Reports

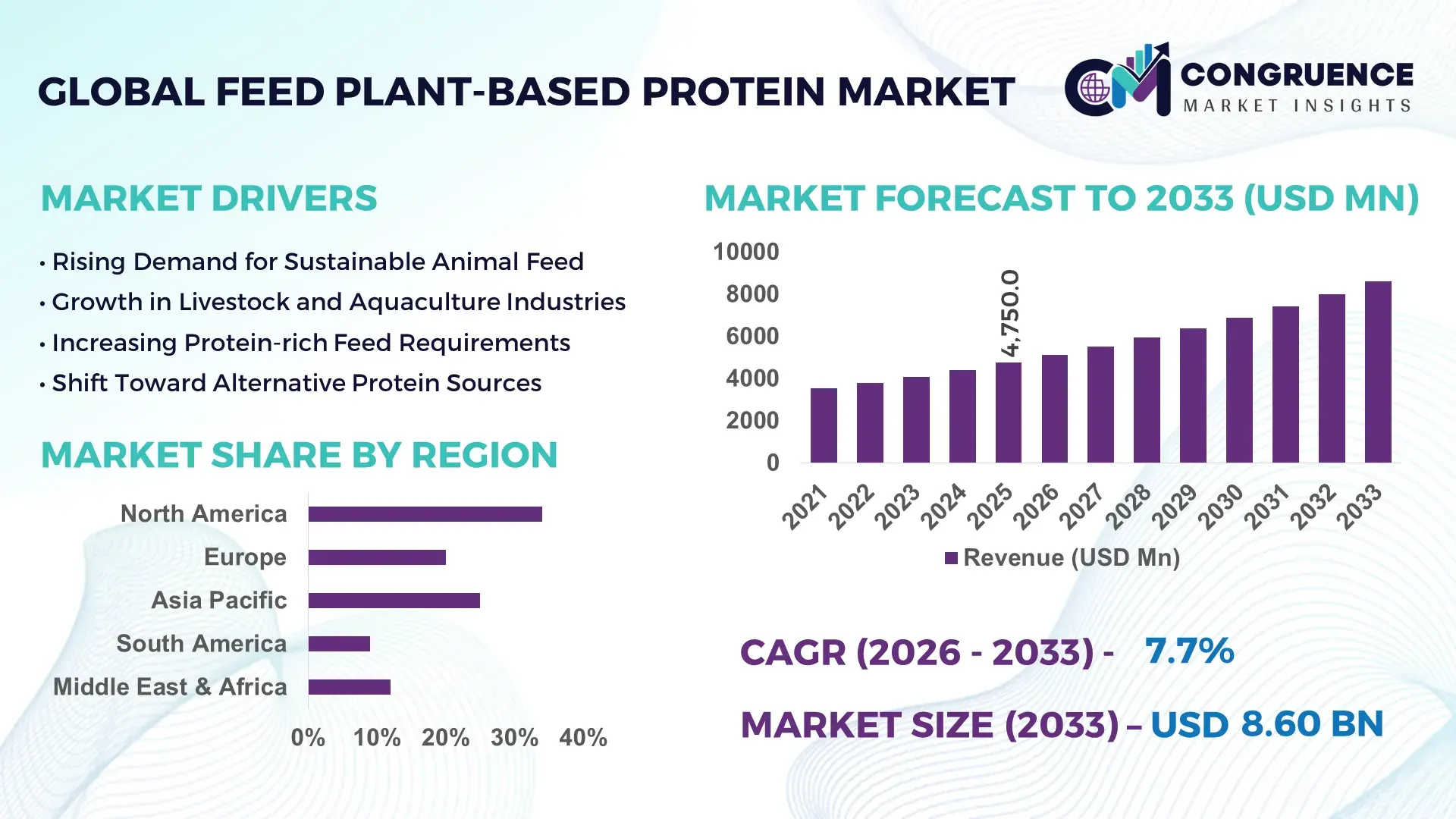

The Global Feed Plant-based Protein Market was valued at USD 4750 Million in 2025 and is anticipated to reach a value of USD 8598.43 Million by 2033 expanding at a CAGR of 7.7% between 2026 and 2033. This growth is primarily driven by the increasing shift toward sustainable livestock nutrition and alternative protein sources in animal feed formulations.

The United States continues to lead the Feed Plant-based Protein market in terms of large-scale production capacity, advanced processing infrastructure, and strong investment inflows. The country processes over 120 million metric tons of soybeans annually, with a significant portion allocated to feed protein extraction such as soybean meal and concentrates. More than 65% of U.S. livestock feed formulations incorporate plant-based proteins, particularly in poultry and swine segments. Additionally, over USD 1.5 billion has been invested in plant protein processing facilities since 2022, supporting innovations such as enzymatic protein extraction and low-anti-nutritional factor formulations. The adoption of precision feed technologies and high-protein feed blends has further strengthened industrial applications across dairy and aquaculture sectors.

Market Size & Growth: USD 4750 Million (2025) to USD 8598.43 Million (2033) at 7.7% CAGR driven by sustainable feed demand and livestock productivity enhancement.

Top Growth Drivers: 48% increase in plant protein adoption in feed, 35% efficiency gains in livestock nutrition, 29% reduction in feed costs with plant alternatives.

Short-Term Forecast: By 2028, optimized feed formulations are projected to improve protein utilization efficiency by 22%.

Emerging Technologies: Enzymatic protein extraction, fermentation-based feed protein enhancement, AI-driven feed optimization platforms.

Regional Leaders: North America projected at USD 2.9 Billion by 2033 with advanced processing, Asia-Pacific at USD 3.4 Billion driven by aquaculture demand, Europe at USD 1.8 Billion with sustainable feed regulations.

Consumer/End-User Trends: Poultry and aquaculture sectors account for over 60% of plant-based protein feed consumption due to cost efficiency and scalability.

Pilot or Case Example: In 2024, a European feed producer improved protein digestibility by 18% using fermentation-enhanced soy protein blends.

Competitive Landscape: Leading player holds approximately 18% share, followed by 4–5 major global feed protein producers with diversified plant protein portfolios.

Regulatory & ESG Impact: Over 40% of feed manufacturers are adopting low-carbon protein sourcing aligned with sustainability mandates.

Investment & Funding Patterns: More than USD 2.3 Billion invested globally in plant protein processing and feed innovation since 2023.

Innovation & Future Outlook: Integration of biotech-enhanced proteins and circular agriculture practices shaping next-generation feed solutions.

The Feed Plant-based Protein market is witnessing strong integration across livestock, aquaculture, and pet nutrition sectors, with soybean meal contributing nearly 55% of total plant-based feed protein consumption. Emerging alternatives such as pea protein and canola meal are gaining traction, accounting for over 20% of new product innovations. Regulatory pressure on reducing animal-based feed inputs and greenhouse gas emissions is accelerating adoption, especially in Europe and Asia-Pacific. Technological advancements including microbial fermentation and protein fortification are improving digestibility rates by up to 15%. Regional consumption patterns show Asia-Pacific leading in aquaculture feed demand, while North America emphasizes high-efficiency livestock nutrition. The market outlook remains positive with increasing demand for sustainable, cost-effective, and high-performance feed protein solutions.

The Feed Plant-based Protein market is becoming strategically critical for ensuring global food security, sustainable livestock production, and cost-efficient feed supply chains. With increasing pressure on reducing environmental impact, feed manufacturers are transitioning toward plant-based protein solutions that offer scalability and lower carbon footprints. Advanced fermentation-based protein enhancement delivers 25% improvement in nutrient absorption compared to conventional soybean meal processing techniques, making it a preferred solution for high-performance livestock feed.

Asia-Pacific dominates in volume due to large-scale aquaculture and poultry production, while Europe leads in adoption with over 52% of feed manufacturers integrating sustainable plant protein solutions into their operations. By 2028, AI-driven feed formulation technologies are expected to reduce feed waste by 20% while improving livestock productivity metrics. Companies are also aligning with ESG commitments, targeting up to 30% reduction in feed-related emissions by 2030 through plant-based protein substitution.

In 2024, a leading agritech firm in the Netherlands achieved a 17% improvement in feed conversion ratios by implementing precision fermentation technology in plant protein processing. These advancements are enabling producers to enhance nutritional profiles while maintaining cost efficiency. The Feed Plant-based Protein market is expected to evolve as a core pillar of resilient agricultural ecosystems, combining innovation, sustainability compliance, and scalable protein production to meet the rising global demand for animal nutrition.

The increasing demand for sustainable livestock nutrition is a primary driver of the Feed Plant-based Protein market. Plant-based proteins significantly reduce dependency on fishmeal and animal-derived proteins, which are associated with higher environmental impacts. Studies indicate that replacing conventional feed proteins with plant-based alternatives can lower greenhouse gas emissions by up to 25%. Additionally, over 60% of global feed manufacturers are incorporating soybean meal and alternative plant proteins into their formulations to enhance feed efficiency. The poultry and aquaculture industries, which account for a major share of global protein consumption, are rapidly adopting plant-based feed solutions due to their cost-effectiveness and scalability. The growing awareness of sustainable farming practices and the need to meet global food demand are further accelerating the adoption of plant-based protein feed solutions.

Fluctuations in raw material availability, particularly soybean and other key crops, pose significant challenges to the Feed Plant-based Protein market. Climate change, unpredictable weather patterns, and supply chain disruptions have led to variability in crop yields, impacting the consistent supply of plant-based proteins. For instance, soybean production can vary by up to 15% annually due to environmental factors, affecting feed manufacturing costs and availability. Additionally, competition between food-grade and feed-grade plant proteins further intensifies supply constraints. The reliance on a limited number of protein-rich crops also creates vulnerabilities in the supply chain, making it difficult for manufacturers to maintain stable production levels. These challenges necessitate the diversification of raw material sources and the development of alternative plant protein options.

Innovation in alternative protein sources such as pea protein, algae-based protein, and insect-derived plant blends is creating new growth opportunities in the Feed Plant-based Protein market. Emerging technologies in fermentation and bioprocessing are enabling the development of high-quality protein ingredients with improved amino acid profiles. For example, fermentation-based protein enhancement can increase protein digestibility by up to 20%, making it suitable for high-performance animal feed applications. The rising demand for aquaculture feed, particularly in Asia-Pacific, is driving the adoption of alternative protein sources that can replace traditional fishmeal. Furthermore, increasing investments in research and development are supporting the commercialization of novel plant protein ingredients, expanding the scope of applications across livestock and pet nutrition sectors.

Processing complexities and cost pressures remain significant challenges for the Feed Plant-based Protein market. Advanced protein extraction methods, such as enzymatic and fermentation-based processes, require substantial capital investment and technical expertise. These processes can increase production costs by up to 18%, limiting their adoption among small and medium-scale feed manufacturers. Additionally, the presence of anti-nutritional factors in plant proteins necessitates further processing to improve digestibility, adding to operational complexity. Regulatory compliance related to feed safety and quality standards also increases production costs and requires continuous monitoring. These factors collectively create barriers for market expansion, particularly in price-sensitive regions where cost efficiency is a critical determinant of adoption.

• Rapid Expansion of Fermentation-Enhanced Protein Technologies:

The adoption of microbial and precision fermentation technologies in feed plant-based protein production has increased by over 38% since 2022, significantly improving amino acid profiles and digestibility. Fermentation-enhanced soy and pea proteins have demonstrated up to 20% higher nutrient absorption rates compared to conventional processing methods. More than 45% of large-scale feed manufacturers have integrated fermentation units into their processing lines to reduce anti-nutritional factors by nearly 30%. This trend is particularly strong in Europe and North America, where regulatory frameworks encourage high-efficiency feed formulations and sustainable protein processing technologies.

• Increasing Substitution of Fishmeal with Plant-based Alternatives:

Global aquaculture feed producers are replacing fishmeal with plant-based protein sources at a rate exceeding 42%, driven by cost efficiency and sustainability concerns. Soy protein concentrate and pea protein now account for approximately 55% of protein inputs in aquaculture feed formulations. Studies indicate that replacing fishmeal with plant proteins can reduce feed costs by up to 28% while maintaining growth performance in species such as tilapia and shrimp. Asia-Pacific leads this transition, with over 60% of aquaculture farms adopting plant-based feed proteins to ensure scalability and supply stability.

• Integration of AI-Driven Precision Feed Formulation Systems:

The deployment of artificial intelligence in feed formulation has increased by nearly 33% among industrial feed producers, enabling real-time optimization of nutrient composition. AI-driven systems have demonstrated up to 18% improvement in feed conversion ratios and a 15% reduction in raw material wastage. More than 50% of Tier-1 feed companies are investing in predictive analytics tools to tailor plant-based protein blends according to species-specific nutritional requirements. This trend is enhancing operational efficiency and supporting data-driven decision-making in large-scale livestock and aquaculture operations.

• Rising Demand for Alternative Plant Protein Sources Beyond Soy:

The diversification toward non-soy plant proteins has grown by over 27%, with pea protein, canola meal, and sunflower meal gaining significant traction. Pea protein alone accounts for nearly 18% of new product development in feed protein formulations due to its favorable amino acid composition and lower allergen content. Additionally, over 35% of feed manufacturers are actively reducing dependence on soybean imports by incorporating regionally available protein crops. This shift is strengthening supply chain resilience while aligning with sustainability goals and regional agricultural policies.

The Feed Plant-based Protein market is segmented based on type, application, and end-user, reflecting diverse demand patterns across the global feed industry. By type, soybean-derived proteins dominate due to their high protein content and established processing infrastructure, while alternative proteins such as pea and canola are rapidly expanding their presence. In terms of application, livestock feed accounts for the largest share, driven by large-scale poultry and swine production, followed by aquaculture, which is witnessing accelerated adoption of plant-based proteins. End-user segmentation highlights commercial feed manufacturers as primary contributors, supported by increasing adoption among integrated farming operations and specialized aquaculture producers. The segmentation landscape is evolving with technological innovations, regional crop availability, and sustainability-driven shifts influencing product development and consumption patterns across key markets.

Soy-based proteins, including soybean meal and soy protein concentrates, dominate the Feed Plant-based Protein market with approximately 54% share, driven by their high protein content exceeding 44% and widespread availability. In comparison, pea protein accounts for nearly 18% of adoption, while canola-based proteins hold around 12%. However, pea protein is emerging as the fastest-growing segment, expanding at an estimated CAGR of 9.2% due to its non-GMO profile, improved digestibility, and reduced allergenic concerns.

Canola meal and sunflower meal collectively contribute about 16% of the market, serving as cost-effective alternatives in regions with limited soybean production. Additionally, emerging protein sources such as lupin and fava bean proteins are gaining niche traction, particularly in Europe, due to their compatibility with sustainable agriculture practices.

Livestock feed applications, particularly poultry and swine, account for nearly 62% of the Feed Plant-based Protein market, driven by the need for high-protein, cost-effective feed solutions. Aquaculture follows with approximately 26% share, reflecting rapid adoption of plant-based proteins to replace fishmeal. In comparison, pet food applications hold around 12%, supported by growing demand for plant-based nutrition in companion animals. Aquaculture is the fastest-growing application segment, expanding at an estimated CAGR of 8.8%, fueled by increasing global seafood consumption and the need for sustainable feed alternatives. Plant-based protein inclusion in aquaculture feed has reached over 50% in several commercial operations, particularly in Asia-Pacific. Other applications, including specialty animal feed and equine nutrition, collectively contribute the remaining share, with gradual adoption driven by cost and sustainability considerations.

Commercial feed manufacturers represent the leading end-user segment in the Feed Plant-based Protein market, accounting for approximately 58% of total demand due to their large-scale production capabilities and integrated supply chains. Integrated livestock farms contribute around 27%, leveraging plant-based proteins to optimize feed efficiency and reduce operational costs. Aquaculture producers account for nearly 15%, reflecting increasing adoption of plant-based feed solutions in fish and shrimp farming. Aquaculture producers are the fastest-growing end-user segment, expanding at an estimated CAGR of 9.5%, driven by rising seafood demand and regulatory pressure to reduce fishmeal usage. Over 60% of large aquaculture enterprises have transitioned to plant-based protein blends to ensure sustainable production practices. Other end-users, including small-scale farms and specialty feed producers, collectively contribute around 10–12% of the market, with adoption rates increasing steadily due to improved availability of cost-effective plant protein options.

Region North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2026 and 2033.

North America’s dominance is supported by high soybean processing volumes exceeding 120 million metric tons annually and over 65% adoption of plant-based protein feed in livestock operations. Europe follows with approximately 27% share, driven by stringent sustainability mandates and over 40% adoption of alternative protein feed solutions. Asia-Pacific holds around 29% share, with aquaculture consumption exceeding 55% of regional demand, particularly in China and India. South America contributes nearly 6%, supported by strong agricultural exports, while the Middle East & Africa account for approximately 4%, driven by increasing livestock production and feed imports. Regional investments in feed innovation have crossed USD 2 billion globally, with over 50% allocated toward sustainable protein processing technologies and alternative feed solutions.

North America holds approximately 34% share of the Feed Plant-based Protein market, driven by large-scale livestock farming and advanced feed manufacturing infrastructure. The poultry and swine industries account for over 70% of plant-based protein consumption in feed applications. Government support programs promoting sustainable agriculture and feed efficiency have resulted in over 45% adoption of environmentally optimized feed formulations. Regulatory frameworks emphasize reducing emissions from livestock, encouraging plant-based protein substitution. Technological advancements such as AI-driven feed formulation and precision nutrition systems have improved feed conversion efficiency by nearly 18%. Digital integration across feed mills has increased production efficiency by over 20%. A leading regional player, Archer Daniels Midland, has expanded its plant-based protein processing capacity by over 15% since 2023, focusing on high-protein soybean meal innovations. Consumer behavior in this region reflects a strong preference for efficiency-driven livestock production, with over 60% of producers prioritizing cost-effective and high-performance feed solutions.

Europe accounts for approximately 27% of the Feed Plant-based Protein market, with key countries such as Germany, France, and the UK leading adoption. Over 50% of feed manufacturers in the region have transitioned toward plant-based protein formulations to comply with sustainability regulations and reduce environmental impact. Regulatory initiatives targeting a 30% reduction in agricultural emissions by 2030 are accelerating demand for alternative protein sources. Technological adoption in Europe includes fermentation-based protein processing and enzyme-enhanced feed solutions, improving digestibility by up to 16%. Regional players such as Roquette have invested in expanding pea protein production, increasing output capacity by over 20% to meet growing demand. Consumer behavior reflects a strong inclination toward environmentally sustainable feed practices, with over 48% of producers prioritizing low-carbon protein sourcing and traceability in feed supply chains.

Asia-Pacific ranks as the fastest-growing region in the Feed Plant-based Protein market, accounting for nearly 29% of total volume consumption. China, India, and Japan are the top consuming countries, collectively contributing over 65% of regional demand. Aquaculture dominates application usage, representing more than 55% of plant-based protein feed consumption in the region. The region is witnessing rapid expansion in feed manufacturing infrastructure, with over 30% increase in processing facilities since 2022. Technological trends include automated feed formulation systems and fermentation-based protein enhancement, improving feed efficiency by up to 14%. A prominent regional player, Wilmar International, has expanded its soybean crushing capacity by over 18% to support feed protein production. Consumer behavior is driven by large-scale livestock and aquaculture operations, with over 60% of producers focusing on cost-effective and scalable feed solutions to meet rising protein demand.

South America accounts for approximately 6% of the Feed Plant-based Protein market, with Brazil and Argentina serving as key contributors due to their strong soybean production capabilities. Brazil alone produces over 150 million metric tons of soybeans annually, supporting large-scale feed protein manufacturing. The region benefits from favorable trade policies and export-oriented agricultural practices, with over 40% of soybean output directed toward feed applications. Infrastructure improvements in feed processing and storage have increased production efficiency by nearly 12% over recent years. Local players such as Cargill have expanded feed production facilities in Brazil, enhancing capacity by over 10% to meet domestic and export demand. Consumer behavior in the region is closely tied to agricultural output, with livestock producers prioritizing cost-effective protein sources and scalable feed solutions to support export-driven meat production industries.

The Middle East & Africa region accounts for approximately 4% of the Feed Plant-based Protein market, with demand driven by increasing livestock production and reliance on imported feed proteins. Countries such as the UAE and South Africa are leading growth, with feed consumption increasing by over 9% annually in key livestock sectors. Technological modernization in feed production has led to a 10% improvement in feed efficiency through the adoption of automated processing systems. Trade partnerships with major agricultural exporters are strengthening supply chains, ensuring consistent availability of plant-based protein feed ingredients. A regional player in South Africa has implemented advanced feed blending technologies, improving protein utilization rates by 13%. Consumer behavior reflects a focus on cost optimization and supply reliability, with over 55% of feed producers prioritizing stable imports and efficient feed formulations to support livestock productivity.

United States – 28% share in the Feed Plant-based Protein market, driven by high soybean processing capacity and advanced feed manufacturing technologies.

China – 22% share in the Feed Plant-based Protein market, supported by large-scale aquaculture production and strong demand for cost-efficient feed protein solutions.

The Feed Plant-based Protein market exhibits a moderately consolidated competitive structure, with the top five companies accounting for approximately 52% of the global market share. Over 40 active global and regional players are operating across the value chain, ranging from raw material processing to advanced protein formulation. Key market participants are focusing on capacity expansion, product innovation, and strategic partnerships to strengthen their competitive positioning.

Recent trends indicate that over 35% of leading companies have invested in fermentation-based protein technologies to enhance product quality and reduce processing costs. Mergers and acquisitions have increased by nearly 18% since 2022, reflecting consolidation strategies aimed at expanding geographic reach and product portfolios. Additionally, more than 50% of companies are integrating digital solutions such as AI-driven feed optimization platforms to improve operational efficiency and customer value propositions.

Innovation remains a key differentiator, with over 25% of new product launches focused on alternative plant proteins such as pea and canola. Strategic collaborations between agritech firms and feed manufacturers have improved supply chain efficiency by up to 15%. The competitive landscape is further shaped by sustainability initiatives, with over 45% of companies committing to reducing carbon emissions in feed production processes, reinforcing long-term market competitiveness.

Archer Daniels Midland Company

Cargill Incorporated

Bunge Limited

Wilmar International Limited

Roquette Frères

Ingredion Incorporated

Kerry Group plc

Glanbia plc

DSM-Firmenich

AGT Food and Ingredients

Burcon NutraScience Corporation

Sotexpro

Axiom Foods Inc.

Emsland Group

Technological advancements in the Feed Plant-based Protein market are transforming production efficiency, nutritional optimization, and supply chain resilience. One of the most impactful innovations is enzymatic processing, which has improved protein digestibility by up to 18% by reducing anti-nutritional factors such as phytates and trypsin inhibitors. This technology is now implemented in over 40% of large-scale feed processing facilities, particularly for soybean and canola meal enhancement. Precision fermentation is another rapidly expanding technology, enabling the modification of plant proteins at a molecular level. This process enhances amino acid profiles and increases bioavailability by approximately 20%, making plant-based feed proteins more competitive with traditional animal-derived alternatives. Additionally, microbial fermentation platforms are being integrated into over 35% of new feed protein production units globally, particularly in Europe and North America.

Artificial intelligence and machine learning are playing a critical role in optimizing feed formulations. AI-driven platforms can analyze over 100 variables, including animal species, growth stage, and environmental conditions, resulting in up to 15% improvement in feed conversion ratios and a 12% reduction in feed waste. More than 50% of Tier-1 feed manufacturers are now deploying digital feed optimization tools to enhance operational efficiency and product performance. Extrusion and thermal processing technologies are also evolving, with high-temperature short-time (HTST) processing reducing microbial contamination by over 95% while preserving protein integrity. Furthermore, advancements in protein isolation techniques, such as membrane filtration and dry fractionation, are enabling the extraction of protein concentrates with purity levels exceeding 75%. These technologies collectively support the development of high-performance, sustainable, and cost-efficient feed plant-based protein solutions tailored for modern livestock and aquaculture systems.

• In March 2025, Archer Daniels Midland Company expanded its Decatur, Illinois facility to enhance soy protein concentrate production capacity by over 20%, supporting growing demand for high-performance animal feed ingredients and improving supply chain efficiency across North American livestock and aquaculture sectors. Source: www.adm.com

• In September 2024, Roquette announced the expansion of its pea protein production site in Vic-sur-Aisne, France, increasing capacity by approximately 30% to address rising demand for sustainable plant-based feed proteins in Europe and global markets. Source: www.roquette.com

• In July 2025, Cargill Incorporated introduced a new line of enzyme-treated soybean meal designed to improve digestibility by up to 15% in poultry feed, enhancing nutrient absorption and supporting more efficient feed utilization across large-scale farming operations. Source: www.cargill.com

• In November 2024, Wilmar International Limited increased its soybean crushing capacity in China by over 18%, strengthening its feed protein supply chain and supporting the growing demand for plant-based protein ingredients in aquaculture and livestock industries across Asia-Pacific. Source: www.wilmar-international.com

The Feed Plant-based Protein Market Report provides a comprehensive evaluation of key industry segments, technological advancements, and regional dynamics shaping the global market landscape. The report covers multiple product categories, including soybean meal, pea protein, canola meal, sunflower meal, and emerging protein sources such as lupin and fava bean, which collectively contribute to over 90% of total plant-based feed protein consumption.

From an application perspective, the report analyzes livestock feed, aquaculture feed, and pet nutrition, with livestock accounting for more than 60% of total demand, followed by aquaculture at approximately 25%. The scope further includes a detailed assessment of end-user segments such as commercial feed manufacturers, integrated farms, and aquaculture producers, highlighting their respective adoption patterns and operational requirements.

Geographically, the report evaluates five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing 100% of global consumption. Asia-Pacific alone contributes nearly 30% of total feed protein demand, driven by large-scale aquaculture and livestock production, while North America leads in technological adoption and processing capabilities.

The report also examines key technologies such as fermentation, enzymatic processing, AI-driven feed optimization, and advanced protein extraction methods, which are currently adopted by over 50% of leading manufacturers. Additionally, it explores emerging trends such as alternative protein diversification, sustainability-driven sourcing, and digital transformation in feed production. This structured analysis enables stakeholders to identify growth opportunities, optimize supply chains, and align with evolving regulatory and environmental standards.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Archer Daniels Midland Company, Cargill Incorporated, Bunge Limited, Wilmar International Limited, Roquette Frères, Ingredion Incorporated, Kerry Group plc, Glanbia plc, DSM-Firmenich, AGT Food and Ingredients, Burcon NutraScience Corporation, Sotexpro, Axiom Foods Inc., Emsland Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |