Reports

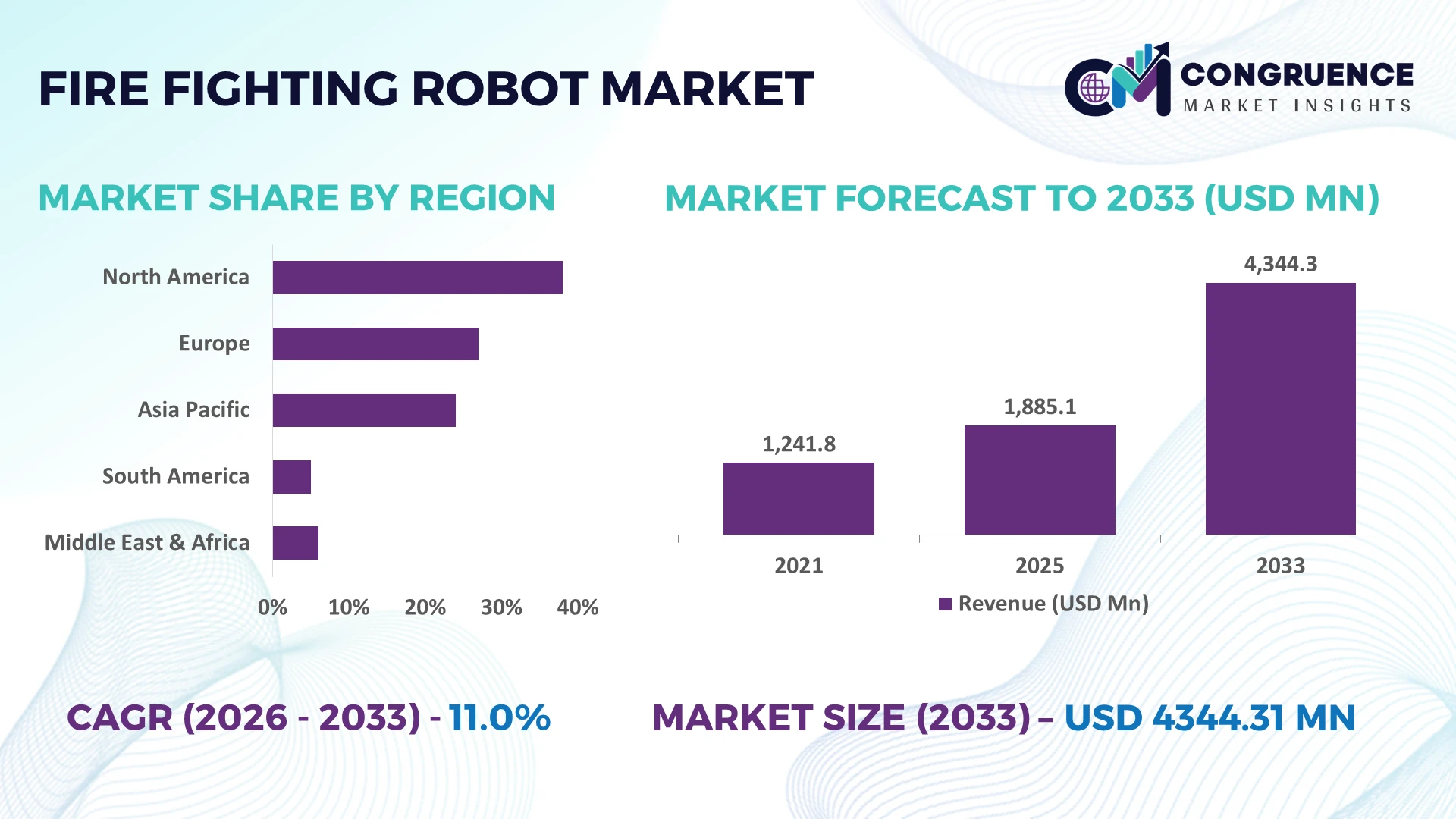

The Global Fire Fighting Robot Market was valued at USD 1885.11 Million in 2025 and is anticipated to reach a value of USD 4344.31 Million by 2033 expanding at a CAGR of 11% between 2026 and 2033. Growth is primarily driven by rising industrial fire safety automation, stricter hazardous-environment compliance, expanding smart infrastructure projects, and AI-enabled robotic systems capable of operating in high-temperature, toxic, and explosion-prone environments.

China leads the global Fire Fighting Robot Market with approximately 34% manufacturing share, supported by large-scale investments in industrial safety, petrochemicals, and smart manufacturing, while Japan maintains higher deployment density across advanced industrial facilities with over 20% greater robot utilization in hazardous-response operations. Ongoing industrial resilience initiatives following global supply-chain realignments continue accelerating autonomous firefighting technology adoption across critical sectors.

The market favors manufacturers and investors that prioritize AI-enabled autonomy, ruggedized platforms, and partnerships across industrial safety ecosystems to strengthen long-term competitive positioning.

Market Size & Growth: USD 1885.11 million in 2025 to USD 4344.31 million by 2033 at 11% CAGR, supported by advanced industrial automation and stricter fire safety compliance.

Top Growth Drivers: Industrial automation adoption +28%, hazardous facility modernization +24%, AI-enabled emergency response deployment +21% accelerate global demand.

Short-Term Forecast: By 2028, emergency response efficiency improves 30% while hazardous firefighter exposure declines nearly 25% through autonomous deployment.

Emerging Technologies: AI vision, thermal imaging, LiDAR navigation, and edge computing improve autonomous obstacle avoidance with over 35% higher mission accuracy.

Regional Leaders: Asia-Pacific exceeds USD 1.9 billion, North America approaches USD 1.2 billion, Europe surpasses USD 850 million, driven by industrial safety upgrades and regional expansion.

Consumer/End-User Trends: More than 42% of large industrial facilities prioritize robotic firefighting solutions for chemical, energy, and logistics operations.

Pilot/Case Example: A 2025 industrial deployment reduced emergency response time by 32% and improved hazardous-area intervention efficiency by 27%.

Competitive Landscape: Leading manufacturers collectively control approximately 38% market share, supported by innovation from several global robotics and industrial safety companies.

Regulatory & ESG Impact: Updated industrial safety standards reduce workplace fire incidents by nearly 18% while strengthening ESG-focused risk management programs.

Investment & Funding: Over USD 1.3 billion supports robotics innovation, strategic partnerships, localized production, and resilient supply-chain expansion across high-growth regions.

Innovation & Future Outlook: Multi-robot coordination, 5G connectivity, and autonomous decision systems increase mission effectiveness by over 40%, reinforcing next-generation emergency response strategies.

Fire Fighting Robot Market demand continues expanding across petrochemical complexes, tunnels, airports, power generation, and logistics hubs where autonomous operation improves responder safety. AI-based thermal analytics, high-pressure suppression systems, and remote command platforms enhance operational precision, while more than 35% of newly deployed industrial safety robots integrate real-time sensor fusion. Strengthening industrial safety regulations and resilient component sourcing continue shaping procurement strategies, setting the stage for deeper strategic evaluation.

The Fire Fighting Robot Market has become strategically important as industrial operators, governments, and critical infrastructure owners prioritize autonomous emergency response to improve operational resilience and workforce safety. Infrastructure modernization, stricter industrial fire protection standards, and digital transformation across energy, chemical, logistics, and transportation sectors are accelerating procurement decisions. Supply-chain restructuring since recent geopolitical disruptions has also encouraged localized production of robotics, sensors, and thermal imaging systems, reducing procurement risks while strengthening long-term deployment capabilities.

Modern AI-enabled fire fighting robots complete hazardous inspections up to 40% faster than conventional manual response teams while reducing firefighter exposure in high-risk environments by nearly 60%. China leads large-scale manufacturing and industrial deployment, whereas Japan emphasizes high-precision autonomous navigation and compact robotic platforms for complex facilities. Over the next two to three years, adoption across hazardous industrial assets is expected to expand by more than 25%, supported by wider integration of edge computing, machine vision, and real-time command platforms into emergency response networks.

A practical example is the deployment of autonomous fire fighting robots in petrochemical complexes, where remote-controlled suppression systems and thermal analytics reduce emergency intervention time while maintaining operational continuity during high-risk incidents. Companies are expanding strategic partnerships with industrial automation providers, investing in software-driven autonomous capabilities, and strengthening localized engineering support to improve deployment efficiency. Organizations that combine intelligent robotics with integrated safety ecosystems will secure stronger competitive positioning through faster emergency response, improved asset protection, and greater operational resilience.

Industrial safety modernization is the primary structural driver reshaping the Fire Fighting Robot Market. More than 45% of newly developed petrochemical and energy facilities now integrate robotic emergency response planning during project design, while AI-assisted navigation improves operational accuracy by nearly 35% and reduces hazardous human exposure by approximately 50%. China continues expanding intelligent manufacturing initiatives, encouraging wider deployment of autonomous safety equipment across industrial parks. This structural transition increases demand for integrated robotic platforms rather than standalone machines. Companies are responding through robotics partnerships, expanded production capacity, and continuous investment in thermal imaging, autonomous mobility, and remote command technologies, creating stronger differentiation through end-to-end industrial safety solutions.

Deployment remains constrained by compatibility challenges between advanced robotic platforms and aging industrial safety infrastructure. Nearly 38% of manufacturing facilities still operate legacy fire detection architectures requiring costly system upgrades, while integration expenses can increase project implementation costs by around 20%. Dependence on specialized sensors, rugged electronic components, and high-performance batteries continues creating procurement pressure during supply-chain disruptions. Industrial operators in India and Southeast Asia frequently phase deployments over multiple investment cycles to control capital expenditure. Manufacturers are reducing implementation risks through modular system architecture, localized component sourcing, long-term supplier agreements, and standardized communication protocols that simplify interoperability while improving deployment scalability.

The strongest opportunity lies in transforming fire fighting robots into intelligent safety platforms supporting inspection, monitoring, and predictive risk management. AI-powered hazard detection improves early incident identification by nearly 30%, while cloud-connected fleet management enhances maintenance efficiency by approximately 25%. South Korea continues accelerating smart industrial infrastructure projects that integrate robotics with digital command centers and industrial IoT platforms. Companies are increasing investment in autonomous navigation software, digital twin integration, and multi-robot coordination instead of focusing solely on suppression equipment. This broader ecosystem approach unlocks recurring software services, lifecycle maintenance contracts, and higher-value enterprise safety solutions across critical industries.

Long-term competitiveness depends on reliably scaling autonomous performance across diverse industrial environments with varying layouts, communication networks, and emergency conditions. More than 40% of industrial operators identify cybersecurity and secure wireless communication as major deployment priorities, while autonomous navigation performance can decline by nearly 18% in dense smoke or GPS-restricted facilities. Japan and Germany continue raising functional safety expectations for autonomous industrial systems, increasing validation requirements before commercial deployment. Companies must strengthen AI model reliability, cyber-resilient control systems, workforce training, and infrastructure partnerships to deliver consistent operational performance and maintain confidence in mission-critical emergency response applications.

Advanced AI Navigation Integration AI-enabled navigation and thermal vision systems are becoming standard across industrial fire response platforms, with autonomous mission accuracy improving by nearly 35% and emergency route optimization reducing response time by around 28%. Stricter industrial safety requirements in China are accelerating deployment, while manufacturers are expanding software partnerships and integrating edge computing to improve autonomous decision-making under hazardous operating conditions.

Localized Manufacturing Expansion Companies are restructuring production networks as supply-chain resilience becomes a competitive priority. Local sourcing of critical electronic components has increased by approximately 22%, while procurement lead times have fallen by nearly 18% through regional manufacturing expansion. This shift lowers deployment delays and strengthens service capability, prompting robotics suppliers to establish engineering hubs closer to major industrial customers.

Multi-Robot Fleet Coordination Enterprise users are replacing single-platform deployments with coordinated robotic fleets capable of suppression, surveillance, and inspection within one operational framework. Fleet utilization has improved by roughly 30%, while maintenance scheduling efficiency has increased by nearly 24% through centralized control platforms. Companies are scaling integrated software ecosystems and strategic automation partnerships to support synchronized emergency response across complex industrial facilities.

Predictive Fire Risk Intelligence Fire fighting robots are increasingly operating beyond emergency response by supporting continuous infrastructure monitoring through AI-driven predictive analytics. Early hazard detection accuracy has improved by about 32%, while unplanned equipment downtime has declined by nearly 20%. Growing digital transformation across critical infrastructure is encouraging vendors to combine robotic platforms with industrial IoT ecosystems, creating recurring service models instead of one-time equipment deployments.

Tracked Robots remain the leading segment because they deliver superior mobility across debris, uneven terrain, and hazardous industrial environments where conventional mobility systems struggle. Approximately 41% of heavy industrial deployments utilize tracked platforms due to higher stability, stronger payload capacity, and reliable operation during high-temperature incidents. Remote-Controlled Robots continue serving facilities requiring direct operator supervision, while Wheeled Robots maintain strong adoption in warehouses, airports, and commercial infrastructure where speed and maneuverability outweigh extreme terrain capability.

Autonomous Robots represent the fastest-growing segment as AI navigation, sensor fusion, and real-time environmental mapping become operational priorities. Autonomous deployments have increased by nearly 29% across newly commissioned industrial facilities, while Aerial Robots are expanding rapidly for fire surveillance, rooftop assessment, and situational awareness before ground intervention. Manufacturers are prioritizing hybrid product portfolios, combining tracked mobility with autonomous software and advanced thermal sensing to strengthen mission flexibility. Investment is increasingly shifting toward intelligent robotic platforms capable of performing inspection, monitoring, and emergency suppression within integrated safety ecosystems.

Industrial Firefighting remains the largest application because petrochemical plants, manufacturing facilities, power stations, and logistics hubs require continuous protection against high-risk incidents where human intervention is limited. Nearly 46% of enterprise deployments are concentrated in industrial facilities, supported by stricter operational safety standards and automation strategies. Urban Firefighting continues expanding through municipal modernization programs, while Hazardous Material Response maintains strategic importance for chemical processing sites handling toxic or explosive materials.

Forest Firefighting is emerging as the fastest-growing application as climate-driven wildfire frequency increases and governments invest in autonomous monitoring and remote suppression capabilities. Deployment of robotic wildfire monitoring platforms has increased by approximately 27%, while AI-assisted fire mapping improves incident assessment accuracy by nearly 31%. Rescue Operations are also evolving through integration with thermal imaging and autonomous navigation for collapsed structures. Companies are strengthening application-specific product development, expanding partnerships with emergency agencies, and integrating robotic systems into broader command-and-control platforms to improve operational coordination.

Industrial Facilities represent the dominant end-user segment because continuous operations, hazardous materials, and strict safety compliance require permanent robotic fire response capability. Around 44% of enterprise procurement originates from manufacturing, chemical processing, mining, and energy facilities seeking faster emergency intervention with reduced workforce exposure. Fire Departments remain major adopters for urban emergency response, while Airports continue integrating robotic systems into critical infrastructure protection strategies for rapid incident containment.

Oil & Gas is the fastest-growing end-user segment as offshore platforms, refineries, and LNG facilities accelerate investment in autonomous emergency technologies capable of operating under extreme conditions. Robotic deployment across high-risk energy facilities has increased by nearly 26%, while remote firefighting capability reduces direct personnel exposure by approximately 40%. Defense organizations continue adopting rugged autonomous platforms for military infrastructure protection. Manufacturers are responding through sector-specific product customization, long-term service agreements, and ecosystem partnerships that integrate robotics with industrial monitoring, predictive maintenance, and digital emergency management platforms.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 13.2% CAGR between 2026 and 2033.

Advanced Industrial Automation Driving Emergency Response

North America represents one of the most technologically advanced Fire Fighting Robot Market ecosystems, supported by widespread deployment across petrochemical facilities, airports, energy infrastructure, and defense installations. The region contributes approximately 28% of global deployment activity, with enterprise demand centered on AI-enabled emergency response and integrated industrial safety platforms. Increasing replacement of conventional firefighting equipment with autonomous robotic systems has accelerated procurement across high-risk industries. During 2025, several industrial operators expanded robotic safety infrastructure, improving hazardous-area response efficiency by nearly 30%. Companies are strengthening collaborations with industrial automation providers while integrating thermal imaging, LiDAR navigation, and digital command systems into enterprise emergency management frameworks, reinforcing long-term operational resilience and asset protection.

United States Market Outlook: The United States remains the regional technology leader through extensive investment in industrial automation, advanced robotics, and critical infrastructure modernization. Large petrochemical complexes along the Gulf Coast, defense facilities, and logistics hubs continue expanding robotic emergency response capabilities. More than 48% of newly commissioned hazardous industrial facilities now evaluate autonomous firefighting technologies during safety planning, encouraging manufacturers to expand software integration, localized engineering services, and strategic partnerships across industrial safety ecosystems.

Industrial Safety Modernization Supporting Autonomous Deployment

Europe continues strengthening its Fire Fighting Robot Market through industrial modernization, rigorous workplace safety regulations, and digital transformation across manufacturing and critical infrastructure. The region accounts for nearly 24% of global deployment activity, with demand concentrated in automotive production, chemical processing, transportation, and public infrastructure. Smart factory expansion and stricter operational compliance are encouraging investment in autonomous emergency response technologies. During 2025, robotic integration across advanced manufacturing facilities improved emergency intervention readiness by approximately 26%. Companies are accelerating platform standardization, expanding automation partnerships, and incorporating predictive maintenance capabilities to improve lifecycle efficiency while supporting sustainable industrial safety management.

Germany Market Outlook: Germany leads the regional market through its advanced manufacturing base, industrial automation expertise, and strong engineering ecosystem. Chemical production facilities, automotive plants, and logistics centers increasingly deploy intelligent firefighting robots as part of integrated Industry 4.0 strategies. Approximately 36% of large industrial enterprises have expanded autonomous safety technologies within facility modernization programs, encouraging robotics suppliers to strengthen local R&D, customized engineering, and industrial software integration.

Manufacturing Scale Accelerates Deployment Leadership

Asia-Pacific dominates the Fire Fighting Robot Market through large-scale manufacturing capacity, expanding industrial infrastructure, and continuous investment in intelligent automation. The region accounts for roughly 42% of global market activity, supported by widespread deployment across petrochemical complexes, electronics manufacturing, ports, and logistics facilities. China, Japan, and South Korea continue increasing production of autonomous robotics and industrial sensors to strengthen domestic supply capability. During 2025, production capacity for industrial robotic safety equipment expanded by nearly 20%, reducing delivery timelines and supporting faster enterprise deployment. Companies are prioritizing localized manufacturing, AI integration, and strategic technology partnerships to improve operational efficiency while enhancing export competitiveness.

China Market Outlook: China remains the largest country market through extensive manufacturing capability, government-backed industrial modernization, and rapid deployment across hazardous industries. Smart industrial parks, energy facilities, and large logistics hubs continue integrating autonomous firefighting systems into digital safety platforms. More than 50% of newly developed high-risk industrial projects now incorporate robotic emergency response planning, encouraging manufacturers to expand production capacity, AI software capabilities, and domestic component sourcing.

Industrial Expansion Reshaping Safety Investments

South America is steadily expanding adoption of fire fighting robots as industrial operators strengthen safety infrastructure across mining, energy, manufacturing, and logistics sectors. The region contributes approximately 4% of global market activity, with demand supported by modernization of hazardous industrial facilities rather than broad municipal deployment. During 2025, automated emergency response investments across major industrial sites improved incident preparedness by nearly 18%. Infrastructure limitations and uneven technology availability continue influencing deployment speed, prompting companies to prioritize phased implementation strategies. Robotics suppliers are responding through regional distribution partnerships, localized technical support, and modular product offerings that improve affordability while reducing deployment complexity.

Brazil Market Outlook: Brazil leads regional adoption through its extensive mining operations, offshore energy assets, and expanding industrial manufacturing base. Large enterprises increasingly integrate robotic firefighting technologies into operational risk management programs to improve worker safety and reduce emergency response time. Nearly 31% of new industrial safety modernization projects within high-risk sectors now evaluate autonomous robotic systems, encouraging greater collaboration between automation providers and industrial engineering firms.

Critical Infrastructure Investments Accelerate Automation

The Middle East & Africa is emerging as the fastest-expanding Fire Fighting Robot Market due to substantial investment in energy infrastructure, industrial diversification, airports, and smart city developments. The region accounts for approximately 2% of global deployment but demonstrates the strongest momentum in new project implementation. Large-scale infrastructure developments increasingly specify autonomous emergency response capabilities during project planning. During 2025, robotic deployment across selected industrial facilities improved hazardous incident response efficiency by nearly 27%. Companies are expanding regional partnerships, establishing technical service networks, and adapting robotic platforms for high-temperature operating environments to support long-term infrastructure resilience.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through industrial diversification initiatives, energy infrastructure expansion, and large-scale smart city development. Petrochemical complexes, oil processing facilities, and transportation infrastructure increasingly adopt autonomous firefighting technologies to strengthen operational continuity. Around 34% of newly planned industrial megaprojects include advanced robotic safety systems during engineering design, encouraging suppliers to localize service capabilities, strengthen technology partnerships, and expand specialized industrial training programs.

The Fire Fighting Robot Market is led by global technology providers including Shark Robotics, LUF GmbH, Howe & Howe Technologies, Hytera, and SuperDroid Robots, competing against regional engineering specialists and industrial automation integrators. Global leaders emphasize autonomous navigation and integrated safety ecosystems, while regional manufacturers compete through cost-efficient customization and localized service. The top five players collectively control approximately 47% of the market. Competition centers on AI capability, mobility performance, deployment speed, and lifecycle support, with autonomous platforms delivering nearly 35% higher mission efficiency and modular architectures reducing deployment time by about 22%. Companies are expanding production, forming software partnerships, integrating thermal imaging and LiDAR, and strengthening component sourcing through vertical integration. The competitive landscape is shifting toward intelligent software-defined robotics rather than hardware differentiation alone, increasing pressure on manufacturers lacking AI expertise. High certification requirements, mission-critical reliability, and advanced sensor integration create significant entry barriers. Winning requires scalable autonomous technology, localized support, rapid customization, resilient supply chains, and continuous software innovation.

Shark Robotics

LUF GmbH

Howe & Howe Technologies

SuperDroid Robots

Hytera

DOK-ING

Milrem Robotics

Tmsuk Co., Ltd.

QinetiQ

Dragon Runner Inc.

Lockheed Martin

Hitachi, Ltd.

Robo-Team Ltd.

Kawasaki Heavy Industries, Ltd.

Autonomous navigation, AI-powered perception, thermal imaging, and LiDAR are becoming the technological foundation of the Fire Fighting Robot Market. More than 45% of newly deployed enterprise systems integrate multi-sensor fusion for obstacle recognition and hazard mapping, improving navigation accuracy by approximately 34%. Compared with conventional remote-controlled platforms, AI-enabled robots complete mission planning nearly 40% faster while reducing operator intervention by about 55%. Industrial operators benefit through faster incident assessment, lower personnel exposure, and improved emergency coordination across hazardous environments.

Emerging technologies increasingly combine edge computing, industrial IoT connectivity, digital twins, and 5G communications to create intelligent emergency response ecosystems. Around 38% of large industrial facilities now prioritize connected robotic platforms capable of transmitting real-time operational data to centralized command centers. Predictive analytics improves equipment availability by roughly 25%, while cloud-based fleet management reduces maintenance planning effort by nearly 20%. Technology leaders and industrial automation providers gain a competitive advantage through integrated software platforms instead of standalone robotic hardware.

Between 2026 and 2028, multi-robot collaboration, autonomous swarm coordination, and AI-driven decision support will redefine industrial emergency response. Early enterprise deployments indicate coordinated robotic fleets improve operational coverage by approximately 30% while reducing response delays by nearly 24%. Companies investing in intelligent software architecture, cybersecurity, advanced battery systems, and interoperable command platforms will establish stronger differentiation as customers increasingly prioritize scalable, connected, and continuously upgradeable robotic safety ecosystems over traditional equipment procurement.

September 2024 Shark Robotics and ONERA announced a joint France 2030 project to develop an autonomous firefighting robot integrating advanced AI capabilities. The initiative targets next-generation autonomous intervention with one flagship R&D program, strengthening France's industrial robotics leadership.

September 2024 Shark Robotics secured renewal of its procurement agreement with France's UGAP, expanding public-sector access to its unmanned ground vehicles. The framework simplifies purchasing for more than 150,000 eligible public buyers, accelerating nationwide deployment opportunities.

November 2025 Shark Robotics confirmed deployment of 40 Colossus firefighting robots in Ukraine to strengthen protection of critical infrastructure against drone-related fires. The large-scale rollout significantly expanded operational emergency-response capacity while reinforcing international market presence.

April 2025 The FDNY conducted a three-day regional robotics training program showcasing robotic dogs, drones, and heavy-response robots. The department's Robotics Unit includes 12 certified robot and drone operators, demonstrating growing institutional adoption and knowledge transfer.

The report provides comprehensive analysis across Wheeled Robots, Tracked Robots, Aerial Robots, Autonomous Robots, and Remote-Controlled Robots while evaluating demand across Industrial Firefighting, Urban Firefighting, Forest Firefighting, Hazardous Material Response, and Rescue Operations. It further assesses procurement patterns among Fire Departments, Industrial Facilities, Oil & Gas, Defense, and Airports, supported by deployment trends, technology integration, and competitive benchmarking across five major geographic regions. More than 40% of the analysis emphasizes industrial automation and autonomous emergency response adoption.

The study evaluates manufacturing capabilities, AI-enabled robotics, thermal imaging, LiDAR navigation, edge computing, industrial IoT integration, and evolving operational strategies between 2026 and 2033. It also examines competitive positioning, product innovation, localization strategies, partnership activity, and supply-chain resilience to support investment decisions, expansion planning, portfolio optimization, and market entry strategies. The report highlights emerging deployment models, enterprise adoption priorities, and niche opportunities within high-risk industrial infrastructure and mission-critical emergency response environments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1885.11 Million |

Market Revenue in 2033 | USD 4344.31 Million |

CAGR (2026 - 2033) | 11% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Shark Robotics, LUF GmbH, Howe & Howe Technologies, SuperDroid Robots, Hytera, DOK-ING, Milrem Robotics, Tmsuk Co., Ltd., QinetiQ, Dragon Runner Inc., Lockheed Martin, Hitachi, Ltd., Robo-Team Ltd., Kawasaki Heavy Industries, Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |