Reports

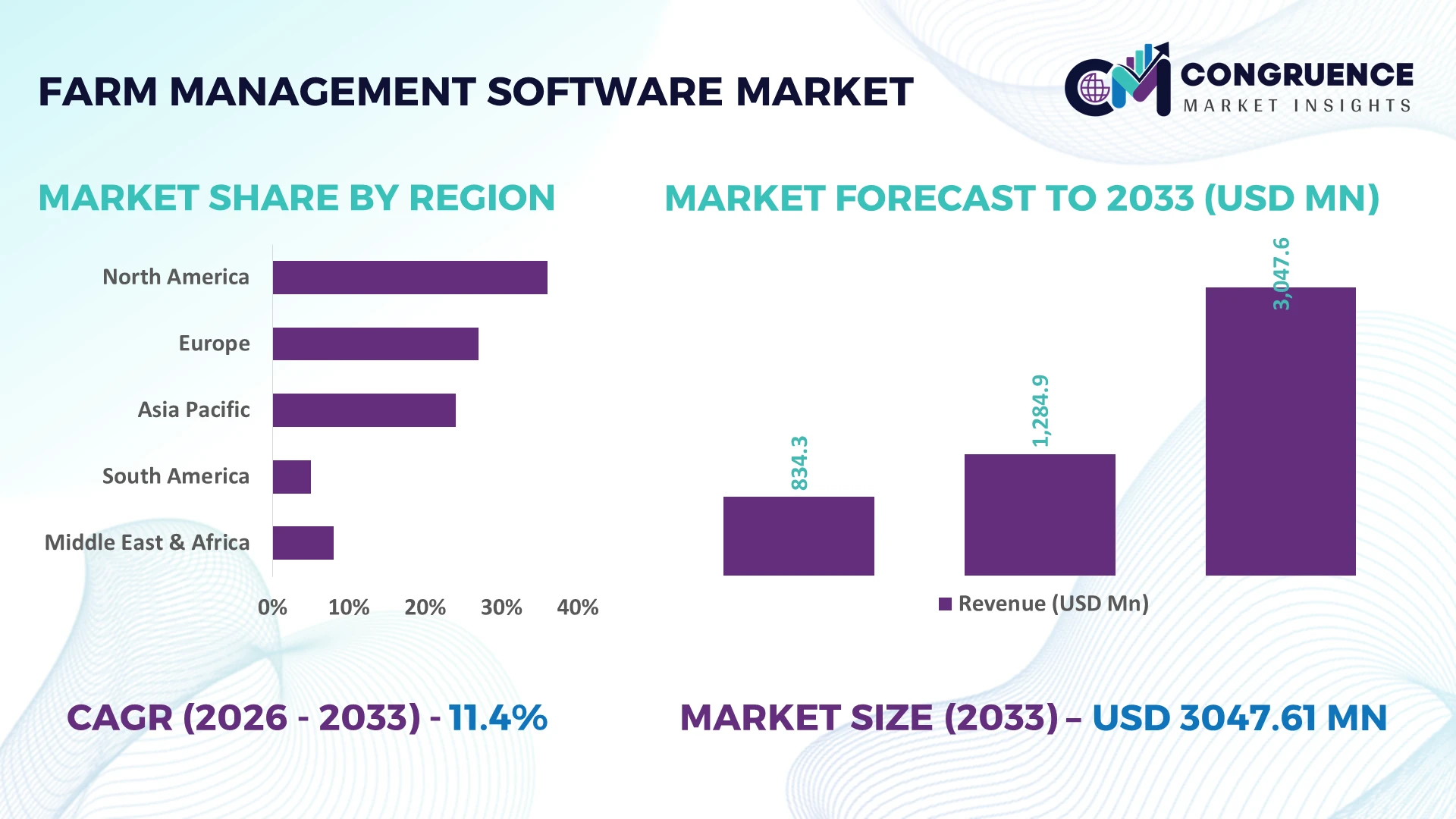

The Global Farm Management Software Market was valued at USD 1284.92 Million in 2025 and is anticipated to reach a value of USD 3047.61 Million by 2033 expanding at a CAGR of 11.4% between 2026 and 2033. Growth is driven by AI-powered precision agriculture, satellite-based field monitoring, connected farm equipment, and regulatory demand for digital traceability across commercial farming operations.

The United States remains the dominant market, accounting for approximately 34% of global software adoption, supported by over USD 2 billion in digital agriculture initiatives, widespread precision farming deployment, and advanced IoT connectivity across large-scale farms. In comparison, China is accelerating adoption through smart agriculture programs, with digital farming technologies expanding across more than 25% of large commercial cultivation areas by 2026. Rising food security priorities following ongoing geopolitical supply-chain disruptions have further strengthened software implementation across major agricultural economies.

The market favors technology providers delivering interoperable platforms, predictive analytics, and measurable productivity gains across diversified farming operations.

Market Size & Growth: USD 1284.92 million (2025) to USD 3047.61 million (2033) at 11.4% CAGR, driven by AI-enabled precision farming and connected equipment integration.

Top Growth Drivers: Precision agriculture adoption exceeds 28%, cloud deployment surpasses 45%, and IoT-enabled farm equipment connectivity expands by over 22%.

Short-Term Forecast: By 2028, digital farm planning reduces input costs by nearly 18% while improving operational efficiency by approximately 21%.

Emerging Technologies: AI analytics, satellite imagery, machine learning, and autonomous equipment optimize irrigation, fertilization, and crop performance with faster decision-making.

Regional Leaders: North America exceeds USD 1.0 billion, Europe approaches USD 820 million, and Asia-Pacific surpasses USD 760 million, supported by expanding smart farming programs.

Consumer/End-User Trends: Nearly 58% of large commercial farms prioritize integrated software combining financial management, field monitoring, and compliance reporting.

Pilot/Case Example: In 2026, a precision farming deployment improved fertilizer efficiency by 19% and reduced irrigation consumption by 16%.

Competitive Landscape: Leading vendors collectively control approximately 41% of the market, with Deere, Trimble, Bayer, AGCO, and Topcon driving platform innovation.

Regulatory & ESG Impact: Digital compliance tools reduce reporting time by nearly 30% while supporting sustainability targets and agricultural traceability requirements.

Investment & Funding: More than USD 1.4 billion supports strategic partnerships, agricultural AI platforms, and regional expansion amid resilient food supply-chain modernization.

Innovation & Future Outlook: Predictive analytics, autonomous operations, and digital twins accelerate next-generation farm management while strengthening enterprise-wide decision intelligence.

Farm Management Software Market demand is expanding across precision crop production, livestock management, greenhouse operations, and large-scale agribusinesses seeking measurable productivity improvements. AI-driven decision support, remote sensing, and predictive agronomic analytics are becoming standard capabilities, while cloud-based platforms report workflow efficiency gains exceeding 20%. Growing digital traceability requirements and resilient agricultural supply-chain planning are reinforcing enterprise software adoption, setting the stage for broader strategic market developments.

Farm management software has become a strategic digital asset as agricultural producers prioritize productivity, input optimization, and operational resilience amid climate variability and tightening food traceability requirements. The market is benefiting from accelerated digital adoption, stricter sustainability reporting, and supply-chain restructuring that encourages real-time visibility across cultivation, storage, and distribution. Investors increasingly favor integrated platforms capable of combining agronomic, financial, and environmental intelligence within a single operating environment.

Modern AI-enabled farm management platforms process field data up to 40% faster than conventional spreadsheet-based systems while reducing manual recordkeeping by approximately 55%, enabling quicker agronomic decisions and stronger compliance management. The United States leads large-scale enterprise deployment through highly mechanized farming, whereas Australia emphasizes remote monitoring technologies across extensive agricultural land with lower labor intensity. Over the next two to three years, connected equipment integration is expected to exceed 60% among large commercial farms, strengthening predictive planning and resource optimization.

A practical example includes integrated irrigation platforms that combine weather forecasting, soil sensors, and satellite imagery to reduce water consumption by nearly 18% while improving crop planning accuracy. Technology providers are expanding partnerships with equipment manufacturers, cloud infrastructure companies, and agricultural cooperatives to strengthen platform interoperability. Organizations that build scalable digital ecosystems with advanced analytics, automation, and seamless data exchange will secure stronger competitive positioning and long-term operational resilience.

Precision agriculture is becoming the primary structural driver as commercial farms pursue measurable improvements in productivity, resource efficiency, and regulatory compliance. More than 52% of large farming enterprises now integrate digital decision-support tools, while AI-assisted crop monitoring improves field scouting efficiency by approximately 30% and connected sensor deployment has expanded by nearly 25% across high-value crop operations. The United States continues strengthening digital agriculture through precision farming initiatives and advanced equipment connectivity. This shift enables faster agronomic decisions, optimized fertilizer allocation, and improved operational planning. Technology providers are responding through cloud platform expansion, strategic equipment partnerships, and AI innovation, creating integrated ecosystems that improve customer retention while establishing long-term competitive differentiation.

Interoperability limitations continue restricting enterprise-scale implementation because many farms operate equipment from multiple manufacturers using incompatible software environments. Approximately 46% of agricultural businesses report data integration challenges, while legacy machinery represents nearly 40% of installed farm equipment in several mature agricultural markets. Rural connectivity gaps remain another operational constraint, particularly across parts of India and Latin America, reducing the effectiveness of cloud-based platforms. These structural limitations increase deployment costs, delay workflow automation, and reduce return on digital investments. Companies are addressing these issues through open API development, localized deployment models, and strategic collaborations with telecommunications providers to improve platform compatibility and operational scalability.

The strongest opportunity lies in expanding intelligent farm management ecosystems across emerging agricultural economies where mechanization and digital adoption continue accelerating. Government-backed smart agriculture initiatives have increased precision farming deployment by over 20% in China, while cloud-based agricultural platforms have recorded user growth exceeding 35% among medium-sized commercial farms. AI-powered yield prediction, autonomous machinery coordination, and carbon monitoring tools are creating differentiated value beyond traditional record management. Software vendors are increasing investment in modular subscription platforms, satellite analytics, and localized language capabilities while partnering with agritech startups and equipment manufacturers. Early ecosystem development creates durable customer relationships and establishes recurring digital service opportunities.

Long-term execution depends on securely integrating diverse operational technologies while maintaining consistent performance across large agricultural networks. Nearly 58% of enterprise farms manage information from multiple disconnected systems, increasing implementation complexity, while agricultural cyber incidents affecting connected operational technology have risen by more than 20% in recent years. Australia and Canada face additional challenges integrating remote operations with continuous real-time analytics across geographically dispersed farms. These factors reduce deployment consistency and complicate enterprise-wide decision-making. Companies must strengthen cybersecurity architecture, standardized data governance, workforce digital training, and scalable cloud infrastructure while investing in interoperable software frameworks that sustain operational resilience and long-term competitiveness.

AI-Driven Decision Automation Commercial farms are embedding AI into planting schedules, disease prediction, and input optimization, with automated recommendations improving agronomic decision speed by nearly 35% and reducing manual planning workloads by around 45%. Labor shortages in the United States are accelerating deployment, prompting software providers to expand AI partnerships, integrate predictive analytics, and automate field-level workflows for higher operational consistency.

Connected Equipment Ecosystems Machinery manufacturers are integrating software directly with tractors, harvesters, drones, and sensor networks, increasing connected equipment utilization by approximately 30% while reducing equipment downtime by nearly 18%. Growing demand for interoperable platforms is driving enterprise collaborations, enabling unified operational dashboards, streamlined maintenance scheduling, and faster data synchronization across large farming operations.

Digital Compliance And Traceability Food traceability regulations and sustainability reporting requirements are encouraging broader digital record management, with compliance automation reducing reporting time by nearly 40% and digital documentation adoption exceeding 55% among export-oriented producers. Companies are restructuring software portfolios to include carbon tracking, audit-ready documentation, and integrated supply-chain visibility that strengthens buyer confidence and export competitiveness.

Mobile-First Farm Operations Smartphone-based farm management is reshaping daily operations as mobile application usage among commercial farm managers exceeds 60%, while real-time field reporting improves response times by approximately 28%. Australia and India are accelerating mobile deployment where distributed field operations require continuous connectivity, encouraging vendors to prioritize offline functionality, multilingual interfaces, and cloud synchronization for geographically dispersed agricultural enterprises.

Cloud-Based solutions remain the leading segment, accounting for approximately 48% of enterprise deployments because they provide scalable infrastructure, centralized data management, rapid software updates, and seamless integration with IoT devices, satellite imagery, and farm equipment. Large agricultural enterprises increasingly favor cloud environments to manage geographically dispersed operations while reducing IT maintenance costs by nearly 30%. Integrated Platforms are the fastest-growing category, with adoption increasing by around 24% as organizations seek unified agronomic, financial, compliance, and operational intelligence within a single ecosystem. Companies continue expanding cloud-native capabilities through AI integration, strategic technology alliances, and enhanced cybersecurity features.

On-Premise platforms retain strategic relevance for organizations requiring strict data control and limited external connectivity, while Web-Based solutions remain widely adopted by medium-sized agricultural businesses seeking browser-based accessibility. Mobile-Based platforms continue expanding through field-level mobility, supporting real-time monitoring and workforce coordination. Investment priorities increasingly favor interoperable cloud ecosystems capable of supporting predictive analytics, automation, and enterprise-scale digital agriculture.

Crop Management represents the largest application segment because commercial producers require continuous monitoring of planting, fertilization, pest management, and harvest optimization. More than 55% of software deployments prioritize crop-focused workflows, while AI-assisted crop analytics improve field productivity planning by approximately 22%. Irrigation Management is the fastest-growing application as increasing water efficiency requirements and climate variability accelerate adoption of sensor-driven irrigation scheduling capable of reducing water usage by nearly 18%. Technology providers are integrating weather intelligence, satellite monitoring, and automated recommendations into comprehensive crop management platforms.

Livestock Management maintains steady demand through herd monitoring, feed optimization, and animal health tracking, while Farm Planning supports long-term operational scheduling and resource allocation. Financial Management continues gaining importance as enterprises integrate budgeting, inventory, and profitability analytics into operational platforms. Vendors increasingly expand automation capabilities and application interoperability to strengthen customer retention and enterprise-wide decision support.

Farms remain the dominant end-user segment because they operate the largest volume of daily agronomic activities requiring integrated planning, monitoring, and compliance management. Approximately 62% of enterprise deployments originate from commercial farming operations, where digital workflow automation reduces administrative effort by nearly 27% and improves operational visibility across multiple production sites. Agribusinesses represent the fastest-growing end-user group as processors, exporters, and vertically integrated agricultural companies adopt unified platforms to coordinate procurement, logistics, traceability, and supplier engagement. Software providers increasingly develop scalable subscription models and enterprise integration capabilities to serve these expanding organizations.

Cooperatives continue adopting shared digital platforms to coordinate member operations and improve resource utilization, while Agricultural Consultants rely on advanced analytics for advisory services and performance benchmarking. Research Institutions support innovation through field trials, predictive modeling, and precision agriculture validation. Vendors are strengthening competitive positioning through customized deployments, strategic ecosystem partnerships, and sector-specific software modules designed for distinct operational requirements.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 13.2% CAGR between 2026 and 2033.

Integrated Precision Agriculture Drives Enterprise Digitalization

North America maintains the leading position through advanced precision agriculture, high farm mechanization, and widespread deployment of connected equipment. Large commercial farms increasingly integrate AI-driven analytics, satellite monitoring, and IoT-enabled machinery into unified farm management platforms, creating strong demand for interoperable software ecosystems. The region contributes nearly 37% of global deployments, supported by mature cloud infrastructure and high digital literacy among agricultural enterprises. More than 65% of large commercial farming operations utilize digital farm records, while enterprise software integration projects continue expanding through partnerships between equipment manufacturers and technology providers. Companies are prioritizing predictive agronomy, automated compliance management, and operational intelligence to improve productivity and reduce input variability across extensive farming operations.

United States Market Outlook: The United States remains the regional technology leader due to extensive commercial farming, advanced precision equipment adoption, and strong agritech innovation. Over 70% of large crop-producing enterprises deploy GPS-guided equipment alongside digital management platforms, enabling integrated field planning and operational monitoring. Software vendors continue strengthening partnerships with agricultural equipment manufacturers, cloud service providers, and farming cooperatives to accelerate enterprise-scale deployments and improve interoperability across diversified agricultural operations.

Sustainability Compliance Accelerates Digital Farm Modernization

Europe is strengthening market adoption through sustainability targets, digital agriculture policies, and increasing traceability requirements across food production systems. The region accounts for approximately 27% of global deployment activity, with commercial farms integrating software for environmental reporting, resource optimization, and precision field management. Automated compliance workflows reduce administrative processing by nearly 35%, while smart irrigation and nutrient optimization technologies continue expanding across high-value agricultural regions. Agricultural technology providers increasingly develop integrated platforms supporting carbon monitoring, biodiversity management, and digital documentation to meet evolving operational standards. Enterprise investments remain focused on interoperability, cloud migration, and precision decision-support capabilities.

Germany Market Outlook: Germany leads the European market through advanced agricultural engineering, strong software innovation, and highly mechanized commercial farming. More than 60% of large agricultural enterprises utilize precision farming technologies integrated with digital management systems. Domestic technology providers continue expanding AI-enabled agronomic analytics, equipment connectivity, and sustainability reporting capabilities, reinforcing the country's leadership in enterprise-scale agricultural digital transformation.

Large-Scale Agricultural Digital Adoption Expands

Asia-Pacific is experiencing the fastest operational expansion as governments and agribusinesses accelerate agricultural modernization through digital infrastructure and smart farming initiatives. Commercial deployment continues rising across large crop-producing economies, with connected farming technologies increasing by approximately 28% in major agricultural districts. Precision irrigation, drone-assisted monitoring, and mobile-first software platforms are becoming standard operational tools for commercial producers. Expanding rural connectivity and public investment in digital agriculture encourage software providers to localize platforms, strengthen cloud infrastructure, and establish strategic partnerships with regional equipment manufacturers and agritech enterprises.

China Market Outlook: China dominates regional deployment through extensive smart agriculture initiatives, advanced digital infrastructure, and large-scale commercial farming operations. More than one-quarter of large agricultural production areas have adopted intelligent farming technologies integrating sensors, satellite monitoring, and automated management platforms. Domestic technology companies continue investing in AI-powered agronomic solutions, precision irrigation systems, and digital supply-chain integration to strengthen agricultural productivity and operational resilience.

Export-Oriented Farming Strengthens Software Adoption

South America continues expanding adoption as commercial agriculture prioritizes productivity, export traceability, and operational efficiency. Large soybean, corn, sugarcane, and livestock operations increasingly implement integrated farm management platforms to optimize production planning and resource allocation. Approximately 20% of commercial agricultural enterprises have accelerated digital transformation initiatives during recent modernization programs. Enterprise software deployment is supported by expanding precision agriculture investments and stronger collaboration between technology providers and agricultural equipment suppliers. Connectivity limitations across remote farming regions remain an operational challenge, encouraging vendors to develop offline-enabled and hybrid deployment models.

Brazil Market Outlook: Brazil represents the region's largest market due to extensive commercial agriculture, expanding precision farming adoption, and strong agribusiness investment. Large farming enterprises increasingly integrate satellite imagery, field analytics, and automated machinery into centralized management platforms. Digital farm technologies continue improving operational efficiency across soybean and sugarcane production while technology providers expand localized software capabilities and strategic implementation partnerships.

Smart Agriculture Investment Reshapes Production Systems

The Middle East & Africa market is advancing through government-backed agricultural modernization, water-efficiency initiatives, and controlled-environment farming investments. Digital farm management platforms are increasingly deployed to optimize irrigation scheduling, greenhouse operations, and resource utilization under challenging climatic conditions. Smart irrigation deployments have improved water-use efficiency by approximately 20% across several commercial projects. Technology providers are expanding regional partnerships, cloud-enabled monitoring platforms, and AI-assisted decision-support tools to address food security priorities while strengthening operational sustainability and agricultural productivity.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment through substantial investment in smart agriculture, greenhouse technologies, and digital water management infrastructure. Commercial agricultural enterprises increasingly deploy AI-enabled farm management platforms integrated with precision irrigation and environmental monitoring systems. National modernization initiatives continue encouraging partnerships between technology developers, agricultural operators, and research organizations to improve food production efficiency while reducing water consumption across intensive farming operations.

The competitive landscape is led by Deere, Trimble, Bayer, AG Leader Technology, Topcon Agriculture, and CropX, with global platform providers competing directly against regional agricultural software specialists and equipment-integrated solution vendors. The top five players collectively control approximately 43% of market activity through broad digital ecosystems and established enterprise relationships. Competition increasingly centers on AI analytics, interoperability, automation, and implementation speed rather than pricing alone. Integrated platforms improve customer retention by nearly 28%, while automated agronomic recommendations reduce operational planning time by approximately 35%, strengthening vendor differentiation. Global leaders expand through equipment partnerships, cloud integration, and precision agriculture investments, whereas regional providers compete through localized workflows, language customization, and lower deployment complexity. The market is shifting toward consolidated digital ecosystems combining machinery connectivity, satellite intelligence, and compliance management within unified platforms. High integration costs, proprietary data architectures, and enterprise migration complexity remain key entry barriers. Winning requires interoperable platforms, measurable operational outcomes, scalable AI capabilities, and trusted long-term customer ecosystems.

Deere & Company

Trimble Inc.

Bayer AG

AG Leader Technology

Topcon Agriculture

CropX Technologies

Farmers Edge Inc.

Agworld

Conservis

Granular

AgriWebb

Raven Industries

Farmbrite

Semios

Artificial intelligence, machine learning, IoT sensors, satellite imagery, and cloud computing define the current technology foundation of farm management software. AI-powered decision engines improve crop planning accuracy by approximately 24%, while connected field sensors reduce manual monitoring effort by nearly 40%. More than 55% of enterprise-scale commercial farms now deploy cloud-enabled digital management platforms integrated with precision agriculture tools. Compared with conventional spreadsheet-based farm management, AI-driven platforms complete operational analysis nearly 45% faster while providing continuous agronomic recommendations that improve resource allocation and field performance.

Emerging technologies are shifting toward digital twins, autonomous machinery coordination, computer vision, and edge computing. Autonomous workflow integration reduces equipment idle time by around 18%, while edge-enabled processing shortens field data response times by nearly 30%. Equipment manufacturers, agritech software providers, and cloud platform companies gain the greatest competitive advantage through seamless interoperability. Businesses increasingly integrate weather intelligence, drone imagery, financial management, and compliance reporting into unified operational ecosystems supporting faster enterprise decisions.

Between 2026 and 2028, predictive agronomic intelligence, generative AI assistants, and blockchain-enabled traceability will become standard enterprise capabilities. Adoption of automated decision-support platforms is expected to exceed 65% among large commercial farms, strengthening planning accuracy, regulatory compliance, and supply-chain transparency. Companies investing early in interoperable AI ecosystems, cybersecurity, and autonomous field operations will secure stronger operational efficiency, faster customer onboarding, and sustainable competitive differentiation.

January 2024 Trimble launched the Connected Climate Exchange, a carbon marketplace linking farmers, agronomists, and sustainability buyers through verified farm data, enabling scalable participation in carbon programs. The platform streamlines emissions verification, strengthening digital farm management value propositions. Source: https://investor.trimble.com

January 2025 John Deere introduced JDLink Boost, extending satellite-based machine connectivity for farms with limited cellular coverage through its Starlink collaboration. The solution delivers connectivity in areas with 0% cellular coverage, improving real-time farm data access and operational continuity. Source: https://www.deere.com

February 2025 John Deere expanded Operations Center with enhanced jobsite analytics, machine health monitoring, and workflow management features based on customer feedback. The update introduced more than 15 new capabilities, enabling faster operational decisions and stronger digital farm management integration. Source: https://www.deere.com

January 2025 Reuters reported John Deere's expansion of autonomous agricultural equipment, adding AI-powered tractors and retrofit autonomy kits equipped with 16 cameras for precision field operations. The development strengthens labor productivity while accelerating enterprise automation across commercial farming. Source: https://www.reuters.com

This report provides comprehensive analysis across Cloud-Based, On-Premise, Web-Based, Mobile-Based, and Integrated Platform solutions, together with detailed assessment of Crop Management, Livestock Management, Farm Planning, Irrigation Management, and Financial Management applications. It evaluates demand across Farms, Agribusinesses, Cooperatives, Agricultural Consultants, and Research Institutions while covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 60% of enterprise deployments emphasize integrated digital agriculture workflows, reflecting accelerating software convergence.

The study examines competitive positioning, technology adoption, AI-enabled precision agriculture, IoT connectivity, cloud integration, satellite analytics, and automation trends shaping commercial farming between 2026 and 2033. It highlights deployment patterns, regional investment priorities, partnership strategies, and enterprise modernization initiatives, enabling stakeholders to strengthen expansion planning, benchmark competitors, identify high-potential market segments, optimize investment decisions, and align product development with evolving operational requirements across the global farm management software ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1284.92 Million |

Market Revenue in 2033 | USD 3047.61 Million |

CAGR (2026 - 2033) | 11.4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Deere & Company, Trimble Inc., Bayer AG, AG Leader Technology, Topcon Agriculture, CropX Technologies, Farmers Edge Inc., Agworld, Conservis, Granular, AgriWebb, Raven Industries, Farmbrite, Semios |

Customization & Pricing | Available on Request (10% Customization is Free) |