Reports

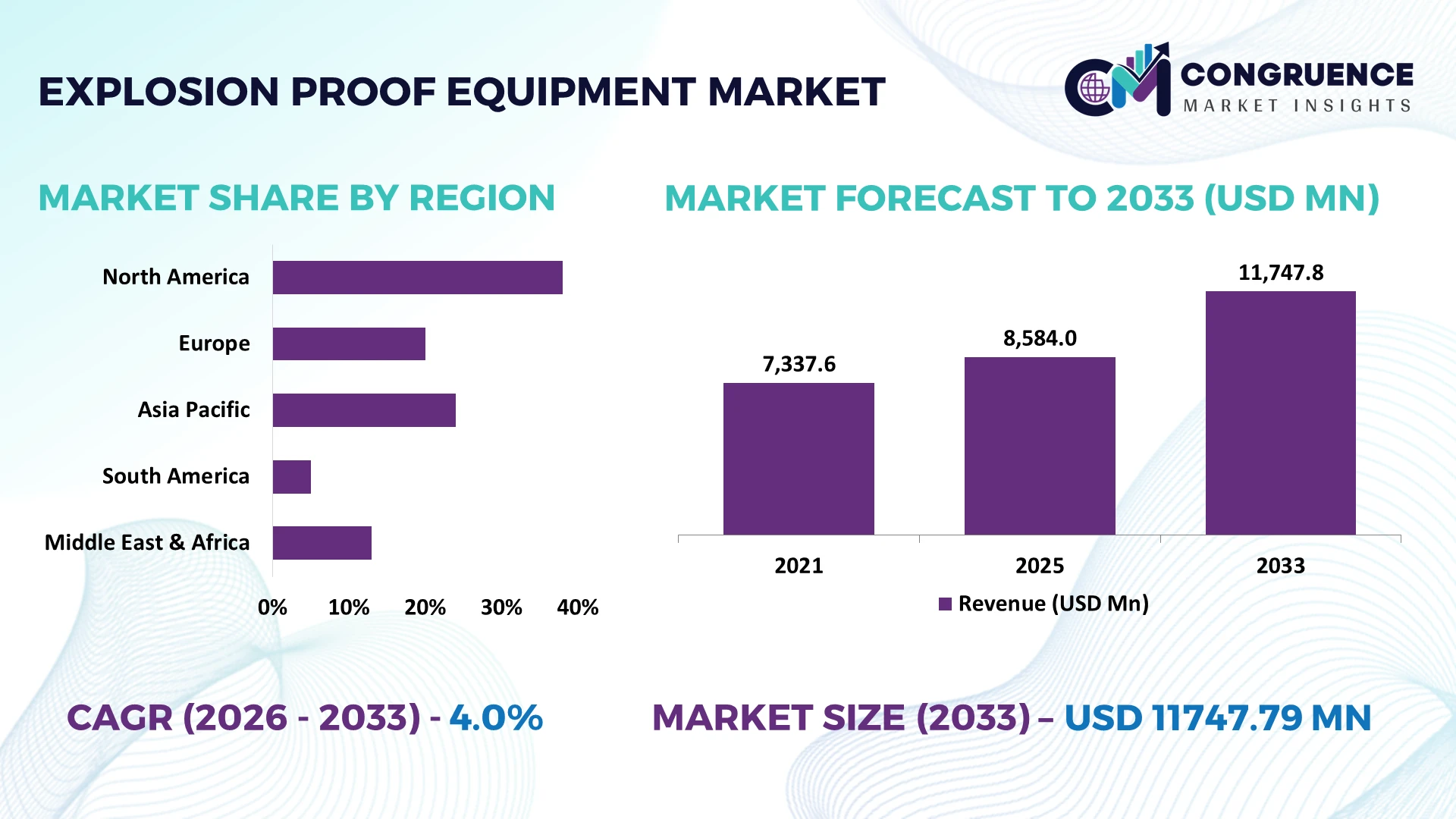

The Global Explosion Proof Equipment Market was valued at USD 8584 Million in 2025 and is anticipated to reach a value of USD 11747.79 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. Stringent hazardous-area safety regulations, rising investments in petrochemical, hydrogen, battery manufacturing, and industrial automation facilities are accelerating the deployment of certified explosion proof equipment across critical industries.

China leads the global Explosion Proof Equipment Market with approximately 31% of global manufacturing capacity, supported by continuous investments in petrochemicals, specialty chemicals, and battery production facilities. The United States accounts for nearly 24% of industrial hazardous-area installations, driven by LNG infrastructure, shale processing, and refinery modernization projects. Continued industrial supply-chain diversification following Red Sea shipping disruptions in 2026 has further strengthened regional manufacturing and adoption of digitally monitored explosion-proof systems.

Manufacturers that expand certified product portfolios, strengthen regional production capabilities, and integrate smart hazardous-area monitoring technologies will gain a stronger competitive advantage in high-growth industrial markets.

Market Size & Growth: The market was valued at USD 8584 Million in 2025 and is projected to reach USD 11747.79 Million by 2033, expanding at a CAGR of 4%, driven by industrial automation and hazardous-area modernization.

Top Growth Drivers: Industrial automation adoption (28%), hydrogen infrastructure investments (22%), and workplace safety compliance upgrades (19%) continue to accelerate global market expansion.

Short-Term Forecast: By 2028, predictive maintenance and digital monitoring are expected to reduce unplanned equipment downtime by approximately 18% across hazardous industrial facilities.

Emerging Technologies: AI-enabled diagnostics, Industrial IoT connectivity, and advanced corrosion-resistant enclosure materials improve equipment reliability by more than 20% in demanding industrial environments.

Regional Leaders: Asia Pacific is projected to reach approximately USD 4.7 Billion, North America USD 2.9 Billion, and Europe USD 2.4 Billion, supported by manufacturing expansion, energy infrastructure, and industrial digitalization.

End-User Adoption: More than 58% of newly commissioned hazardous industrial facilities integrate digitally monitored explosion proof equipment during initial project development.

Pilot Project Example: In 2026, deployment of connected explosion-proof monitoring systems at a large refinery improved maintenance efficiency by approximately 21% while strengthening operational safety performance.

Competitive Landscape: The top five manufacturers collectively account for nearly 42% of the global market, with competition focused on certified smart industrial safety technologies.

Regulatory & ESG Impact: Updated industrial safety regulations have contributed to approximately 15% lower workplace incident rates while accelerating replacement of aging hazardous-area equipment.

Investment & Funding: More than USD 3 Billion has been invested in manufacturing expansion, regional partnerships, and localized supply-chain development across strategic industrial hubs.

Innovation & Future Outlook: Wireless monitoring, edge-enabled safety devices, modular explosion-proof systems, and digital lifecycle management are strengthening next-generation industrial safety strategies worldwide.

Growing investments in hazardous industrial facilities continue to reshape the Explosion Proof Equipment Market through intelligent monitoring, flameproof enclosures, and connected safety technologies. Demand is increasing across chemicals, hydrogen, pharmaceuticals, semiconductor manufacturing, and battery production, where digital asset management adoption exceeds 35% in newly commissioned facilities. Strengthened industrial safety regulations and localized component sourcing are improving operational resilience, setting the foundation for the strategic market analysis that follows.

Explosion proof equipment has become a strategic investment priority as manufacturers modernize hazardous industrial operations while complying with increasingly stringent safety regulations. The market is shifting beyond conventional electrical protection toward digitally connected safety ecosystems that improve operational continuity across oil & gas, chemicals, pharmaceuticals, mining, hydrogen production, and battery manufacturing. Supply-chain restructuring and industrial localization since 2026 have further encouraged companies to expand certified production closer to key manufacturing hubs, reducing procurement risks and project lead times.

Smart explosion proof systems equipped with Industrial IoT sensors reduce inspection time by nearly 30% and improve maintenance efficiency by approximately 20% compared with conventional standalone equipment. China continues to lead large-scale manufacturing deployment through integrated industrial clusters, while Germany focuses on advanced engineering, digital compliance, and high-performance hazardous-area automation. Over the next two to three years, adoption of connected monitoring platforms is expected to exceed 40% across newly commissioned hazardous industrial facilities as predictive maintenance becomes a standard operating practice.

A recent refinery modernization project integrated wireless explosion-proof monitoring devices with centralized asset management, reducing manual inspection frequency while improving equipment availability. Manufacturers are responding through strategic partnerships, localized manufacturing investments, and digital product development to strengthen certification capabilities and lifecycle services. Companies that combine smart safety technologies with resilient regional supply networks will establish stronger competitive positioning in increasingly regulated industrial environments.

Rapid expansion of hazardous industrial facilities is strengthening demand for certified explosion proof equipment across energy, chemicals, pharmaceuticals, mining, and battery manufacturing. More than 58% of newly commissioned hazardous facilities now specify digitally integrated safety equipment during project planning, while industrial automation deployment has increased by approximately 28% across high-risk production environments. China's continued investment in petrochemical capacity and India's expansion of specialty chemical manufacturing are accelerating certified equipment installations. In response, manufacturers are expanding localized production, developing smart hazardous-area monitoring solutions, and forming technology partnerships to shorten delivery cycles. Companies integrating compliance, automation, and predictive maintenance into product portfolios are improving operational reliability while strengthening long-term customer retention.

Lengthy certification procedures and dependence on specialized electrical components continue to restrict deployment speed for explosion proof equipment. Certification timelines frequently extend project schedules by 15–20%, while prices for selected industrial electronic components remain approximately 12% above pre-disruption levels due to ongoing supply-chain adjustments. European manufacturers also face evolving compliance requirements that increase engineering and validation costs for multi-country product deployment. To reduce operational exposure, companies are diversifying supplier networks, localizing component sourcing, and establishing long-term procurement agreements for certified materials. Standardized product platforms are also helping manufacturers minimize redesign efforts while improving production flexibility across multiple hazardous industry applications.

The strongest opportunity lies in integrating explosion proof equipment with intelligent industrial monitoring platforms capable of delivering predictive maintenance and remote diagnostics. Connected hazardous-area assets have demonstrated maintenance cost reductions of approximately 18% while improving equipment utilization by nearly 22%. Japan and South Korea are increasing investments in smart manufacturing, creating demand for digitally certified safety infrastructure across semiconductor, electronics, and battery production facilities. Manufacturers are expanding R&D programs, collaborating with industrial software providers, and developing cloud-enabled asset management platforms that generate recurring service opportunities. The convergence of certified hardware with industrial intelligence is creating differentiated business models beyond traditional equipment sales.

Successful deployment increasingly depends on integrating explosion proof equipment with plant-wide automation, cybersecurity frameworks, and skilled technical operations. Nearly 35% of industrial facilities report shortages of qualified personnel capable of commissioning advanced hazardous-area systems, while digital integration projects typically require 20–25% longer implementation periods than conventional installations. Complex interoperability between legacy control systems and modern intelligent safety devices remains a significant operational challenge, particularly across aging industrial facilities in the United States and Europe. Companies must strengthen workforce training, expand engineering partnerships, and invest in standardized digital architectures to ensure consistent deployment quality, improve lifecycle performance, and maintain long-term competitiveness in increasingly automated industrial environments.

Explosion Proof Lighting holds the largest share of the market at approximately 34%, driven by mandatory installation across hazardous production environments and continuous replacement of conventional fixtures with energy-efficient LED systems. The segment benefits from lower maintenance requirements, improved illumination performance, and seamless integration with industrial automation platforms. Explosion Proof Enclosures and Explosion Proof Motors continue to represent mature product categories due to their essential role in protecting critical electrical assets and rotating equipment operating in explosive atmospheres.

Explosion Proof Sensors are the fastest-growing product category as industrial facilities accelerate digital monitoring and predictive maintenance initiatives. Adoption of intelligent sensing solutions has increased by nearly 29%, while connected hazardous-area monitoring has reduced manual inspection requirements by approximately 25%. Explosion Proof Control Panels are gaining importance through plant automation projects that require centralized process control and certified safety systems. Manufacturers are expanding intelligent product portfolios, strengthening automation partnerships, and investing in integrated hazardous-area solutions to address evolving industrial safety requirements and higher operational efficiency.

Oil & Gas represents the leading application segment with an estimated 38% market share, supported by extensive refinery operations, offshore platforms, LNG infrastructure, and petrochemical processing facilities that require certified explosion proof equipment. Chemical Processing continues to generate strong demand through expanding specialty chemical production and increasingly automated hazardous manufacturing operations. Mining remains an established application where underground safety regulations and modernization initiatives continue to drive equipment replacement and infrastructure upgrades.

Pharmaceuticals are emerging as the fastest-growing application as manufacturers invest in automated production lines handling volatile solvents and hazardous processing environments. Digital monitoring adoption within pharmaceutical facilities has increased by approximately 24%, while automated hazardous-area operations have expanded by nearly 18%. Power Generation is also strengthening demand through hydrogen-ready facilities and gas-based infrastructure modernization. Equipment manufacturers are developing application-specific solutions, expanding engineering services, and integrating intelligent monitoring capabilities to improve operational safety and equipment lifecycle performance.

Oil & Gas Companies account for approximately 36% of total equipment procurement owing to extensive exploration, refining, petrochemical processing, and LNG infrastructure requiring continuous safety upgrades and certified electrical systems. Chemical Manufacturers remain a major purchasing group as investments in specialty chemicals and process automation increase hazardous-area equipment requirements. Utility Companies continue strengthening procurement through modernization of gas-fired power facilities and hydrogen-compatible electrical infrastructure.

Pharmaceutical Manufacturers are the fastest-growing end-user category as regulatory compliance and automated production environments increase demand for certified explosion proof systems. Smart hazardous-area equipment deployment among pharmaceutical producers has increased by approximately 22%, while integrated monitoring technologies have improved maintenance efficiency by nearly 17%. Mining Companies continue investing in intelligent underground safety infrastructure and equipment modernization. Manufacturers are responding through customized product development, lifecycle service agreements, strategic industrial partnerships, and sector-specific engineering support to strengthen long-term customer relationships.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 5.3% CAGR between 2026 and 2033.

Industrial Modernization Strengthens Hazardous-Area Automation

North America represents a mature Explosion Proof Equipment Market supported by advanced industrial infrastructure, accounting for approximately 26% of global demand. Continuous modernization across oil & gas, chemicals, pharmaceuticals, mining, and LNG processing is driving replacement of conventional safety systems with digitally connected explosion proof equipment. More than 55% of newly upgraded hazardous facilities now incorporate intelligent monitoring platforms integrated with plant automation systems. Investments in industrial cybersecurity and predictive maintenance are further increasing deployment of certified hazardous-area electrical equipment. Manufacturers are expanding engineering capabilities, strengthening distribution partnerships, and increasing localized production to reduce project delivery timelines while supporting stringent industrial safety compliance across critical infrastructure.

United States Market Outlook: The United States leads regional demand through extensive refining capacity, shale production, petrochemical complexes, and pharmaceutical manufacturing. More than 60% of hazardous industrial modernization projects include connected explosion proof monitoring technologies, reflecting increasing investment in operational reliability and compliance. Domestic manufacturers continue expanding certified production capacity while collaborating with industrial automation providers to deliver integrated hazardous-area solutions across large industrial facilities.

Engineering Excellence Drives Certified Industrial Safety

Europe accounts for approximately 22% of the global market, supported by advanced manufacturing, strict industrial safety regulations, and continuous modernization of chemical, pharmaceutical, food processing, and energy infrastructure. Industrial operators are accelerating replacement of legacy hazardous-area equipment with digitally integrated certified systems that improve operational visibility and maintenance planning. Nearly 48% of hazardous industrial upgrades now include intelligent monitoring capabilities to strengthen compliance and plant efficiency. Manufacturers are focusing on high-performance certified products, automation integration, and engineering innovation while expanding partnerships with industrial technology providers to support increasingly complex operational requirements.

Germany Market Outlook: Germany remains the largest market within Europe due to its strong industrial manufacturing base, advanced automation ecosystem, and leadership in hazardous-area engineering. Nearly 45% of industrial automation projects within hazardous facilities integrate certified explosion proof electrical systems. German manufacturers continue investing in smart manufacturing technologies, advanced product certification, and engineering innovation to strengthen industrial competitiveness across domestic and export markets.

Large-Scale Industrial Expansion Sustains Market Leadership

Asia-Pacific dominates the global Explosion Proof Equipment Market with approximately 41% market share, supported by large-scale manufacturing, petrochemical expansion, mining operations, battery production, and infrastructure development. Industrial investment across hazardous processing facilities continues to accelerate deployment of certified electrical equipment and intelligent monitoring systems. More than 35% of newly commissioned hazardous manufacturing facilities incorporate connected explosion proof technologies during initial construction. Regional manufacturers are expanding production capacity, strengthening export capabilities, and increasing investment in digital safety technologies to support rising industrial automation and regulatory compliance requirements.

China Market Outlook: China remains the region's largest contributor through extensive petrochemical production, specialty chemical manufacturing, battery manufacturing, and industrial automation investments. Approximately 31% of global explosion proof equipment manufacturing capacity is concentrated in China, supported by integrated industrial clusters and localized component supply chains. Domestic companies continue expanding intelligent product portfolios while increasing certification capabilities and advanced manufacturing investments to strengthen international competitiveness.

Resource Industries Drive Equipment Modernization

South America continues to strengthen demand for explosion proof equipment through mining, oil & gas production, chemical processing, and expanding industrial infrastructure. The region contributes approximately 7% of global demand, with hazardous industrial modernization projects increasing deployment of certified electrical equipment across production facilities. Digital monitoring adoption has increased by nearly 18% as industrial operators prioritize operational safety and maintenance efficiency. While logistics infrastructure and equipment availability remain execution challenges, manufacturers are expanding distributor networks, localized technical support, and regional partnerships to improve project implementation and after-sales service.

Brazil Market Outlook: Brazil leads regional demand due to its offshore oil production, mining activities, and growing chemical manufacturing sector. More than 50% of large industrial safety upgrade projects involve certified hazardous-area electrical equipment to strengthen compliance and operational continuity. Equipment suppliers continue expanding regional engineering support, service capabilities, and strategic industrial partnerships to address increasing modernization requirements across critical industries.

Energy Infrastructure Investments Accelerate Deployment

The Middle East & Africa is emerging as the fastest-expanding regional market, supported by large-scale investments in oil & gas infrastructure, petrochemical complexes, LNG facilities, mining operations, and industrial diversification initiatives. The region represents approximately 11% of global demand while experiencing rapid deployment of certified hazardous-area equipment across newly developed industrial assets. More than 30% of recent energy infrastructure projects include intelligent explosion proof monitoring systems designed to improve operational efficiency and plant reliability. Manufacturers are strengthening regional distribution networks, certification capabilities, and engineering partnerships to support expanding industrial investment programs.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's most strategically significant market through continuous investment in petrochemical production, refinery expansion, industrial cities, and energy infrastructure modernization. Hazardous industrial developments increasingly integrate connected explosion proof technologies, with digitally monitored safety systems incorporated into more than 40% of newly commissioned large-scale industrial facilities. Global manufacturers continue expanding regional partnerships, localized engineering services, and certified product availability to support long-term industrial transformation.

The Explosion Proof Equipment Market is led by Eaton, Emerson Electric, ABB, Siemens, Honeywell, and R. Stahl, with global technology leaders competing directly against regional manufacturers specializing in certified hazardous-area products and cost-efficient customization. The top five companies collectively account for approximately 42% of the global market, creating competition centered on intelligent safety systems, engineering expertise, and delivery capability rather than price alone. Premium manufacturers compete through digital monitoring, predictive diagnostics, and integrated automation, improving maintenance efficiency by nearly 20%, while regional suppliers remain competitive by reducing delivery lead times by approximately 15% through localized manufacturing. Companies are expanding production facilities, strengthening industrial automation partnerships, pursuing vertical integration for critical components, and developing software-enabled lifecycle services. Competitive momentum is shifting toward connected explosion proof platforms that combine hardware with real-time asset intelligence, increasing switching costs for industrial customers. Product certification complexity and regulatory compliance remain major entry barriers. Winning requires certified innovation, resilient supply networks, rapid engineering support, and integrated digital safety capabilities.

Eaton

Emerson Electric Co.

ABB Ltd.

Siemens AG

Honeywell International Inc.

R. Stahl AG

Pepperl+Fuchs SE

BARTEC Group

Rockwell Automation, Inc.

Warom Technology Incorporated Company

Adalet

Cortem S.p.A.

Extronics Ltd.

Hubbell Incorporated

Digital transformation is redefining explosion proof equipment through Industrial IoT integration, AI-enabled diagnostics, wireless monitoring, and intelligent asset management platforms. Connected hazardous-area equipment now supports continuous condition monitoring across approximately 45% of newly modernized industrial facilities, while predictive maintenance lowers unplanned downtime by nearly 20%. Companies are integrating certified hardware with cloud-based monitoring software to improve operational visibility, maintenance scheduling, and regulatory compliance across high-risk industrial environments.

Conventional standalone explosion proof equipment is increasingly being replaced by connected intelligent systems capable of remote diagnostics and automated asset monitoring. Compared with legacy installations, modern digital platforms reduce inspection time by approximately 30% while improving maintenance productivity by nearly 22%. Large automation providers and certified equipment manufacturers gain the greatest competitive advantage by delivering integrated hardware, software, and lifecycle services, whereas traditional hardware-only suppliers face increasing competitive pressure as industrial customers prioritize operational intelligence over isolated equipment performance.

Between 2026 and 2028, edge computing, AI-assisted fault detection, digital twins, and wireless hazardous-area communication are expected to become standard components of industrial modernization projects. More than 50% of newly commissioned hazardous facilities are projected to deploy connected explosion proof monitoring platforms integrated with enterprise automation systems. Manufacturers investing in cybersecurity, intelligent certification platforms, and interoperable digital ecosystems will strengthen long-term customer retention, improve service revenues, and establish sustainable competitive differentiation as industrial operations become increasingly data-driven and autonomous.

May 2026 Pepperl+Fuchs introduced a high-current Electronic Processing Control Unit (EPCU) for its 6000 Series purge and pressurization system, increasing enclosure contact capacity from 8 A to 12 A per contact. The enhancement supports higher-current applications while reducing auxiliary hardware requirements and project costs.

November 2025 ABB launched the System 800xA High Integrity R7.1 distributed control system with SIL 3 certification and OPC UA PubSub connectivity for hazardous-area operations. The release strengthens deterministic communication with Zone 1 devices, improving industrial safety and automation integration.

October 2025 Honeywell expanded its industrial safety software portfolio by acquiring Safety Manager SC, adding automated SIL verification capabilities to the Honeywell Forge platform. The integration streamlines functional safety validation and strengthens digital lifecycle management for hazardous industrial facilities.

September 2025 Eaton introduced the ACE10 Class I, Division 1 variable frequency drive featuring integrated active harmonic filtering and regenerative braking technology. The innovation improves power quality and energy efficiency while simplifying deployment in hazardous industrial environments.

This report provides comprehensive analysis of the Explosion Proof Equipment Market across product categories, applications, end-user industries, competitive dynamics, technology trends, and regional performance. It evaluates Explosion Proof Lighting, Motors, Enclosures, Sensors, and Control Panels across Oil & Gas, Chemical Processing, Mining, Power Generation, and Pharmaceutical applications while assessing procurement trends among major industrial end users. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, industrial modernization, and hazardous-area infrastructure developments.

The report examines adoption patterns across intelligent monitoring, Industrial IoT integration, predictive maintenance, and certified automation systems, with connected hazardous-area equipment exceeding 40% adoption in newly modernized industrial facilities. It also evaluates competitive positioning, investment priorities, supply-chain developments, regional manufacturing capabilities, and emerging industrial opportunities between 2026 and 2033, enabling businesses to strengthen expansion planning, technology investments, partnership strategies, operational resilience, and long-term market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 8584 Million |

Market Revenue in 2033 | USD 11747.79 Million |

CAGR (2026 - 2033) | 4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Eaton, Emerson Electric Co., ABB Ltd., Siemens AG, Honeywell International Inc., R. Stahl AG, Pepperl+Fuchs SE, BARTEC Group, Rockwell Automation, Inc., Warom Technology Incorporated Company, Adalet, Cortem S.p.A., Extronics Ltd., Hubbell Incorporated |

Customization & Pricing | Available on Request (10% Customization is Free) |