Reports

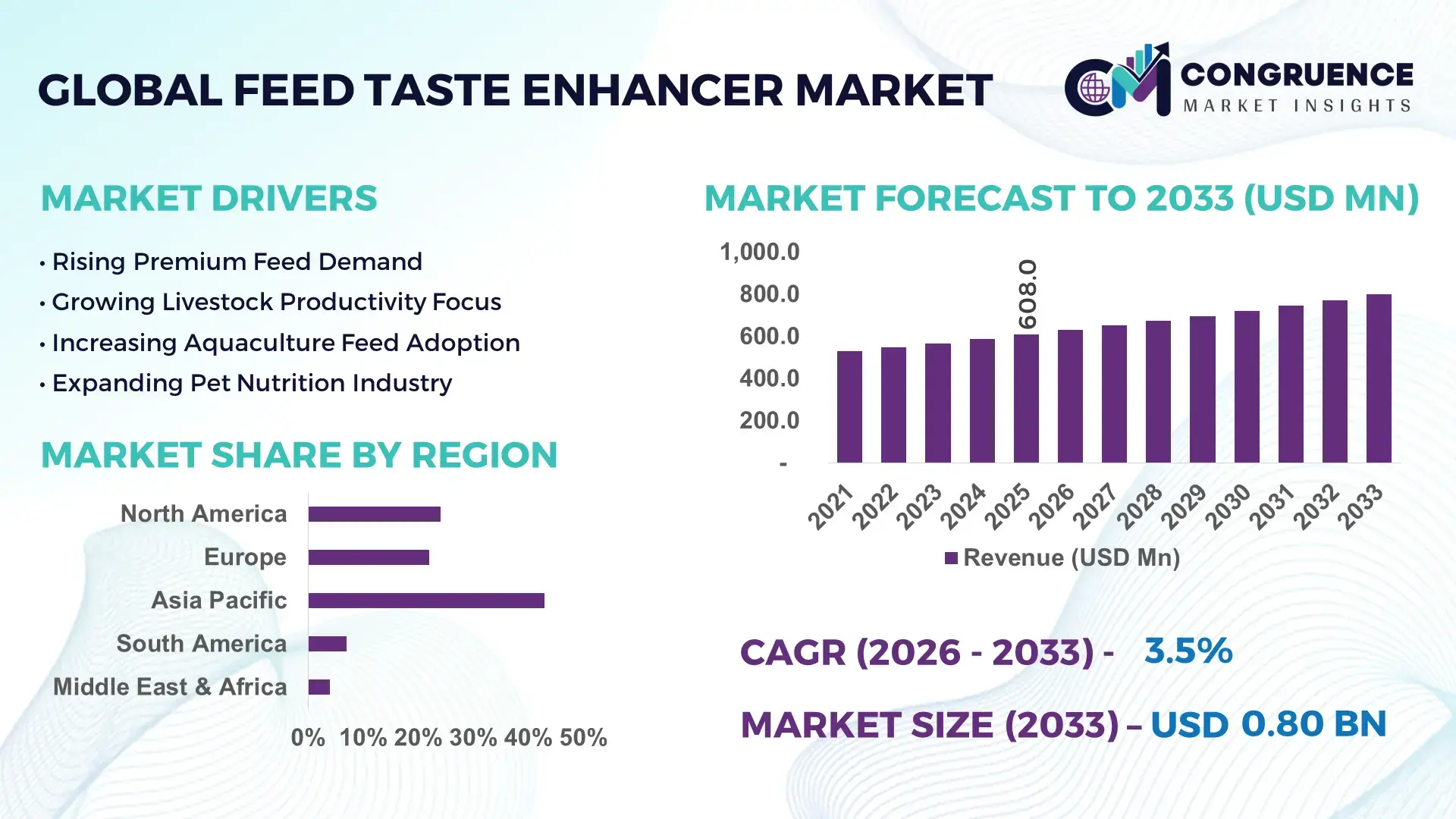

The Global Feed Taste Enhancer Market was valued at USD 608.0 Million in 2025 and is anticipated to reach a value of USD 799.4 Million by 2033 expanding at a CAGR of 3.48% between 2026 and 2033. Rapid intensification in commercial livestock production, combined with rising feed conversion optimization targets, is accelerating the deployment of advanced palatability enhancers across poultry, aquaculture, and swine nutrition systems. Feed manufacturers are increasingly integrating amino acid-based flavor systems and natural sweeteners to improve intake efficiency by over 18% in high-performance animal diets, particularly in protein-stressed markets. Between 2024 and 2026, global feed supply chains experienced significant restructuring due to grain cost volatility linked to Red Sea shipping disruptions and tighter European additive regulations, forcing producers to localize sourcing and optimize feed utilization efficiency. Precision livestock farming adoption increased by nearly 22% across industrial farming clusters, strengthening demand for functional feed additives with measurable performance outcomes.

China continues to dominate the global Feed Taste Enhancer Market with approximately 31% share of global consumption volume, supported by its livestock feed production exceeding 315 million metric tons annually. The country has accelerated smart-feed integration investments across large-scale poultry and swine farms, while domestic additive manufacturers expanded fermentation-based flavor enhancer capacity by nearly 16% during 2025. Compared with mature Western markets, Chinese producers achieve faster commercialization cycles due to vertically integrated feed operations and lower production costs, enabling broader penetration of species-specific enhancer formulations.

The market is increasingly shifting toward species-targeted, efficiency-driven feed enhancement systems where companies capable of combining formulation science, regional sourcing resilience, and scalable production infrastructure are securing long-term competitive positioning.

Market Size & Growth: USD 608.0 million in 2025 reaching USD 799.4 million by 2033 at 3.48% CAGR, driven by precision livestock nutrition and feed optimization technologies.

Top Growth Drivers: Feed efficiency gains (+18%), aquaculture additive adoption (+21%), and natural ingredient preference growth (+16%) are accelerating global demand.

Short-Term Forecast: By 2028, feed intake efficiency is projected to improve by 14% while formulation waste declines by nearly 11% across commercial farms.

Emerging Technologies: AI-assisted feed formulation, encapsulated flavor systems, and fermentation-derived enhancers are improving nutrient utilization by over 17%.

Regional Leaders: Asia-Pacific leads near USD 255 million demand, Europe exceeds USD 165 million compliance-driven adoption, while North America expands automated feed integration by 19%.

Consumer/End-User Trends: More than 48% of industrial feed producers now prioritize natural palatability enhancers over synthetic formulations for livestock performance optimization.

Pilot/Case Example: In 2025, a poultry feed optimization project in Southeast Asia improved feed conversion ratios by 13% using amino acid-based enhancers.

Competitive Landscape: The top five companies collectively control nearly 42% market share, including DSM-Firmenich, Adisseo, Kemin, Novus International, and Kerry Group.

Regulatory & ESG Impact: European clean-label feed regulations reduced synthetic additive dependence by 15%, accelerating demand for plant-derived enhancer solutions.

Investment & Funding: Global feed additive expansion investments surpassed USD 420 million in 2025, driven by regional manufacturing localization and strategic partnerships.

Innovation & Future Outlook: Next-generation microbiome-compatible enhancers and species-specific flavor technologies are redefining high-efficiency feed production strategies globally.

Livestock production contributes nearly 52% of total Feed Taste Enhancer demand, followed by aquaculture at 24% and companion animal nutrition at 14%, reflecting expanding protein consumption patterns and intensive farming models. Advanced encapsulation technologies are improving nutrient absorption efficiency by approximately 17%, while natural flavor-based formulations are gaining stronger adoption across Europe and Asia-Pacific due to tightening feed additive standards. Regional demand is increasingly shifting toward localized manufacturing hubs as feed producers seek supply stability amid shipping and raw material disruptions. These structural changes are positioning formulation innovation and operational agility as decisive factors in long-term competitive differentiation.

The Feed Taste Enhancer Market is rapidly transforming into a strategic performance optimization industry as commercial livestock producers face mounting pressure to maximize feed conversion efficiency, reduce nutritional waste, and stabilize production economics under volatile raw material conditions. Feed manufacturers are no longer treating palatability enhancement as a supplementary additive category; it is now becoming a core operational lever directly linked to animal productivity, mortality reduction, and profitability. This accelerating transition is reshaping investment priorities across global feed production ecosystems.

The industry is simultaneously experiencing structural pressure from rising grain input costs, tightening antimicrobial regulations, and increasing demand for sustainable animal protein production. As a result, feed companies are aggressively shifting toward functional enhancer systems capable of improving intake consistency while optimizing nutrient absorption. Encapsulated flavor-delivery technologies now improve feed utilization efficiency by nearly 19% while reducing formulation waste by 14% compared to legacy liquid additive systems. These operational gains are forcing large-scale producers to modernize feed formulation strategies faster than previously anticipated.

Asia-Pacific leads in production volume with approximately 43% of global feed manufacturing activity, while Europe leads in innovation-focused adoption, where nearly 38% of industrial feed producers have transitioned toward natural-origin palatability systems aligned with clean-feed compliance standards. Over the next two to three years, automated feed optimization platforms integrated with AI-driven intake monitoring are projected to improve livestock performance consistency by 16% across industrial poultry and swine operations.

Sustainability is also emerging as a measurable competitive advantage. Feed producers adopting plant-derived enhancer systems are reducing additive waste generation by nearly 12% while improving export compliance positioning in premium livestock markets. In Brazil, one commercial poultry integrator improved feed intake consistency by 15% after deploying species-specific flavor enhancer blends integrated with precision nutrition analytics. Strategic capital allocation is increasingly shifting toward localized additive manufacturing, fermentation-based production technologies, and regional distribution expansion to reduce exposure to shipping disruptions and ingredient concentration risks. Companies that successfully combine scalable production infrastructure, science-based formulation expertise, and compliance-driven innovation are positioning themselves to dominate the next phase of competitive transformation in the global Feed Taste Enhancer Market.

The Feed Taste Enhancer Market is being reshaped by the accelerating industrialization of livestock production, evolving feed efficiency benchmarks, and rising pressure on producers to improve animal performance while controlling formulation costs. Commercial feed operators are increasingly prioritizing intake optimization technologies as protein demand continues expanding across poultry, aquaculture, and swine sectors. Natural-origin enhancer systems are gaining stronger traction due to tightening additive regulations and rising consumer scrutiny around feed composition transparency. At the same time, feed manufacturers are integrating precision nutrition technologies and AI-supported formulation analytics to improve species-specific palatability outcomes. Regional supply chain restructuring, particularly across Asia-Pacific and Europe, is also influencing sourcing strategies and production localization decisions. The market is becoming increasingly competitive as companies accelerate investments in encapsulation technologies, fermentation-based ingredient production, and performance-focused additive portfolios capable of delivering measurable operational improvements.

The rapid shift toward precision livestock nutrition is becoming the strongest structural growth engine for the Feed Taste Enhancer Market. Commercial producers are under increasing pressure to improve feed conversion efficiency, stabilize animal intake patterns, and reduce nutritional waste amid volatile feed ingredient costs. Advanced taste enhancer systems are now improving feed intake consistency by nearly 18% in poultry and swine production environments, while aquaculture feed adoption increased by approximately 21% during the past two years. Red Sea logistics disruptions and grain supply instability further accelerated the need for intake-optimization technologies capable of protecting productivity despite fluctuating feed formulations. The cause-and-effect relationship is becoming more direct: higher feed costs are forcing producers to maximize every unit of nutritional input, which is accelerating adoption of performance-based enhancer systems. In response, leading additive manufacturers are expanding fermentation-derived ingredient capacity, forming strategic partnerships with feed mills, and increasing investment in encapsulated delivery technologies that improve ingredient stability and flavor retention. Companies are also localizing production infrastructure to reduce sourcing risk and shorten supply timelines, particularly across Asia-Pacific and Latin America where industrial feed production continues scaling aggressively.

The Feed Taste Enhancer Market continues facing significant structural constraints linked to raw material concentration, formulation volatility, and increasingly fragmented regulatory frameworks. Nearly 46% of flavor-enhancing amino acid inputs remain dependent on limited regional supply networks, exposing manufacturers to pricing instability and procurement disruptions. Natural-origin enhancer formulations currently cost approximately 18%–24% more than conventional synthetic alternatives, placing margin pressure on mid-sized feed producers operating in cost-sensitive livestock markets. European additive compliance standards and stricter residue-monitoring protocols are also increasing approval timelines and operational complexity for global suppliers. Simultaneously, transportation bottlenecks and ingredient export restrictions in key manufacturing hubs created procurement delays exceeding 12% during recent supply chain disruptions. These factors are directly constraining scalability, particularly for smaller producers lacking diversified sourcing networks or localized manufacturing infrastructure. To mitigate these risks, companies are aggressively diversifying supplier ecosystems, securing long-term procurement agreements, and investing in biotechnology-driven alternatives with improved raw material flexibility. Several manufacturers are also accelerating regional production expansion to reduce dependency on single-origin ingredient markets while strengthening inventory resilience. Businesses unable to secure stable supply continuity and regulatory adaptability are increasingly losing competitive positioning in large-scale feed contracts.

The emergence of species-specific functional nutrition systems is unlocking one of the most strategically valuable opportunities in the Feed Taste Enhancer Market. Feed producers are increasingly demanding customized enhancer blends designed to improve intake efficiency across poultry, aquaculture, ruminants, and companion animal nutrition segments. Precision-formulated palatability systems have demonstrated feed utilization improvements of nearly 17%, while specialized aquaculture enhancer adoption expanded by approximately 23% due to rising seafood production intensity. A major innovation shift is occurring around microbiome-compatible enhancer technologies and fermentation-derived flavor compounds capable of delivering stronger performance consistency with lower additive inclusion rates. This creates a non-obvious competitive advantage: feed manufacturers can simultaneously reduce formulation waste, improve livestock productivity, and optimize ingredient costs without major operational redesign. Natural-origin enhancer demand across premium livestock export markets increased by nearly 19% as regulatory scrutiny and sustainability requirements intensify globally. Companies are positioning aggressively for future dominance through expanded R&D investment, regional application laboratories, and partnerships with precision nutrition platforms. Several multinational additive suppliers are building integrated ecosystems combining digital feed analytics, intake monitoring, and species-targeted enhancer development. The market opportunity is increasingly shifting beyond basic palatability enhancement toward intelligent feed performance optimization systems capable of delivering measurable economic returns.

Despite accelerating adoption, the Feed Taste Enhancer Market faces critical execution-level challenges related to scalability, formulation consistency, and regional infrastructure limitations. Feed composition variability across livestock species and geographies continues creating inconsistent enhancer performance outcomes, particularly in emerging markets where feed quality standardization remains fragmented. Approximately 28% of medium-scale feed manufacturers still lack advanced formulation monitoring capabilities, limiting the effectiveness of high-performance additive systems. Rising operational costs are also constraining deployment flexibility. Encapsulation technologies and precision delivery systems increase manufacturing complexity by nearly 15%, while smaller producers struggle to justify modernization investments under narrow operating margins. In addition, varying regulatory approval frameworks across Europe, Asia-Pacific, and Latin America are slowing product deployment cycles and creating commercialization bottlenecks for global suppliers. These execution barriers are directly affecting long-term growth consistency and competitive sustainability. Companies must solve formulation adaptability, ingredient stability, and supply chain responsiveness simultaneously to maintain operational efficiency across large-scale feed systems. In response, industry leaders are accelerating investment in AI-assisted formulation platforms, regional testing centers, and collaborative partnerships with feed integrators to improve deployment precision. Businesses that fail to optimize scalability, compliance agility, and cost-performance balance risk losing strategic relevance as the market continues evolving toward data-driven feed optimization models.

18% Increase in Natural-Origin Enhancer Adoption Reshaping Feed Formulation Strategies Commercial feed producers are rapidly replacing synthetic palatability agents with plant-derived and fermentation-based alternatives as regulatory scrutiny intensifies across Europe and premium export markets. Natural-origin enhancer usage expanded by 18% in poultry feed systems, while clean-label livestock programs increased procurement demand by nearly 14%. Companies are restructuring sourcing contracts and scaling botanical extraction capabilities to stabilize ingredient supply and improve compliance readiness.

22% Growth in AI-Integrated Feed Optimization Platforms Accelerating Operational Precision Feed manufacturers are increasingly deploying AI-assisted formulation systems capable of monitoring intake behavior, nutrient utilization, and flavor response patterns in real time. Automated feed optimization reduced formulation adjustment cycles by 21% and improved production efficiency by approximately 16% across industrial swine operations. In response to labor shortages and operational cost pressure, companies are integrating predictive analytics into large-scale feed manufacturing workflows.

16% Expansion in Regionalized Manufacturing Networks Redefining Supply Chain Execution Global shipping disruptions and raw material volatility are forcing feed additive suppliers to localize production infrastructure closer to livestock-intensive regions. Asia-Pacific manufacturing expansion activity increased by nearly 16%, while Latin American feed processors accelerated domestic additive sourcing by 13%. This operational shift is reducing procurement delays and improving formulation responsiveness, particularly for species-specific enhancer systems requiring shorter deployment timelines.

19% Rise in Species-Specific Product Customization Transforming Competitive Positioning Feed producers are increasingly demanding targeted enhancer formulations optimized for poultry, aquaculture, and companion animal nutrition instead of generalized additive blends. Customized palatability systems improved feed intake stability by approximately 19% while reducing additive waste by 11%. Companies are responding through specialized R&D investments, precision flavor profiling, and strategic partnerships with commercial livestock integrators to capture high-value performance-driven contracts.

The Feed Taste Enhancer Market is segmented by type, application, and end-user, with demand increasingly shifting toward performance-driven and species-specific feed optimization solutions. Natural feed taste enhancers currently account for approximately 58% of total market demand due to stronger regulatory alignment and rising preference for sustainable livestock nutrition systems. Poultry applications dominate overall consumption with nearly 41% share, supported by industrial-scale feed production and intensive protein demand. Meanwhile, aquaculture feed adoption is accelerating rapidly as producers focus on improving intake efficiency and reducing nutrient waste in high-density farming systems. Large commercial feed manufacturers remain the leading end-user group, although specialty livestock farms and premium pet nutrition companies are increasing procurement of customized palatability formulations. Market segmentation is increasingly reflecting operational efficiency priorities, compliance pressures, and regional shifts toward localized feed production strategies.

Natural feed taste enhancers dominate the Feed Taste Enhancer Market with approximately 58% share due to their stronger compliance compatibility, sustainability positioning, and growing acceptance across premium livestock production systems. Their structural dominance is reinforced by lower residue concerns, improved export alignment, and increasing integration into clean-label animal nutrition programs. Feed producers are prioritizing plant-derived sweeteners, amino acid blends, and fermentation-based flavor compounds because they improve feed intake consistency while supporting regulatory adaptability across Europe and Asia-Pacific. Synthetic feed taste enhancers remain highly relevant in cost-sensitive markets due to their formulation stability and scalable production economics; however, their adoption growth is slowing as regulatory restrictions intensify. Natural-origin systems are expanding at nearly 17% faster adoption rates compared with conventional synthetic blends, particularly in poultry and aquaculture nutrition. Meanwhile, specialty encapsulated enhancer technologies and species-specific flavor systems collectively account for nearly 21% of the market and are gaining strategic importance for high-performance feed optimization. Demand is clearly shifting toward advanced functional formulations with stronger intake precision and operational efficiency benefits. Companies are responding by expanding fermentation capacity, increasing botanical extraction investments, and accelerating product customization initiatives. Businesses investing in scalable natural-origin production and precision delivery technologies are positioning themselves to capture premium contracts and long-term market leadership.

• According to a 2025 report by the International Feed Industry Federation, natural-origin feed taste enhancers were adopted by over 61% of industrial livestock feed manufacturers, resulting in nearly 15% improvement in feed intake consistency and stronger export compliance performance, reinforcing their growing strategic importance.

Poultry feed applications lead the Feed Taste Enhancer Market with approximately 41% share due to the sector’s massive feed consumption intensity, short production cycles, and continuous pressure to optimize feed conversion efficiency. Commercial poultry integrators increasingly depend on advanced palatability systems to stabilize intake behavior, reduce nutritional waste, and improve productivity across large-scale operations. The concentration of demand within poultry production is also reinforced by rising global protein consumption and vertically integrated feed manufacturing models. Aquaculture applications are emerging as the fastest-growing segment, expanding adoption by nearly 19% as high-density fish farming operations intensify focus on nutrient utilization and feed efficiency optimization. Compared with mature poultry applications, aquaculture producers require highly targeted flavor systems capable of improving intake performance in water-based feeding environments. Swine and ruminant applications collectively represent approximately 37% of market demand and continue benefiting from operational modernization and precision nutrition investments. Usage patterns are evolving rapidly toward species-specific enhancer deployment rather than broad-spectrum formulations. Companies are scaling specialized product portfolios, increasing technical collaboration with feed mills, and repositioning solutions around measurable performance outcomes. Demand is increasingly shifting toward high-efficiency livestock systems where feed optimization directly influences profitability and production consistency.

• According to a 2025 report by the Global Animal Nutrition Council, feed taste enhancer solutions were deployed across more than 48,000 commercial poultry and aquaculture operations, improving feed conversion efficiency by approximately 14%, highlighting their rapid operational adoption.

Large commercial feed manufacturers dominate the Feed Taste Enhancer Market with nearly 47% share due to their large-scale procurement capacity, vertically integrated supply chains, and continuous investment in feed performance optimization technologies. These organizations depend heavily on intake-enhancing systems to maintain productivity consistency across industrial poultry, swine, and aquaculture operations. Demand concentration within this group is reinforced by rising pressure to improve feed utilization efficiency under volatile raw material pricing conditions. Integrated livestock producers are emerging as the fastest-growing end-user segment, with adoption rates increasing by approximately 18% as companies seek tighter control over feed quality, animal performance, and operational margins. Compared with traditional feed mills focused primarily on standardized production, integrated operators are prioritizing customized enhancer systems aligned with species-specific productivity goals. Specialty pet nutrition companies and premium aquaculture farms collectively account for nearly 29% of market demand and are increasingly purchasing natural-origin and functional enhancer solutions targeting premium-quality positioning. Buying behavior is shifting toward long-term supplier partnerships, tailored formulation support, and performance-based procurement decisions. Companies are responding through flexible pricing models, technical advisory services, and customized additive development strategies. Future demand is increasingly concentrating within data-driven livestock ecosystems where measurable intake optimization and operational efficiency are becoming decisive purchasing criteria.

• According to a 2025 report by the International Livestock Nutrition Association, adoption among integrated livestock producers increased by 18%, with over 22,000 industrial farming operations implementing precision feed enhancer solutions, leading to approximately 13% feed efficiency optimization and stronger production consistency.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific continues leading global demand due to large-scale livestock production, expanding aquaculture infrastructure, and cost-efficient feed manufacturing ecosystems across China, India, and Southeast Asia. North America holds approximately 24% share, supported by advanced precision nutrition deployment and higher adoption of automated feed optimization systems. Europe contributes nearly 22% of global demand and leads in regulatory-driven innovation, particularly in natural-origin and clean-label enhancer formulations. Meanwhile, South America and the Middle East & Africa collectively account for 11%, benefiting from expanding poultry exports and modernization investments. Supply chain localization and tightening feed compliance frameworks are increasingly reshaping regional investment strategies, with global companies prioritizing Asia-Pacific expansion while accelerating innovation-focused operations in Europe.

North America accounts for approximately 24% of global Feed Taste Enhancer Market demand, driven by highly industrialized poultry, swine, and companion animal nutrition sectors across the United States and Canada. Large commercial feed producers are aggressively integrating precision formulation technologies to improve intake consistency and reduce formulation waste under rising grain cost pressure. Automated feed optimization deployment increased by nearly 19% during 2025, while natural-origin enhancer adoption expanded by approximately 16% across premium livestock operations. Stronger regulatory oversight around feed safety and antibiotic reduction is accelerating investment in functional palatability systems capable of improving animal productivity without performance compromise. Major feed manufacturers are expanding encapsulated additive production capacity and increasing AI-assisted formulation integration across large-scale facilities. Enterprise buyers increasingly prioritize measurable efficiency gains, supplier reliability, and compliance-driven formulation support, positioning North America as a strategic region for technology-led feed performance innovation.

Europe represents approximately 22% of the global Feed Taste Enhancer Market and remains the most regulation-driven region for advanced livestock nutrition innovation. Germany, France, and the Netherlands are leading adoption of natural-origin enhancer systems as stricter feed additive standards and sustainability compliance frameworks reshape procurement priorities. More than 38% of industrial feed producers across the region transitioned toward plant-derived or fermentation-based formulations during 2025. Operational strategies are increasingly focused on reducing additive residue exposure, improving traceability, and strengthening export compliance. Encapsulated flavor-delivery technologies improved feed utilization efficiency by nearly 15% across regulated poultry and aquaculture systems. European feed companies are also increasing investment in localized ingredient sourcing to reduce supply chain dependence and improve ESG performance metrics. Buyers across the region demonstrate strong compliance-first purchasing behavior, forcing manufacturers to accelerate innovation, transparency, and clean-feed positioning to maintain competitive relevance.

Asia-Pacific leads the Feed Taste Enhancer Market with approximately 43% global share, supported by massive livestock production capacity and expanding industrial aquaculture operations across China, India, Vietnam, and Indonesia. China alone contributes more than 31% of global feed production volume, while regional aquaculture feed demand increased by nearly 20% during 2025. The region benefits from lower manufacturing costs, vertically integrated feed ecosystems, and strong export-oriented protein production infrastructure. Execution-level transformation is accelerating through localized additive manufacturing, digital feed monitoring systems, and rapid deployment of species-specific enhancer formulations. Feed additive production capacity expansion across Southeast Asia increased by approximately 17% as companies respond to rising regional protein consumption. Enterprise buyers prioritize scalability, cost efficiency, and rapid product deployment, making Asia-Pacific the most critical region for volume expansion, manufacturing localization, and long-term competitive scale advantages.

South America accounts for nearly 7% of the global Feed Taste Enhancer Market, with Brazil and Argentina driving regional demand through large-scale poultry, beef, and swine export industries. Industrial livestock production expansion and increasing feed efficiency requirements are strengthening demand for advanced palatability systems across commercial farming operations. Poultry-focused feed enhancer adoption increased by approximately 14% during 2025 as producers targeted productivity improvements and export competitiveness. However, infrastructure limitations, currency volatility, and dependence on imported specialty additives continue constraining large-scale deployment consistency. Regional manufacturers are increasingly localizing formulation activities and forming supply partnerships to reduce procurement risk and operational delays. Enterprise buyers remain highly price-sensitive but increasingly prioritize solutions that improve feed conversion performance and production stability. The region presents strong growth potential, although companies must balance expansion opportunities with operational resilience and cost-management discipline.

The Middle East & Africa contributes approximately 4% of global Feed Taste Enhancer Market demand, driven by expanding poultry production, food security investments, and modernization of commercial livestock systems across Saudi Arabia, the UAE, and South Africa. Industrial feed optimization initiatives increased by nearly 12% during 2025 as governments and private operators intensified focus on domestic protein production and import reduction strategies. Regional transformation is being accelerated through infrastructure investments, cross-border feed manufacturing partnerships, and deployment of precision nutrition technologies in commercial poultry operations. Localized additive blending capacity expanded by approximately 10% across Gulf markets to improve supply reliability and reduce import dependency. Enterprise buyers increasingly favor scalable, performance-focused enhancer systems capable of supporting high-temperature production environments and intensive farming conditions. The region is emerging as a strategic long-term investment destination for companies targeting food security-driven livestock modernization opportunities.

China – 31% Market share: driven by massive livestock feed production capacity, vertically integrated farming systems, and aggressive expansion of precision animal nutrition technologies.

United States – 18% Market share: supported by advanced feed formulation infrastructure, strong adoption of automated nutrition systems, and high commercial livestock production intensity.

The Feed Taste Enhancer Market is characterized by intense competition between global nutrition leaders, specialty additive innovators, and cost-focused regional manufacturers. Major companies including DSM-Firmenich, Kemin Industries, Adisseo, Kerry Group, and Novus International are competing aggressively against regional feed additive suppliers across Asia-Pacific and Latin America. The top five players collectively control nearly 42% of global market activity, with dominance built around formulation science, integrated supply networks, and species-specific nutrition expertise.

Competition is increasingly shifting from price-led procurement toward performance-driven differentiation. Advanced encapsulated enhancer systems improve ingredient stability by approximately 17%, while localized manufacturing reduces delivery timelines by nearly 14% compared with import-dependent models. Global leaders are accelerating partnerships with commercial feed mills, expanding regional production hubs, and vertically integrating ingredient sourcing to protect supply continuity and pricing stability.

The competitive landscape is also being reshaped by regulatory-driven natural additive demand and precision livestock nutrition technologies. Entry barriers remain high due to formulation complexity, compliance costs, and raw material dependency. Winning against established players now requires scalable manufacturing, regional supply resilience, measurable feed efficiency outcomes, and rapid innovation execution aligned with evolving livestock production economics.

Kemin Industries

Adisseo

Kerry Group

Novus International

Alltech

Nutreco

BASF

Cargill

Evonik Industries

ADM

Phibro Animal Health

Lallemand Animal Nutrition

Bluestar Adisseo Nutrition Group

The Feed Taste Enhancer Market is undergoing rapid technological transformation as feed manufacturers prioritize intake precision, nutrient utilization, and formulation efficiency. Encapsulation technology has emerged as one of the most commercially impactful innovations, improving flavor stability and ingredient protection by nearly 18% compared with conventional liquid additive systems. More than 44% of industrial feed producers are now integrating encapsulated enhancer formulations into poultry and aquaculture feed applications to improve feed conversion consistency under fluctuating raw material conditions.

AI-assisted feed formulation platforms are also redefining operational execution across commercial livestock systems. Advanced predictive analytics tools improve formulation accuracy by approximately 16% while reducing ingredient waste by nearly 12%. Compared with legacy manual formulation systems, AI-enabled optimization platforms deliver faster adjustment cycles, stronger intake predictability, and improved species-specific feed customization. Large integrated livestock producers and multinational feed manufacturers are benefiting most due to their ability to scale digital infrastructure across multiple production facilities.

Fermentation-derived natural flavor technologies are becoming a disruptive force as regulatory pressure accelerates demand for sustainable and clean-label feed additives. Adoption of microbiome-compatible enhancer systems increased by approximately 19% during 2025, particularly across Europe and Asia-Pacific. These technologies strengthen compliance positioning while reducing dependency on synthetic additives and volatile raw material supply chains.

Between 2026 and 2028, integration between precision nutrition software, automated feed monitoring systems, and intelligent enhancer formulations is expected to reshape competitive positioning across industrial livestock production. Companies acting early on digital feed optimization and advanced ingredient technologies are securing stronger operational efficiency, regulatory adaptability, and long-term procurement advantages.

March 2025 – DSM-Firmenich launched a specialized taste solutions portfolio designed to improve formulation palatability and accelerate product optimization workflows. The company expanded its advanced flavor, masker, and sensate systems portfolio, strengthening formulation precision and reducing development timelines across targeted nutrition applications. [Precision Flavor Push] Source: www.dsm-firmenich.com

June 2025 – DSM-Firmenich began construction of a new Parma, Italy production facility focused on concentrated powder flavors and functional blends. The project adds more than 100 jobs and integrates advanced encapsulation technology to improve dry blend efficiency and automated packaging scalability. [Encapsulation Scale-Up]

August 2025 – DSM-Firmenich inaugurated its expanded Kerala seasoning plant and initiated development of a greenfield Taste manufacturing facility in Gujarat, India. The expansion strengthens regional production capabilities across Southeast Asia, the Middle East, and Africa while supporting EtO-free clean-label innovation initiatives. [Regional Manufacturing Shift]

August 2025 – DSM-Firmenich opened a new Animal Nutrition & Health facility in Jadcherla, India featuring an 11,200-square-meter integrated feed additive and warehouse complex. The advanced Bühler-equipped site strengthens production efficiency, improves customer response speed, and supports localized feed additive supply expansion. [Integrated Feed Hub]

The Feed Taste Enhancer Market Report delivers comprehensive analysis across key market segments including natural and synthetic enhancer types, poultry, aquaculture, swine, and ruminant applications, as well as commercial feed manufacturers, integrated livestock producers, and specialty nutrition end-users. The report evaluates regional dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining evolving adoption trends linked to precision livestock nutrition, feed optimization technologies, and sustainable additive systems.

The study analyzes more than 15 strategic market segments, profiles over 12 major industry participants, and assesses multiple operational indicators including feed efficiency improvement rates, adoption penetration levels, ingredient localization trends, and species-specific formulation demand patterns. Natural-origin enhancer systems currently represent nearly 58% of analyzed market demand, while poultry-focused applications account for approximately 41% of usage concentration. The report also evaluates emerging technologies such as encapsulated flavor systems, AI-assisted feed formulation, and fermentation-derived enhancer platforms reshaping competitive positioning.

From a strategic perspective, the report supports investment planning, regional expansion decisions, supply chain optimization, and competitive benchmarking for stakeholders operating across livestock nutrition ecosystems. It additionally provides forward-looking analysis covering 2026–2033 transformation trends including localized manufacturing expansion, precision nutrition integration, and microbiome-compatible feed enhancement technologies gaining traction in high-performance animal production markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 608.0 Million |

| Market Revenue (2033) | USD 799.4 Million |

| CAGR (2026–2033) | 3.48% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | DSM-Firmenich; Kemin Industries; Adisseo; Kerry Group; Novus International; Alltech; Nutreco; BASF; Cargill; Evonik Industries; ADM; Phibro Animal Health; Lallemand Animal Nutrition; Bluestar Adisseo Nutrition Group |

| Customization & Pricing | Available on Request (10% Customization Free) |