Reports

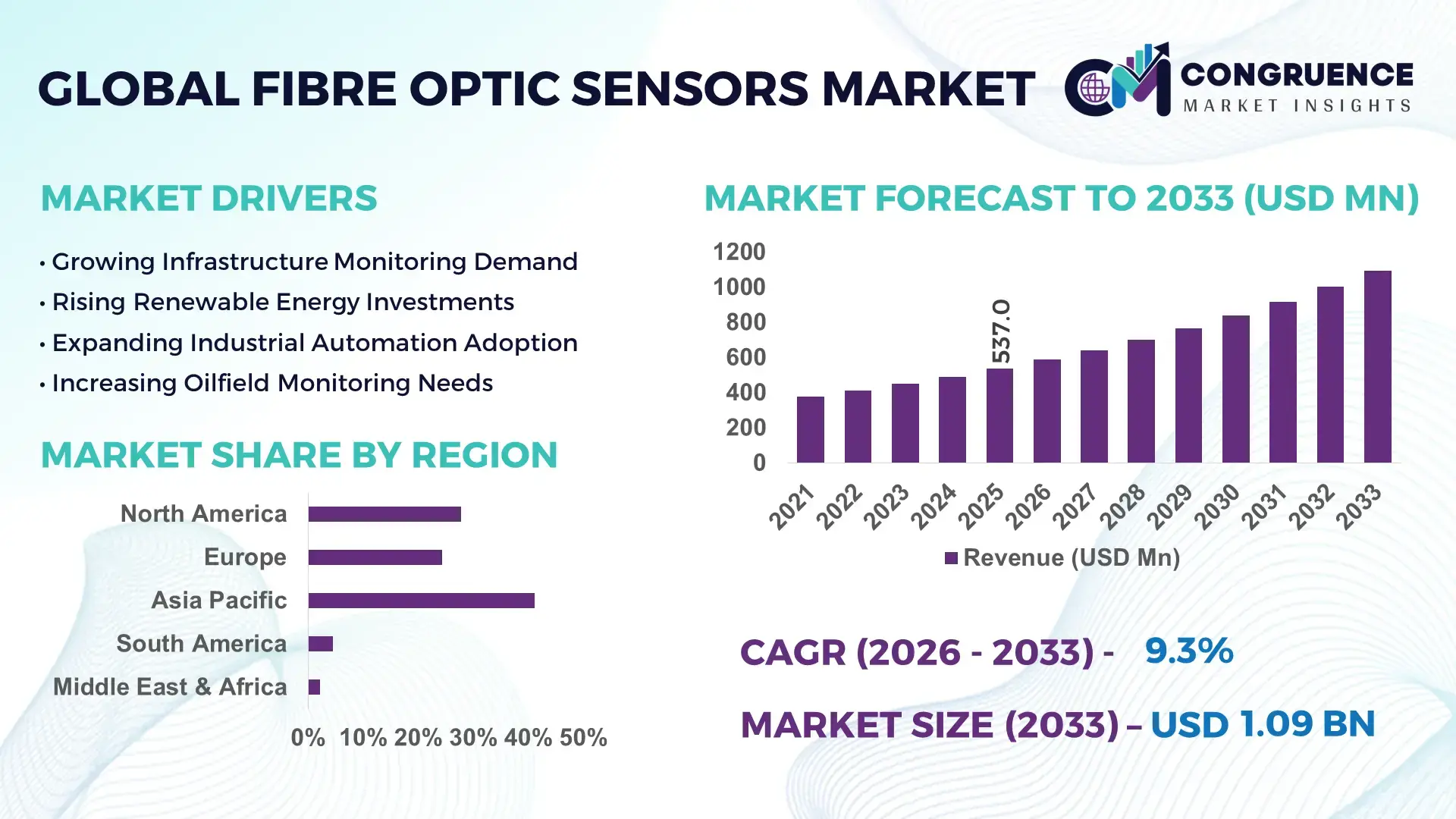

The Global Fibre Optic Sensors Market was valued at USD 537.0 Million in 2025 and is anticipated to reach a value of USD 1,093.8 Million by 2033 expanding at a CAGR of 9.3% between 2026 and 2033. Growth is being accelerated by large-scale deployment of structural health monitoring systems across energy pipelines, offshore assets, smart transportation corridors, and high-voltage power networks requiring continuous real-time sensing accuracy.

China dominates the market with approximately 31% of global fibre optic sensor deployment capacity, supported by over 42,000 km of high-speed rail infrastructure, extensive power transmission modernization, and expanding offshore energy projects. The United States accounts for nearly 24% market participation, driven by advanced aerospace and defense integration, while China deploys around 1.3x more fibre-based infrastructure monitoring systems annually. Rising investments linked to critical infrastructure resilience and industrial digitalization continue strengthening national adoption rates.

Companies securing positions in infrastructure monitoring, energy asset integrity, and industrial automation ecosystems are best placed to capture long-term value creation opportunities.

Market Size & Growth: USD 537.0 Million in 2025 reaching USD 1,093.8 Million by 2033, supported by expanding smart infrastructure monitoring and industrial automation deployment.

Top Growth Drivers: Infrastructure monitoring adoption (+28%), energy transmission modernization (+24%), and industrial digitalization investments (+21%) remain primary demand catalysts.

Short-Term Forecast: By 2028, predictive maintenance efficiency is expected to improve by nearly 30% while inspection costs decline by approximately 18%.

Emerging Technologies: AI-driven analytics, distributed acoustic sensing (DAS), and advanced photonic sensing platforms are enhancing monitoring precision by over 25%.

Regional Leaders: Asia Pacific (~USD 430 Million), North America (~USD 285 Million), and Europe (~USD 220 Million) benefit from railway, utility, and industrial monitoring expansion.

Consumer/End-User Trends: More than 52% of new critical infrastructure projects now incorporate continuous fiber-based sensing capabilities.

Pilot/Case Example: In 2024, advanced pipeline monitoring deployments reduced leak detection response times by nearly 40% across selected energy assets.

Competitive Landscape: Top five suppliers control roughly 45% of market activity, led by companies including Halliburton, Luna Innovations, Yokogawa, HBM FiberSensing, and Omnisens.

Regulatory & ESG Impact: Infrastructure resilience programs improved asset monitoring coverage by nearly 22%, supporting lower maintenance-related environmental risks.

Investment & Funding: More than USD 1.2 Billion in cumulative infrastructure sensing investments supports partnerships, localization, and capacity expansion initiatives.

Innovation & Future Outlook: Next-generation distributed sensing platforms and edge analytics are reducing monitoring latency by up to 35%, strengthening operational intelligence.

Fibre optic sensors are increasingly deployed across power transmission, oil & gas pipelines, transportation networks, and industrial facilities where continuous real-time monitoring is critical. Recent innovations in distributed acoustic sensing, AI-enabled signal interpretation, and high-density photonic networks have improved detection accuracy by over 25%. Growing infrastructure resilience requirements and stricter asset integrity standards are accelerating adoption, particularly as operators prioritize predictive maintenance and operational continuity, setting the stage for broader strategic transformation.

Fibre optic sensors are becoming strategically important as governments, utilities, transportation operators, and industrial enterprises prioritize infrastructure resilience, operational visibility, and predictive asset management. Infrastructure modernization programs, grid expansion initiatives, and industrial digitalization strategies are shifting investment toward continuous monitoring technologies capable of delivering real-time intelligence. The market is increasingly benefiting from supply-chain localization efforts and national investments aimed at protecting critical infrastructure against operational disruptions.

Compared with conventional electronic sensing systems, advanced fibre optic sensing networks can reduce maintenance interventions by nearly 30% while extending monitoring coverage across hundreds of kilometers through a single deployment architecture. China continues leading large-scale infrastructure deployment, while the United States maintains an innovation advantage through aerospace, defense, and energy-sector integration. Over the next two to three years, adoption across smart utility networks and transportation corridors is expected to accelerate as operators prioritize asset uptime and predictive maintenance efficiency.

A practical example is pipeline integrity monitoring, where distributed acoustic sensing systems enable continuous leak detection and intrusion identification across extensive network assets. Companies are strengthening competitive positioning through technology partnerships, photonics R&D investments, and expansion into infrastructure modernization projects. Organizations that integrate advanced sensing, analytics, and digital asset management capabilities will secure stronger operational advantages and long-term market relevance.

Rising investment in infrastructure resilience is creating substantial demand for advanced fibre optic sensing solutions. More than 52% of newly commissioned critical infrastructure projects now incorporate continuous monitoring technologies, while utility operators report up to 30% reductions in unplanned maintenance events through real-time sensing deployment. Power transmission modernization programs, high-speed rail expansion, and offshore energy developments are increasing sensor installation density across strategic assets. Following heightened focus on energy security and infrastructure reliability, operators are prioritizing asset visibility and fault detection capabilities. In response, leading companies are expanding distributed sensing portfolios, forming engineering partnerships, and investing in AI-enabled analytics platforms. A notable strategic outcome is the transition from periodic inspections toward permanent monitoring architectures that improve operational continuity and asset lifecycle performance.

Despite strong adoption momentum, deployment economics remain a significant structural limitation. Installation expenses can account for 35–45% of total project costs, particularly in brownfield environments requiring network retrofitting. Complex integration with legacy SCADA, utility, and industrial control systems increases implementation timelines by approximately 20–25%. Dependence on specialized optical components and precision manufacturing capabilities also exposes projects to supply-chain fluctuations. In countries with limited fiber infrastructure penetration, deployment scalability remains constrained by installation complexity and workforce availability. Companies are addressing these challenges through localization strategies, long-term procurement agreements, and modular deployment architectures. A key operational insight is that lifecycle savings frequently outweigh upfront costs, yet procurement decisions continue to be heavily influenced by capital expenditure limitations.

The convergence of AI, edge computing, and distributed fibre optic sensing creates significant opportunities beyond traditional monitoring applications. Distributed acoustic sensing adoption across energy and transportation assets has improved event detection accuracy by more than 25%, while predictive maintenance programs have reduced inspection requirements by nearly 20%. India, Saudi Arabia, and Southeast Asian infrastructure corridors are emerging as high-potential deployment markets due to accelerating utility and transportation investments. Government-backed smart infrastructure initiatives and industrial digital transformation programs are encouraging wider adoption of advanced sensing ecosystems. Companies are increasing R&D investments, forming technology alliances, and integrating analytics capabilities directly into sensing platforms. An important strategic opportunity lies in transforming sensor networks from monitoring tools into decision-support systems delivering actionable operational intelligence.

Long-term market expansion depends on solving operational scalability challenges associated with massive sensor-generated datasets. Large distributed sensing deployments can generate data volumes exceeding 40% growth annually, creating processing, storage, and cybersecurity pressures for operators. Integration complexity across multi-vendor infrastructure environments can increase deployment timelines by approximately 20%, while shortages of specialized photonics and analytics professionals continue limiting project execution capacity. As critical infrastructure operators increase reliance on real-time monitoring, maintaining data integrity and network reliability becomes increasingly important. Companies are responding through cloud-enabled analytics, cybersecurity investments, workforce development programs, and strategic partnerships with technology providers. The strongest competitive advantage will belong to organizations capable of converting high-volume sensing data into reliable operational intelligence at scale.

AI-Driven Monitoring Intelligence Industrial operators are rapidly integrating AI-enabled analytics with fibre optic sensing networks to enhance asset visibility and automate decision-making. Distributed acoustic sensing deployments have improved event detection accuracy by nearly 28%, while automated anomaly classification has reduced manual data interpretation requirements by approximately 25%. Energy utilities and transportation operators are restructuring monitoring workflows around predictive maintenance rather than periodic inspection cycles. This shift is reducing downtime, accelerating fault response, and improving operational continuity. Companies are scaling cloud-based analytics platforms, expanding software partnerships, and embedding machine learning capabilities directly into sensing architectures to create intelligent monitoring ecosystems.

Grid Modernization Deployment Surge Power transmission upgrades are driving large-scale deployment of fibre optic sensors across critical electricity networks. More than 55% of new high-voltage transmission projects now include real-time monitoring infrastructure, while fault localization times have declined by nearly 35%. Rising electricity demand, renewable integration, and grid resilience requirements are accelerating deployment across China, India, and the United States. Utilities are prioritizing continuous asset monitoring to improve network reliability and reduce maintenance costs. In response, manufacturers are expanding production capacity, strengthening utility partnerships, and developing specialized sensing solutions optimized for long-distance transmission corridors.

Photonic Miniaturization Advances Sensor manufacturers are accelerating photonic integration strategies that reduce hardware footprints while increasing sensing density. Compact sensing modules have lowered installation complexity by approximately 18% and improved deployment flexibility by nearly 22% across industrial facilities. The transition toward miniaturized optical components is enabling broader implementation within manufacturing plants, offshore platforms, and transportation systems. A less obvious benefit is reduced calibration frequency, which improves lifecycle efficiency. Companies are investing in advanced photonic packaging, automated production processes, and next-generation integrated sensing platforms to improve performance consistency.

Supply Chain Localization Strategies Growing infrastructure security priorities and component availability concerns are reshaping procurement and manufacturing practices throughout the fibre optic sensor ecosystem. Regional sourcing of critical optical components has increased by nearly 25%, while average procurement lead times have fallen by approximately 15%. Enterprises are diversifying supplier networks to reduce operational exposure and improve production predictability. Strategic localization initiatives in China, India, Germany, and the United States are strengthening manufacturing resilience and shortening delivery cycles. Companies are responding through regional assembly investments, long-term supplier agreements, and vertically integrated production models that improve operational control and deployment speed.

Distributed Fibre Optic Sensors represent the leading segment, accounting for approximately 48% of total market deployment due to their ability to provide continuous monitoring across long distances with a single sensing architecture. Their scalability, broad coverage capability, and suitability for pipelines, railways, power transmission assets, and perimeter security applications make them the preferred choice for infrastructure operators. Point Fibre Optic Sensors continue to maintain strong adoption in aerospace, industrial automation, and precision manufacturing environments where localized measurement accuracy is critical. Companies are increasing investments in distributed acoustic sensing and distributed temperature sensing platforms to strengthen monitoring efficiency across large-scale assets. Extrinsic Fibre Optic Sensors are emerging as the fastest-growing category, supported by rising adoption in harsh industrial environments where remote measurement capabilities offer operational advantages. Intrinsic Fibre Optic Sensors remain strategically important for structural health monitoring and defense applications requiring high sensitivity and electromagnetic immunity. Approximately 60% of new infrastructure monitoring deployments now favor distributed sensing architectures, while advanced extrinsic solutions have improved measurement reliability by nearly 20% in high-temperature operating environments. Manufacturers are expanding product portfolios, strengthening photonics R&D capabilities, and prioritizing integrated sensing platforms to address evolving infrastructure and industrial monitoring requirements.

Infrastructure Monitoring holds the largest market share, representing nearly 35% of total application demand due to extensive deployment across bridges, tunnels, rail networks, pipelines, and power transmission corridors. Asset owners increasingly rely on continuous structural health monitoring systems to improve reliability and reduce inspection requirements. Oil & Gas remains a significant application segment where fibre optic sensors support leak detection, intrusion monitoring, and wellbore surveillance. Approximately 52% of newly commissioned critical infrastructure projects now incorporate permanent fibre-based sensing systems, reflecting the shift toward predictive asset management strategies. Energy & Utilities is emerging as the fastest-growing application segment as grid modernization initiatives and renewable energy integration increase demand for real-time monitoring. Aerospace & Defense continues to benefit from the technology's immunity to electromagnetic interference and lightweight characteristics. Industrial Process Monitoring is also gaining traction as manufacturers adopt advanced sensing systems to improve operational efficiency and equipment reliability. Companies are expanding deployment partnerships, integrating AI-enabled analytics, and developing application-specific sensing platforms. Demand is increasingly shifting toward continuous monitoring environments where operational visibility and asset integrity directly influence performance outcomes.

Utilities and Energy companies represent the dominant end-user group, accounting for approximately 38% of total market demand due to extensive deployment across transmission networks, substations, pipelines, and renewable energy facilities. Their reliance on real-time monitoring, asset protection, and predictive maintenance creates sustained demand for advanced fibre optic sensing technologies. Transportation operators remain major adopters as railway modernization and smart infrastructure initiatives expand monitoring requirements. More than 50% of newly upgraded transmission infrastructure projects now include continuous fibre optic monitoring systems to improve network reliability and fault detection efficiency. Industrial Manufacturing is the fastest-growing end-user segment as factories accelerate automation initiatives and digital asset management strategies. Aerospace & Defense organizations continue investing in precision sensing applications where environmental resilience and measurement accuracy are critical. Government and Public Infrastructure agencies are also increasing deployment activity to support infrastructure resilience and security objectives. Companies are targeting these segments through customized monitoring platforms, strategic partnerships, service-based deployment models, and integrated analytics capabilities. Approximately 30% of large industrial facilities have expanded continuous monitoring investments during the past two years, highlighting the growing operational importance of advanced sensing technologies.

Asia-Pacific accounted for the largest market share at 41.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2026 and 2033.

North America represents approximately 27.8% of global market activity, supported by widespread deployment across power transmission networks, oil & gas pipelines, transportation infrastructure, and defense applications. The region maintains a strong position due to advanced industrial automation adoption and extensive utilization of predictive maintenance technologies. Utilities and energy operators are increasingly integrating distributed acoustic sensing and distributed temperature sensing systems into critical assets. More than 55% of newly upgraded transmission projects incorporate continuous monitoring capabilities, strengthening operational reliability. Enterprise investment remains concentrated in infrastructure resilience, cybersecurity-integrated sensing platforms, and AI-enabled asset intelligence solutions, reinforcing the region's leadership in high-value sensing deployments.

United States Market Outlook: The United States remains the largest market within North America due to its extensive energy infrastructure, advanced aerospace sector, and ongoing grid modernization initiatives. Large-scale deployment across pipeline integrity monitoring and transmission networks continues to accelerate adoption. Approximately 60% of regional fibre optic sensing deployments are concentrated in the U.S., supported by substantial investment in utility modernization and defense infrastructure. Technology developers are expanding partnerships with energy operators and transportation agencies to integrate real-time sensing with predictive analytics platforms.

Europe accounts for nearly 24.3% of global demand, supported by industrial automation investments, transportation modernization programs, and increasing emphasis on infrastructure sustainability. The region demonstrates strong adoption across railway networks, manufacturing facilities, offshore wind installations, and civil infrastructure monitoring applications. Advanced sensing technologies are being incorporated into strategic infrastructure projects to improve lifecycle management and operational efficiency. More than 45% of major rail infrastructure upgrades now include continuous structural monitoring systems. Market participants are focusing on smart infrastructure integration, photonics innovation, and long-term operational efficiency improvements to strengthen competitive positioning.

Germany Market Outlook: Germany serves as the region's technology and industrial hub, benefiting from its advanced manufacturing ecosystem and strong photonics expertise. Industrial operators are increasingly deploying fibre optic sensors across automated production facilities and transportation infrastructure. Nearly 30% of European industrial sensing installations are concentrated in Germany, reflecting the country's leadership in Industry 4.0 implementation. Strong engineering capabilities, infrastructure modernization initiatives, and manufacturing digitization programs continue to support sustained deployment activity across multiple end-use sectors.

Asia-Pacific leads the global market with approximately 41.2% share, driven by extensive infrastructure construction, utility modernization programs, industrial expansion, and strong manufacturing capabilities. The region hosts significant deployment activity across rail networks, smart cities, power transmission corridors, and industrial automation facilities. High investment levels in critical infrastructure and digital transformation initiatives continue to expand sensing adoption. More than 50% of newly commissioned large-scale transportation and energy projects across major economies incorporate advanced monitoring technologies. Manufacturers are scaling production capacity, strengthening regional supply chains, and investing in photonic innovation to meet growing enterprise demand.

China Market Outlook: China remains the most influential country market due to its extensive infrastructure footprint, advanced manufacturing ecosystem, and large-scale utility modernization initiatives. High-speed rail systems, power transmission projects, and industrial facilities continue driving deployment volumes. The country accounts for roughly 31% of global fibre optic sensor installation activity, supported by strong domestic manufacturing capacity and substantial infrastructure investment. Technology providers are expanding integrated sensing solutions to support smart infrastructure management and industrial digitalization objectives across strategic sectors.

South America represents approximately 4.5% of global market participation, with demand concentrated in oil & gas operations, mining activities, utility infrastructure, and transportation modernization projects. Infrastructure monitoring requirements and operational efficiency initiatives are encouraging adoption across critical industrial assets. Energy operators are increasingly implementing real-time monitoring technologies to improve asset integrity and reduce maintenance-related disruptions. Pipeline monitoring deployments have expanded by nearly 18% over recent years as operators strengthen risk management strategies. While infrastructure investment remains uneven across countries, growing industrial digitalization efforts continue supporting market development.

Brazil Market Outlook: Brazil dominates regional demand due to its large energy sector, extensive pipeline infrastructure, and expanding industrial base. Fibre optic sensors are increasingly deployed across offshore energy assets, power transmission systems, and mining operations to improve operational visibility. More than 45% of South American deployment activity is concentrated in Brazil, supported by infrastructure modernization and energy sector investment. Companies are strengthening local partnerships and technical service capabilities to support increasingly sophisticated monitoring requirements across industrial sectors.

Middle East & Africa accounts for approximately 2.2% of global market activity, supported by infrastructure modernization programs, energy-sector investments, and large-scale industrial development projects. Demand is increasingly concentrated in pipeline monitoring, utility infrastructure, transportation corridors, and smart city initiatives. Governments and industrial operators are prioritizing advanced monitoring technologies to improve asset reliability and operational efficiency. Deployment of intelligent monitoring systems across strategic infrastructure assets has increased by nearly 20% in recent years. Companies are expanding regional partnerships and investing in localized technical support capabilities to strengthen long-term market presence.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant market in the region due to extensive energy infrastructure, industrial diversification initiatives, and large-scale smart infrastructure investments. Fibre optic sensing technologies are increasingly integrated into pipeline networks, utility systems, and industrial facilities to support operational reliability and digital transformation objectives. Approximately one-third of regional infrastructure monitoring investments are concentrated in the country. Continued focus on industrial modernization, infrastructure resilience, and advanced technology adoption positions Saudi Arabia as a key deployment center for next-generation sensing solutions.

The Fibre Optic Sensors Market is characterized by competition between technology leaders such as Luna Innovations, Yokogawa Electric Corporation, HBM FiberSensing, Omnisens, Bandweaver, and FISO Technologies, alongside regional sensing specialists and cost-focused component suppliers. The top five players collectively control approximately 42–46% of market activity, creating a moderately consolidated structure. Global leaders compete through sensing accuracy, distributed monitoring capabilities, software integration, and project execution expertise, while regional suppliers compete on customization and deployment costs. Performance improvements of 20–30% in distributed sensing accuracy and 15–25% reductions in maintenance interventions increasingly influence purchasing decisions. Companies are expanding through infrastructure partnerships, photonics innovation, software analytics integration, and selective acquisitions. The competitive shift is moving from standalone hardware toward integrated sensing ecosystems combining analytics, monitoring platforms, and lifecycle services. High certification requirements, engineering expertise, and critical-infrastructure references create substantial entry barriers. Winning requires superior sensing intelligence, scalable deployment capability, and strong customer integration expertise.

Yokogawa Electric Corporation

Omnisens SA

Bandweaver Technologies

FISO Technologies Inc.

OFS Fitel LLC

Weatherford International plc

AP Sensing GmbH

Sensornet Ltd.

Smart Fibres Ltd.

FBGS Technologies GmbH

Proximion AB

Halliburton Company

The market is increasingly defined by distributed acoustic sensing (DAS), distributed temperature sensing (DTS), and fiber Bragg grating (FBG) technologies. DAS platforms now enable monitoring across distances exceeding 100 km from a single sensing point, while advanced FBG systems improve measurement precision by nearly 20% compared with earlier-generation optical sensing architectures. Approximately 55% of newly deployed infrastructure monitoring systems now utilize distributed sensing technologies due to their ability to provide continuous operational visibility. Utilities, transportation operators, and energy companies benefit through faster fault detection and lower inspection requirements.

Emerging technology development is centered on AI-integrated sensing analytics, edge processing, and photonic miniaturization. Automated event classification systems have improved anomaly identification accuracy by approximately 25%, while edge-enabled monitoring platforms reduce data processing latency by nearly 30%. Compared with conventional electronic sensors, advanced fibre optic systems can lower maintenance interventions by roughly 25% while providing broader coverage. Infrastructure operators and industrial enterprises gain the greatest competitive advantage through improved asset utilization and predictive maintenance performance.

Between 2026 and 2028, multi-parameter sensing platforms capable of simultaneously measuring temperature, strain, vibration, and acoustic activity are expected to become mainstream. Adoption across critical infrastructure environments is projected to exceed 60% of new deployments. Companies investing now in integrated sensing ecosystems, analytics platforms, and photonic innovation will secure stronger operational intelligence, enhanced infrastructure resilience, and long-term competitive differentiation.

December 2024 – Yokogawa Electric Corporation launched OpreX Subsea Power Cable Monitoring for offshore wind applications, integrating fibre optic temperature sensing for continuous cable integrity management. The solution supports condition-based maintenance and early fault detection across subsea power infrastructure, strengthening renewable energy asset reliability. Source: www.yokogawa.com

January 2025 – Luna Innovations Incorporated announced expanded commercialization initiatives for its distributed fibre optic sensing portfolio following integration of acquired sensing technologies. The company strengthened deployment capabilities across infrastructure and energy monitoring applications, expanding its global sensing footprint and project execution capacity.

May 2025 – Luna Innovations Incorporated reported substantial bookings growth, with quarterly bookings increasing by approximately 8% year-over-year. Strong demand from energy, utility, and infrastructure monitoring applications reinforced investment momentum in advanced fibre optic sensing platforms and supported expansion of sensing operations.

September 2025 – Luna Innovations Incorporated highlighted growing global deployment of its ATLAS Acoustic Sensing Platform, supporting infrastructure, utility, and energy monitoring projects. The company reported a 24% increase in quarterly revenue, reflecting expanding adoption of advanced distributed sensing technologies across critical asset monitoring environments.

The report provides a comprehensive assessment of the global Fibre Optic Sensors Market across major sensing technologies, applications, end-user industries, and regional markets. Coverage includes distributed, intrinsic, extrinsic, and point sensing technologies deployed across infrastructure monitoring, energy systems, industrial automation, transportation networks, aerospace, defense, and utility applications. More than 50% of analyzed deployments are concentrated within infrastructure and energy monitoring environments, reflecting the market’s operational focus on asset integrity and predictive maintenance.

The study evaluates competitive positioning, technology adoption patterns, deployment trends, and strategic investment priorities across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It examines emerging opportunities in AI-enabled sensing analytics, distributed monitoring platforms, photonic integration, and multi-parameter sensing systems. The report supports investment planning, market entry evaluation, expansion strategies, partnership development, and competitive benchmarking by identifying evolving demand patterns, technology shifts, and operational priorities expected to shape industry direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 537.0 Million |

| Market Revenue (2033) | USD 1,093.8 Million |

| CAGR (2026–2033) | 9.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Luna Innovations Incorporated; Yokogawa Electric Corporation; HBM FiberSensing S.A.; Omnisens SA; Bandweaver Technologies; FISO Technologies Inc.; OFS Fitel LLC; Weatherford International plc; AP Sensing GmbH; Sensornet Ltd.; Smart Fibres Ltd.; FBGS Technologies GmbH; Proximion AB; Halliburton Company |

| Customization & Pricing | Available on Request (10% Customization Free) |