Reports

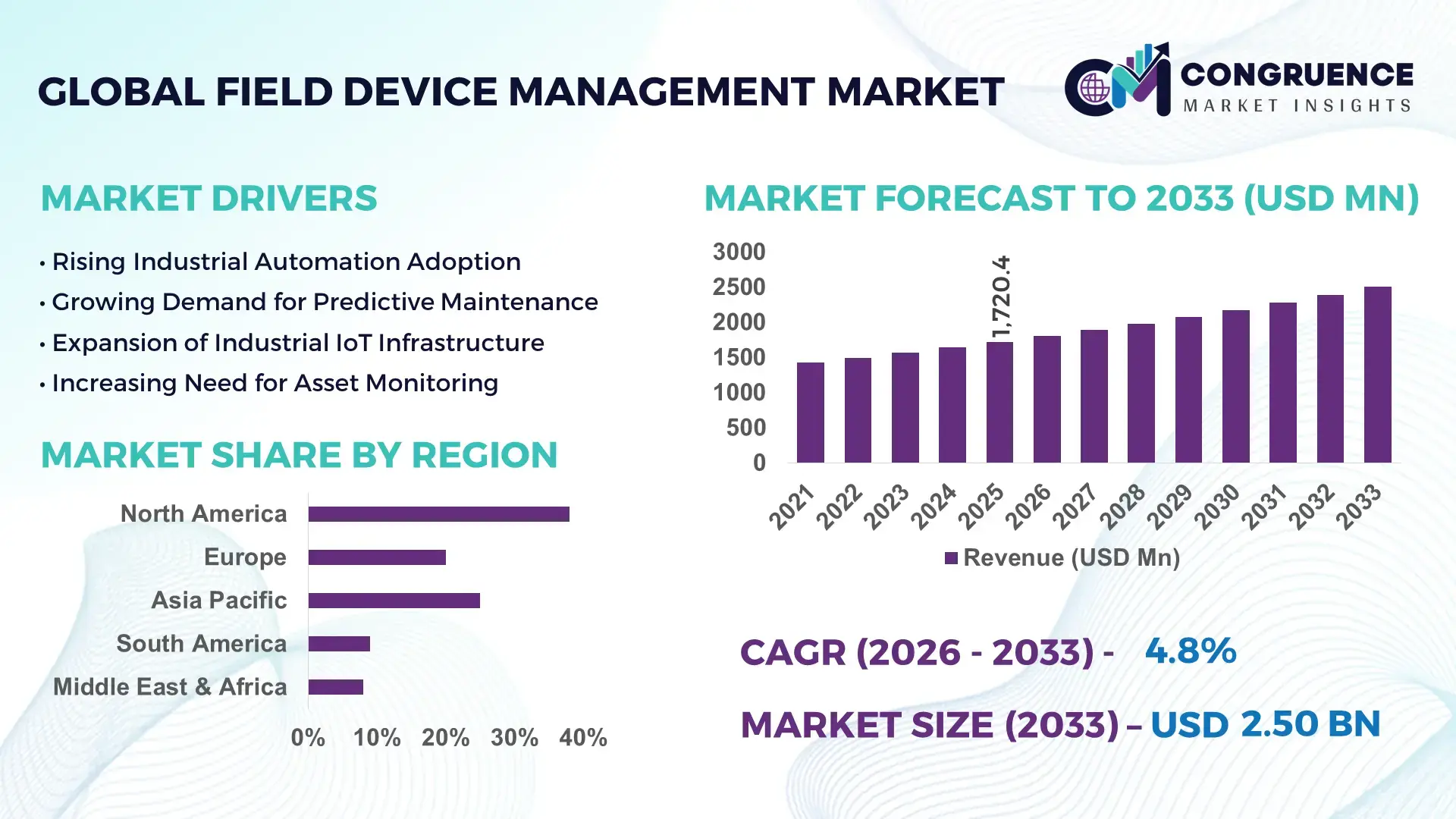

The Global Field Device Management Market was valued at USD 1720.38 Million in 2025 and is anticipated to reach a value of USD 2503.31 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033. This growth is primarily driven by rising demand for advanced industrial automation and predictive maintenance solutions across manufacturing, energy, and process industries.

The United States remains a dominant hub for field device management deployment across industrial automation infrastructure. The country hosts over 25,000 large-scale process plants that utilize intelligent field instruments integrated with digital asset management platforms. In sectors such as oil and gas, chemical processing, and power generation, more than 68% of industrial facilities use smart field devices equipped with communication protocols like HART, FOUNDATION Fieldbus, and Modbus. Industrial automation investment in the U.S. exceeded USD 240 billion in recent years, with a significant share allocated to industrial software platforms for device configuration, diagnostics, and lifecycle management. In addition, over 72% of U.S. manufacturing enterprises have implemented Industrial Internet of Things (IIoT) solutions that integrate field device management systems for real-time monitoring, predictive analytics, and operational optimization. These deployments enable centralized device configuration across thousands of instruments, significantly improving asset visibility and reducing maintenance downtime in large-scale industrial facilities.

Market Size & Growth: Valued at USD 1720.38 Million in 2025 and projected to reach USD 2503.31 Million by 2033 at a CAGR of 4.8%, driven by increased industrial automation and digital asset management adoption.

Top Growth Drivers: Industrial automation adoption (62%), predictive maintenance implementation (48%), expansion of IIoT-enabled industrial systems (55%).

Short-Term Forecast: By 2028, predictive maintenance enabled by field device management platforms is expected to reduce industrial maintenance costs by nearly 18% while improving equipment availability by 22%.

Emerging Technologies: Integration of Industrial Internet of Things platforms, AI-based diagnostics, and cloud-enabled device lifecycle management tools is reshaping field instrumentation monitoring.

Regional Leaders: North America projected to exceed USD 850 Million by 2033 with strong oil and gas adoption; Europe expected to surpass USD 700 Million driven by industrial digitalization initiatives; Asia-Pacific anticipated to reach USD 640 Million as manufacturing automation accelerates.

Consumer/End-User Trends: Oil and gas operators, chemical manufacturers, and power utilities increasingly deploy field device management software to monitor thousands of sensors and transmitters across distributed assets.

Pilot or Case Example: In 2024, a large refinery in the Middle East implemented AI-enabled field device diagnostics, reducing equipment downtime by 27% and improving maintenance scheduling efficiency by 31%.

Competitive Landscape: Emerson Electric leads with approximately 21% market presence, followed by Siemens, ABB, Honeywell International, and Schneider Electric.

Regulatory & ESG Impact: Industrial emission monitoring regulations and energy efficiency directives are pushing companies to adopt digital instrumentation management systems for compliance tracking.

Investment & Funding Patterns: More than USD 3.2 billion has been invested globally in industrial automation software platforms and IIoT-based asset management technologies over the last few years.

Innovation & Future Outlook: AI-enabled predictive diagnostics, digital twin integration, and cloud-based instrumentation management platforms are expected to redefine industrial asset monitoring and device lifecycle optimization.

Field device management solutions play a crucial role across multiple industrial sectors including oil and gas, power generation, chemicals, pharmaceuticals, and water treatment. Oil and gas operations account for nearly 30% of industrial field instrumentation usage due to extensive pipeline monitoring and process control requirements. Power utilities contribute approximately 22% of deployments, particularly for turbine monitoring and grid automation systems. Continuous innovation in wireless instrumentation, edge analytics, and remote configuration technologies is transforming device lifecycle management capabilities. Governments across North America, Europe, and Asia are introducing stricter industrial emission monitoring regulations, encouraging companies to deploy intelligent instrumentation and centralized management platforms. Additionally, the adoption of predictive analytics and digital twins is enabling operators to monitor thousands of field devices in real time, significantly improving equipment reliability and operational safety across complex industrial environments.

The Field Device Management Market holds strategic importance in modern industrial operations as organizations transition toward data-driven automation and smart manufacturing ecosystems. Advanced device management platforms enable centralized configuration, calibration, diagnostics, and lifecycle monitoring for thousands of industrial sensors, actuators, and transmitters. In comparison, AI-enabled predictive maintenance platforms deliver nearly 35% improvement in equipment failure detection compared to traditional manual inspection and maintenance procedures.

Asia-Pacific dominates in industrial device deployment volume due to large-scale manufacturing and energy infrastructure, while North America leads in digital adoption with nearly 70% of industrial enterprises implementing integrated device management systems across operational technology networks. By 2028, AI-driven diagnostic analytics integrated into field device management software are expected to reduce unplanned equipment downtime by approximately 25% across process industries.

From an ESG perspective, industrial operators are committing to operational efficiency targets including up to 30% reduction in energy losses and emission monitoring improvements by 2030 through intelligent instrumentation management. In 2024, a German chemical manufacturing facility implemented AI-powered field device diagnostics and achieved a 28% reduction in maintenance interventions through automated condition monitoring. As industries pursue digital transformation and operational resilience, the Field Device Management Market is emerging as a critical pillar supporting intelligent infrastructure, regulatory compliance, and sustainable industrial growth.

The expansion of industrial automation across manufacturing, energy, and chemical sectors is significantly increasing demand for field device management platforms. Globally, more than 40 billion industrial sensors are expected to be deployed within the next few years, requiring centralized configuration and lifecycle monitoring. Automated plants often operate over 5,000 field instruments including transmitters, controllers, and analyzers that require continuous diagnostics. Field device management solutions improve operational visibility and can reduce maintenance response time by up to 35%, making them essential tools for digital factories and large-scale industrial process facilities.

Integrating field device management systems into legacy industrial infrastructure remains a major challenge for many companies. Older industrial plants still operate with proprietary protocols and incompatible communication standards, making system integration complex and expensive. Studies indicate that nearly 45% of industrial facilities worldwide still rely on legacy instrumentation platforms that require manual configuration processes. Upgrading these systems to support modern device management software can require extensive retrofitting, specialized technical expertise, and extended downtime during installation, which discourages some organizations from immediate adoption.

The rapid adoption of Industrial Internet of Things technology presents significant growth opportunities for field device management solutions. IIoT platforms allow companies to collect real-time operational data from thousands of sensors and transmitters deployed across production environments. Industrial data generation is projected to exceed 175 zettabytes globally in the coming years, creating strong demand for intelligent device management platforms capable of processing, analyzing, and optimizing field instrumentation performance. These systems enable predictive analytics, remote diagnostics, and automated asset monitoring across distributed industrial networks.

Cybersecurity vulnerabilities represent a major challenge for field device management deployment in industrial environments. Modern industrial control systems increasingly rely on network-connected devices, making them potential targets for cyberattacks. Studies indicate that more than 54% of industrial organizations have experienced attempted cyber intrusions targeting operational technology infrastructure. Compromised field devices can disrupt process control systems and critical infrastructure operations. As a result, companies must invest heavily in secure communication protocols, network segmentation, and advanced cybersecurity frameworks when implementing device management platforms across industrial networks.

• Expansion of Industrial Internet of Things Integration:

Industrial facilities are rapidly integrating field device management platforms with Industrial Internet of Things ecosystems. More than 65% of modern manufacturing plants now deploy connected sensors and transmitters linked to centralized management systems. Industrial networks in advanced plants manage over 10,000 field devices simultaneously, enabling automated configuration and diagnostics. Adoption of IIoT-enabled monitoring has reduced maintenance response times by nearly 32% and improved asset reliability by 27% in high-automation industries.

• Growth of Predictive Maintenance and AI-Driven Diagnostics:

Artificial intelligence is transforming field instrumentation monitoring by enabling predictive analytics across industrial assets. Nearly 58% of industrial operators now deploy predictive maintenance tools integrated with device management software. These systems analyze thousands of operational parameters per device and can detect early equipment failures with nearly 35% higher accuracy than traditional inspection methods. As a result, industrial downtime linked to field instrument failures has declined by approximately 24% in digitally enabled plants.

• Rise in Wireless Field Devices and Remote Configuration:

Wireless communication protocols such as WirelessHART and ISA100 are expanding the reach of field device management systems. Over 40% of new industrial instrumentation installations now include wireless connectivity, allowing remote configuration and calibration. Large process facilities can remotely monitor more than 5,000 field instruments from centralized control centers. This transition has reduced on-site maintenance visits by nearly 30% while improving operational efficiency and equipment utilization.

• Adoption of Digital Twin Technology for Asset Monitoring:

Digital twin platforms are increasingly integrated with field device management software to replicate industrial assets in virtual environments. Nearly 48% of large industrial organizations are deploying digital twin simulations to monitor thousands of field instruments in real time. These platforms enable predictive scenario testing and performance optimization, improving process efficiency by nearly 20% while reducing unplanned shutdown events by approximately 18% in advanced manufacturing facilities.

The Field Device Management market demonstrates diverse segmentation across product types, industrial applications, and end-user industries. Device management platforms are deployed to configure, monitor, and maintain thousands of industrial sensors, transmitters, and control instruments operating in complex process environments. By type, hardware interfaces, software platforms, and integrated communication modules form the primary segments supporting device configuration and lifecycle monitoring. Application segmentation is driven by industries such as oil and gas, power generation, chemical manufacturing, and water treatment facilities where operational reliability is critical. End-user analysis highlights strong adoption among large industrial enterprises that manage extensive instrumentation networks across geographically distributed plants. Increasing demand for predictive maintenance and automated diagnostics is accelerating adoption across manufacturing and energy sectors. Additionally, rising regulatory requirements for emission monitoring and operational safety are encouraging industries to implement centralized instrumentation management systems capable of monitoring thousands of field devices in real time.

Software platforms represent the leading segment in the Field Device Management market, accounting for nearly 46% of total adoption due to their role in device configuration, diagnostics, and lifecycle monitoring across industrial automation systems. Hardware interface modules hold approximately 32% share, supporting connectivity between field instruments and control networks. Communication protocol integration tools and device adapters collectively represent around 22% of the remaining market, serving niche roles in legacy equipment connectivity and protocol translation.Software-based field device management solutions are also the fastest-growing type with an estimated 6.2% growth rate, driven by increased adoption of cloud-enabled monitoring and AI-powered diagnostics in industrial environments. Advanced software platforms allow operators to manage more than 10,000 devices from a centralized interface, improving operational efficiency and reducing manual maintenance tasks.

Oil and gas operations dominate application deployment in the Field Device Management market, accounting for approximately 34% of global adoption due to extensive instrumentation across upstream exploration, pipelines, and refining operations. Power generation represents around 27% of the market as utilities increasingly rely on digital instrumentation monitoring for turbines, generators, and grid infrastructure. However, chemical processing facilities are emerging as the fastest-growing application segment with an estimated 5.9% growth rate, driven by increasing automation and strict process safety monitoring requirements.Water treatment plants, pharmaceutical manufacturing facilities, and food processing industries collectively account for nearly 39% of remaining adoption, where real-time device monitoring improves process control and regulatory compliance.

Large industrial enterprises represent the dominant end-user segment in the Field Device Management market, accounting for nearly 52% of total deployments due to their extensive networks of industrial sensors, valves, and process controllers. These organizations often manage facilities with over 5,000 field instruments requiring centralized configuration and lifecycle monitoring. Mid-size manufacturing companies account for approximately 28% of adoption, particularly in automated production environments. Infrastructure utilities such as power grids, water management authorities, and transportation systems collectively represent around 20% of remaining market adoption. Among these segments, infrastructure utilities are the fastest-growing end-user group with an estimated 6.1% growth rate as governments invest in smart infrastructure monitoring systems.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

Europe held approximately 28% of the global Field Device Management market in 2025, supported by advanced industrial automation across Germany, France, and the United Kingdom. Asia-Pacific represented nearly 24% of total installations with more than 15,000 manufacturing facilities deploying smart field instrumentation. South America contributed around 7%, while the Middle East & Africa accounted for roughly 5%, largely driven by oil and gas monitoring infrastructure and industrial modernization programs.

How Are Industrial Automation and Predictive Maintenance Accelerating Digital Instrumentation Management?

North America represents approximately 36% of the global Field Device Management market, supported by advanced industrial automation infrastructure and extensive deployment of smart instrumentation. The region hosts more than 30,000 large-scale manufacturing and process plants utilizing thousands of field sensors, controllers, and transmitters for automated monitoring. Oil and gas, power generation, and pharmaceutical manufacturing remain the primary industries driving adoption. Regulatory initiatives emphasizing operational safety, environmental monitoring, and energy efficiency are encouraging organizations to implement centralized device management platforms capable of monitoring thousands of instruments simultaneously. Digital transformation trends are also reshaping industrial maintenance strategies. More than 70% of industrial enterprises have implemented predictive maintenance systems linked to field device management software. A notable example includes Emerson Electric, which continues to expand advanced digital asset management platforms supporting more than 12,000 connected field devices across large industrial facilities. Consumer behavior across enterprises in this region reflects strong adoption of cloud-based automation platforms and real-time operational analytics to enhance equipment reliability and reduce maintenance costs.

How Are Industrial Sustainability Regulations Driving Demand for Intelligent Device Monitoring Systems?

Europe accounts for nearly 28% of the global Field Device Management market, supported by strong industrial automation adoption in Germany, the United Kingdom, France, and Italy. Germany alone hosts more than 8,000 automated manufacturing facilities deploying smart sensors and transmitters connected to centralized instrumentation management systems. Regulatory initiatives aimed at improving industrial efficiency and reducing emissions are accelerating the adoption of advanced monitoring technologies across energy and chemical processing sectors. The European Union’s sustainability frameworks encourage industrial companies to implement intelligent monitoring tools that enable precise equipment diagnostics and energy consumption analysis. More than 60% of European process industries are currently integrating Industrial Internet of Things platforms with field device management solutions to monitor thousands of operational instruments in real time. Siemens, a major regional technology provider, has introduced advanced digital instrumentation management software that allows operators to manage over 10,000 industrial field devices through centralized automation systems. Consumer adoption trends show strong preference for explainable and compliance-focused industrial monitoring technologies due to strict environmental and safety regulations.

What Factors Are Accelerating Smart Industrial Instrumentation Adoption Across Emerging Manufacturing Hubs?

Asia-Pacific represents approximately 24% of the global Field Device Management market and ranks among the fastest expanding regions for industrial automation deployment. China, Japan, and India collectively operate more than 20,000 high-volume manufacturing plants that rely on thousands of smart field instruments for process monitoring and control. Rapid expansion of electronics manufacturing, chemical production, and energy infrastructure is accelerating demand for advanced instrumentation management systems. Industrial modernization programs across the region are integrating digital control systems with predictive maintenance technologies. More than 55% of newly automated factories in Asia-Pacific now deploy centralized field device monitoring platforms capable of managing over 8,000 connected sensors and controllers. ABB has expanded its industrial automation solutions in several Asian manufacturing hubs, introducing cloud-enabled device management tools designed to monitor complex instrumentation networks across large production environments. Consumer adoption patterns indicate strong demand for scalable automation technologies as manufacturers seek to improve equipment reliability and optimize operational performance.

How Is Industrial Modernization Supporting the Expansion of Smart Instrumentation Systems?

South America accounts for roughly 7% of the global Field Device Management market, with Brazil and Argentina serving as the primary contributors to industrial instrumentation adoption. Brazil alone operates more than 2,500 large-scale industrial plants across energy, mining, and manufacturing sectors that rely heavily on field sensors and control devices for operational monitoring. Growing investment in energy infrastructure and refinery modernization is increasing demand for advanced device management solutions. Government initiatives supporting digital industrial infrastructure are encouraging companies to deploy predictive maintenance platforms capable of monitoring thousands of connected field instruments. More than 40% of industrial facilities in Brazil have begun transitioning toward automated monitoring systems integrated with field device management software. Schneider Electric has expanded automation technology deployment across multiple industrial plants in the region, introducing digital monitoring solutions that improve equipment diagnostics and operational visibility. Regional adoption trends show growing demand for intelligent monitoring systems in energy and mining sectors where operational efficiency and safety remain critical.

How Are Energy Infrastructure Investments Driving Intelligent Device Monitoring Systems?

The Middle East & Africa region holds approximately 5% of the global Field Device Management market and is witnessing increased demand driven by energy sector modernization. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are investing heavily in advanced oil, gas, and power infrastructure that requires continuous monitoring of thousands of field instruments. Large refineries and offshore energy facilities often operate more than 7,000 sensors and transmitters integrated with automated monitoring platforms. Technological modernization initiatives are encouraging industrial operators to implement predictive maintenance and digital instrumentation management systems capable of detecting equipment anomalies in real time. Regional partnerships between industrial automation providers and national energy companies are expanding adoption of intelligent monitoring technologies. Honeywell has deployed advanced device management solutions across several energy facilities in the region, enabling centralized monitoring of complex instrumentation networks. Consumer behavior reflects strong demand for automation technologies that enhance operational reliability, safety compliance, and infrastructure resilience across large energy projects.

United States – 32% share in the Field Device Management market: Dominance supported by large-scale industrial automation infrastructure and extensive deployment of predictive maintenance systems across manufacturing and energy facilities.

Germany – 18% share in the Field Device Management market: Strong industrial engineering sector and advanced smart factory adoption drive extensive use of intelligent field instrumentation management platforms.

The Field Device Management market exhibits a moderately consolidated competitive structure with more than 40 active technology providers offering industrial automation software, instrumentation diagnostics platforms, and device lifecycle management tools. The top five companies collectively control approximately 48% of global deployments, reflecting strong technological capabilities and established industrial partnerships. Competition is primarily driven by innovation in predictive analytics, Industrial Internet of Things integration, and cloud-enabled instrumentation monitoring platforms.

Strategic collaborations between automation vendors and industrial manufacturers are increasing, with over 25 partnership initiatives announced across automation software providers and equipment manufacturers in recent years. Product innovation is another key competitive factor, with more than 60 new industrial device management software upgrades launched globally in the last two years. Vendors are also investing heavily in artificial intelligence diagnostics, cybersecurity frameworks, and digital twin technologies to strengthen market positioning and address evolving industrial automation requirements.

Emerson Electric Co.

Siemens AG

ABB Ltd.

Honeywell International Inc.

Schneider Electric SE

Yokogawa Electric Corporation

Endress+Hauser Group

Rockwell Automation Inc.

Azbil Corporation

Metso Corporation

General Electric Company

Mitsubishi Electric Corporation

Technological innovation is significantly reshaping the Field Device Management market as industries adopt advanced automation and digital asset monitoring platforms. Modern device management systems now support more than 20 communication protocols including HART, FOUNDATION Fieldbus, Profibus, and Modbus, enabling interoperability across thousands of field instruments. In highly automated facilities, a single management platform can monitor over 10,000 connected sensors, transmitters, and actuators simultaneously.

Industrial Internet of Things integration is a major technological advancement enabling real-time monitoring and predictive diagnostics across distributed industrial assets. More than 60% of new industrial plants now deploy IIoT-enabled field devices capable of transmitting continuous operational data for centralized analytics. Artificial intelligence algorithms embedded within management platforms analyze thousands of performance parameters per device, improving fault detection accuracy by nearly 35%.

Cloud-enabled device management software is also expanding rapidly, allowing remote configuration and firmware updates for large fleets of instruments across multiple facilities. Wireless communication technologies such as WirelessHART and ISA100 are increasingly deployed, with over 40% of new industrial instrumentation installations supporting wireless connectivity. Additionally, digital twin platforms are being integrated with device management tools, enabling operators to simulate operational conditions and predict equipment performance, reducing unplanned shutdown incidents by approximately 20% in advanced industrial environments.

• In March 2025, Emerson Electric launched an enhanced version of its AMS Device Manager platform with integrated AI-based predictive diagnostics. The upgrade enables industrial operators to monitor over 12,000 connected field devices simultaneously and automatically detect potential instrument failures through real-time performance analytics. Source: www.emerson.com

• In September 2024, Siemens introduced an advanced update to its SIMATIC Process Device Manager, expanding compatibility with more than 10,000 field instruments across multiple communication protocols including HART, PROFIBUS, and PROFINET. The update improves centralized device configuration and lifecycle monitoring across large industrial automation environments. Source: www.siemens.com

• In May 2025, ABB expanded its Ability™ Field Information Manager platform with enhanced cloud-based device monitoring capabilities. The system now supports remote diagnostics for thousands of field instruments across industrial plants, enabling predictive maintenance and reducing manual inspection requirements in complex process facilities.

• In November 2024, Schneider Electric released an upgraded EcoStruxure Field Device Expert platform designed to improve cybersecurity and interoperability for industrial instrumentation networks. The new platform allows centralized configuration and monitoring of over 8,000 connected devices across multiple production sites, improving operational reliability and compliance management.

The Field Device Management Market Report provides a comprehensive analysis of global industry developments across key technology segments, applications, and geographic regions. The report evaluates device management software platforms, hardware communication interfaces, and integrated industrial monitoring tools used to configure, diagnose, and maintain thousands of connected field instruments within automated industrial systems.

The study covers major application sectors including oil and gas, power generation, chemical processing, pharmaceuticals, water treatment, and manufacturing industries where advanced instrumentation management is critical for operational efficiency and safety compliance. It analyzes the deployment of more than 50 types of industrial sensors, transmitters, and controllers integrated with digital asset management systems.

Geographically, the report assesses market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering over 30 major industrial economies with strong automation infrastructure. In addition, the report examines emerging technologies such as Industrial Internet of Things integration, wireless instrumentation networks, artificial intelligence diagnostics, and digital twin-based asset monitoring platforms. The analysis also explores adoption trends among large enterprises, infrastructure utilities, and mid-size manufacturing organizations that manage extensive instrumentation networks across complex industrial facilities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Emerson Electric Co., Siemens AG, ABB Ltd., Honeywell International Inc., Schneider Electric SE, Yokogawa Electric Corporation, Endress+Hauser Group, Rockwell Automation Inc., Azbil Corporation, Metso Corporation, General Electric Company, Mitsubishi Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |