Reports

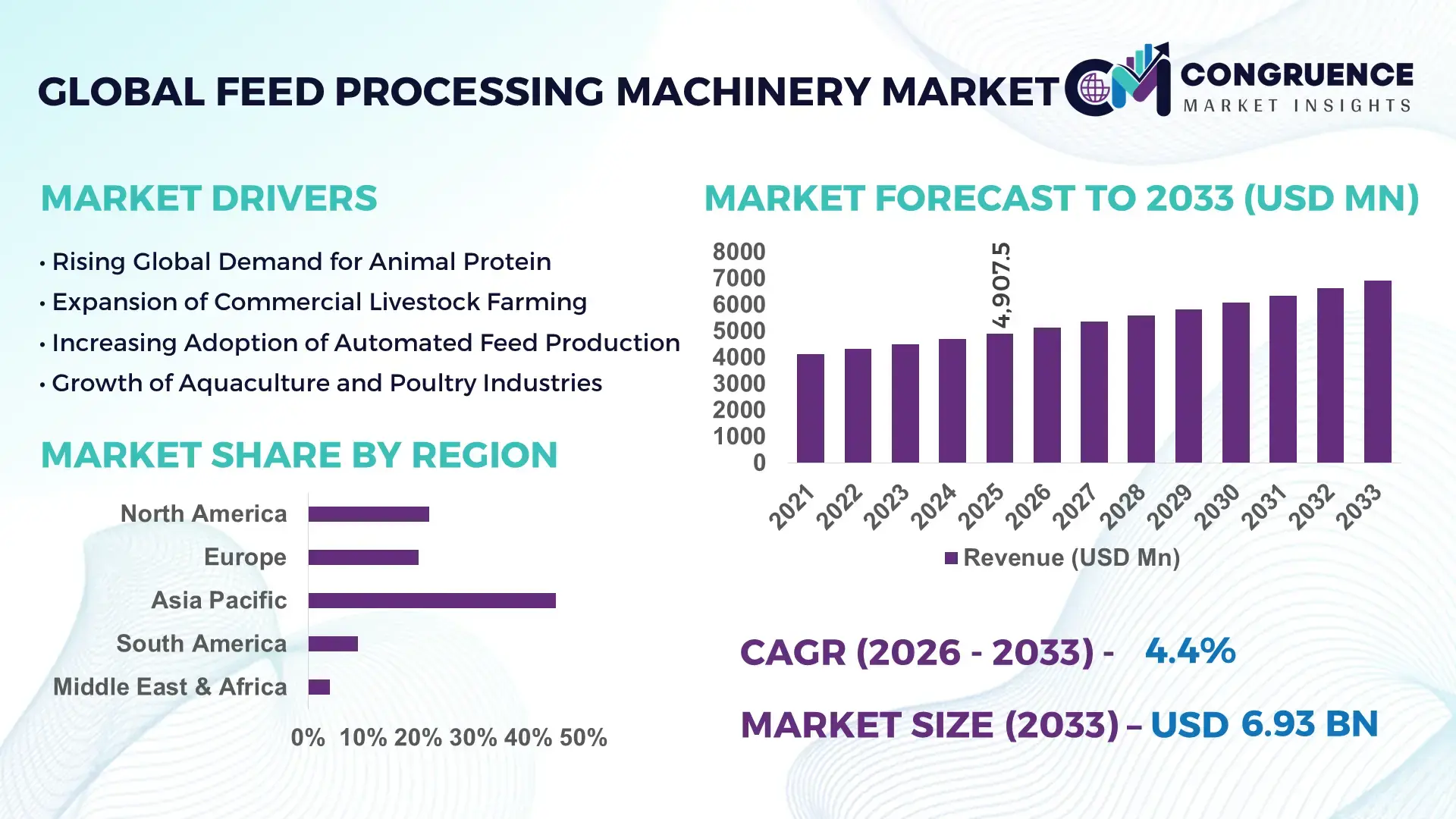

The Global Feed Processing Machinery Market was valued at USD 4,907.54 Million in 2025 and is anticipated to reach a value of USD 6,925.77 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. This growth is driven by rising global demand for high‑efficiency feed production systems and automation technologies that enhance operational throughput and sustainability.

China stands as the most significant contributor to the global Feed Processing Machinery market, with the country’s processing capacity exceeding 220 million metric tons of feed annually, reflecting intense production scale and investment in advanced pelleting, grinding, and extrusion technologies. Over 80% of major feed mills in China have adopted automated mixing and control systems with real‑time data feedback to improve feed uniformity and reduce waste. Capital expenditure in China’s feed equipment sector surpassed USD 1.2 billion in 2024, with technological advancements such as IoT monitoring and smart sensor integration increasing processing efficiency and reducing energy consumption by up to 18% in modern installations.

Market Size & Growth: Valued at ~USD 4.9 billion in 2025 and projected at ~USD 6.9 billion by 2033 with a 4.4% CAGR driven by automation adoption and precision nutrition demand.

Top Growth Drivers: Surge in demand for quality animal protein (48% adoption rise), precision processing tech integration (36% efficiency gain), expansion of aquaculture and poultry feed segments (42% volume increase).

Short‑Term Forecast: By 2028, feed mill system cost inefficiencies expected to drop by ~22% through digital control optimizations.

Emerging Technologies: IoT‑enabled monitoring systems, AI‑driven predictive maintenance, and modular processing lines for flexible capacity scaling.

Regional Leaders: Asia‑Pacific ~USD 3.2B by 2033 with strong aquafeed demand, North America ~USD 1.8B driven by automated batching, Europe ~USD 1.1B focusing on energy‑efficient systems.

Consumer/End‑User Trends: Increased adoption among commercial feed manufacturers and on‑farm operations embracing precision nutrition and automated quality assurance.

Pilot or Case Example: In 2025, a Thailand feed mill pilot integrating smart sensors achieved a 25% reduction in unplanned downtime and 15% improvement in output consistency.

Competitive Landscape: Leading platform commands ~28% share, with major competitors including global and regional manufacturers driving innovation.

Regulatory & ESG Impact: Enhanced feed safety mandates and energy‑efficiency standards are boosting modern equipment uptake across regions.

Investment & Funding Patterns: Recent investment in feed infrastructure exceeded USD 3.4 billion, with significant funding directed toward digital integration and sustainable processing technologies.

Innovation & Future Outlook: Focus on AI analytics, flexible modular designs, and energy‑saving technologies shaping next‑generation feed systems.

The Feed Processing Machinery market continues to benefit from diversification across agricultural livestock, aquaculture, and specialty feed segments. Key industry sectors such as poultry, aquaculture, swine, and ruminants contribute significantly to equipment demand, with machinery tailored for pellet durability, moisture control, and ingredient precision emerging as differentiators. Recent innovations include smart production lines with predictive analytics, energy recovery systems, and modular extrusion units that support nutritional customization and operational resilience. Environmental and regulatory drivers are accelerating the adoption of low‑emission and energy‑efficient machinery, while economic factors such as feed cost optimization bolster demand for automated solutions and real‑time process control across global feed manufacturing landscapes.

The strategic relevance of the Feed Processing Machinery market lies in its critical role in enabling feed producers to meet rising global demand for animal‑based protein with efficient, cost‑effective processing systems. As livestock and aquaculture sectors intensify production, advanced feed machinery delivers significant improvements in throughput, consistency, and quality control. For example, IoT‑enabled automation delivers up to 25% improvement in operational monitoring compared to older manual systems, reducing waste and enhancing feed uniformity. Asia‑Pacific dominates in processing volume, while Europe leads in adoption of intelligent systems with over 70% of new installations featuring energy‑efficient and traceable solutions. By 2028, AI‑driven predictive maintenance is expected to improve uptime by approximately 30%, cutting unplanned stoppages and reducing lifecycle costs. Firms are increasingly committing to ESG metrics, such as a 20% reduction in energy consumption and waste generation targets by 2030, reflecting the importance of regulatory compliance and sustainable growth strategies. In 2026, a mid‑tier manufacturer achieved a 24% reduction in energy usage through retrofit of digital controllers across its grinding and pelleting lines. This convergence of strategic investments, digital transformation, and sustainability goals positions the Feed Processing Machinery market as an essential pillar of resilient, compliant, and future‑ready feed production infrastructure for the global agri‑food ecosystem.

The surge in global meat, dairy, and aquaculture consumption is a significant driver for Feed Processing Machinery, prompting producers to scale capacity and improve per‑batch efficiency. With global meat consumption per capita increasing year‑on‑year, feed processors are investing in high‑capacity grinders, mixers, and pelleting lines to handle expanded throughput without compromising nutrient balance. Adoption of automated processing systems improves feed conversion ratios and enhances pellet durability, supporting healthier livestock growth. Advanced machinery also enables customization for specific feed types, such as aqua feed with specialized extrusion and moisture control, meeting diverse end‑user requirements. This increased adoption reflects a broader trend toward precision feeding to balance production efficiency with nutritional quality.

High upfront investment in modern Feed Processing Machinery, including automated and energy‑efficient systems, poses a restraint for many operators, particularly small and mid‑sized producers. Capital expenditure for setting up or upgrading feed processing plants can range from hundreds of thousands to several million dollars, influencing procurement decisions. Additionally, the availability of refurbished or second‑hand machines remains significant in certain regions due to budget constraints, but these older systems often lack modern efficiency, predictive maintenance, and control features. Technical expertise to operate and maintain advanced equipment is also limited in emerging markets, slowing the transition to digitalized processing. Supply chain bottlenecks for key components such as sensors and control units further delay installations and upgrades, impacting overall market uptake.

The expanding aquaculture industry presents a lucrative opportunity for the Feed Processing Machinery market, with demand for specialized extrusion systems designed for floating and sinking feed pellets. Aquaculture feed requirements drive innovation in moisture‑controlled dryers and twin‑screw extruder technologies, enabling producers to meet precise nutrient specifications and improve fish and shrimp health outcomes. Additionally, the growing pet food and specialty feed segments necessitate flexible, small‑batch processing solutions with high precision and customization capabilities. Innovations such as vacuum coating for nutrient enrichment and modular equipment for scalable capacity address these emerging needs. With aquaculture and specialty feed production volumes rising, demand for tailored machinery solutions is expected to accelerate, particularly in Asia‑Pacific and North American markets where these segments show robust growth.

Volatility in key feed raw materials such as corn and soybean meal significantly affects processing costs, influencing feed formulation strategies and machine throughput economics. Energy expenses, which can account for a substantial portion of operational costs in grinding and pelleting processes, further challenge producers seeking to maintain profitability. Maintenance costs for high‑capacity machinery are also considerable, with annual expenses for predictive systems and spare parts adding to total cost of ownership. Inconsistent adoption of advanced monitoring and predictive technologies across facilities means many producers face unplanned downtime and reduced output efficiency. These cost and operational pressures underscore the need for continuous innovation in energy‑efficient designs and predictive maintenance solutions to mitigate production risks and enhance long‑term market resilience.

• Increasing Adoption of Modular and Prefabricated Machinery Units

The Feed Processing Machinery market is witnessing a measurable rise in modular and prefabricated equipment installations, with 55% of new feed production facilities reporting reduced project lead‑times and up to 18% lower labor costs due to off‑site fabrication. Automated cutting and pre‑bending systems are enabling plants in Europe and North America to complete structural assembly 30% faster than traditional site‑built approaches. This shift is prompting demand for high‑precision modular mixers, pelletizers, and conveyors that can be rapidly deployed and scaled, resulting in documented improvements in commissioning speed and overall equipment utilization rates.

• Surge in Smart Automation and Predictive Maintenance Uptake

Smart Automation integration in Feed Processing Machinery has increased operations efficiency by over 40% in mid‑to‑large commercial mills, with predictive diagnostics reducing unplanned downtime by approximately 25%. Real‑time sensor feedback on moisture levels, motor performance, and throughput enables operators to implement corrective actions before failures occur. Digital twin simulations are also being used by 38% of advanced feed producers to optimize line balancing and reduce energy expenditure during peak production schedules, fostering higher overall equipment effectiveness.

• Enhanced Focus on Energy‑Efficient Grinding and Pelleting

Energy‑efficient milling and pelleting equipment is now deployed in nearly 60% of greenfield projects globally, driven by the need to reduce electrical consumption and thermal loss. Upgraded roller mill designs and variable frequency drives are achieving 22% lower energy use compared to legacy machines, and dryers with heat‑recovery systems are cutting fuel costs by up to 15%. These measurable enhancements are allowing processors to maintain stringent feed quality standards while significantly lowering operating expenditures tied to power and fuel.

• Expansion of Specialty Feed Machinery for Aquaculture and Pet Nutrition

The demand for machinery tailored to specialty feed formats is rapidly rising, with extrusion lines for aquaculture feed accounting for over 28% of new equipment inquiries and pet food processing solutions representing 19% of product customization requests. Innovations in twin‑screw extruders and low‑temperature drying systems have enabled precise control of pellet density and nutrient retention, meeting the unique requirements of fish, shrimp, and premium pet feeds. A documented deployment of advanced specialty extruders in a Southeast Asian aquafeed facility improved pellet durability by 32%, reflecting the growing emphasis on segment‑specific processing capability.

Market segmentation within the Feed Processing Machinery industry reflects a detailed breakdown by product types, application areas, and end‑user categories, each with distinct adoption patterns and operational priorities. Types range from grinders and mixers to dryers and pelletizers, with varying degrees of automation and precision built into each category. Application segmentation includes livestock feed, aquaculture, pet nutrition, and specialty feed, where operational requirements influence equipment choice and configuration. End‑user segmentation encompasses commercial mills, farm‑based processors, and contract manufacturers, each demonstrating unique investment behavior based on scale, throughput demands, and regulatory expectations. Together, these segmentation layers provide industry stakeholders with a nuanced understanding of demand drivers, equipment functionalities, and operational contexts that shape purchasing decisions and long‑term capital planning across the feed processing landscape.

In the Feed Processing Machinery market, pelletizers currently account for approximately 34% of installed equipment units due to their critical role in producing uniform density feed pellets required across livestock, poultry, and aquaculture segments. Grinders and mixers follow with combined usage in roughly 28% of facilities, valued for their role in achieving precise particle size and consistent formulation prior to pelleting. Dryers and coolers are integral to approximately 18% of systems, especially where moisture control and storage stability are paramount. Extruders, although currently representing about 12% of installations, are experiencing the fastest growth at a notable annual rate due to their specialized ability to produce floating and sinking aquafeed pellets with enhanced nutrient retention—responding to rising aquaculture demands. Other machinery types, including automated control panels, dust collection systems, and batching equipment, contribute the remaining 8% of the segment, supporting overall plant safety and throughput optimization.

Among application areas in the Feed Processing Machinery market, livestock feed production holds the largest share, covering approximately 42% of installations globally due to extensive demand for cattle, swine, and poultry feeds requiring robust grinding, pelleting, and mixing capabilities. Pet nutrition applications account for around 26%, driven by growth in premium, customized kibble formats needing precise extrusion and coating systems. Aquaculture feed processing, representing roughly 21%, is rapidly advancing through specialized extruder and dryer systems optimized for fish and shrimp diets with controlled pellet characteristics. Specialty and niche feed formats such as equine and exotic animal feed hold the remaining 11%, where tailored machinery supports small‑batch precision.

Commercial feed mills remain the leading end‑user segment within the Feed Processing Machinery market, accounting for about 38% of overall equipment utilization due to the high throughput demands and diverse feed formats they process. Farm‑based processors, encompassing integrated livestock operations and agricultural cooperatives, follow with roughly 29%, often investing in compact, automated systems that deliver reliable output with manageable footprint requirements. Contract manufacturers that provide toll processing services represent around 22%, using flexible machinery capable of handling a wide range of formulations and batch sizes. Small‑to‑medium enterprise feed producers contribute the remaining 11%, often adopting modular or second‑tier equipment to balance cost and capability.

Asia‑Pacific accounted for the largest market share at 45.75% in 2025 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 7.x% between 2026 and 2033 driven by rapid industrialization of animal husbandry and aquaculture sectors.

In 2025, Asia‑Pacific’s feed production volume exceeded 530 million metric tons, with China alone producing over 220 million metric tons, supporting strong demand for advanced grinding, pelleting, and extrusion machinery. North America held approximately 30% of installed machinery units, backed by over 240 million metric tons of feed processing activity and widespread automation adoption. Europe accounted for around 25‑30%, driven by regulatory compliance and precision feeding mandates, with Germany and France leading installations of AI‑enabled mixers and pelleting systems. South America contributed near 9%, notably Brazil and Argentina expanding poultry and cattle feed investments. Middle East & Africa, while smaller at roughly 7‑8%, saw 18% year‑on‑year equipment installations in 2023, particularly for modular and mobile processing units. These numeric distributions reflect diverse regional strategies, from high‑volume industrial outputs in Asia‑Pacific to technology‑led modernization in North American and European markets.

Is automation and precision nutrition reshaping operational performance?

North America’s Feed Processing Machinery market commands a significant ~30% market share of global installations, with the U.S. producing over 240 million metric tons of feed annually. Commercial feed mills and integrated livestock producers are key demand drivers, particularly in poultry, swine, and dairy applications where high throughput and quality assurance are critical. Regulatory frameworks emphasizing feed safety, traceability, and energy‑efficient operations have prompted mills to adopt advanced SCADA, IoT‑enabled automation, and variable frequency drives across 60%+ of new installations. Technological advancements such as real‑time moisture control and predictive maintenance systems are reducing unplanned downtime by an estimated 25%. Regional consumer behavior shows higher enterprise adoption of precision nutrition and digital control systems compared with smaller, farm‑level operations. A local player, for example, sees over 40% adoption of cloud‑connected feed mixers across mid‑sized U.S. feed producers, highlighting the shift toward smart processing lines that enhance throughput and compliance.

How are regulatory and sustainability priorities influencing machinery investments?

Europe’s Feed Processing Machinery market holds approximately 25‑30% of global installed units, with Germany, France, and the UK leading in adoption. Regulatory bodies across the EU enforce stringent feed safety, hygiene, and traceability standards, prompting feed processors to invest in dust‑tight mixers, hygienic conveyors, and advanced extrusion systems. Over 5,000 advanced mixers and extruders were installed in key European markets in a recent period to enhance compliance and reduce waste by 18% through precision feeding mandates. Sustainability initiatives in Europe are driving demand for energy‑efficient motors and lifecycle‑optimized machinery, while AI‑enabled plant‑wide controls are increasingly adopted to monitor emissions and quality. Consumer behavior in Europe reflects a preference for explainable, traceable equipment with robust performance analytics. A notable trend is digital retrofitting, where legacy plants are upgrading to automated batching and monitoring tools that improve operational consistency and traceability across multiple feed formats.

What makes this region a dominant force in feed processing modernization?

Asia‑Pacific is the largest Feed Processing Machinery market by volume, accounting for roughly 45.75% of global installations in 2025, supported by major consumption from China, India, and Southeast Asian countries. China alone contributed over 220 million metric tons of feed production, while India upgraded 800+ feed plants with modern grinding and pelleting lines in a recent year. Infrastructure trends in Asia‑Pacific include both greenfield commercial mills and modernization of older facilities with predictive control and energy‑saving systems. Regional tech innovations such as twin‑screw extruders for aquafeed and IoT‑integrated batching systems are proliferating, particularly in high‑demand markets like Vietnam’s shrimp feed sector, which produced 6.8 million metric tons of feed. Consumer behavior shows a blend of high‑volume commercial adoption and increasing small‑mill upgrades, influenced by rising incomes and urban dietary shifts toward animal protein.

How are agricultural trends shaping machinery demand across key Latin markets?

South America’s Feed Processing Machinery market contributes approximately 9–10% of global installations, led by Brazil and Argentina where robust cattle, poultry, and aquaculture activities necessitate mechanized processing lines. In Brazil, feed production exceeding 150 million metric tons supports investments in robust grinding, mixing, and pelleting systems optimized for tropical conditions. Infrastructure trends include expansion of large‑scale feed mills and integration of energy‑efficient extruders to reduce moisture and improve pellet quality. Government incentives focused on agricultural modernization and export expansion are encouraging new feed plant setups, with trade policies promoting technology transfer and capital investment. Consumer behavior variations show strength in large commercial operations, whereas smaller rural feed producers increasingly adopt modular and mobile milling units to serve localized demand.

What regional trends are driving adoption in emerging livestock economies?

The Middle East & Africa Feed Processing Machinery market accounts for ~7–8% of global installations, with notable growth in UAE, South Africa, Egypt, and Nigeria where livestock and poultry production is expanding. Regional demand trends include investment in modular and mobile feed systems that cater to decentralized farming communities. Over 18% year‑on‑year growth in equipment installations reflects modernization efforts, particularly in poultry feed lines and small‑to‑medium compound feed operations. Local regulations and trade partnerships aimed at improving food security are stimulating adoption of energy‑efficient milling and extrusion technologies. Consumer behavior in this region is influenced by cost‑sensitive procurement and growing preference for versatile machinery capable of handling diverse raw materials and feed formats.

China – ~40‑45% market share: High production capacity and extensive commercial feed mill network drive demand for advanced processors.

United States – ~30% market share: Strong end‑user demand in poultry, swine, and dairy coupled with high automation adoption sustains leadership.

The competitive landscape of the Feed Processing Machinery market is moderately concentrated, with approximately 30+ active global competitors vying across segments such as grinding, mixing, pelleting, and extrusion. The combined share of the top 5 companies accounts for a significant portion of installed machinery units, reflecting moderate consolidation in a landscape where global players compete with regional specialists. Market leaders are investing in product launches and strategic partnerships to enhance automation, energy efficiency, and intelligent systems integration. Companies are embedding predictive analytics and IoT connectivity in machinery, increasing overall equipment effectiveness by 20‑40% in high‑end installations. Over 150 new machine models with advanced control capabilities were introduced in recent years, signaling innovation momentum that supports end‑user demand for quality and sustainability. Strategic initiatives include mergers between automation technology providers and traditional feed processing equipment firms to integrate digital platforms into core machinery functions. The varied product portfolios and regional footprints of competitors fuel dynamic positioning, with Europe and Asia‑Pacific seeing high competitive intensity, while North America emphasizes precision nutrition and traceability. Operational excellence, service networks across 100+ countries, and technology adoption trends are central to competitive differentiation in this evolving market.

Buhler

Andritz

CPM

Jiangsu Muyang Group

Amandus Kahl

Shanghai ZhengChang International Machinery

Wenger Feeds

Sudenga Industries

Van Aarsen

Clextral

Current and emerging technologies are reshaping the Feed Processing Machinery market, significantly improving operational performance, efficiency, and product quality. Smart sensor systems embedded in grinders, mixers, and conveyors now monitor up to 27 operational parameters, including motor vibrations, temperature, and moisture content, enabling real‑time detection of inefficiencies and informing immediate corrective actions that enhance batch consistency by over 20% in advanced mills. AI and machine learning analytics are being integrated for predictive maintenance, reducing unexpected downtime by 30–40% and extending machine life by up to 8–12 years with optimized performance tracking. These systems help forecast failures with better than 90% accuracy, resulting in measurable increases in throughput and reduced service disruptions.

Digital twin technology is gaining traction, allowing operators to simulate feed production processes and adjust setpoints dynamically, which has improved pellet quality uniformity and reduced waste. IoT connectivity and cloud‑based remote monitoring systems connect control units across multi‑site operations, enabling centralized process oversight, reducing manual intervention, and improving decision latency. Twin‑screw extruders with precision temperature and moisture control systems are now common in aquafeed lines, delivering up to 95% uniformity in pellet density across production runs. Energy‑recovery and heat‑integration technologies in modern dryers and coolers can recapture up to 60–80% of thermal energy, significantly reducing power consumption per ton of processed feed.

Automation and robotics are also being adopted in loading and ingredient handling stages, with robotic arms reducing manual handling errors by nearly 47% and decreasing material spillage. Closed‑loop control systems with feedback from real‑time vision systems inspect up to 1,200 pellets per minute for quality control, substantially reducing rejects and improving output standards. These technological advancements are enabling producers to achieve greater productivity, enhanced feed quality, and improved sustainability outcomes across diverse processing environments, making technology a key factor in competitive differentiation for decision‑makers.

• In January 2024, Yemmak introduced a PLC‑integrated micro‑dosing system with up to 99.8% dosing accuracy for vitamins and minerals, adopted in over 60 poultry and pig feed mills within two months of release.

• In May 2025, Wenger and Extru‑Tech launched EXPRO AI, an AI‑powered extrusion process optimization software that predicts outcomes, optimizes setpoints, and enhances product quality and operational efficiency in extrusion applications.

• In early 2024, CPM Holdings, Inc. expanded its pet food processing lineup at a major industry expo, unveiling twin‑screw extruders, advanced dryers, precision coating systems, and hammermills designed for improved throughput and nutritional integrity.

• Between 2023 and 2025, several global and regional manufacturers announced new manufacturing and assembly facility investments in Asia‑Pacific aimed at shortening lead times and better serving the growing Feed Processing Machinery demand in the region.

The Feed Processing Machinery Market Report provides a comprehensive overview of the global landscape across key segments, geographies, applications, and technological innovations shaping the industry. It covers product types such as grinders, mixers, extruders, pelleting lines, and dryers, detailing specific functional insights like precision moisture control, high‑speed pellet durability optimization, and smart batching solutions. Geographic segmentation spans Asia‑Pacific, North America, Europe, South America, Middle East & Africa, with variations in adoption patterns, production capacities, and technology integration. The report also examines end‑user categories, including commercial feed mills, on‑farm processors, contract manufacturers, and specialty feed producers, noting differences in procurement behavior, automation uptake, and regional preferences.

Technology coverage encompasses IoT‑enabled sensors, AI‑based predictive maintenance analytics, digital twin simulations, and advanced extrusion control systems that enhance consistency and output quality. Emerging niches such as modular processing units, energy recovery systems, and dust‑control mechanisms are also detailed, with insights into how these innovations reduce waste and improve sustainability metrics across operations. In addition, the report highlights regulatory and ESG implications, including feed safety compliance, traceability standards, and energy‑efficient machinery trends that influence investment decisions. Regional case examples illustrate infrastructure trends, localized consumer behavior, and innovation hubs driving modernization. Overall, the scope extends to operational best practices, segment‑specific adoption drivers, and technology roadmaps that inform strategic planning and capital allocation for industry professionals and decision‑makers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Buhler, Andritz, CPM, Jiangsu Muyang Group, Amandus Kahl, Shanghai ZhengChang International Machinery, Wenger Feeds, Sudenga Industries, Van Aarsen, Clextral |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |