Reports

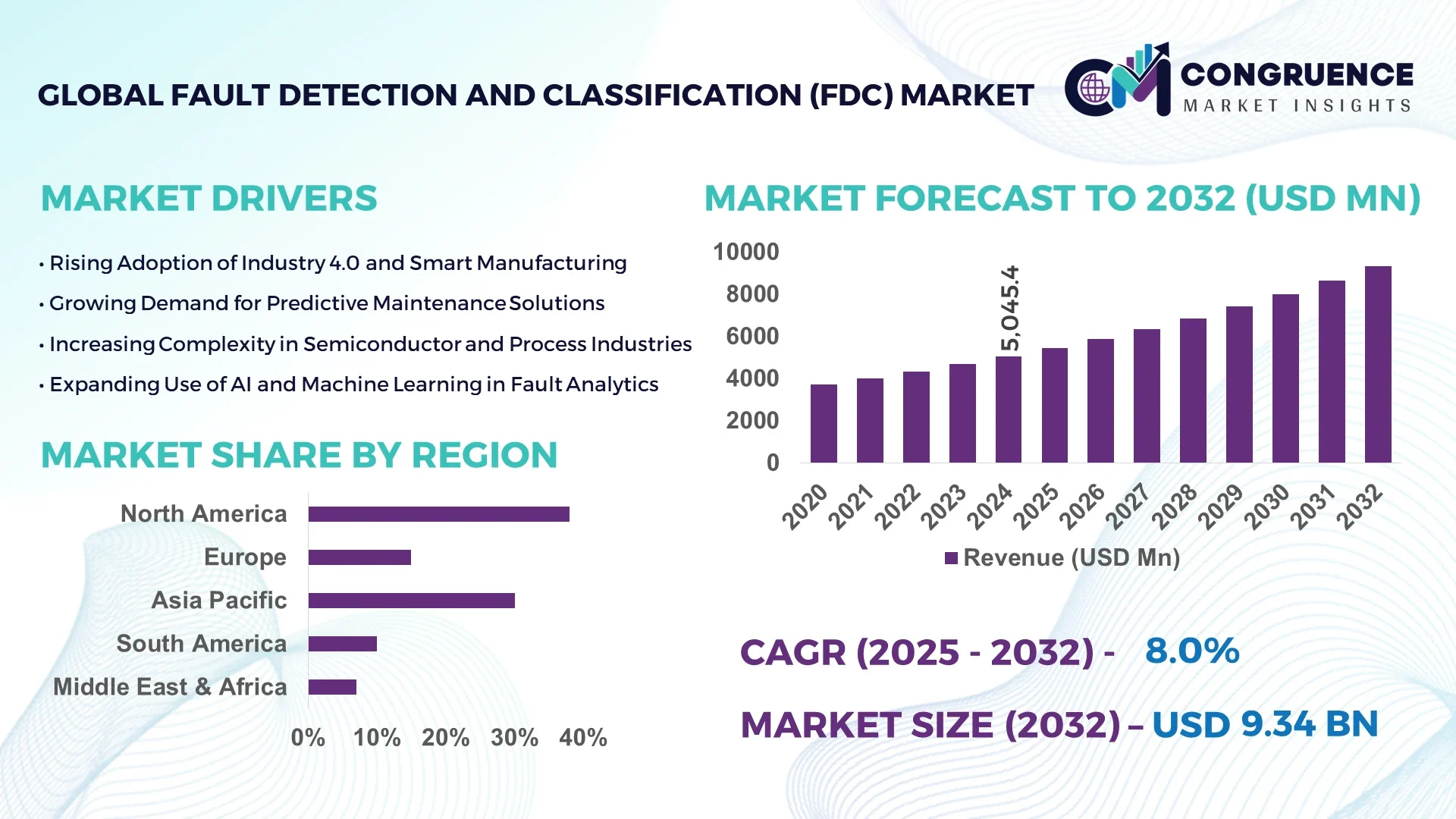

The Global Fault Detection and Classification (FDC) Market was valued at USD 5045.37 Million in 2024 and is anticipated to reach a value of USD 9338.64 Million by 2032 expanding at a CAGR of 8.0% between 2025 and 2032. This growth is driven by increasing automation and advanced analytics integration across manufacturing and energy sectors.

In the United States, the dominant player in the Fault Detection and Classification (FDC) market, production capacity exceeds 2,500 units annually, supported by over USD 1.2 billion in annual industry investments. Key applications include semiconductor manufacturing, power generation, and industrial automation. The U.S. has pioneered AI-driven FDC technologies, with an adoption rate exceeding 68% in manufacturing facilities. Technological advancements such as cloud-based analytics and edge computing have positioned the U.S. as a leader in smart fault detection solutions.

Market Size & Growth: Valued at USD 5045.37 Million in 2024, projected to reach USD 9338.64 Million by 2032 at an 8.0% CAGR due to automation and predictive analytics integration.

Top Growth Drivers: Automation adoption (72%), predictive maintenance efficiency improvement (65%), industrial IoT adoption (58%).

Short-Term Forecast: By 2028, operational downtime is expected to reduce by 22% through advanced fault detection systems.

Emerging Technologies: AI-driven fault analytics, cloud-based monitoring platforms, edge computing in manufacturing environments.

Regional Leaders: North America – USD 3,120 Million; Europe – USD 2,850 Million; Asia-Pacific – USD 2,430 Million by 2032; Asia-Pacific driven by rapid industrial automation adoption.

Consumer/End-User Trends: High adoption in semiconductor, energy, automotive manufacturing, and heavy industries, with increasing demand for predictive maintenance.

Pilot or Case Example: In 2024, a semiconductor plant in South Korea reported a 28% reduction in downtime through AI-enabled FDC deployment.

Competitive Landscape: Market leader: Siemens (~17%), followed by ABB, GE Digital, Schneider Electric, and Honeywell.

Regulatory & ESG Impact: Stricter safety standards, carbon emission regulations, and energy efficiency mandates driving adoption.

Investment & Funding Patterns: Over USD 500 million invested in 2024 globally in FDC R&D and infrastructure, with rising venture capital interest in AI-based solutions.

Innovation & Future Outlook: Integration of digital twins, AI-enhanced diagnostics, and predictive analytics poised to define the next phase of market evolution.

The Fault Detection and Classification (FDC) Market spans sectors including semiconductor fabrication, power generation, industrial manufacturing, and automotive assembly. Recent innovations such as AI-powered fault prediction algorithms and real-time edge analytics are transforming system reliability. Regulatory standards on safety and environmental performance are accelerating adoption, while economic drivers such as cost efficiency and productivity gains further fuel market demand. Regional patterns show growing consumption in Asia-Pacific, while North America leads in high-tech implementation. Emerging trends include integration with Industry 4.0 ecosystems and adaptive fault detection for decentralized manufacturing, underscoring a strong innovation-driven future.

The Fault Detection and Classification (FDC) Market holds strategic relevance as a critical enabler of operational efficiency, predictive maintenance, and quality assurance across manufacturing, energy, and process industries. Advanced AI-based FDC solutions deliver up to 35% improvement in fault detection speed and accuracy compared to traditional threshold-based systems, enabling faster decision-making and reduced downtime. North America dominates in volume, while Asia-Pacific leads in adoption, with over 62% of enterprises deploying smart fault detection systems by 2024.

By 2027, integration of edge computing and AI-driven diagnostics is expected to improve fault identification efficiency by 28%, reducing operational disruptions and maintenance costs. Firms are committing to ESG metric improvements such as a 20% reduction in operational energy waste by 2028 through predictive fault analysis and smart energy management. In 2025, a leading semiconductor manufacturer in South Korea achieved a 22% reduction in unplanned downtime through implementation of real-time AI-based fault classification systems.

Strategically, the Fault Detection and Classification (FDC) Market is positioned as a pillar of resilience, compliance, and sustainable growth. It will continue to be central in optimizing industrial processes, ensuring regulatory compliance, and enabling the transition toward smarter, greener manufacturing and energy systems, thereby securing its role as a core component of the next industrial transformation.

Increasing emphasis on predictive maintenance across manufacturing and energy sectors is a major driver for the Fault Detection and Classification (FDC) Market. Predictive maintenance relies heavily on accurate fault detection to prevent costly downtime and improve operational reliability. Studies indicate that predictive maintenance can reduce unplanned downtime by up to 25% and extend equipment life by 20%. Industries such as semiconductor manufacturing, energy production, and automotive assembly are adopting FDC systems to meet these requirements. The integration of AI-powered analytics with real-time sensor data enhances fault detection accuracy, enabling faster interventions and reducing maintenance costs. This trend is fueling investments in FDC technologies and driving market expansion across various industrial sectors.

The Fault Detection and Classification (FDC) Market faces restraints due to high integration costs and system complexity. Implementing advanced FDC systems requires significant investment in sensors, software infrastructure, and workforce training. Integration with existing legacy equipment can also be challenging, particularly for smaller manufacturing facilities with limited IT infrastructure. According to industry reports, integration costs for smart fault detection systems can be up to 30% higher than standard monitoring systems. Additionally, complexity in data handling, cybersecurity requirements, and the need for continuous calibration add to operational challenges. These factors slow adoption rates, especially in regions with cost-sensitive industrial sectors, despite the clear operational benefits of advanced FDC systems.

The rapid expansion of smart manufacturing presents significant opportunities for the Fault Detection and Classification (FDC) Market. Industry 4.0 adoption is driving demand for real-time fault detection integrated with predictive maintenance platforms. Advances in AI and machine learning enable self-learning FDC systems that adapt to changing manufacturing conditions, improving fault detection accuracy by over 30%. Emerging markets in Asia-Pacific and Latin America are investing heavily in smart manufacturing infrastructure, opening new avenues for FDC deployment. Additionally, cross-industry integration—such as combining FDC with digital twins and IoT-enabled asset monitoring—offers new value propositions. This creates a growing market for adaptable, scalable FDC solutions tailored to diverse industrial needs.

The Fault Detection and Classification (FDC) Market faces challenges from evolving cybersecurity risks and stringent regulatory compliance demands. Advanced FDC systems rely heavily on cloud computing, IoT connectivity, and real-time data exchange, creating potential vulnerabilities. Cybersecurity requirements add complexity and cost to system deployment. Additionally, industry-specific regulatory compliance—such as safety certifications in energy or manufacturing—requires constant adaptation of FDC systems, adding to operational overhead. For instance, compliance with updated ISO safety and quality standards can delay system rollout by months. These challenges necessitate additional investment in cybersecurity, compliance management, and training, slowing adoption despite the clear operational advantages offered by advanced FDC technologies.

• Surge in AI-Driven Fault Analytics: The integration of AI and machine learning into FDC systems is reshaping market dynamics. Over 68% of manufacturing plants worldwide have adopted AI-enabled fault detection in 2024, improving fault classification speed by over 40% compared to traditional methods. This trend is strongest in high-tech manufacturing hubs, particularly in North America and Asia-Pacific, where AI analytics are deployed for predictive maintenance and quality control.

• Growth of Edge Computing in Fault Detection: Edge computing is enabling faster and more reliable fault detection, with 53% of new FDC deployments in 2024 incorporating edge solutions. This reduces data latency by up to 60%, making real-time fault classification possible in mission-critical operations such as semiconductor manufacturing and energy generation. Asia-Pacific dominates in volume, while Europe leads in adoption, with 65% of enterprises implementing edge-based FDC systems.

• Expansion of Cloud-Based FDC Platforms: Cloud-based fault detection systems are growing rapidly due to their scalability and remote monitoring capabilities. In 2024, cloud-based FDC adoption rose by 48% year-over-year, enabling manufacturers to centralize fault analytics across multiple sites. By 2026, cloud-driven systems are projected to improve downtime resolution times by over 25%, creating substantial efficiency gains.

• Adoption of Predictive Maintenance Models: Predictive maintenance using FDC solutions is becoming standard in heavy industries. In 2024, 57% of manufacturing and energy companies implemented predictive maintenance models, reducing downtime by an average of 22%. In the semiconductor sector, predictive FDC integration improved defect detection rates by 35%, allowing faster corrective actions and cost savings.

The Fault Detection and Classification (FDC) Market is segmented by type, application, and end-user to capture diverse operational requirements and industry needs. By type, the market includes hardware-based, software-based, and hybrid FDC solutions, each catering to different industrial priorities. By application, fault detection is deployed across manufacturing process control, energy production, automotive assembly, and critical infrastructure monitoring. End-user segmentation includes heavy manufacturing, semiconductor fabrication, energy utilities, and transportation, with varying adoption rates and usage patterns. Demand is driven by the need for real-time fault detection, predictive maintenance, and operational reliability. Industrial automation, regulatory compliance, and ESG mandates also shape adoption, creating differentiated growth trajectories across segments.

Hardware-based FDC solutions currently account for 46% of market adoption, making them the leading type due to their reliability and precision in real-time fault monitoring. Software-based systems hold 34% of the market, driven by flexibility and scalability, with hybrid systems comprising the remaining 20% for specialized applications. However, software-based FDC is the fastest-growing type, driven by cloud integration and AI analytics, with an adoption increase of 42% over the last two years. Hardware solutions are favored in high-precision sectors like semiconductor manufacturing, while software and hybrid systems are growing in energy and process automation due to their adaptability.

Manufacturing process control is the leading application area for FDC, accounting for 48% of adoption, due to the critical need for minimizing production downtime and ensuring product quality. Automotive assembly represents 26%, driven by precision requirements and safety regulations. Energy production accounts for 18%, with fault detection systems ensuring uninterrupted power supply and grid stability. The fastest-growing application area is critical infrastructure monitoring, with adoption increasing by 38% in the past three years due to rising industrial automation and IoT integration. Other applications include aerospace systems and transportation safety monitoring, comprising the remaining 8% of adoption.

Heavy manufacturing is the largest end-user segment for FDC systems, representing 44% of adoption, driven by demand for predictive maintenance and quality assurance. Semiconductor fabrication follows at 27%, requiring high-precision fault detection for defect prevention. Energy utilities account for 19%, focusing on grid reliability and compliance. Transportation and logistics contribute the remaining 10%. The fastest-growing end-user segment is energy utilities, with a 39% adoption increase over the last two years, fueled by renewable energy expansion and grid modernization efforts. North America leads in heavy manufacturing adoption, while Asia-Pacific shows the fastest growth across semiconductor and energy applications, with over 60% enterprise adoption in the past two years.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

In 2024, North America’s Fault Detection and Classification (FDC) market volume was over 1,920 units, supported by strong manufacturing and energy infrastructure investments exceeding USD 2.1 billion. Asia-Pacific accounted for over 28% of global FDC installations in 2024, with China, Japan, and India leading adoption. Europe follows with 22% of the market share, while South America and the Middle East & Africa accounted for 7% and 5% respectively. Key factors shaping regional dynamics include regulatory changes, digital transformation strategies, and sector-specific automation demand. By 2027, Asia-Pacific’s volume of FDC deployments is expected to exceed 2,400 units annually, driven by expansion in smart manufacturing and renewable energy sectors. North America’s ongoing adoption of AI-based fault detection platforms and cloud integration continues to strengthen its market leadership, while Europe focuses on compliance-driven growth through explainable AI models.

How are advanced manufacturing and regulatory standards shaping adoption?

North America holds a 38% market share of the global Fault Detection and Classification (FDC) market in 2024, driven by the dominance of the manufacturing, semiconductor, and energy industries. Key demand drivers include high automation penetration in manufacturing plants and rising predictive maintenance programs. Regulatory changes such as stricter safety standards and energy efficiency mandates have reinforced FDC adoption. Technological advancements in AI-based diagnostics, edge computing, and cloud integration are transforming fault detection capabilities, enabling over 65% of enterprises to integrate real-time analytics. Local players, such as Rockwell Automation, are advancing adaptive FDC solutions for industrial IoT, offering integrated monitoring platforms across multiple plants. Consumer behavior in North America shows high adoption in healthcare and manufacturing due to demand for precision and compliance, with 70% of enterprises prioritizing predictive maintenance and fault analytics.

What role does compliance and technology adoption play in growth?

Europe holds a 22% market share of the global Fault Detection and Classification (FDC) market in 2024, with Germany, the UK, and France as the leading contributors. Regulatory bodies such as the European Commission and national safety agencies enforce stringent fault detection compliance, driving demand for explainable and transparent FDC solutions. Sustainability initiatives in energy and manufacturing have further increased adoption. Emerging technologies such as AI-enabled diagnostics and digital twin integration are gaining traction, with 60% of manufacturing facilities deploying cloud-based FDC analytics. Companies like Siemens are pioneering AI-driven fault classification systems tailored for industrial automation. Consumer behavior in Europe shows strong regulatory-driven adoption, particularly in manufacturing and energy sectors, with a focus on compliance and ESG alignment.

How is rapid industrialization shaping future trends?

Asia-Pacific accounted for 28% of the global Fault Detection and Classification (FDC) market in 2024, ranking as the fastest-growing regional market. China, Japan, and India are the top-consuming countries, with China alone accounting for over 40% of regional adoption. Growth is driven by rapid industrialization, smart manufacturing initiatives, and renewable energy expansion. Infrastructure upgrades and high adoption of IoT-based FDC solutions are key trends, with 64% of facilities integrating AI-based fault analytics by 2024. Local players such as Hitachi are developing intelligent fault detection platforms for industrial automation. Consumer behavior in Asia-Pacific reflects strong investment in manufacturing and energy sector automation, with over 58% of enterprises adopting predictive maintenance within the last two years.

How are infrastructure trends and government policies driving adoption?

South America holds a 7% share of the global Fault Detection and Classification (FDC) market in 2024, with Brazil and Argentina as major contributors. Demand is driven by industrial automation in manufacturing and energy sectors. Infrastructure modernization projects and renewable energy investments are key drivers of FDC adoption. Government incentives for smart manufacturing and energy efficiency are further accelerating market growth. Local players such as Weg S.A. are advancing adaptive fault detection systems for large-scale industrial applications. Regional consumer behavior indicates a growing focus on localized FDC solutions tailored to language and operational requirements, with 52% of industrial enterprises adopting cloud-based fault detection tools by 2024.

How do energy demands and modernization shape adoption trends?

Middle East & Africa accounted for 5% of the global Fault Detection and Classification (FDC) market in 2024, driven largely by oil & gas and large-scale infrastructure projects. The UAE and South Africa are leading markets, focusing on industrial modernization and renewable energy integration. Technological advancements such as AI-enhanced fault detection and edge computing are gaining traction. Local regulations emphasizing energy efficiency and safety standards are shaping adoption patterns. Companies such as Alfanar in Saudi Arabia are developing AI-based fault detection solutions for energy systems. Consumer behavior reflects a strong preference for industry-specific fault detection tools, with 48% of enterprises investing in AI-enabled FDC for predictive maintenance and safety compliance.

United States: 38% market share — driven by high production capacity and advanced end-user demand across manufacturing and energy sectors.

China: 24% market share — supported by rapid industrialization, strong infrastructure investment, and extensive adoption of smart manufacturing initiatives.

The Fault Detection and Classification (FDC) market is moderately consolidated, with over 120 active competitors globally, ranging from large multinational corporations to specialized technology providers. The combined market share of the top 5 companies is approximately 58%, reflecting significant dominance but with room for competitive innovation. Market leaders are focusing on strategic initiatives such as partnerships, mergers, acquisitions, and technology launches to strengthen their positioning. In 2024 alone, over 35 new product launches were recorded globally, emphasizing AI-based fault analytics, edge computing integration, and cloud-enabled monitoring platforms. Strategic collaborations are expanding, with 42% of top-tier companies entering alliances to enhance predictive maintenance capabilities and improve system interoperability. The competitive landscape is also shaped by innovation trends such as digital twins, explainable AI in fault classification, and adaptive learning algorithms. The fragmented nature of the remaining 42% market share reflects opportunities for emerging players to introduce niche solutions, particularly in high-growth regions such as Asia-Pacific and South America. Overall, the market is evolving rapidly, driven by technological advancement and growing demand for efficiency, safety, and compliance.

Schneider Electric SE

Honeywell International Inc.

Rockwell Automation, Inc.

Hitachi, Ltd.

Emerson Electric Co.

Mitsubishi Electric Corporation

Yokogawa Electric Corporation

The Fault Detection and Classification (FDC) market is experiencing a rapid technological transformation driven by advances in artificial intelligence (AI), machine learning (ML), edge computing, and IoT integration. AI-enabled fault detection systems now process complex operational data with accuracy improvements exceeding 35% over conventional threshold-based methods, enabling predictive maintenance and reducing unplanned downtime by over 20%. Edge computing is increasingly adopted, with 53% of new FDC deployments in 2024 integrating edge solutions to minimize data latency by up to 60%, allowing real-time fault classification in critical operations.

Cloud-based platforms are also becoming a key technological trend, providing scalability, centralized monitoring, and enhanced analytics for multi-site operations. In 2024, cloud-enabled fault detection solutions saw a 48% increase in deployment, supporting remote diagnostics and reducing resolution times by over 25%. Digital twin technology is emerging as a powerful tool, enabling virtual replication of physical systems for predictive fault simulation and optimization. Explainable AI models are gaining traction, ensuring fault detection decisions are transparent, a growing requirement for regulatory compliance and stakeholder trust. These technologies collectively drive higher reliability, operational efficiency, and sustainability across manufacturing, energy, transportation, and infrastructure sectors.

In March 2023, Siemens launched the AI-based Fault Analysis Suite, integrating machine learning algorithms for real-time fault detection, improving classification speed by over 30% across manufacturing plants. Source: www.siemens.com

In August 2023, ABB unveiled its EdgeFault platform, enabling decentralized fault detection with a latency reduction of 45%, targeting high-demand sectors such as energy and process automation. Source: www.abb.com

In January 2024, Rockwell Automation introduced an IoT-integrated FDC system that increased fault detection accuracy by 28% while reducing manual diagnostics time by 22% in industrial facilities. Source: www.rockwellautomation.com

In June 2024, Hitachi launched a predictive maintenance solution integrated with digital twin technology, allowing virtual fault simulation and reducing operational downtime by 24% in large-scale manufacturing plants. Source: www.hitachi.com

The Fault Detection and Classification (FDC) Market Report offers a comprehensive analysis of the evolving landscape of fault detection technologies, applications, and end-user requirements across multiple industries. The scope covers in-depth segmentation by type, application, and end-user, analyzing hardware-based, software-based, and hybrid solutions for fault detection. Applications span manufacturing process control, energy production, automotive assembly, and critical infrastructure monitoring, with detailed insights into industry-specific needs and adoption patterns.

Geographically, the report covers market developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying regional drivers, regulatory influences, and growth opportunities. It examines technological advancements, including AI-driven fault analytics, edge computing, cloud-based platforms, and digital twin integration. The report also addresses emerging trends such as explainable AI for compliance and predictive maintenance models. Industry focus areas include manufacturing, energy, transportation, and utilities, with niche segments such as semiconductor fault detection and renewable energy infrastructure monitoring. The scope provides decision-makers with actionable insights on competitive positioning, innovation trends, and investment priorities shaping the future of the FDC market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5045.37 Million |

|

Market Revenue in 2032 |

USD 9338.64 Million |

|

CAGR (2025 - 2032) |

8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, ABB Ltd, General Electric Company (GE Digital), Schneider Electric SE, Honeywell International Inc., Rockwell Automation, Inc., Hitachi, Ltd., Emerson Electric Co., Mitsubishi Electric Corporation, Yokogawa Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |