Reports

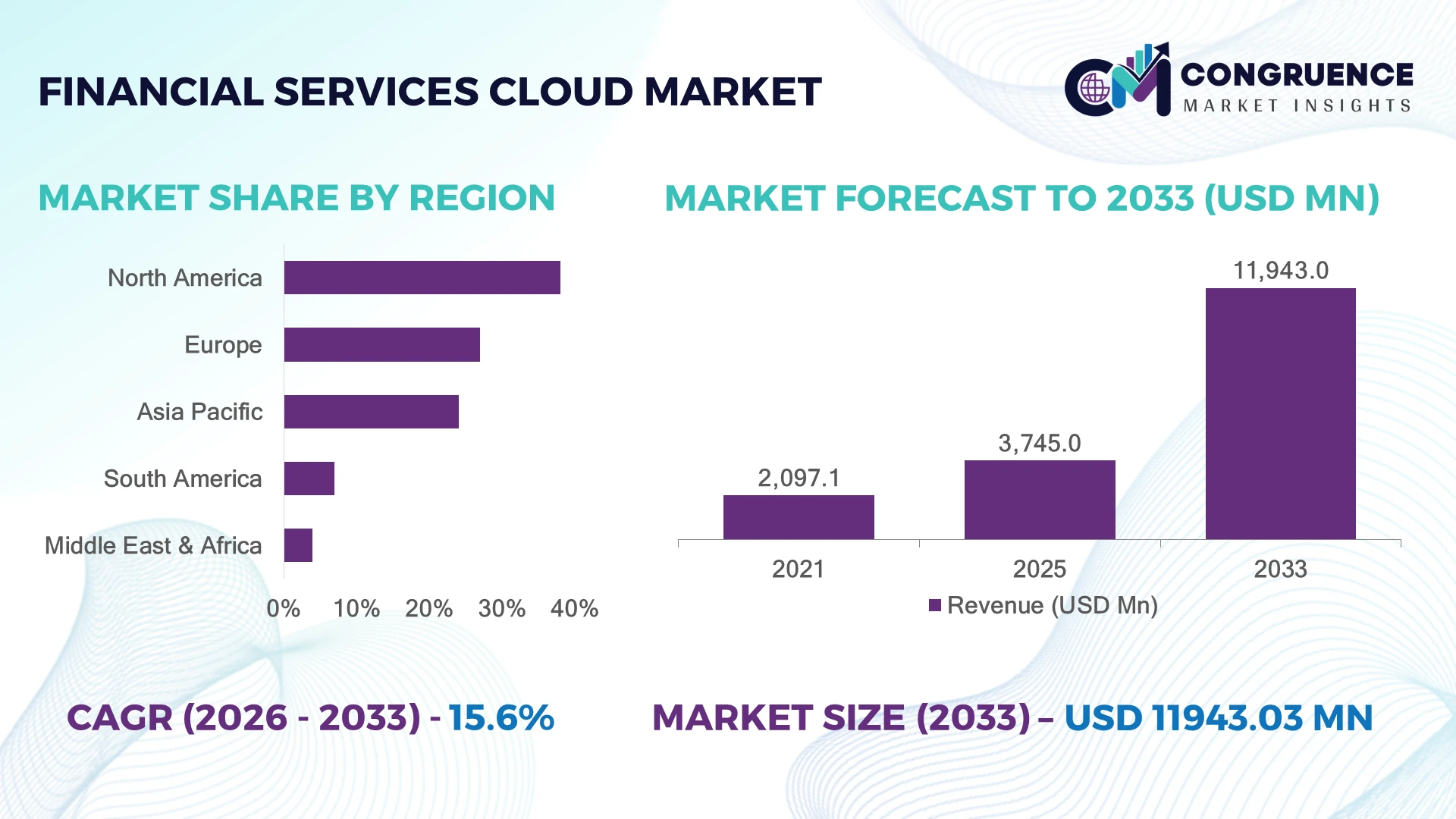

The Global Financial Services Cloud Market was valued at USD 3,745.0 Million in 2025 and is anticipated to reach a value of USD 11,943.0 Million by 2033 expanding at a CAGR of 15.6% between 2026 and 2033. Growth is driven by accelerated cloud-native banking transformation, AI-enabled risk analytics, cybersecurity modernization, and financial institutions replacing legacy infrastructure with scalable digital platforms.

The United States dominates the market with approximately 38% share, supported by major cloud investments from banks, insurers, and fintech firms, while over 70% of large financial institutions operate hybrid cloud environments. China follows with around 18% share, backed by rapid fintech expansion and regulatory technology adoption. Compared with Europe’s stricter compliance-led cloud migration approach, North America maintains faster enterprise deployment cycles.

Strategic decisions increasingly focus on secure, AI-ready cloud ecosystems that improve resilience and competitive differentiation.

Market Size & Growth: USD 3,745.0 Million (2025) to USD 11,943.0 Million (2033), 15.6% CAGR; driven by AI adoption and banking infrastructure modernization.

Top Growth Drivers: AI analytics (32%), cybersecurity upgrades (28%), digital banking transformation (25%) are accelerating cloud migration.

Short-Term Forecast: By 2028, financial institutions target 35% lower infrastructure costs and 40% faster application deployment through cloud platforms.

Emerging Technologies: AI automation, cloud-native architectures, confidential computing, and advanced cybersecurity frameworks reshape financial operations.

Regional Leaders: North America reaches USD 4.5 Billion with hybrid cloud adoption; Europe reaches USD 3.1 Billion with compliance-focused deployments; Asia-Pacific reaches USD 3.0 Billion with fintech expansion.

Consumer/End-User Trends: Over 65% of banks prioritize cloud-based customer platforms to enhance digital experiences and personalization.

Pilot/Case Example: 2024 AI-driven cloud banking initiatives reduced transaction processing time by 45% through automated workflows.

Competitive Landscape: Amazon Web Services leads with approximately 30% financial cloud presence, alongside Microsoft Azure, Google Cloud, IBM Cloud, and Oracle Cloud Infrastructure.

Regulatory & ESG Impact: Cloud compliance frameworks improve reporting efficiency by 30% while supporting sustainable data-center operations.

Investment & Funding: More than USD 20 Billion invested globally in cloud infrastructure partnerships, fintech platforms, and AI-powered financial services expansion.

Innovation & Future Outlook: Next-generation cloud banking focuses on autonomous operations, real-time risk intelligence, and strategic ecosystem partnerships.

Financial Services Cloud solutions are gaining momentum through AI-driven fraud detection, automated compliance platforms, and real-time customer engagement tools. More than 60% of financial institutions are prioritizing cloud-based modernization programs, while innovations in zero-trust security and distributed computing address regulatory challenges. Global banks are also adapting infrastructure strategies amid evolving data sovereignty rules and cross-border digital finance expansion, creating a strong pathway toward advanced cloud ecosystems.

The Financial Services Cloud Market is becoming strategically important as banks, insurers, and investment firms prioritize operational agility, cybersecurity resilience, and faster digital innovation. Regulatory modernization, rising cybersecurity requirements, and the shift toward real-time financial services are accelerating enterprise cloud adoption. Institutions are restructuring technology investments to replace fragmented legacy systems with integrated cloud platforms.

Modern cloud environments deliver measurable advantages compared with traditional infrastructure, reducing application deployment cycles by nearly 40% and improving operational scalability through automation. North America leads in enterprise cloud maturity, while Asia-Pacific demonstrates faster fintech-driven adoption through digital banking expansion and mobile-first financial ecosystems. European markets emphasize compliance, data governance, and secure cloud frameworks due to evolving financial regulations.

Over the next 2–3 years, financial institutions are increasing investments in AI-powered cloud analytics, automated compliance, and embedded finance capabilities. Major banks are partnering with cloud providers to deploy secure digital platforms, enhance customer experiences, and optimize operational workflows. Strategic deployment of cloud technologies will determine competitive positioning by enabling faster innovation, stronger resilience, and long-term financial ecosystem leadership.

Financial institutions are accelerating cloud adoption as legacy infrastructure modernization becomes a competitive priority, with over 70% of large banks operating hybrid cloud models and nearly 60% increasing investments in AI-enabled financial platforms. In the United States, stricter cybersecurity requirements and real-time payment expansion are pushing banks toward scalable cloud architectures. The shift from data-center ownership to flexible cloud ecosystems is reducing deployment cycles and improving operational agility. Companies are responding through strategic partnerships, multi-cloud investments, and AI integration initiatives to strengthen digital banking capabilities and deliver faster, more secure financial services.

Cloud migration faces structural barriers from data sovereignty requirements, integration complexity, and rising cybersecurity expenses. Approximately 45% of financial institutions identify regulatory compliance as a major cloud deployment challenge, while nearly 35% report difficulties integrating cloud platforms with existing core banking systems. In countries such as Germany and India, evolving data localization policies increase operational complexity for global financial providers. These constraints affect deployment speed, cost efficiency, and scalability. Companies are reducing exposure through localized cloud infrastructure, hybrid deployment strategies, stronger vendor contracts, and investments in compliance automation tools to manage operational risks.

The expansion of AI-powered financial services creates significant opportunities for advanced cloud platforms, with more than 65% of banks prioritizing AI analytics and automation capabilities. Financial institutions are deploying cloud-based fraud detection, personalized banking engines, and automated regulatory reporting systems to improve efficiency. In Singapore and the United Arab Emirates, digital finance initiatives are accelerating adoption of intelligent cloud ecosystems. Companies are increasing R&D spending, forming technology partnerships, and developing industry-specific cloud solutions. A key strategic opportunity lies in combining cloud infrastructure with generative AI models to enable predictive decision-making and create new financial service business models.

Financial cloud providers face long-term execution challenges from cybersecurity threats, workforce shortages, and complex multi-platform integration requirements. Around 40% of financial organizations cite security management as a critical barrier, while over 30% struggle with cloud skill shortages during transformation programs. The increasing adoption of open banking frameworks and interconnected financial ecosystems adds additional pressure on operational resilience. Companies must address these issues through advanced encryption, zero-trust security models, employee training, and ecosystem partnerships. Strategic success depends on building reliable cloud architectures that maintain compliance, performance consistency, and customer trust across rapidly evolving financial environments.

AI-Powered Cloud Operations Financial institutions are rapidly embedding AI into cloud workflows, with over 60% of large banks prioritizing automated analytics, fraud monitoring, and intelligent customer platforms. Generative AI adoption is reshaping operational processes by reducing manual review workloads by nearly 35% and improving decision speed. Banks in the United States and Singapore are expanding AI-cloud partnerships to modernize risk management and personalized financial services.

Multi-Cloud Strategy Expansion Enterprises are shifting toward multi-cloud architectures as approximately 55% of financial organizations operate across multiple cloud environments to improve resilience and compliance. Regulatory pressure around data sovereignty, including evolving rules in Europe and Asia, is accelerating localized cloud deployment. Companies are restructuring technology stacks through strategic partnerships with multiple cloud providers to reduce dependency risks and improve service continuity.

Cloud Security Modernization Zero-trust security, confidential computing, and automated compliance monitoring are becoming operational priorities, with nearly 50% of financial institutions increasing cybersecurity cloud investments. Rising digital payment volumes and cross-border transactions are forcing enterprises to strengthen identity management and threat detection. Cloud providers are responding through advanced encryption solutions and integrated security platforms.

Embedded Finance Integration Financial firms are expanding cloud-based embedded finance capabilities, with over 40% of enterprises exploring API-driven banking services and automated financial ecosystems. The growth of digital marketplaces and real-time payment networks is changing how institutions distribute services. Companies are investing in cloud-native platforms and fintech collaborations to create faster, scalable financial products.

Hybrid cloud is the leading type in the Financial Services Cloud Market, accounting for approximately 55% of enterprise deployments due to its balance between regulatory compliance, scalability, and control over sensitive financial data. Large banks in the United States, United Kingdom, and Japan continue prioritizing hybrid models to connect legacy banking systems with modern cloud-native applications. Public cloud adoption remains significant, representing nearly 35% of deployments, especially among fintech firms seeking rapid scalability and lower infrastructure complexity. Private cloud is evolving as a specialized segment for institutions requiring enhanced security, data governance, and customized compliance environments. Public cloud platforms and hybrid architectures are attracting stronger investment as financial organizations increase automation and AI workloads. Hybrid cloud is also the fastest-growing deployment model, supported by rising demand for flexible infrastructure and multi-cloud resilience. Companies are responding by expanding cloud partnerships, developing industry-specific solutions, and improving interoperability frameworks to support secure financial transformation.

Digital banking platforms represent the leading application segment, driven by increasing demand for mobile banking, real-time payments, and personalized financial experiences. More than 65% of financial institutions are prioritizing cloud-based customer engagement platforms to improve service delivery and operational efficiency. Core banking modernization, payment processing, and risk management applications are also expanding as institutions replace fragmented systems with integrated cloud environments. AI-driven analytics and fraud detection represent the fastest-growing application area, with adoption increasing as banks focus on automated decision-making and cybersecurity enhancement. Approximately 45% of financial organizations are implementing advanced cloud analytics to improve fraud monitoring and customer insights. Insurance technology, wealth management platforms, and regulatory compliance applications continue gaining importance as financial ecosystems become more digital. Companies are scaling cloud-based solutions through automation, API integration, and partnerships with technology providers to improve speed, accuracy, and customer experience.

Banks and financial institutions represent the dominant end-user group, accounting for nearly 60% of Financial Services Cloud deployments due to their extensive infrastructure requirements, high transaction volumes, and regulatory obligations. Major banking organizations in the United States, China, and India are accelerating cloud adoption to modernize payment systems, improve cybersecurity, and support digital-first services. Insurance companies and investment firms are also expanding cloud usage to enhance analytics, customer engagement, and automated operations. Fintech companies are emerging as the fastest-growing end-user segment, supported by flexible cloud architectures, API-based platforms, and rapid product innovation. Nearly 50% of fintech firms rely heavily on cloud-native infrastructure to scale services efficiently and launch new financial products faster. Traditional banks are responding by increasing partnerships with fintech ecosystems and adopting specialized cloud platforms. Insurance providers, wealth managers, and credit institutions are focusing on customized solutions that improve automation, compliance management, and customer personalization.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of18.2% between 2026 and 2033.

North America held the dominant position with approximately 38% market share in 2025, supported by advanced banking infrastructure, high enterprise cloud penetration, and strong fintech ecosystems. The United States contributes the majority of regional demand as large financial institutions accelerate hybrid cloud deployments, cybersecurity modernization, and AI-powered analytics adoption. More than 70% of major North American banks operate hybrid or multi-cloud environments to improve flexibility and regulatory compliance. Cloud providers and financial enterprises are expanding partnerships focused on automation, risk intelligence, and secure digital platforms. Increasing investments in data centers and AI infrastructure are strengthening the region’s position as the global hub for financial cloud innovation.

United States Market Outlook: The United States represents the largest country market within North America, supported by major banking groups, fintech companies, and technology providers. Over 75% of large financial institutions in the country have adopted cloud-based solutions for customer platforms, analytics, and operational modernization. Strong cybersecurity frameworks and enterprise technology spending continue driving cloud transformation across banking and insurance sectors.

Europe accounted for approximately 27% market share in 2025, driven by strong regulatory frameworks, financial technology innovation, and modernization of traditional banking infrastructure. Countries including Germany, the United Kingdom, and France are increasing cloud adoption to support digital payments, compliance automation, and customer-centric financial services. The implementation of stricter data governance requirements is encouraging financial institutions to invest in secure cloud architectures and localized infrastructure. Nearly 60% of European financial enterprises prioritize cloud-based compliance and risk management solutions. Companies are strengthening partnerships with cloud providers to improve operational efficiency while maintaining regulatory alignment across complex financial markets.

United Kingdom Market Outlook: The United Kingdom remains Europe’s leading financial cloud market due to its global banking ecosystem, fintech concentration, and advanced digital finance infrastructure. More than 65% of financial organizations in the country use cloud platforms for operational workloads, with banks focusing on AI-driven analytics, cybersecurity, and automated compliance solutions. London’s financial technology ecosystem continues attracting cloud investment and innovation partnerships.

Asia-Pacific represented approximately 24% market share in 2025 and is positioned as the fastest-transforming market due to rapid fintech expansion, digital payment growth, and large-scale banking modernization. China, India, Japan, and Singapore are driving cloud adoption through mobile banking ecosystems, financial inclusion programs, and AI-based financial services. Over 65% of fintech companies in major Asia-Pacific markets rely on cloud-native infrastructure to scale operations efficiently. Government-backed digital finance initiatives and expanding data-center investments are accelerating enterprise deployment. Companies are increasing regional partnerships, developing localized cloud solutions, and expanding infrastructure capacity to support rising transaction volumes.

China Market Outlook: China is the largest financial cloud market in Asia-Pacific, supported by extensive digital payment networks, large banking institutions, and advanced technology infrastructure. More than 80% of leading financial enterprises in China utilize cloud-based systems for analytics, risk management, and digital banking services. Strong investment in AI, data centers, and financial technology platforms continues strengthening the country’s cloud ecosystem.

South America accounted for approximately 7% market share in 2025, with growth supported by expanding digital banking adoption, fintech innovation, and financial inclusion initiatives. Brazil and Argentina are leading regional adoption as banks transition from traditional systems toward scalable cloud platforms. More than 45% of financial institutions in major South American economies are increasing cloud investments to improve customer services and operational efficiency. Infrastructure development remains uneven, but partnerships between banks and technology providers are improving cloud accessibility. Companies are focusing on localized solutions, cybersecurity improvements, and flexible deployment models to overcome connectivity and compliance challenges.

Brazil Market Outlook: Brazil dominates the South American financial cloud landscape due to its large banking sector, advanced fintech ecosystem, and strong digital payment adoption. Over 60% of major Brazilian financial institutions have adopted cloud-based applications across payments, customer management, and analytics. Regulatory support for digital finance and open banking frameworks continues encouraging enterprise cloud transformation.

The Middle East & Africa region accounted for approximately 4% market share in 2025, supported by financial digitization programs, cloud infrastructure investments, and modernization initiatives across banking sectors. Countries such as the United Arab Emirates and Saudi Arabia are leading adoption through smart finance strategies, data-center expansion, and fintech ecosystem development. Cloud adoption among financial institutions has increased as organizations prioritize automation, cybersecurity, and digital customer engagement. More than 40% of banks in leading Middle Eastern markets are expanding cloud-based operations to improve scalability and service delivery. Companies are investing in regional data centers, strategic technology partnerships, and compliance-focused cloud platforms.

United Arab Emirates Market Outlook: The United Arab Emirates represents the leading financial cloud market in the Middle East & Africa due to strong digital banking initiatives, advanced infrastructure, and government-supported technology transformation. More than 50% of financial institutions in the UAE have accelerated cloud adoption programs focused on AI, cybersecurity, and digital financial services. The country’s fintech ecosystem and data-center expansion continue attracting enterprise cloud investments.

The Financial Services Cloud Market features competition between global cloud leaders such as Amazon Web Services, Microsoft Azure, Google Cloud, and Oracle Cloud Infrastructure against specialized financial technology providers and regional cloud operators. The top five players collectively account for approximately 65% market influence. Competition centers on AI capability, security, customization, deployment speed, and compliance, with 60%+ of banks prioritizing hybrid cloud strategies and nearly 50% increasing cybersecurity investments. Leaders compete through industry partnerships, AI platforms, regional data-center expansion, and vertical solutions. The market is shifting toward AI-integrated cloud ecosystems, while high compliance requirements and infrastructure costs create entry barriers. Winning requires secure platforms, financial expertise, rapid innovation, and ecosystem partnerships.

Microsoft Azure

Google Cloud

Oracle Cloud Infrastructure

IBM Cloud

Salesforce

SAP

Alibaba Cloud

Tencent Cloud

VMware

Snowflake

ServiceNow

Financial cloud technology is shifting from traditional infrastructure hosting toward AI-enabled, cloud-native financial ecosystems. Generative AI, machine learning, and automated compliance platforms are being integrated into banking workflows, with adoption exceeding 60% among large financial institutions. These technologies improve fraud detection accuracy, reduce manual processing workloads by nearly 35%, and accelerate customer service operations. Companies are prioritizing AI partnerships and specialized financial cloud platforms to gain competitive advantages.

Hybrid cloud and confidential computing are replacing conventional infrastructure models by improving security, scalability, and regulatory control. Compared with legacy banking systems, modern cloud-native architectures reduce application deployment cycles by approximately 40% and improve operational flexibility. Multi-cloud strategies are also expanding, with more than 50% of enterprises adopting multiple providers to strengthen resilience and avoid dependency risks.

Between 2026 and 2028, autonomous banking platforms, real-time analytics, and AI-driven risk management will become major differentiators. Global cloud leaders benefit from infrastructure scale, while financial institutions gain faster innovation, improved compliance, and stronger customer personalization through advanced technology adoption.

February 2025 Amazon Web Services expanded its collaboration with Commonwealth Bank of Australia to accelerate cloud and AI adoption. The partnership enabled AI solutions to move from concept to production in six weeks, improving digital banking delivery speed. Source: www.press.aboutamazon.com

September 2025 Nasdaq and AWS expanded cloud deployment options for Nasdaq Calypso, enabling managed capital markets infrastructure. The initiative improved scalability and reduced platform management complexity for financial institutions adopting cloud-based trading operations. Source: www.press.aboutamazon.com

September 2024 Oracle Corporation announced Oracle Financial Crime and Compliance Management Monitor Cloud Service, helping banks improve risk visibility and compliance workflows. The solution introduced centralized monitoring capabilities for financial crime management and regulatory reporting processes. Source: www.oracle.com

September 2024 Oracle Corporation supported Muthoot FinCorp migration to Oracle Cloud Infrastructure, improving system performance and operational efficiency by 50%. The deployment strengthened scalability, security, and digital lending operations across India.

The Financial Services Cloud Market Report covers comprehensive analysis across deployment types, applications, end-user groups, regional markets, technology trends, competitive positioning, and strategic opportunities. The study evaluates hybrid cloud, public cloud, and private cloud models along with banking, insurance, payments, investment management, and fintech applications.

The report examines adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting enterprise transformation strategies and emerging digital finance ecosystems. With more than 60% of financial institutions prioritizing cloud modernization initiatives, the report provides insights into AI integration, cybersecurity advancement, automation, partnerships, and infrastructure evolution. The analysis supports investment planning, market expansion decisions, competitive benchmarking, and long-term positioning strategies between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,745.0 Million |

| Market Revenue (2033) | USD 11,943.0 Million |

| CAGR (2026–2033) | 15.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Amazon Web Services; Microsoft Azure; Google Cloud; Oracle Cloud Infrastructure; IBM Cloud; Salesforce; SAP; Alibaba Cloud; Tencent Cloud; VMware; Snowflake; ServiceNow |

| Customization & Pricing | Available on Request (10% Customization Free) |