building safety are driving demand in emerging economies. Regional manufacturers are also leveraging local production and international partnerships to bridge demand-supply gaps effectively.

North America Fire-resistant Adhesives Market Trends

Construction Retrofitting and Aerospace Innovations Fuel Demand in North America

In 2024, North America accounted for approximately 23.7%of the global fire-resistant adhesives market. The U.S. leads this region, driven by growing infrastructure renovation projects, building code compliance, and increased aircraft manufacturing. In the construction sector, fire-retardant materials are widely used in insulation systems, wall paneling, and ducting applications. Boeing and other aerospace giants are utilizing flame-resistant adhesives for interior assemblies and thermal shielding, especially in newer aircraft fleets. Canada is also observing a rise in adoption, particularly in the rail and defense sectors. Additionally, the presence of major chemical manufacturers and ongoing investments in R&D for low-VOC and halogen-free formulations are strengthening the region’s position.

Europe Fire-resistant Adhesives Market Trends

Strict Fire Safety Standards in Buildings Accelerate European Market Growth

Europe held around 21.9%of the fire-resistant adhesives market in 2024, with Germany, France, and the UK being the primary contributors. Germany is at the forefront due to its stringent EU safety standards for building materials and widespread usage of flame-retardant adhesives in modular construction and high-rise buildings. France has significantly integrated these adhesives into public infrastructure such as tunnels and rail stations. Meanwhile, the UK is implementing more rigorous fire protection rules post-Grenfell disaster, accelerating the usage of certified bonding agents in housing and public buildings. The region is also actively adopting fire-safe adhesives in EV battery manufacturing, especially across Scandinavia and Central Europe.

Asia-Pacific Fire-resistant Adhesives Market Trends

Industrial Expansion and EV Production Drive Asia-Pacific Market Surge

Asia-Pacific dominated the market with 39.4%share in 2024, attributed to rapid industrial growth, infrastructure development, and escalating fire safety standards. China remains the largest contributor, with extensive application in real estate, electronics, and transportation sectors. Japan and South Korea are increasing their focus on fire-rated adhesives in electric vehicle battery assembly and consumer electronics. India is showing impressive growth due to large-scale public construction, road tunnels, and metro rail systems. This region is also witnessing a shift toward high-temperature adhesives in aerospace and defense, supported by governmental policies encouraging the domestic production of advanced materials.

South America Fire-resistant Adhesives Market Trends

Infrastructure Projects and Automotive Growth Stimulate South American Market

South America contributed around 6.2%of the global fire-resistant adhesives market in 2024, with Brazil and Argentina accounting for the majority of the share. Brazil is heavily investing in urban infrastructure upgrades, stadiums, airports, and transportation hubs, all of which require certified fire-resistant bonding materials. The country is also seeing increased applications in railways and automotive interiors. Argentina is catching up due to growing industrial safety regulations and its emerging electronics assembly sector. The rise in prefab construction and automotive export activities from South America is encouraging manufacturers to focus on thermally resistant adhesive formulations to meet both local and international safety standards.

Middle East & Africa Fire-resistant Adhesives Market Trends

Mega Infrastructure and Aviation Projects Bolster Demand in MEA

The Middle East & Africa held about 8.8%of the market in 2024 and is expected to witness the fastest expansion by 2032. Saudi Arabia and the UAE are leading demand due to massive infrastructure investments in Neom City, Expo legacy projects, and airport terminals. Flame-retardant adhesives are widely being used in aluminum composite panel installations, HVAC insulation, and smart building systems. South Africa is also showing traction, particularly in commercial and industrial zones where new fire safety regulations are being enforced. The surge in aerospace parts manufacturing and luxury vehicle imports further boosts adhesive usage in high-performance and temperature-sensitive applications.

Top Two Countries Holding Highest Market Share:

-

Chinaholds the highest market share at 28.1%, driven by its expansive construction sector, electronics manufacturing, and the rapidly growing electric vehicle industry.

-

United Statesfollows with 17.3%of the market share, supported by strong demand in aerospace, defense, and retrofitting projects, making it a significant player in the fire-resistant adhesives market.

Market Competition Landscape

The fire-resistant adhesives market is highly competitive, with a mix of global and regional players contributing to market growth. Several leading companies are focusing on innovation, product diversification, and strategic partnerships to maintain their position. The market is characterized by significant mergers, acquisitions, and joint ventures to expand market reach and product offerings. Industry leaders such as Henkel AG, 3M Company, and Sika AG are actively involved in the development of advanced fire-resistant adhesives for a wide range of applications, from construction to automotive and electronics. Additionally, companies are emphasizing sustainability and the use of eco-friendly materials in their adhesive formulations to align with evolving regulatory standards and consumer preferences. The increasing demand for fire safety, particularly in construction and industrial sectors, is driving manufacturers to invest in research and development to meet the growing need for high-performance adhesives. As the market continues to mature, competition is expected to intensify, with more companies looking to strengthen their market presence through technological advancements.

Companies Profiled in the Fire-resistant Adhesives Market Report

Technology Insights for the Fire-resistant Adhesives Market

The fire-resistant adhesives market has seen significant advancements in technology, driven by increasing demand for safety and efficiency in various industries, such as construction, automotive, and electronics. The development of high-performance adhesives that offer superior fire resistance, durability, and environmental sustainability has become a major focus for manufacturers. Key technological innovations include the introduction of advanced formulations that improve the adhesive's thermal stability, water resistance, and structural bonding strength, which are critical for applications in high-risk environments.

One major technological trend is the incorporation of intumescent additivesin fire-resistant adhesives. These additives expand when exposed to heat, creating a protective barrier that prevents the spread of flames and reduces the temperature of the underlying surface. This technology is particularly beneficial in building and construction applications, where fire safety is paramount. Additionally, nanotechnologyis gaining traction, with companies exploring the use of nanomaterials to enhance the properties of fire-resistant adhesives. These materials improve the adhesive’s performance by increasing its heat resistance and ensuring a stronger bond even under extreme temperatures.

Furthermore, eco-friendly and sustainable adhesivesare becoming a significant area of focus, as industries push toward reducing their environmental footprint. Adhesive manufacturers are increasingly using bio-based resins and recycled materials in their formulations to meet environmental regulations and cater to the growing consumer demand for green solutions. These technological advancements are driving the fire-resistant adhesives market, ensuring that products meet the highest standards of fire safety, environmental impact, and performance.

Recent Developments in the Global Fire-resistant Adhesives Market

-

In February 2024, Henkel AG launched two new medical-grade cyanoacrylate-based instant adhesives designed to deliver increased strength during and after heat cycling. These adhesives contain no Carcinogenic, Mutagenic, or Reproductively Hazardous (CMR) substances, aligning with stringent safety standards in medical applications.

-

In September 2023, DELO introduced the first dual-curing, high-temperature adhesive, DELO DUALBOND HT2990, specifically designed for electric motor applications. This adhesive is suitable for a range of applications, including magnet bonding and stacking in electric motor manufacturing.

-

In October 2024, Bostik rolled out Born2Bond Ultra K85, a heat-resistant adhesive solution for product designers, design engineers, and manufacturers seeking an adhesive that offers resistance to high temperatures and humidity, catering to industries requiring robust bonding solutions.

-

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

Scope of Fire-resistant Adhesives Market Report

The Fire-resistant Adhesives market report provides comprehensive insights into the evolving industry landscape, focusing on the demand, production, and application of high-performance adhesives capable of withstanding extreme heat. The scope of the report covers a detailed analysis of various types of fire-resistant adhesives, including epoxies, polyurethanes, and silicones, designed for use in a range of industrial applications.

The report emphasizes market trends such as the increasing adoption of these adhesives in the automotive, aerospace, and construction sectors, where fire safety standards are paramount. Furthermore, it highlights the growing demand for fire-resistant materials that contribute to sustainability and energy efficiency, with a particular focus on regulations and their impact on product development.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing insights into regional demand and emerging market trends. It also examines end-user industries, such as automotive manufacturing, construction, and electronics, where fire-resistant adhesives play a critical role in ensuring safety, durability, and performance.

This market report is essential for companies seeking to understand the competitive landscape, technological advancements, and regional market dynamics shaping the future of fire-resistant adhesive solutions.

Fire-resistant Adhesives Market Report Summary

| Report Attribute/Metric |

Report Details |

|

Market Revenue in 2024

|

USD 266.56 Million

|

|

Market Revenue in 2032

|

USD 353.734 Million

|

|

CAGR (2025 - 2032)

|

3.6%

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2032

|

|

Historic Period

|

2020 - 2024

|

|

Segments Covered

|

By Types

-

Acrylic

-

Silicone

-

Epoxy

-

Polyurethane

-

Others

By Application

By End-User

-

Residential

-

Commercial

-

Industrial

|

|

Key Report Deliverable

|

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape

|

|

Region Covered

|

North America, Europe, Asia-Pacific, South America, Middle East, Africa

|

|

Key Players Analyzed

|

Henkel AG, 3M Company, Sika AG, BASF SE, H.B. Fuller Company, Arkema S.A., ITW (Illinois Tool Works), Lord Corporation, Avery Dennison Corporation, Dupont

|

|

Customization & Pricing

|

Available on Request (10% Customization is Free)

|