Reports

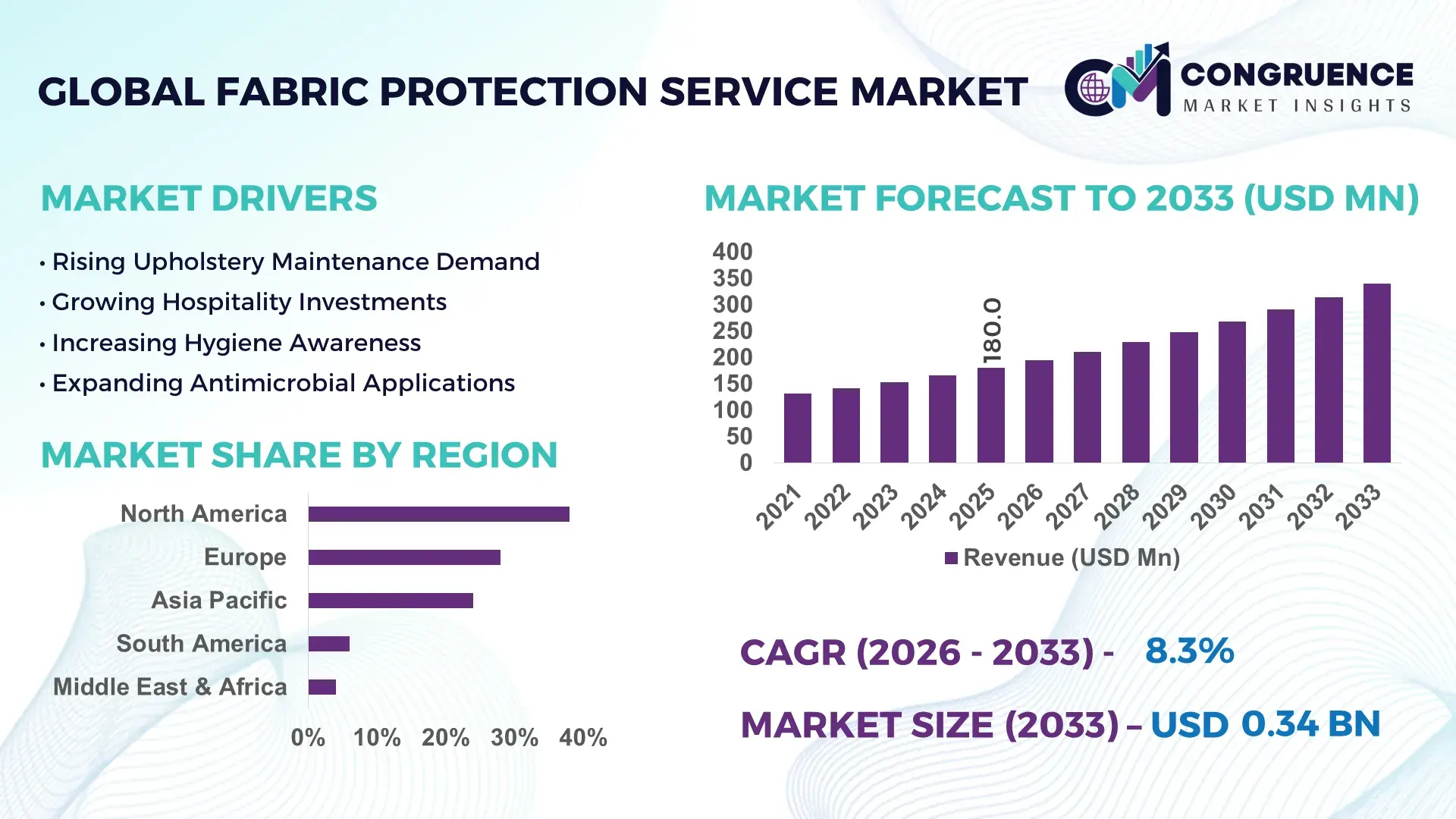

The Global Fabric Protection Service Market was valued at USD 180.0 Million in 2025 and is anticipated to reach a value of USD 340.6 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033. Growth is being driven by rising adoption of advanced stain-resistant and antimicrobial fabric treatments across hospitality, healthcare, automotive interiors, and premium residential furnishing applications.

The United States remains the dominant country, accounting for approximately 31% of global market activity, supported by a commercial furnishings sector exceeding 5.5 million serviced properties and widespread adoption of fluorine-free protection technologies. Fabric treatment penetration in premium hospitality assets exceeds 60%, compared with nearly 42% in Germany, where sustainability regulations are accelerating demand for eco-certified coating solutions. Ongoing investment in high-performance textile maintenance services and stricter indoor environment standards continue strengthening market leadership across North American service networks.

Strategic implication: Companies with scalable eco-friendly treatment portfolios and strong commercial-service partnerships are positioned to secure long-term contracts in high-value asset protection segments.

Market Size & Growth: USD 180.0 Million in 2025 reaching USD 340.6 Million by 2033, supported by expanding antimicrobial textile treatment adoption across hospitality and healthcare facilities.

Top Growth Drivers: Commercial furnishing protection demand (+28%), sustainable coating adoption (+35%), and premium upholstery maintenance contracts (+24%).

Short-Term Forecast: By 2028, automated fabric inspection and treatment workflows are expected to reduce service turnaround times by nearly 18%.

Emerging Technologies: AI-assisted stain diagnostics, fluorine-free nanocoatings, and smart textile protection systems are improving treatment consistency by over 20%.

Regional Leaders: North America (~USD 105 Million), Europe (~USD 82 Million), and Asia-Pacific (~USD 70 Million) supported by hospitality upgrades, sustainability compliance, and urban residential expansion.

Consumer/End-User Trends: More than 55% of premium furniture buyers now request protection treatments at the point of purchase.

Pilot/Case Example: A 2024 hospitality textile maintenance program reduced upholstery replacement frequency by 30% across managed properties.

Competitive Landscape: Leading providers collectively control nearly 38% market share, with major participants including ServiceMaster, Stanley Steemer, Guardsman, Fiber-Seal, and Chem-Dry.

Regulatory & ESG Impact: Fluorocarbon-reduction initiatives have increased demand for eco-certified fabric treatments by approximately 32%.

Investment & Funding: Industry expansion and service-network investments exceeded USD 120 Million globally, emphasizing regional partnerships and franchise growth.

Innovation & Future Outlook: Next-generation bio-based protectants and predictive maintenance platforms are reshaping high-growth commercial asset management strategies.

Fabric Protection Service Market demand is increasingly concentrated in hospitality furnishings, healthcare textiles, automotive upholstery, and premium residential interiors where lifecycle extension remains a key operational priority. Recent innovations include fluorine-free nanocoatings, antimicrobial surface technologies, and AI-enabled fabric assessment tools. Nearly 35% of newly introduced protection solutions emphasize environmentally compliant formulations, while evolving chemical regulations and resilient textile supply chains are encouraging service providers to develop sustainable, performance-focused treatment portfolios, setting the stage for deeper strategic market evolution.

Fabric protection services are becoming strategically important as businesses prioritize asset preservation, maintenance efficiency, and sustainability objectives. Hotels, healthcare facilities, automotive fleets, and commercial property operators increasingly view textile protection as a cost-control mechanism rather than a discretionary service. The market is also benefiting from stricter chemical compliance standards and growing adoption of environmentally responsible maintenance programs that extend product lifecycles while reducing replacement frequency.

Modern nanotechnology-based protection treatments deliver 25–35% longer stain resistance and durability compared with conventional solvent-based solutions while reducing retreatment requirements. The United States leads in large-scale commercial deployment, whereas Germany and the Nordic countries are advancing eco-certified treatment technologies and fluorine-free solutions. Over the next two to three years, digital inspection systems and predictive maintenance platforms are expected to improve treatment scheduling accuracy by more than 15%, enabling better resource allocation and service consistency.

A practical example can be seen in hospitality operators integrating fabric protection contracts into facility management agreements to reduce refurbishment cycles and operational downtime. Service providers are responding through regional expansion, technology partnerships, and sustainable chemistry investments. As procurement decisions increasingly prioritize durability, compliance, and lifecycle optimization, fabric protection services are evolving into a critical competitive differentiator across commercial and institutional environments.

Commercial asset owners are placing greater emphasis on extending the usable life of furnishings and textile-based infrastructure. Premium hospitality properties report upholstery replacement cost reductions of 20–30% when proactive protection programs are implemented, while healthcare facilities have increased treated textile adoption by nearly 25% over the past five years. Regulatory scrutiny surrounding indoor hygiene standards is further accelerating demand for antimicrobial and stain-resistant treatments. This shift creates measurable operational savings and supports sustainability targets through waste reduction. Service providers are responding by expanding specialized treatment capabilities, forming partnerships with furniture manufacturers, and investing in advanced nanocoating technologies. A notable strategic insight is that protection services are increasingly being bundled with facility management contracts, creating recurring revenue streams and stronger customer retention.

The transition from traditional fluorinated chemistries to environmentally compliant alternatives continues to pressure operating margins. Eco-certified treatment formulations can carry costs 15–25% higher than conventional products, while specialty chemical input prices have experienced fluctuations exceeding 12% in several major sourcing markets. Regulatory divergence between the United States, European countries, and Asian manufacturing hubs adds further complexity to product standardization. These factors impact pricing flexibility, service scalability, and procurement planning. Companies are mitigating risks through supplier diversification, long-term purchasing agreements, and localized sourcing strategies. A key operational challenge remains maintaining treatment performance standards while adapting formulations to meet evolving environmental requirements without significantly increasing service costs.

Digital transformation is creating new value opportunities beyond traditional protection treatments. AI-enabled fabric assessment systems can improve stain detection accuracy by approximately 30%, while predictive maintenance platforms reduce unnecessary service visits by nearly 18%. Commercial building operators are increasingly integrating textile maintenance data into broader asset management systems. Japan and South Korea are emerging as early adopters of sensor-integrated textile monitoring applications for healthcare and transportation environments. Service providers are investing in software partnerships, treatment analytics, and performance-monitoring ecosystems to create differentiated service offerings. A particularly attractive opportunity lies in subscription-based protection programs that combine preventive maintenance, inspection, and treatment services into long-term contractual relationships with commercial customers.

Maintaining consistent treatment quality across geographically dispersed service networks remains a significant execution challenge. Industry assessments indicate treatment effectiveness can vary by 15–20% depending on technician expertise, application methods, and environmental conditions. Increasing complexity of advanced nanocoatings and antimicrobial formulations requires specialized training that many regional providers struggle to implement at scale. At the same time, customer expectations for measurable performance outcomes continue rising. Companies must invest in technician certification programs, digital quality-control systems, and standardized application protocols to ensure consistency. A critical long-term strategic issue is balancing rapid service-network expansion with operational excellence, as inconsistent execution can undermine customer trust and weaken competitive positioning in premium commercial segments.

Fluorine-Free Chemistry Adoption Regulatory restrictions on PFAS-containing formulations are accelerating the shift toward fluorine-free fabric protection technologies. More than 40% of newly launched commercial treatment solutions now utilize alternative chemistries, while adoption among premium hospitality operators has increased by nearly 28% since 2024. This transition is reshaping procurement standards and supplier qualification processes. Service providers are expanding partnerships with specialty chemical manufacturers and restructuring product portfolios to maintain performance standards while meeting evolving compliance requirements.

Digital Inspection Workflow Integration AI-assisted fabric assessment platforms are becoming embedded within commercial maintenance operations. Automated inspection tools have improved stain detection accuracy by approximately 30% and reduced manual evaluation time by nearly 22%. Large facility operators in the United States are increasingly integrating textile condition monitoring into broader asset-management systems. The operational result is faster service scheduling, lower labor intensity, and improved treatment consistency. Companies are scaling digital workflows and investing in predictive maintenance capabilities to improve contract performance.

Subscription-Based Service Expansion Long-term textile protection contracts are replacing one-time treatment engagements across institutional facilities. Contract renewal rates exceed 70% among major hospitality operators, while bundled maintenance programs have reduced furnishing replacement cycles by nearly 25%. Rising cost-control pressures are encouraging enterprises to prioritize lifecycle management rather than reactive replacement. Providers are responding through multi-year service agreements, facility-management partnerships, and performance-based maintenance models that improve customer retention.

Antimicrobial Textile Protection Growth Healthcare and public-use environments are increasing demand for antimicrobial fabric treatment solutions. Treated textile deployment has expanded by more than 32% across healthcare facilities, while institutional procurement specifications incorporating hygiene-focused coatings have risen by nearly 20%. Labor shortages and stricter sanitation protocols are driving adoption of longer-lasting protective treatments. Service providers are investing in specialized application technologies and certification programs to differentiate offerings in highly regulated operating environments.

On-site fabric protection services represent the leading segment, accounting for an estimated 42% of market demand due to immediate deployment capability, minimal operational disruption, and strong integration with hospitality, healthcare, and commercial facility maintenance schedules. Enterprise customers increasingly prefer on-location treatment because it eliminates transportation costs and reduces service downtime by nearly 30%. The segment also benefits from recurring commercial contracts where large property portfolios require standardized textile maintenance programs. Companies continue expanding technician networks and regional service hubs to improve response times and service coverage. Specialized antimicrobial protection services are emerging as the fastest-growing segment as healthcare facilities, educational institutions, and public venues strengthen hygiene-focused procurement standards. Adoption within institutional environments has increased by approximately 24% over the past two years. Subscription-based protection programs are also gaining traction as operators seek predictable maintenance expenditures and longer asset lifecycles. Off-site treatment services remain strategically relevant for premium textile restoration and specialized coating applications where controlled processing environments deliver superior treatment consistency. Investment priorities are increasingly shifting toward high-performance treatment formulations and long-term service agreements.

Hospitality remains the leading application segment, supported by extensive deployment across hotels, resorts, serviced apartments, and event venues where upholstery preservation directly impacts operational costs and guest experience. The segment accounts for roughly 38% of market demand, with large hotel operators reporting upholstery replacement reductions of up to 30% through preventive protection programs. Growing emphasis on asset optimization and sustainability targets continues reinforcing adoption. Service providers are expanding dedicated hospitality service packages and integrating digital inspection capabilities into maintenance contracts. Healthcare is the fastest-growing application segment as hospitals and long-term care facilities increase use of antimicrobial and stain-resistant textile treatments. Demand within healthcare environments has expanded by approximately 26%, supported by stricter sanitation standards and infection-control protocols. Residential applications continue benefiting from premium furniture ownership trends and growing awareness of fabric preservation services. Automotive interiors are emerging as a niche growth area, particularly for premium vehicle fleets and luxury mobility operators seeking longer-lasting cabin aesthetics. Companies are responding through customized treatment formulations and sector-specific service offerings.

Commercial facilities constitute the dominant end-user segment, representing approximately 45% of total demand due to extensive textile inventories across hotels, offices, entertainment venues, and managed properties. Demand concentration is linked to operational intensity, high furniture replacement costs, and ongoing facility-maintenance requirements. More than 60% of large hospitality operators now include fabric protection within broader asset-management programs. Service providers are targeting this segment through multi-site agreements, customized maintenance schedules, and integrated facility-management partnerships. Healthcare institutions represent the fastest-growing end-user group as hygiene compliance requirements and patient-environment standards continue strengthening. Adoption of specialized textile protection solutions has increased by nearly 25% across institutional settings. Residential consumers remain an important market segment, particularly among premium furniture owners seeking asset preservation and stain resistance. Automotive service providers are expanding use of fabric protection treatments within detailing and fleet-maintenance operations. To strengthen competitive positioning, companies are introducing tiered service packages, subscription models, and sector-specific treatment solutions aligned with distinct customer requirements.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America maintains the leading position in the Fabric Protection Service Market due to its extensive hospitality infrastructure, mature facility-management ecosystem, and widespread adoption of preventive maintenance programs. The region contributes nearly 38% of global demand, supported by large-scale deployment across hotels, healthcare facilities, office complexes, and premium residential properties. More than 60% of major hospitality operators incorporate textile protection services within broader asset-management frameworks. Growing adoption of fluorine-free treatment technologies and AI-assisted inspection systems is improving service efficiency and compliance readiness. Strategic partnerships between facility-management firms and fabric treatment providers are expanding recurring contract opportunities while reducing furnishing replacement cycles by approximately 25%.

United States Market Outlook: The United States serves as the primary market engine due to its concentration of commercial properties, premium hospitality assets, and advanced facility-management practices. Hospitality groups increasingly integrate fabric protection into long-term maintenance contracts to control operational expenditure and extend furnishing lifecycles. More than 5.5 million commercial accommodation units create a substantial recurring service base. Adoption of antimicrobial textile treatments is accelerating across healthcare and public-use facilities, while digital inspection platforms are improving service consistency and technician productivity across multi-state operations.

Europe represents a significant share of the global market, supported by stringent environmental regulations, strong commercial furnishing standards, and increasing preference for sustainable maintenance solutions. The region accounts for approximately 28% of market activity, with demand concentrated in hospitality, healthcare, and institutional infrastructure. Regulatory pressure surrounding fluorinated chemicals has accelerated adoption of eco-certified protection treatments, with environmentally compliant solutions now representing more than 45% of new service deployments. Service providers are investing in green chemistry innovation, certification programs, and specialized application technologies. Enterprise customers increasingly prioritize lifecycle extension strategies to reduce material waste and support corporate sustainability objectives.

Germany Market Outlook: Germany remains the most influential market due to its strong commercial property sector, advanced textile technology capabilities, and strict environmental compliance framework. Large facility operators increasingly require certified low-emission treatment solutions as part of procurement specifications. Commercial furnishing protection programs have expanded across hospitality and healthcare networks, while domestic technology providers continue investing in fluorine-free coating innovation. The country's industrial focus on sustainability and operational efficiency supports growing demand for advanced textile preservation services with measurable environmental performance benefits.

Asia-Pacific is emerging as the fastest-expanding regional market, supported by urbanization, hospitality development, growing middle-class consumption, and increasing investment in commercial infrastructure. The region accounts for nearly 24% of global demand, while large-scale hotel construction and premium residential development are creating new service opportunities. Textile maintenance outsourcing has increased by approximately 22% among commercial property operators seeking improved operational efficiency. Rising awareness of asset preservation and hygiene standards is driving broader adoption across healthcare, transportation, and institutional facilities. Service providers are expanding franchise networks, regional partnerships, and localized treatment capabilities to capture emerging demand.

China Market Outlook: China leads regional market activity through its extensive hospitality infrastructure, large commercial property inventory, and rapidly expanding premium furniture market. Large urban centers continue investing in high-quality interior asset management as commercial real estate standards evolve. Demand for advanced stain-resistant and antimicrobial treatments is increasing across healthcare facilities, transportation hubs, and premium residential developments. Growing deployment of digital facility-management platforms is also supporting more structured textile maintenance programs, improving treatment scheduling and asset-performance monitoring across large property portfolios.

South America is experiencing steady market expansion as hospitality modernization, commercial property upgrades, and premium residential furnishing adoption increase. The region contributes approximately 6% of global market activity, with demand centered on hotels, business centers, and urban residential developments. Textile maintenance outsourcing has expanded by nearly 18% among large property operators seeking longer asset utilization and lower refurbishment costs. Infrastructure limitations and uneven service-network coverage continue affecting scalability in certain markets, but growing investment in commercial real estate is strengthening long-term demand fundamentals. Service providers are focusing on localized partnerships and technician training programs to improve deployment consistency.

Brazil Market Outlook: Brazil represents the largest market within South America due to its extensive hospitality sector, large urban population, and concentration of commercial real estate assets. Hotel operators increasingly adopt preventive textile maintenance programs to improve furnishing durability and reduce refurbishment expenditure. Major metropolitan areas such as São Paulo and Rio de Janeiro continue generating significant service demand through commercial property expansion. Growing awareness of asset lifecycle management and premium interior preservation is encouraging broader adoption of specialized fabric treatment solutions across both institutional and residential sectors.

The Middle East & Africa market is benefiting from large-scale infrastructure projects, luxury hospitality expansion, and modernization initiatives across commercial real estate sectors. The region accounts for roughly 4% of global demand, with strong concentration in premium hotels, mixed-use developments, and high-end residential projects. Hospitality-related textile protection deployments have increased by approximately 20% as operators prioritize asset preservation and guest-experience standards. Ongoing investment in tourism infrastructure and premium property developments continues creating opportunities for specialized treatment providers. Companies are expanding regional partnerships and technical-service capabilities to support increasingly sophisticated customer requirements.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's strategic market hub due to its concentration of luxury hospitality assets, premium commercial developments, and globally recognized tourism infrastructure. High-value hotels and mixed-use projects increasingly deploy advanced textile protection services to maintain furnishing quality under intensive usage conditions. Large-scale property operators prioritize preventive maintenance programs that extend asset lifecycles and support premium customer experiences. Continued investment in tourism, hospitality, and commercial real estate development strengthens long-term demand for specialized fabric protection solutions across the country.

The Fabric Protection Service Market is characterized by competition between premium protection specialists such as Fiber-Seal Systems, Guardsman, and Chem-Dry, global chemical technology providers including DuPont and 3M, and regional service networks focused on cost-efficient deployment. The top five participants collectively account for approximately 35–40% of market activity, creating a moderately consolidated structure where brand credibility and service consistency determine market positioning. Competition increasingly centers on treatment performance, sustainability compliance, deployment speed, and contract retention. Advanced fluorine-free solutions deliver up to 25% longer protection cycles, while AI-assisted inspection workflows reduce service assessment time by nearly 20%. Premium providers compete through customized commercial contracts, whereas regional operators compete on pricing that can be 15–20% lower. Companies are expanding franchise networks, investing in sustainable chemistry, forming facility-management partnerships, and integrating digital maintenance platforms. The current competitive shift favors technology-enabled and compliance-focused providers as PFAS-related regulatory pressure reshapes procurement standards. The primary entry barrier remains technical expertise and enterprise trust. Winning requires scalable service delivery, proven treatment performance, and strong commercial customer retention.

Guardsman

Chem-Dry

ServiceMaster Clean

DuPont

3M Company

Stanley Steemer

Ultra-Guard Fabric Protection Services

Protex International Group

Servpro Industries

Furniture Clinic

Scotchgard Professional Solutions

Fabric protection technologies are transitioning from conventional solvent-based repellents toward fluorine-free nanocoatings, antimicrobial treatment platforms, and AI-enabled inspection systems. Modern nanocoating formulations improve stain and liquid resistance by 20–30% while reducing retreatment frequency. Nearly 40% of newly introduced commercial-grade protection solutions now incorporate environmentally compliant chemistries, reflecting procurement shifts across hospitality, healthcare, and commercial facilities. These technologies help operators reduce furnishing replacement frequency and improve lifecycle management efficiency.

The most significant comparison is between legacy fluorochemical treatments and advanced nanostructured coatings. New-generation solutions provide approximately 25% longer protection performance while lowering maintenance intervention requirements by nearly 18%. AI-driven textile assessment systems are achieving adoption rates exceeding 20% among large facility-management providers, improving inspection accuracy and accelerating service deployment. Commercial property operators benefit most because predictive maintenance workflows strengthen asset utilization and reduce unplanned refurbishment activity.

Between 2026 and 2028, integration of sensor-enabled textile monitoring, digital maintenance platforms, and antimicrobial protection technologies is expected to accelerate. Companies investing early in smart maintenance ecosystems can improve operational productivity by 15–20% while strengthening customer retention. Competitive advantage increasingly belongs to providers combining sustainable chemistry, digital diagnostics, and scalable service delivery models capable of supporting large enterprise contracts.

January 2025 – DuPont collaborated with Sesame Technologies to deploy next-generation protective material solutions utilizing Kevlar® EXO™ technology. The platform represents the most significant aramid innovation in over 50 years, strengthening advanced protection performance and expanding specialty textile applications across industrial environments. Source: www.sesametechnologies.com

August 2025 – Grasim Industries launched Raysileco, a fully traceable sustainable filament yarn platform designed to improve textile supply-chain transparency. The initiative delivers 100% traceability to origin, supporting sustainability-focused textile protection and furnishing applications while strengthening compliance-driven procurement strategies.

September 2025 – Loop Industries and Hyosung TNC formed a strategic alliance to expand textile-to-textile circular polyester supply chains. The collaboration utilizes 100% recycled textile feedstock, improving sustainable material availability and supporting next-generation fabric treatment ecosystems serving global textile and furnishing markets.

September 2025 – Circ and Arvind Limited entered a five-year purchase and commercialization partnership to scale recycled polyester and lyocell deployment. The agreement expands access to advanced circular textile materials and strengthens sustainable sourcing pathways for large-scale apparel and furnishing manufacturers.

The report provides comprehensive analysis across service types, applications, end-user industries, technology adoption patterns, and regional deployment trends. Coverage includes on-site protection services, off-site treatment solutions, subscription-based maintenance programs, and antimicrobial protection offerings. Key application sectors assessed include hospitality, healthcare, residential furnishings, and automotive interiors. The study evaluates demand distribution across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level assessment of major markets.

The report examines technology adoption trends including fluorine-free coatings, nanotechnology-based protectants, antimicrobial treatments, and AI-assisted inspection systems. More than 60% of commercial demand originates from enterprise-driven asset preservation programs, while sustainability-focused treatments represent one of the fastest-expanding deployment categories. Strategic insights cover competitive positioning, partnership activity, operational efficiency trends, regulatory impacts, customer purchasing behavior, and investment priorities. The analysis supports market-entry planning, expansion strategy development, portfolio optimization, and long-term decision-making across the 2026–2033 strategic outlook period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 180.0 Million |

| Market Revenue (2033) | USD 340.6 Million |

| CAGR (2026–2033) | 8.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Fiber-Seal Systems; Guardsman; Chem-Dry; ServiceMaster Clean; DuPont; 3M Company; Stanley Steemer; Ultra-Guard Fabric Protection Services; Protex International Group; Servpro Industries; Furniture Clinic; Scotchgard Professional Solutions |

| Customization & Pricing | Available on Request (10% Customization Free) |