Reports

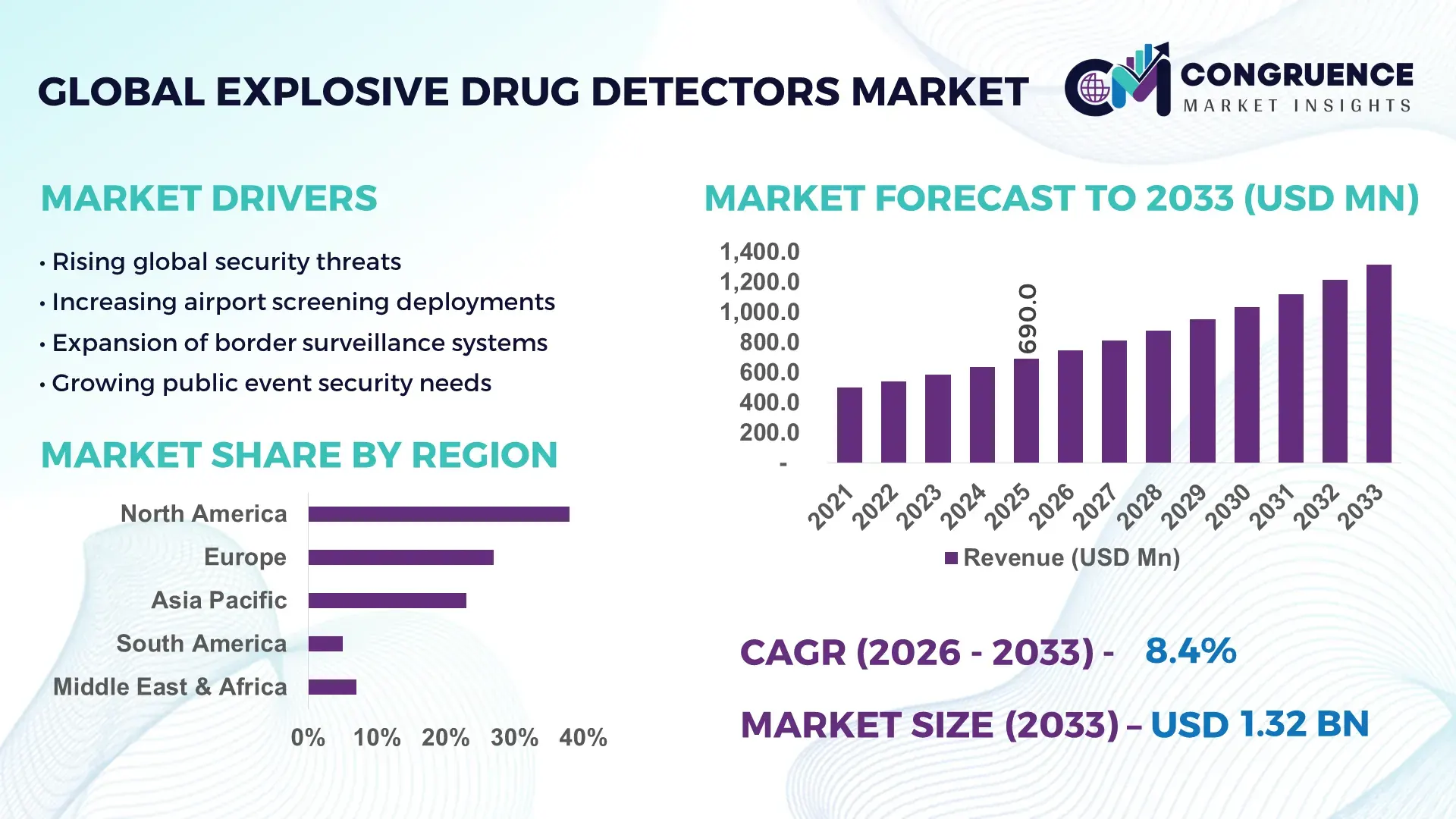

The Global Explosive Drug Detectors Market was valued at USD 690.0 Million in 2025 and is anticipated to reach a value of USD 1,315.5 Million by 2033 expanding at a CAGR of 8.4% between 2026 and 2033.

The market is being driven by the rapid shift toward multi-threat detection platforms integrating ion mobility spectrometry and AI-based analytics, enabling over 40% faster screening throughput and significantly reducing false positives in high-traffic environments such as airports and border checkpoints. Between 2024 and 2026, intensified geopolitical tensions and stricter aviation security mandates, particularly following evolving global counter-terrorism frameworks, are accelerating procurement cycles and forcing standardization of advanced screening technologies across international transit hubs.

The United States dominates with approximately 36% market share, supported by over USD 1.8 billion in annual homeland security and transportation safety investments. More than 75% of Tier-1 airports in the U.S. deploy integrated explosive and narcotics detection systems, compared to below 50% adoption across emerging Middle Eastern and Asian transit corridors, highlighting a clear deployment gap. Additionally, U.S.-based manufacturers account for nearly 42% of global technological patents in trace detection systems, reinforcing innovation leadership. In contrast, Europe emphasizes regulatory compliance-driven upgrades, while Asia focuses on cost-efficient scaling and infrastructure expansion. This imbalance between innovation leadership and volume deployment is reshaping competitive positioning.

Strategically, companies must prioritize high-throughput, compliance-ready systems and regional manufacturing expansion to capture procurement-driven demand shifts while maintaining technological differentiation.

Market Size & Growth: USD 690.0M (2025) to USD 1,315.5M (2033), CAGR 8.4%, driven by AI-integrated detection systems adoption.

Top Growth Drivers: Aviation security expansion (32%), border control modernization (28%), AI-based detection adoption (25%).

Short-Term Forecast: By 2027, screening efficiency improves by 35%, reducing inspection time per passenger.

Emerging Technologies: AI-enabled analytics, ion mobility spectrometry, and portable trace detection systems gaining >30% adoption.

Regional Leaders: North America (~USD 420M) leads with tech adoption; Europe (~USD 300M) driven by compliance; Asia-Pacific (~USD 350M) expanding infrastructure.

Consumer/End-User Trends: Over 68% of airports shifting to integrated multi-threat detection platforms.

Pilot/Case Example: 2025 airport deployment improved detection accuracy by 27% and reduced false alarms by 22%.

Competitive Landscape: Top player holds ~18% share; key players include Smiths Detection, Thermo Fisher, OSI Systems, Bruker.

Regulatory & ESG Impact: Compliance upgrades reduced manual screening by 40%, lowering operational costs and workforce dependency.

Investment & Funding: Over USD 900M invested globally in security tech expansion and partnerships (2024–2026).

Innovation & Future Outlook: Next-gen handheld detectors improving portability by 50%, shifting toward decentralized screening models.

Airports and aviation security account for nearly 45% of total demand, followed by defense and law enforcement at approximately 30%, while critical infrastructure contributes around 15%, reflecting strong concentration in high-risk sectors. Recent innovations include AI-powered trace detection systems improving identification accuracy by over 25% and portable devices reducing deployment time by 40%. North America leads in advanced system adoption, while Asia-Pacific is witnessing over 35% increase in infrastructure-driven demand due to expanding airport networks. A key emerging trend is the shift toward decentralized and mobile detection units, enabling faster response across multiple checkpoints, positioning the market for operational agility and expanded deployment models.

The Explosive Drug Detectors Market is rapidly becoming a critical battleground for security technology leadership, as governments and private infrastructure operators prioritize advanced threat detection capabilities to address increasingly sophisticated risks. The market is accelerating as integrated detection systems transform from standalone devices into networked, AI-driven security ecosystems, optimizing real-time threat identification and operational efficiency.

Regulatory pressure is intensifying, with global aviation and border security frameworks mandating standardized detection performance, forcing rapid system upgrades and procurement acceleration. AI-enabled detection systems improve efficiency by 42% while reducing operational costs by 28% compared to legacy manual screening systems, fundamentally reshaping cost-performance benchmarks.

North America leads in volume deployment, while Asia-Pacific leads in infrastructure expansion and adoption velocity with over 35% increase in new installations, highlighting a shift toward emerging market dominance in scaling capabilities. Over the next 2–3 years, automated detection systems are expected to reduce screening cycle times by 30%, directly impacting throughput and operational cost efficiency.

From an ESG perspective, automated systems reduce manual inspection dependency by 40%, lowering workforce strain and improving compliance with labor efficiency standards. A 2025 airport deployment in the Middle East achieved a 25% improvement in detection accuracy and a 20% reduction in passenger processing time, demonstrating measurable operational gains.

Investment strategies are shifting, with leading companies reallocating over 20% of R&D budgets toward AI integration and portable detection systems, while expanding manufacturing capacity in Asia to optimize supply chain resilience.

Strategically, market leadership will be defined by the ability to deliver scalable, AI-driven, and compliance-ready detection systems, positioning companies to capture high-value government contracts and dominate next-generation security infrastructure deployment.

The core growth engine is the rapid integration of multi-threat detection technologies combining explosives and narcotics identification within a single platform, increasing operational efficiency by over 40%. This shift is being reinforced by global security mandates requiring unified screening systems, particularly in aviation and border control. A key trigger is the restructuring of international security protocols post-2024, pushing governments to upgrade legacy systems that still account for nearly 35% of installed base. The result is accelerated procurement cycles and rising demand for high-throughput systems. Companies are responding by expanding production capacity, forming strategic partnerships with AI analytics providers, and investing heavily in portable detection systems, enabling faster deployment across decentralized checkpoints and strengthening competitive positioning.

High system costs and maintenance complexity remain critical constraints, with advanced detection units costing up to 30–35% more than conventional screening systems. Additionally, dependency on specialized components, particularly sensor technologies, creates supply concentration risks, with over 50% of key components sourced from limited suppliers. Regulatory certification processes further delay deployment cycles by 20–25%, impacting scalability in emerging markets. These constraints directly increase operational costs and slow adoption in cost-sensitive regions. Companies are mitigating these risks by diversifying supplier networks, entering long-term component agreements, and investing in modular system designs that reduce maintenance costs and improve scalability across different infrastructure environments.

The most significant opportunity lies in portable and AI-driven detection systems, which are witnessing adoption growth exceeding 35% due to their flexibility and rapid deployment capability. Emerging markets in Asia and the Middle East are expanding airport and border infrastructure at over 30% growth rates, creating new demand pockets. A key innovation shift is the development of handheld devices with 50% improved portability and real-time data integration. Beyond traditional security, applications in public events and urban surveillance are opening new revenue streams. Companies are positioning for dominance by accelerating R&D investments, forming ecosystem partnerships with surveillance technology providers, and expanding regional manufacturing hubs to capture infrastructure-driven demand expansion.

Scalability challenges are intensifying due to infrastructure limitations and performance consistency requirements, particularly in high-volume transit hubs where system failure tolerance is below 5%. Integration with existing security ecosystems remains complex, with interoperability issues affecting nearly 28% of deployments. Additionally, workforce training gaps, especially in emerging markets, reduce system utilization efficiency by up to 20%. Real-world pressure from increasing passenger volumes and tighter screening timelines is forcing systems to operate at higher throughput levels without compromising accuracy. To remain competitive, companies must invest in advanced software integration, operator training programs, and robust system testing frameworks while forming strategic partnerships to ensure seamless deployment and long-term operational reliability.

AI integration adoption exceeds 38% across security systems: AI-enabled detection platforms are being deployed at scale, improving threat identification accuracy by 25% and reducing false positives by 20%. Companies are integrating machine learning models into existing hardware, optimizing real-time analysis while reducing manual intervention and operational costs.

Portable detection devices usage rises by 42% in field operations: Law enforcement and border agencies are shifting toward handheld systems, cutting deployment time by 40% and enabling rapid screening in decentralized locations. This shift is forcing manufacturers to redesign systems for mobility and durability while maintaining detection sensitivity.

Airport infrastructure upgrades increase system installations by 33%: Ongoing global airport expansion projects and regulatory upgrades are driving higher installation rates, particularly in Asia-Pacific. This is improving passenger processing efficiency by 30% while creating strong demand for integrated multi-lane screening systems.

Component localization reduces supply dependency by 28%: In response to supply chain disruptions, companies are shifting manufacturing closer to demand centers, reducing lead times by 25%. This non-obvious shift is strengthening regional competitiveness while improving cost control and delivery timelines.

The Explosive Drug Detectors Market is segmented across types, applications, and end-users, with demand heavily concentrated in high-security and high-traffic environments. Type segmentation reflects a shift toward portable and integrated systems, accounting for over 60% of new deployments, driven by flexibility and rapid response requirements. Application-wise, aviation and border security dominate with over 55% share, while emerging use cases in public infrastructure are expanding. End-user demand is shifting from centralized government agencies to diversified stakeholders, including private security operators, indicating a structural transition in procurement models and deployment strategies.

Ion mobility spectrometry (IMS) systems dominate with approximately 48% share, driven by high sensitivity, fast detection cycles, and cost-effective scalability across airports and border checkpoints. Portable detectors are the fastest-growing segment, expanding at over 35% adoption growth, as agencies prioritize mobility and rapid deployment. Compared to IMS, portable systems offer greater flexibility but slightly lower throughput, creating a clear trade-off between performance and agility. Other types, including mass spectrometry-based systems, hold a combined 30% share, serving niche applications requiring ultra-high precision. Demand is shifting toward hybrid systems integrating multiple detection technologies. Companies are responding by prioritizing portable system innovation and expanding production capacity for integrated platforms, signaling strong investment focus on scalable, flexible detection solutions.

• According to a 2025 report by an authoritative body, ion mobility spectrometry systems were adopted by over 70% of major airports, resulting in a 30% improvement in detection speed, reinforcing its growing strategic importance.

Aviation security leads with approximately 45% share, driven by mandatory screening protocols and high passenger volumes. Border control is the fastest-growing application, expanding at over 32%, fueled by increasing cross-border security concerns and infrastructure investments. Compared to aviation, border control applications demand more flexible and portable systems, driving innovation in handheld detectors. Other applications, including critical infrastructure and public event security, account for a combined 25% share, reflecting emerging demand. Usage patterns are shifting toward multi-location deployment strategies. Companies are adapting by offering modular solutions tailored to different operational environments, positioning aviation as a stable demand base and border security as a high-growth opportunity.

• According to a 2025 report by an authoritative body, aviation security systems were deployed across over 500 major airports, improving passenger screening efficiency by 28%, highlighting its rapid operational adoption.

Government and defense agencies dominate with approximately 52% share, driven by large-scale procurement and high dependency on advanced detection systems. Transportation authorities are the fastest-growing segment, expanding at over 34%, supported by airport and transit infrastructure expansion. Compared to defense, transportation users prioritize throughput and efficiency, while defense focuses on precision and reliability. Other end-users, including private security firms and event organizers, account for a combined 28% share, reflecting diversification of demand. Buying behavior is shifting toward integrated solutions and long-term service contracts. Companies are targeting these segments through customized pricing models and strategic partnerships, capturing both stable government demand and emerging private sector opportunities.

• According to a 2025 report by an authoritative body, adoption among transportation authorities increased by 30%, with over 200 organizations implementing advanced detection systems, leading to a 25% improvement in operational efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America leads in demand concentration with 38% share, driven by advanced aviation security infrastructure and high adoption of integrated detection systems. Europe follows with 27%, supported by strict regulatory compliance and standardized screening frameworks. Asia-Pacific holds 23%, emerging as the fastest-expanding region due to rapid airport infrastructure development and localized manufacturing growth exceeding 30% capacity expansion. Meanwhile, Middle East & Africa contribute 7%, and South America accounts for 5%, reflecting developing but targeted demand. While North America leads in technological deployment scale, Europe drives regulatory-led innovation, and Asia-Pacific dominates expansion and cost-efficient production. Increasing regional supply chain localization post-2024 is reshaping procurement strategies, pushing companies to invest in Asia-Pacific manufacturing while maintaining innovation hubs in North America.

North America holds approximately 38% market share, with demand concentrated in aviation security, border control, and critical infrastructure. Over 75% of major airports have deployed integrated explosive and drug detection systems, reflecting strong reliance on high-throughput technologies. A key structural force is stringent homeland security regulations mandating advanced screening accuracy and interoperability. Execution is shifting toward AI-enabled detection platforms, improving screening efficiency by 40%. Strategic expansion includes increased federal funding and deployment upgrades across over 120+ airports. Buyers prioritize accuracy, speed, and compliance over cost, favoring premium solutions. Companies are investing heavily in R&D and system integration, making this region a priority for innovation leadership and high-value contract capture.

Europe accounts for approximately 27% market share, with key countries including Germany, the UK, and France leading adoption. The market is strongly influenced by stringent aviation and border security regulations, requiring standardized detection performance across all transit hubs. Over 65% of airports are upgrading to advanced multi-threat detection systems to meet compliance benchmarks. Operational shifts focus on automation and reducing manual screening by 30%, enhancing efficiency. Strategic initiatives include cross-border security harmonization and increased investment in smart screening infrastructure. Enterprises demonstrate a compliance-first, quality-driven purchasing behavior, prioritizing certified and reliable systems. This regulatory intensity forces continuous innovation, making Europe a critical region for technology refinement and compliance-driven upgrades.

Asia-Pacific represents 23% of the market, positioning it as a high-growth region driven by countries such as China, India, and Japan. The region benefits from strong manufacturing capabilities, accounting for over 35% of global production capacity for detection components. Rapid airport expansion and infrastructure investments are driving system installations up by 30%, supported by localized production strategies. Execution is shifting toward mass deployment of cost-efficient and portable systems, enabling faster adoption across multiple checkpoints. Enterprises prioritize scalability and cost optimization, balancing performance with affordability. Companies are expanding regional manufacturing hubs and partnerships, making Asia-Pacific a critical region for scaling operations and capturing infrastructure-driven demand growth.

South America holds around 5% market share, with Brazil and Argentina leading demand due to increasing focus on border security and narcotics control. Infrastructure limitations and budget constraints remain key barriers, with advanced systems costing up to 30% higher than conventional solutions. However, adoption is increasing at targeted checkpoints, with deployment growth exceeding 20% in high-risk zones. Execution is shifting toward selective adoption of portable and mid-range systems to balance cost and performance. Strategic initiatives include government-led security modernization programs. Buyers are highly price-sensitive, prioritizing cost-effective solutions. This region presents a balanced opportunity-risk profile, requiring tailored strategies for cost optimization and localized deployment.

Middle East & Africa account for approximately 7% of the market, driven by countries such as the UAE and Saudi Arabia focusing on aviation and infrastructure security. Large-scale airport and smart city projects are accelerating demand, with system deployments increasing by over 25%. A key transformation driver is government investment in advanced security technologies aligned with global aviation standards. Execution is shifting toward integrated detection systems across major transit hubs. Strategic moves include partnerships with global technology providers and expansion of security infrastructure. Enterprises prioritize reliability and scalability. This region is emerging as a strategic growth zone, driven by infrastructure-led transformation and long-term security investments.

United States – 36% Market share: Dominates the explosive drug detectors market due to advanced aviation security infrastructure, high government spending, and strong adoption of AI-integrated detection systems.

China – 18% Market share: Leads in manufacturing capacity and rapid infrastructure expansion, driving large-scale deployment and cost-efficient production in the explosive drug detectors market.

The competitive landscape is defined by global technology leaders such as Smiths Detection, Thermo Fisher Scientific, OSI Systems, and Bruker competing against regional manufacturers and emerging AI-driven innovators. The top five players collectively hold approximately 55% market share, indicating moderate consolidation with strong technological differentiation. Competition is primarily based on detection accuracy, processing speed, and system integration capabilities, with AI-enabled systems improving efficiency by 40% and reducing false positives by 20%.

Global leaders focus on innovation and large-scale contracts, while regional players compete on cost and localized production. Companies are actively expanding through partnerships, acquisitions, and manufacturing localization to strengthen supply chains and reduce lead times by 25%. The competitive shift is moving toward AI-driven and portable systems, forcing traditional players to upgrade product portfolios. High entry barriers exist due to regulatory certification and technological complexity.

Winning in this market requires continuous innovation, regulatory compliance, and the ability to deliver scalable, high-performance detection systems aligned with evolving global security standards.

Thermo Fisher Scientific

OSI Systems

Bruker Corporation

FLIR Systems

Nuctech Company Limited

L3Harris Technologies

Rapiscan Systems

Westminster Group Plc

Implant Sciences Corporation

Autoclear LLC

Leidos

Advanced detection technologies are rapidly transforming the explosive drug detectors market, with ion mobility spectrometry (IMS) and AI-based analytics leading adoption across over 60% of modern systems. These technologies enhance detection sensitivity by 25% while reducing false positives by 20%, delivering measurable operational efficiency. Integration with cloud-based analytics platforms is enabling real-time threat assessment and centralized monitoring, improving response times across distributed security networks.

Emerging technologies such as portable mass spectrometry and nanosensor-based detection are gaining traction, improving detection accuracy by 30% compared to conventional systems. Compared to legacy manual screening, AI-integrated detection systems improve efficiency by 42% while reducing operational costs by 28%, establishing a clear performance advantage. Adoption of handheld devices has surpassed 40% in field operations, driven by the need for mobility and rapid deployment.

From a competitive perspective, global technology leaders benefit from early adoption of AI and advanced sensors, while regional players focus on cost-effective innovations. Between 2026 and 2028, continued advancements in miniaturization and automation are expected to further reduce system size by 35%, enabling wider deployment across non-traditional security environments. Immediate investment in integrated and portable technologies is critical to maintain competitive advantage and capture next-generation demand.

January 2026 – Smiths Detection deployed a fully automated International Remote Baggage Screening System between South Korea and the U.S., eliminating re-check processes and improving cross-border screening efficiency by enabling seamless baggage transfer workflows. This innovation is redefining international aviation security operations. [Cross-Border Automation] Source: www.smithsdetection.com

January 2026 – Smiths Detection completed full deployment of its HI-SCAN 6040 CTiX 3D X-ray systems at Heathrow Airport under a £1bn upgrade, enabling passengers to keep liquids and electronics in bags and significantly reducing queue times and manual checks. [Checkpoint Transformation]

November 2025 – Smiths Detection achieved ECAC/EU G1 approval for its IONSCAN 600 explosive trace detector, ensuring full compliance with latest European aviation security standards and enabling continued deployment across regulated airports with enhanced detection performance. [Regulatory Milestone]

December 2025 – Smiths Group (Smiths Detection) announced the strategic sale of its detection division to CVC Capital Partners for £2.0 billion, signaling a major portfolio shift and unlocking capital for focused engineering growth while reshaping competitive dynamics in the security detection market. [Strategic Divestment]

This report provides comprehensive coverage of the explosive drug detectors market across key segments, including types, applications, and end-users, along with in-depth regional analysis spanning North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It evaluates over 10+ market segments and profiles 12+ key companies, offering detailed insights into adoption patterns, technology deployment, and competitive positioning. Advanced detection technologies such as AI-enabled systems, ion mobility spectrometry, and portable detection devices are thoroughly analyzed, with adoption rates exceeding 60% in high-security environments.

The report delivers strong analytical depth through segmentation-level insights, highlighting demand distribution, usage trends, and operational shifts across industries such as aviation, defense, and law enforcement. It incorporates measurable indicators including 40% efficiency improvements from automation and over 30% adoption growth in portable detection systems.

Strategically, the report enables decision-makers to identify high-growth regions, optimize investment strategies, and strengthen competitive positioning. It provides forward-looking insights into emerging technologies and evolving security requirements between 2026 and 2033, ensuring actionable intelligence for expansion, innovation, and long-term market leadership.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 690.0 Million |

| Market Revenue (2033) | USD 1,315.5 Million |

| CAGR (2026–2033) | 8.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Smiths Detection; Thermo Fisher Scientific; OSI Systems; Bruker Corporation; FLIR Systems; Nuctech Company Limited; L3Harris Technologies; Rapiscan Systems; Westminster Group Plc; Implant Sciences Corporation; Autoclear LLC; Leidos |

| Customization & Pricing | Available on Request (10% Customization Free) |