Reports

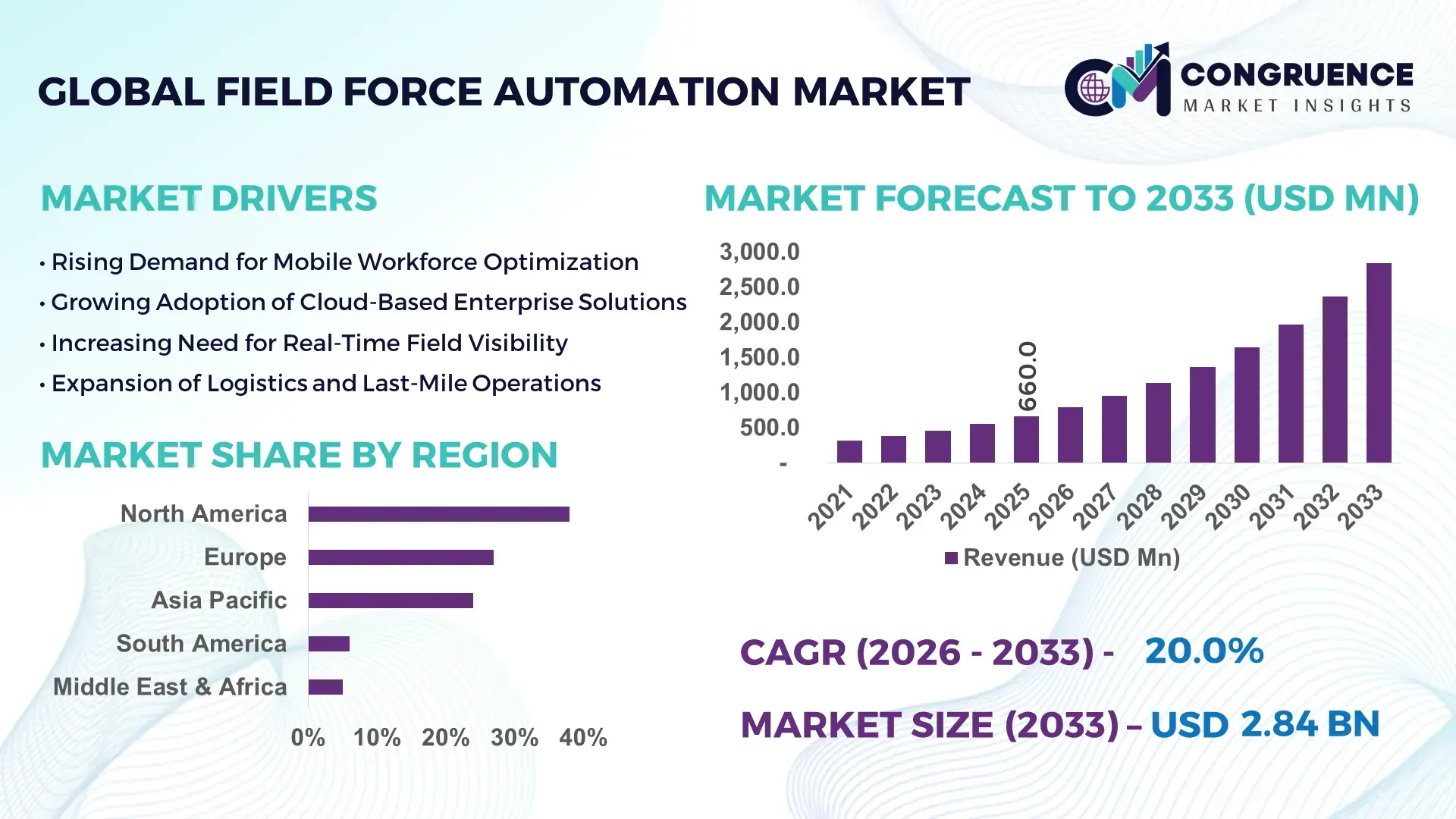

The Global Field Force Automation Market was valued at USD 660.0 Million in 2025 and is anticipated to reach a value of USD 2,837.9 Million by 2033 expanding at a CAGR of 20% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rapid enterprise digitization and the integration of AI-enabled mobility platforms to enhance field productivity, compliance tracking, and real-time service optimization.

In the United States, which dominates the global Field Force Automation Market, enterprise mobility penetration exceeds 85% across large service-based organizations, and more than 72% of utilities and telecom companies have deployed mobile workforce management platforms integrated with IoT-enabled asset monitoring. The country hosts over 40 major field service software providers and records annual enterprise SaaS investments exceeding USD 150 billion, a portion of which is allocated to automation and CRM-integrated field solutions. Key applications include telecommunications infrastructure management, healthcare home services, HVAC maintenance, and energy utilities, where predictive maintenance systems have reduced equipment downtime by up to 30%. AI-driven route optimization tools are adopted by nearly 60% of logistics-intensive service enterprises, while cloud-native deployments account for over 65% of new implementations.

Market Size & Growth: Valued at USD 660.0 Million in 2025, projected to reach USD 2,837.9 Million by 2033, expanding at 20% CAGR; growth supported by enterprise-wide mobility and AI-driven workforce optimization.

Top Growth Drivers: 68% enterprise mobile workforce expansion, 35% improvement in field productivity via automation, 42% increase in cloud-based deployments.

Short-Term Forecast: By 2028, predictive scheduling tools are expected to reduce operational costs by 18% and improve first-time fix rates by 22%.

Emerging Technologies: AI-powered route optimization, IoT-enabled predictive maintenance, low-code workflow automation platforms.

Regional Leaders: North America projected at USD 1,050.0 Million by 2033 with advanced SaaS penetration; Europe at USD 780.0 Million driven by regulatory compliance digitization; Asia-Pacific at USD 650.0 Million supported by telecom infrastructure expansion.

Consumer/End-User Trends: Utilities, telecom, healthcare, and FMCG sectors represent over 60% of deployments, emphasizing mobile CRM and real-time reporting.

Pilot or Case Example: In 2024, a telecom operator achieved 25% faster service resolution after deploying AI-based dispatch automation across 5,000 field technicians.

Competitive Landscape: Microsoft holds approximately 18% share, followed by Salesforce, Oracle, SAP, and ServiceNow.

Regulatory & ESG Impact: Data protection regulations and ESG tracking mandates have increased digital compliance reporting by 40% among enterprise users.

Investment & Funding Patterns: Over USD 2.5 Billion invested globally in field service SaaS platforms between 2022–2024, with strong venture funding in AI-enabled workforce analytics.

Innovation & Future Outlook: Integration of generative AI assistants and digital twins for asset servicing is expected to transform remote diagnostics and autonomous scheduling.

Field Force Automation Market adoption is strongest in telecom (28%), utilities (22%), healthcare (15%), and manufacturing services (14%). Recent innovations include AI chat-based field assistants and 5G-enabled real-time diagnostics tools. Regulatory frameworks such as data localization and digital reporting mandates are accelerating SaaS-based deployments. North America and Europe show mature consumption patterns, while Asia-Pacific demonstrates infrastructure-led expansion. Emerging trends include hyperautomation, predictive analytics integration, and sustainability-linked operational optimization strategies.

The Field Force Automation Market holds strategic relevance as enterprises shift toward outcome-based service delivery models and real-time operational intelligence. AI-driven dispatch systems combined with IoT-enabled asset monitoring improve technician utilization by up to 28% and reduce mean time to repair by 24%. Cloud-native Field Force Automation platforms deliver 35% faster deployment compared to legacy on-premise workforce systems, enabling agile scaling across geographically dispersed teams. For example, AI-based route optimization delivers 20% fuel savings compared to manual scheduling methods.

North America dominates in deployment volume, while Asia-Pacific leads in new enterprise adoption with nearly 48% of mid-sized enterprises digitizing field workflows in the past three years. By 2028, predictive analytics embedded within Field Force Automation systems is expected to reduce service downtime by 30% and improve compliance documentation accuracy by 25%.

From a compliance and ESG perspective, firms are committing to 20% carbon footprint reductions by 2030 through optimized route planning and digital documentation eliminating paper-based processes. In 2024, a U.S.-based utility company achieved 27% improvement in technician productivity through AI-powered dynamic scheduling integrated with IoT asset sensors.

Looking ahead, the Field Force Automation Market will evolve as a pillar of operational resilience, regulatory compliance, and sustainable service delivery, enabling enterprises to integrate AI, automation, and mobility into unified, intelligent workforce ecosystems.

The Field Force Automation Market dynamics are shaped by enterprise digital transformation, cloud infrastructure maturity, IoT integration, and AI-based analytics adoption. Organizations are transitioning from manual scheduling systems to integrated platforms that combine CRM, ERP, GPS tracking, and predictive maintenance modules. Over 70% of enterprises with distributed service teams have adopted mobile-based reporting tools, improving transparency and performance benchmarking. Growing demand for real-time field visibility, technician safety monitoring, and customer experience enhancement continues to influence purchasing decisions. Integration with 5G networks further strengthens real-time communication and diagnostics capabilities. Competitive pressures are pushing vendors toward modular, subscription-based SaaS models, while cybersecurity compliance and data governance regulations shape deployment frameworks globally.

Enterprise mobility expansion is significantly accelerating the Field Force Automation Market as organizations deploy smartphones, rugged tablets, and connected devices across field teams. More than 80% of large enterprises now operate bring-your-own-device (BYOD) or managed mobility programs, enabling instant data synchronization between field agents and headquarters. Mobile-enabled technicians demonstrate 30% faster task completion rates compared to paper-based workflows. GPS-integrated platforms improve route efficiency by nearly 25%, reducing fuel consumption and response times. Additionally, cloud-connected mobility solutions enhance customer satisfaction scores by 18% through faster issue resolution and transparent service updates. These mobility-led efficiencies directly contribute to higher technician productivity and operational optimization.

Cybersecurity risks and integration challenges act as restraints in the Field Force Automation Market. Nearly 43% of enterprises report concerns over data breaches involving mobile workforce applications. Integrating automation software with legacy ERP and CRM systems can increase implementation timelines by 20–30%. Complex data migration processes and interoperability issues often require specialized IT resources, raising deployment costs. Furthermore, compliance with regional data protection regulations demands advanced encryption, access control mechanisms, and audit trails. Smaller enterprises with limited IT budgets face difficulties in managing secure cloud transitions, which slows adoption rates despite recognized operational benefits.

AI-driven predictive maintenance presents strong opportunities within the Field Force Automation Market. IoT-enabled sensors generate real-time performance data, allowing predictive analytics systems to detect equipment anomalies with up to 85% accuracy. Predictive maintenance can reduce unplanned downtime by 30% and maintenance costs by nearly 20%. Utilities and manufacturing service providers increasingly deploy digital twin simulations to anticipate equipment failures before they occur. The integration of generative AI-based field assistants further enhances technician troubleshooting capabilities, shortening repair cycles by 22%. These advancements create new revenue streams in subscription-based analytics and remote monitoring services.

Workforce skill gaps and organizational resistance present notable challenges for the Field Force Automation Market. Approximately 38% of field technicians require additional digital training to effectively use advanced mobile applications. Transitioning from manual systems to AI-enabled platforms can initially reduce productivity by 10–15% during adaptation phases. Enterprises must invest in structured training programs and change management frameworks to ensure smooth technology adoption. Additionally, multigenerational workforce environments may experience varying levels of digital proficiency, complicating implementation strategies. Without adequate onboarding and continuous training, automation investments may fail to deliver expected operational improvements.

AI-Driven Intelligent Dispatching Improving Productivity by 28%: AI-based scheduling platforms now analyze real-time traffic, technician skill sets, and job priority levels, increasing technician utilization rates by 28%. Enterprises deploying machine learning dispatch engines report 22% improvement in first-time fix rates and 18% reduction in travel time across large service networks.

IoT-Integrated Predictive Service Reducing Downtime by 30%: Over 65% of utility and telecom operators integrate IoT sensors with Field Force Automation platforms. Predictive alerts reduce equipment downtime by 30% and lower emergency repair visits by 24%, significantly enhancing service reliability and operational transparency.

Cloud-Native Platforms Accelerating Deployment by 35%: Cloud-based Field Force Automation solutions reduce deployment timelines by 35% compared to on-premise systems. Approximately 70% of new enterprise implementations favor SaaS-based subscription models, enabling scalable integration with CRM, ERP, and analytics tools.

5G-Enabled Real-Time Diagnostics Enhancing Resolution Speed by 25%: With 5G rollout expanding globally, real-time video diagnostics and augmented reality support tools are improving issue resolution speed by 25%. Remote expert assistance models reduce repeat site visits by 20%, strengthening cost control and customer satisfaction metrics.

The Field Force Automation Market is segmented by type, application, and end-user, reflecting the operational diversity of industries deploying mobile workforce technologies. By type, organizations choose between cloud-based platforms, on-premise deployments, and hybrid systems depending on data governance, scalability, and integration requirements. Cloud-based solutions currently dominate adoption due to lower upfront infrastructure needs and faster deployment cycles, while hybrid models are gaining traction in regulated sectors.

From an application perspective, core use cases include workforce scheduling, route optimization, inventory tracking, performance analytics, and customer relationship integration. Scheduling and dispatch management represent the most widely deployed functionality due to measurable improvements in technician productivity and response time reduction.

End-user segmentation highlights utilities, telecommunications, healthcare, manufacturing services, logistics, and FMCG sectors as primary adopters. Utilities and telecom operators prioritize predictive maintenance integration, while healthcare providers emphasize compliance documentation and mobile reporting accuracy. Segmentation trends indicate increasing convergence between AI analytics, IoT connectivity, and CRM-linked mobile service execution platforms.

Field Force Automation solutions are primarily categorized into cloud-based, on-premise, and hybrid deployment models. Cloud-based platforms lead the segment, accounting for approximately 65% of total adoption, driven by subscription-based scalability, remote accessibility, and 30–35% faster deployment cycles compared to traditional infrastructure models. In contrast, on-premise systems hold nearly 20% share, primarily preferred by government agencies and defense contractors requiring strict data residency controls. Hybrid models represent around 15% but are expanding steadily. Cloud-based systems are also the fastest-growing type, expanding at an estimated 22% CAGR, supported by increasing enterprise migration toward SaaS ecosystems and integration with AI-powered analytics tools. Hybrid deployments are gaining attention in highly regulated industries such as energy and healthcare, where 40% of enterprises maintain partial on-site data hosting. On-premise systems, though declining in relative share, remain relevant for mission-critical environments demanding full internal control. Collectively, on-premise and hybrid deployments account for roughly 35% of the market, serving compliance-heavy sectors.

In 2024, the U.S. federal IT modernization framework reported that over 60% of newly approved workforce management systems across government departments were deployed using secure cloud-based architectures, improving inter-agency data access and mobile workforce coordination.

Key applications in the Field Force Automation Market include workforce scheduling & dispatch, route optimization, real-time reporting, inventory management, and performance analytics. Workforce scheduling and dispatch management lead with approximately 34% share due to measurable improvements in field productivity and a 25% reduction in service response times. Route optimization follows with around 22% adoption, particularly in logistics-intensive sectors. While scheduling remains dominant, predictive maintenance and AI-driven performance analytics are the fastest-growing applications, expanding at nearly 24% CAGR. Adoption is fueled by IoT sensor integration enabling up to 30% reduction in unplanned downtime. Inventory tracking and CRM-integrated reporting together contribute nearly 28% of usage, ensuring seamless parts management and customer transparency. In 2025, more than 41% of enterprises globally reported piloting AI-enabled dispatch systems to improve service-level compliance. Additionally, 58% of field technicians indicate higher efficiency when supported by mobile analytics dashboards.

In 2025, a national public utilities modernization program integrated AI-based dispatch platforms across 120 service districts, reducing emergency response times by 19% and improving asset visibility across 8,000 field workers.

Utilities represent the leading end-user segment in the Field Force Automation Market, accounting for approximately 28% of total adoption due to widespread deployment of predictive maintenance systems and grid management platforms. Telecommunications follows with nearly 24%, leveraging automation for network infrastructure servicing and 5G rollout operations. Healthcare accounts for around 16%, emphasizing mobile patient documentation and home-care workforce coordination. Healthcare is the fastest-growing end-user, expanding at nearly 23% CAGR, driven by telehealth integration and remote diagnostics adoption. Manufacturing services, logistics, and FMCG sectors collectively contribute roughly 32% of total usage, with 45% of logistics firms implementing GPS-enabled route optimization tools. In 2025, 44% of large enterprises globally reported expanding mobile workforce management budgets, while 52% of telecom operators deployed AI-based troubleshooting assistants for field engineers.

In 2025, a national energy authority implemented predictive maintenance automation across 3,500 substations, improving technician productivity by 26% and reducing grid maintenance delays by 18%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23% between 2026 and 2033.

Europe follows with 27% share, supported by regulatory-driven digital compliance initiatives, while Asia-Pacific currently holds 24% but demonstrates strong enterprise digitization momentum. South America and Middle East & Africa collectively contribute 11%, driven by infrastructure modernization and energy-sector automation. Over 70% of North American utilities utilize AI-based dispatch platforms, compared to 55% in Europe and 48% in Asia-Pacific. Asia-Pacific records the highest new enterprise onboarding rate, with nearly 46% of mid-sized companies digitizing field operations within the past three years. Europe reports that 62% of large enterprises integrate automation tools to meet ESG and regulatory reporting standards. Emerging markets show increasing telecom infrastructure deployment, with 5G-related field servicing demand rising by 31% year-over-year across Asia-Pacific economies.

North America holds approximately 38% of the global Field Force Automation Market share. Utilities, telecommunications, healthcare, and industrial services are the primary demand drivers. More than 72% of large enterprises in the region deploy mobile workforce management systems integrated with CRM and ERP software. Regulatory frameworks such as federal data protection standards and digital compliance mandates encourage secure cloud adoption. Technological advancements include AI-driven predictive analytics, IoT-enabled asset monitoring, and 5G-supported remote diagnostics. A leading regional provider, ServiceNow, expanded AI-powered field workflow automation across major U.S. utility providers, improving technician scheduling accuracy by over 20%. Consumer behavior in the region shows higher enterprise adoption in healthcare and financial service support operations, where compliance documentation accuracy exceeds 90% through automated reporting systems.

Europe accounts for nearly 27% of global adoption, led by Germany, the United Kingdom, and France. Strong regulatory oversight and sustainability directives drive demand for digital compliance tracking and ESG-based operational monitoring. Approximately 62% of European enterprises deploy automation tools aligned with data governance standards. Emerging technologies such as AI-enabled route optimization and carbon-tracking dashboards are increasingly embedded within workforce platforms. SAP, headquartered in Germany, has enhanced its field service management suite with AI-driven analytics modules tailored for manufacturing and energy firms. Regional enterprises demonstrate cautious but steady adoption, with regulatory pressure leading to demand for explainable AI systems and secure hybrid deployments.

Asia-Pacific holds approximately 24% of the global market and ranks second in overall deployment volume. China, India, and Japan are the top consuming countries, driven by telecom expansion and infrastructure modernization. Over 48% of mid-sized enterprises in the region have adopted mobile workforce applications in the past three years. Infrastructure growth, smart city initiatives, and manufacturing automation are key drivers. Regional innovation hubs emphasize AI-based route planning and mobile-first SaaS deployment. A major Indian telecom operator deployed AI-assisted field diagnostics across 4,000 technicians, improving service restoration times by 21%. Consumer behavior trends show growth driven by e-commerce logistics and mobile-enabled applications.

South America contributes around 6% of the global Field Force Automation Market, with Brazil and Argentina as primary adopters. Infrastructure and energy sector modernization projects are increasing demand for predictive maintenance platforms. Government-backed digital transformation initiatives in Brazil encourage SaaS-based enterprise software deployment. Telecom network expansion and utilities digitization programs are key growth areas. Regional enterprises focus on cost-efficient mobile solutions, with 39% of logistics operators implementing GPS-based tracking systems. Demand is tied to localized service management and multilingual support integration.

The Middle East & Africa region accounts for approximately 5% of the global market. Demand is concentrated in oil & gas, construction, and utilities sectors, particularly in the UAE and South Africa. Infrastructure modernization projects and smart city investments stimulate automation deployment. Regional technology modernization includes IoT-enabled asset tracking and AI-based maintenance scheduling. Local energy companies increasingly adopt digital inspection platforms, with 33% of large oil & gas operators implementing automated field reporting systems. Trade partnerships and government-backed digital economy programs support enterprise mobility expansion.

United States – 34% Market Share: It leads due to advanced enterprise SaaS infrastructure, large-scale utility automation projects, and widespread AI integration across telecom and healthcare sectors.

Germany – 11% Market Share: It is driven by strong manufacturing service demand, regulatory-driven digital compliance requirements, and high adoption of AI-enabled industrial service platforms.

The Field Force Automation Market is moderately fragmented, with more than 120 active global and regional vendors competing across cloud-based workforce management, AI-enabled dispatch systems, and mobile CRM integration platforms. The top five companies collectively account for approximately 52% of total market share, indicating a semi-consolidated structure dominated by enterprise SaaS providers with broad digital ecosystem capabilities.

Market leaders differentiate themselves through integrated AI analytics, IoT compatibility, and low-code workflow customization tools. Approximately 68% of leading vendors now offer AI-driven predictive maintenance modules, while 55% provide embedded route optimization engines powered by machine learning algorithms. Strategic partnerships with telecom operators, utilities, and ERP providers have increased by over 30% between 2023 and 2025, reflecting ecosystem-based competition.

Product innovation cycles have accelerated, with major vendors launching at least one significant feature upgrade annually. Cloud-native deployments represent nearly 70% of new contracts among leading firms. Mergers and acquisitions activity has also intensified, with over 15 notable acquisitions in workforce automation and AI scheduling startups since 2023. Competitive positioning increasingly focuses on vertical specialization, cybersecurity certifications, ESG tracking capabilities, and industry-specific compliance modules to secure enterprise-level contracts.

SAP

ServiceNow

IFS

Trimble Inc.

ClickSoftware

Zoho Corporation

Verizon Connect

Honeywell International Inc.

OverIT

FieldAware

Coresystems

ServiceMax

Praxedo

The Field Force Automation Market is undergoing rapid technological transformation driven by AI, IoT, 5G connectivity, and advanced analytics integration. AI-powered dispatch algorithms improve technician utilization rates by up to 28% by dynamically assigning jobs based on skill set, location, and urgency. Machine learning-based predictive maintenance platforms analyze sensor data streams from IoT-enabled assets, reducing unplanned downtime by nearly 30% across utilities and manufacturing services.

IoT integration remains a key enabler, with over 65% of utility operators deploying connected sensors that transmit real-time performance metrics to centralized dashboards. 5G-enabled field diagnostics facilitate high-definition video troubleshooting and augmented reality (AR)-based remote assistance, improving first-time fix rates by 22%. AR smart glasses adoption in industrial field servicing increased by 18% between 2023 and 2025.

Cloud-native microservices architecture supports modular deployment, enabling enterprises to scale workforce operations across multiple geographies with 35% faster implementation timelines. Low-code and no-code workflow customization platforms are increasingly adopted, with nearly 40% of mid-sized enterprises leveraging configurable dashboards to tailor automation processes without dedicated development teams.

Cybersecurity technologies such as end-to-end encryption, multi-factor authentication, and zero-trust architecture models are integrated into over 60% of newly deployed systems, addressing data governance requirements. Generative AI assistants are emerging within technician mobile apps, delivering real-time troubleshooting recommendations and automated documentation, reducing administrative workload by approximately 20%.

• In February 2025, PTC launched ServiceMax AI, a generative AI-powered field service management assistant that helps technicians automate manual tasks, review service history, answer job-specific questions, and provide predictive maintenance guidance, enhancing frontline technician efficiency across service organizations. Source: www.ptc.com

• In September 2025, PTC expanded its ServiceMax portfolio with new Service Lifecycle Management AI solutions, introducing agentic AI enhancements in ServiceMax AI and Servigistics that accelerate work order execution, improve first-time fix rates, and provide smarter parts planning intelligence for service supply chains. Source: www.prnewswire.com

• In April 2025, IFS unveiled the IFS Cloud 25R1 release, incorporating over 200 industrial AI-based capabilities—such as AI forecasting, 3D visualization of maintenance tasks, and AI-driven work generation—enabling enterprises to automate workflows, optimize inventory planning, and deliver improved situational decision-making across asset- and service-intensive operations. Source: www.ifs.com

• In May/June 2025, Dynamics 365 Field Service introduced major enhancements including the Online Mode for live data access and announced that the Exchange integration feature (syncing Field Service work orders with Outlook and Teams calendars) became generally available as part of the 2025 release wave 2, improving schedule visibility for technicians across enterprise Microsoft ecosystems. Source: www.microsoft.com

The Field Force Automation Market Report provides a comprehensive analysis of deployment models, applications, technologies, end-user industries, and regional performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study evaluates over 15 major vendors and profiles more than 100 active competitors operating across enterprise SaaS, AI-driven dispatch, and IoT-integrated service platforms.

The report covers segmentation by type, including cloud-based, on-premise, and hybrid systems, as well as detailed application insights such as workforce scheduling, route optimization, predictive maintenance, inventory tracking, and performance analytics. End-user coverage spans utilities (28% adoption), telecommunications (24%), healthcare (16%), manufacturing services, logistics, and FMCG sectors.

Technological scope includes AI-based analytics, IoT asset monitoring, 5G-enabled diagnostics, augmented reality support tools, low-code automation frameworks, and cybersecurity integration models. The report also assesses enterprise mobility penetration exceeding 80% in developed economies and rising mid-market digitization rates nearing 46% in emerging regions.

Geographic analysis incorporates infrastructure modernization projects, regulatory digitization mandates, ESG compliance initiatives, and sector-specific digital transformation programs influencing adoption patterns. Additionally, the report evaluates competitive strategies, partnership ecosystems, product innovation frequency, and digital transformation investment trends shaping the global Field Force Automation Market landscape for strategic decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 660.0 Million |

| Market Revenue (2033) | USD 2,837.9 Million |

| CAGR (2026–2033) | 20% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft; Salesforce; Oracle; SAP; ServiceNow; IFS; Trimble Inc.; ClickSoftware; Zoho Corporation; Verizon Connect; Honeywell International Inc.; OverIT; FieldAware; Coresystems; ServiceMax; Praxedo |

| Customization & Pricing | Available on Request (10% Customization Free) |