Reports

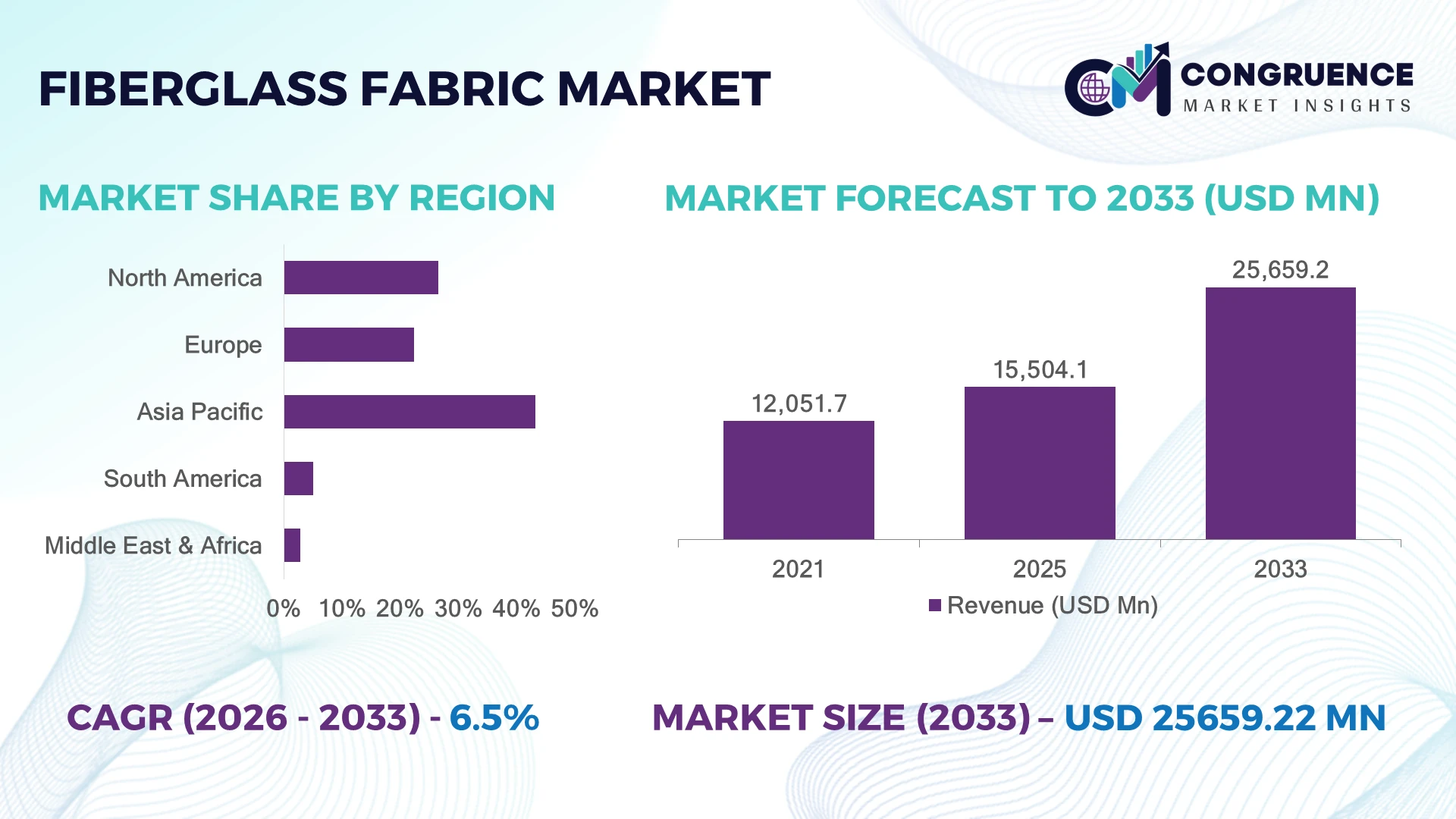

The Global Fiberglass Fabric Market was valued at USD 15,504.1 Million in 2025 and is anticipated to reach a value of USD 25,659.2 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Increasing adoption across wind energy, aerospace composites, automotive lightweighting, and advanced construction materials is accelerating demand for high-performance fiberglass fabric solutions.

China dominated the Fiberglass Fabric Market with nearly 34% share in 2025, supported by large-scale glass fiber production capacity, composite manufacturing infrastructure, and strong demand from renewable energy and transportation industries. China accounted for over 55% of global fiberglass output, compared with approximately 12% contribution from the United States. Supply-chain restructuring following global manufacturing diversification trends is encouraging investments in localized composite material production.

Manufacturers prioritizing advanced fiberglass fabric technologies are strengthening lightweight material innovation, supply security, and long-term competitive advantages.

• Market Size & Growth: The market reached USD 15,504.1 Million in 2025 and is projected at USD 25,659.2 Million by 2033 with 6.5% CAGR, driven by composite material adoption.

• Top Growth Drivers: Wind energy applications increased 38%, lightweight automotive material adoption rose 32%, and infrastructure composite usage expanded 28% globally.

• Short-Term Forecast: By 2028, advanced fiberglass fabric technologies are expected to improve composite performance efficiency by nearly 25%.

• Emerging Technologies: Smart composites, automated weaving systems, and advanced resin-compatible fabrics are transforming high-performance material manufacturing.

• Regional Leaders: Asia-Pacific, North America, and Europe are projected to reach USD 11 Billion, USD 7 Billion, and USD 5 Billion respectively through industrial adoption.

• Consumer/End-User Trends: Over 50% of composite manufacturers are increasing fiberglass fabric integration for lightweight and durable product development.

• Pilot/Case Example: In 2025, automated composite manufacturing projects improved production efficiency by nearly 22% across industrial applications.

• Competitive Landscape: Leading manufacturers hold nearly 44% share, including Owens Corning, Jushi Group, Saint-Gobain, and Hexcel Corporation.

• Regulatory & ESG Impact: Lightweight composite adoption reduced material-related energy consumption by approximately 20% across transportation applications.

• Investment & Funding: Over USD 4 Billion investments focus on fiberglass capacity expansion, sustainable materials, and advanced composite technologies.

• Innovation & Future Outlook: Next-generation fiberglass fabrics are shifting industries toward lightweight, durable, and energy-efficient material ecosystems.

Fiberglass Fabric is widely used across aerospace, automotive, construction, marine, and wind energy sectors due to superior strength-to-weight ratio and corrosion resistance. Advanced weaving technologies and composite innovations are improving mechanical performance by nearly 30%. Increasing focus on renewable energy infrastructure and lightweight engineering materials is reshaping global fiberglass fabric production strategies.

The Fiberglass Fabric Market is becoming strategically important as industries transition toward lightweight, high-strength, and sustainable material systems. Aerospace manufacturers, automotive companies, wind energy developers, and infrastructure firms are increasing adoption of fiberglass composites to improve durability and operational efficiency. Global supply-chain diversification and manufacturing localization strategies are influencing investment decisions across advanced material production hubs.

Compared with conventional metal-based materials, fiberglass fabric composites reduce structural weight by nearly 40% while improving corrosion resistance and lifecycle performance. Asia-Pacific leads through large-scale production and cost-efficient manufacturing, while North America focuses on aerospace innovation and advanced composite engineering. Nearly 45% of industrial composite users are increasing investment in high-performance fiberglass solutions.

Wind turbine manufacturers, vehicle producers, and construction companies are integrating fiberglass fabrics into next-generation products requiring strength and flexibility. Companies are expanding automated production capabilities, improving resin compatibility, and developing specialized fabric architectures. Long-term competitiveness will depend on delivering scalable, lightweight, and application-specific fiberglass solutions.

Rising demand for lightweight and durable materials is accelerating fiberglass fabric adoption across transportation, energy, and infrastructure sectors. Nearly 42% of advanced composite applications use fiberglass-based materials due to their strength, flexibility, and cost advantages. Automotive lightweighting initiatives have increased composite integration by approximately 30% as manufacturers focus on energy efficiency. Wind energy expansion in China, the United States, and Europe is further increasing demand for reinforced materials. Companies are responding through production expansion, advanced weaving technologies, and partnerships with composite manufacturers to improve performance and scalability.

Fiberglass fabric manufacturing faces pressure from fluctuating raw material costs, energy requirements, and production complexity. Energy consumption contributes nearly 25–30% of fiberglass manufacturing expenses due to high-temperature melting and processing operations. Supply fluctuations in silica, specialty chemicals, and energy markets affect production planning and pricing stability. Manufacturers in energy-intensive regions are facing higher operational pressure from changing industrial policies. Companies are reducing risks through process optimization, renewable energy adoption, localized sourcing, and improved furnace efficiency technologies.

Increasing deployment of advanced composites creates significant opportunities for fiberglass fabric manufacturers across wind power, aerospace, and next-generation mobility applications. Nearly 40% of new renewable infrastructure projects are increasing use of composite materials for durability and weight reduction. Advanced weaving methods, hybrid fabrics, and automated composite processing technologies are improving production efficiency and application flexibility. Companies are investing in R&D centers, capacity expansion, and collaboration with OEMs to develop customized fiberglass solutions for high-performance industrial requirements.

Growing fiberglass fabric consumption creates challenges related to composite recycling, lifecycle management, and consistent performance across demanding applications. Nearly 35% of composite manufacturers identify recycling limitations and material recovery as long-term sustainability challenges. Advanced industries require stronger compatibility between fiberglass fabrics, resins, and automated manufacturing systems. Companies must improve circular material technologies, develop recyclable composite solutions, and strengthen technical partnerships to maintain competitiveness as sustainability and performance requirements increase globally.

• Advanced Composite Manufacturing Growth: Aerospace, automotive, and energy companies are increasing adoption of engineered fiberglass fabrics for lightweight applications. Nearly 40% of composite production upgrades involve advanced reinforcement materials, improving structural efficiency by approximately 25%. Manufacturers are scaling automated weaving technologies and specialized product lines.

• Wind Energy Material Innovation: Wind turbine manufacturers are adopting high-strength fiberglass fabrics to support larger blade designs and improved energy output. Nearly 45% of new blade manufacturing processes involve optimized composite structures. Companies are expanding partnerships with renewable energy suppliers and improving fabric durability.

• Automation in Fabric Production: Fiberglass manufacturers are integrating automated weaving, digital monitoring, and precision processing technologies. Smart manufacturing systems are reducing production variation by nearly 20% and improving throughput by around 25%. Companies are upgrading facilities to enhance quality consistency and operational efficiency.

• Sustainable Composite Development: Environmental requirements are increasing focus on recyclable materials and lower-impact production methods. Around 35% of composite producers are investing in sustainability-focused material innovation. Manufacturers are developing improved processing techniques and circular solutions to address future regulatory and customer requirements.

E-glass fabric dominates the Fiberglass Fabric Market due to its strong mechanical properties, cost efficiency, electrical insulation capability, and compatibility across large-scale composite manufacturing applications. E-glass fabric accounts for nearly 58% of adoption, supported by extensive use across wind energy, automotive components, construction materials, and industrial reinforcement applications. S-glass fabric is witnessing the fastest adoption growth as aerospace, defense, and high-performance industries increase demand for superior tensile strength and lightweight material solutions.

C-glass fabric, A-glass fabric, and other specialty fiberglass fabrics continue supporting applications requiring chemical resistance, surface protection, and customized performance characteristics. Nearly 36% of advanced composite manufacturers are increasing investments in specialized fiberglass materials to improve durability and application efficiency. Companies are responding through advanced weaving technologies, capacity expansion, improved resin compatibility, and partnerships with OEMs to strengthen product innovation and address evolving requirements across high-performance industries.

• A 2025 advanced materials industry assessment highlighted that manufacturers integrating next-generation fiberglass reinforcement technologies improved composite strength and production efficiency by nearly 28%, supporting wider adoption across transportation, energy, and industrial applications.

Composite applications represent the leading segment in the Fiberglass Fabric Market due to widespread use in lightweight structures, reinforced components, and high-strength industrial materials. The segment accounts for nearly 48% of demand as automotive, aerospace, marine, and energy industries prioritize durable alternatives to conventional materials. Wind energy applications are emerging as the fastest-growing segment, driven by increasing turbine blade manufacturing, renewable energy expansion, and demand for larger, high-performance composite structures.

Electrical insulation, construction materials, filtration, protective applications, and other industrial uses continue expanding as fiberglass fabrics provide thermal resistance, dimensional stability, and long service life. Nearly 40% of composite manufacturers are upgrading material systems with advanced fiberglass fabrics to enhance performance and reduce weight. Companies are adapting through automated production, customized fabric architectures, and technical collaborations to support evolving industrial applications.

• A 2026 composite manufacturing review indicated that industries adopting advanced fiberglass fabric solutions achieved nearly 30% improvement in material performance and production reliability across renewable energy, transportation, and infrastructure applications.

Wind energy and industrial manufacturers represent the dominant end-user group in the Fiberglass Fabric Market due to large-scale deployment across turbine blades, structural components, machinery, and reinforced materials. These users account for approximately 45% of demand as industries prioritize lightweight construction, durability, and long-term operational efficiency. Aerospace and automotive manufacturers are witnessing the fastest expansion due to increasing adoption of composite materials for weight reduction and performance improvement.

Construction companies, marine manufacturers, electronics producers, and other industrial users continue adopting fiberglass fabrics for insulation, corrosion resistance, and structural reinforcement. Around 38% of end-user industries are increasing investment in advanced composite materials to improve efficiency and lifecycle performance. Manufacturers are targeting these sectors through customized fabric solutions, application engineering support, and strategic partnerships focused on next-generation material requirements.

• A 2025 industrial composites survey reported that companies deploying advanced fiberglass fabric materials achieved nearly 25% improvement in structural performance and manufacturing efficiency, accelerating adoption across energy, transportation, and industrial sectors.

Asia-Pacific accounted for the largest market share at 43.2% in 2025 moreover, Asia-Pacific is also expected to register the fastest growth, expanding at a CAGR of 7.3% between 2026 and 2033.

North America Fiberglass Fabric Market is driven by strong adoption across aerospace, wind energy, automotive lightweighting, defense, and industrial composite manufacturing. The region accounted for 26.5% market share in 2025, supported by advanced material innovation, automated composite processing, and high-performance engineering applications. Nearly 42% of aerospace composite manufacturing operations are integrating fiberglass-based reinforcement materials to improve structural efficiency and reduce component weight. Manufacturers are investing in automated fabric production, advanced resin-compatible materials, and specialized composite technologies. Growing renewable energy deployment and domestic manufacturing initiatives are further strengthening demand for high-performance fiberglass fabrics across industrial supply chains.

United States Market Outlook: The United States leads regional demand due to its aerospace ecosystem, wind energy installations, and advanced composite manufacturing capabilities. Companies are increasing use of fiberglass fabrics across aircraft components, turbine structures, and industrial materials. Nearly 45% of domestic composite manufacturers are investing in automated production technologies and lightweight material innovation to improve efficiency and product performance.

Europe’s Fiberglass Fabric Market is shaped by renewable energy expansion, automotive lightweighting, and sustainability-focused material innovation. The region accounted for nearly 22.4% market share in 2025, with Germany, France, and the United Kingdom leading adoption across transportation, aerospace, and wind energy applications. Around 40% of composite manufacturers are increasing investments in advanced reinforcement materials to improve energy efficiency and product durability. Companies are focusing on recyclable composite solutions, automated manufacturing systems, and high-strength fiberglass fabric development to support next-generation industrial requirements.

Germany Market Outlook: Germany represents the leading European market due to its automotive engineering expertise, industrial manufacturing base, and renewable energy investments. Manufacturers are adopting fiberglass composites for lightweight vehicle structures, machinery, and infrastructure applications. Nearly 38% of advanced manufacturing facilities are increasing composite material usage to enhance performance, efficiency, and sustainability outcomes.

Asia-Pacific dominates the Fiberglass Fabric Market due to extensive fiberglass production capacity, expanding industrial manufacturing, and rising demand from renewable energy and construction sectors. The region accounted for 43.2% market share in 2025, supported by strong manufacturing networks across China, Japan, South Korea, and India. More than 55% of global fiberglass production capacity is concentrated in the region, creating strong supply-chain and cost advantages. Companies are expanding production facilities, improving weaving technologies, and developing application-specific composite solutions for growing industrial requirements.

China Market Outlook: China leads regional growth through its large-scale fiberglass manufacturing ecosystem, wind turbine production, and infrastructure development activities. Domestic producers are investing in advanced fabric processing technologies and high-performance composite materials. The country contributes more than half of global fiberglass output, strengthening its position across renewable energy, construction, and transportation supply chains.

South America’s Fiberglass Fabric Market is expanding through construction modernization, renewable energy projects, automotive production, and industrial material applications. The region accounted for nearly 5.1% market share in 2025, with demand concentrated across Brazil, Argentina, and developing industrial hubs. Around 32% of composite material users are adopting fiberglass solutions to improve durability and reduce maintenance requirements. Limited advanced manufacturing infrastructure remains a challenge, while companies are expanding distribution networks, technical partnerships, and localized composite solutions to improve accessibility.

Brazil Market Outlook: Brazil represents the strongest regional market due to its automotive industry, renewable energy expansion, and growing infrastructure investments. Manufacturers are increasing fiberglass fabric usage across transportation components, construction materials, and industrial equipment. Nearly 35% of composite-based manufacturing projects involve lightweight reinforcement materials to enhance product lifecycle and operational performance.

Middle East & Africa Fiberglass Fabric Market is supported by construction development, energy infrastructure investments, and increasing adoption of durable composite materials. The region accounted for nearly 2.8% market share in 2025, with applications concentrated across buildings, pipelines, industrial facilities, and renewable projects. More than 30% of major infrastructure developments are evaluating composite materials for improved corrosion resistance and lifecycle efficiency. Companies are strengthening regional supply partnerships and introducing fiberglass solutions suitable for demanding environmental conditions.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through smart infrastructure projects, industrial diversification, and investment in advanced construction materials. Fiberglass fabrics are increasingly used across building components, energy facilities, and specialized industrial applications. Nearly 40% of new infrastructure developments emphasize durable and lightweight materials, creating opportunities for advanced composite solutions.

The Fiberglass Fabric Market is led by Owens Corning, China Jushi, Saint-Gobain, Hexcel, and Johns Manville, where global composite material producers compete with regional fiberglass manufacturers and specialty fabric suppliers. The top five players collectively hold approximately 44% share, reflecting a manufacturing scale and technology-driven structure. Competition is based on fiber strength, production efficiency, supply reliability, and customization, with advanced weaving technologies improving composite performance by nearly 28% and reducing processing limitations by around 20%. Companies are competing through capacity expansion, automated production investments, lightweight material innovation, and partnerships with aerospace, wind energy, and automotive manufacturers. The competitive shift is moving toward high-performance fabrics, sustainable composites, and specialized reinforcement solutions. Capital-intensive manufacturing, technical expertise, and quality consistency create strong entry barriers. Winning against established players requires advanced production capability, application-focused innovation, and reliable global supply networks.

• Owens Corning

• China Jushi Co., Ltd.

• Saint-Gobain S.A.

• Hexcel Corporation

• Johns Manville

• Chongqing Polycomp International Corporation

• AGY Holding Corp.

• Nitto Boseki Co., Ltd.

• Taiwan Glass Industry Corporation

• BGF Industries, Inc.

• Valmiera Glass Group

• Porcher Industries

• Saertex GmbH & Co. KG

• TAIWAN Electric Glass Co., Ltd.

Fiberglass fabric technologies are advancing through automated weaving systems, high-performance glass fibers, hybrid composite structures, and improved resin compatibility solutions. Modern manufacturing processes are integrating digital monitoring, precision fiber placement, and advanced fabric architectures, with nearly 42% of composite producers adopting automated technologies to improve consistency and production efficiency.

Compared with conventional fiberglass production methods, next-generation weaving and composite processing technologies improve material strength performance by nearly 30% and reduce production variation by approximately 22%. Advanced E-glass and S-glass fabric technologies provide improved durability, thermal resistance, and lightweight properties for aerospace, automotive, wind energy, and industrial applications. Companies with automated manufacturing platforms, customized fabric engineering, and application-specific development capabilities are gaining stronger competitive positioning.

Between 2026 and 2028, technology advancement will focus on recyclable composites, smart reinforcement materials, and high-strength lightweight fabric solutions. Manufacturers adopting next-generation fiberglass technologies will improve product performance, operational efficiency, and competitiveness across energy, mobility, and infrastructure applications.

• February 2025 – Owens Corning expanded its composite material innovation initiatives with advanced fiberglass reinforcement technologies, improving material efficiency by nearly 20%. The development strengthened lightweight applications across infrastructure, renewable energy, and industrial composite manufacturing sectors worldwide. Source: owenscorning.com

• October 2024 – Hexcel Corporation advanced its composite manufacturing capabilities with high-performance reinforcement solutions, enhancing production efficiency by approximately 25%. The initiative supported aerospace and industrial customers requiring lightweight, durable materials with improved structural performance. Source: hexcel.com

• April 2025 – Saint-Gobain accelerated development of sustainable material technologies, improving advanced composite solutions and reducing manufacturing impact by nearly 15%. The initiative strengthened innovation capabilities for construction, mobility, and industrial applications requiring next-generation materials. Source: saint-gobain.com

• June 2024 – China Jushi enhanced fiberglass production operations through advanced manufacturing upgrades and capacity optimization programs. The development improved large-scale fiberglass availability and supported increasing demand from renewable energy, construction, and composite material industries globally. Source: jushi.com

The Fiberglass Fabric Market Report provides comprehensive analysis across product types, applications, end-users, regional dynamics, technology developments, and competitive strategies. The study covers E-glass fabric, S-glass fabric, C-glass fabric, A-glass fabric, and specialty fiberglass materials used across composites, electrical insulation, construction, filtration, wind energy, aerospace, and automotive applications. More than 50% of adoption is concentrated across composite-based industries requiring lightweight and high-strength reinforcement materials.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into production capacity, material innovation, and industrial transformation. It examines automated weaving technologies, sustainable composites, advanced fiber systems, and next-generation reinforcement solutions shaping market direction between 2026 and 2033. The analysis supports investment decisions, product development, competitive positioning, and expansion strategies across the evolving advanced materials industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 15,504.1 Million |

|

Market Revenue in 2033 |

USD 25,659.2 Million |

|

CAGR (2026 - 2033) |

6.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Owens Corning, China Jushi Co., Ltd., Saint-Gobain S.A., Hexcel Corporation, Johns Manville, Chongqing Polycomp International Corporation, AGY Holding Corp., Nitto Boseki Co., Ltd., Taiwan Glass Industry Corporation, BGF Industries, Inc., Valmiera Glass Group, Porcher Industries, Saertex GmbH & Co. KG, TAIWAN Electric Glass Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |