Reports

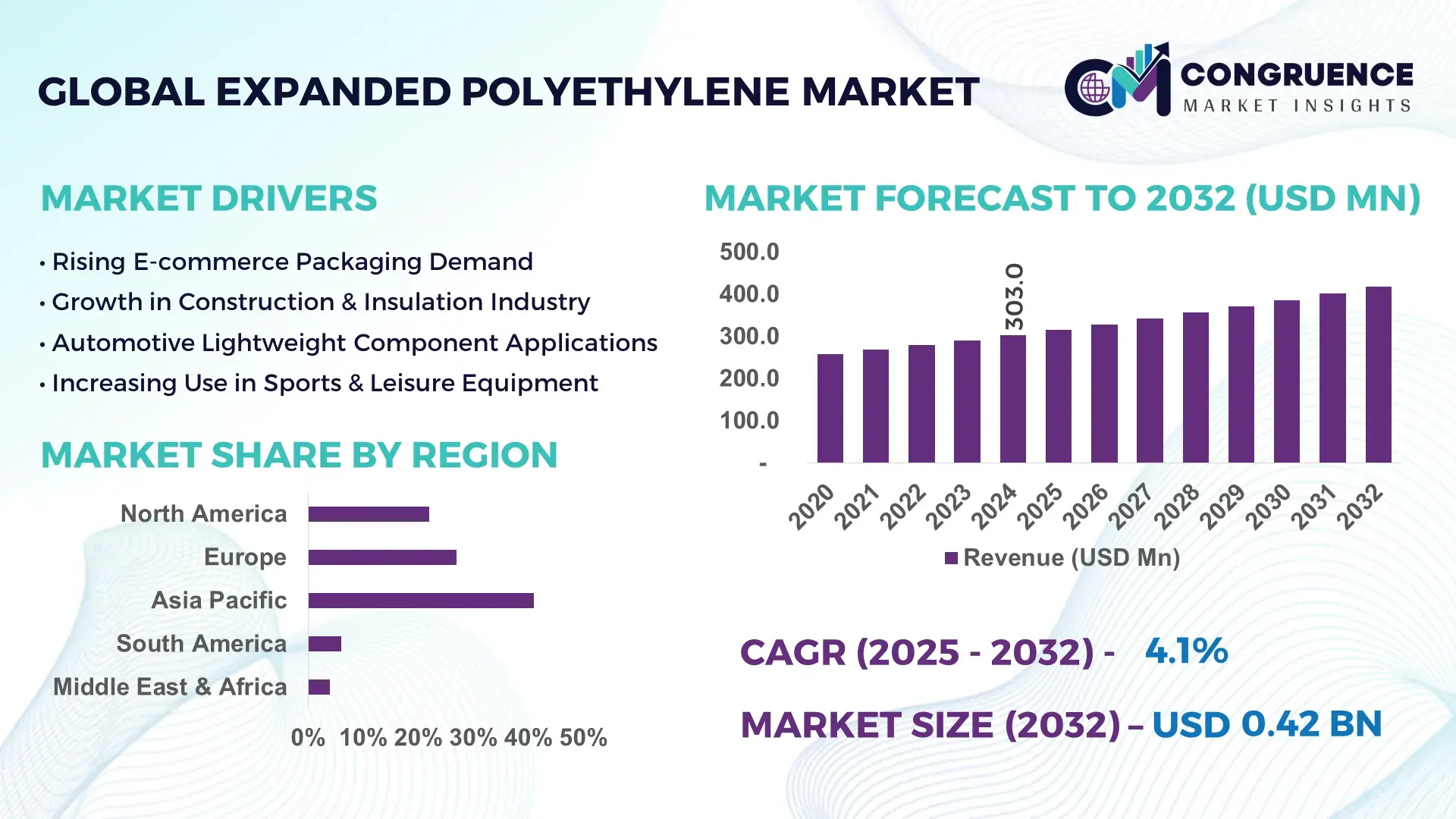

The Global Expanded Polyethylene Market was valued at USD 303.0 Million in 2024 and is anticipated to reach a value of USD 417.9 Million by 2032, expanding at a CAGR of 4.10% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is supported by rising penetration of lightweight, durable, and recyclable polymer foams in protective packaging and industrial insulation applications.

The market is significantly shaped by developments in China, which holds one of the world’s largest EPE production ecosystems backed by an estimated 2.8–3.0 million tons per year polymer processing capacity. The country continues to expand its high-density EPE extrusion capabilities, supported by more than USD 1.2 billion annual investments in packaging materials and automated foam conversion technologies. China’s EPE industry is characterized by rapid adoption of precision molding systems, with over 40% of EPE converters integrating high-speed, energy-efficient extruders to meet demand from electronics, automotive interiors, and logistics sectors. Continuous advancements in cross-linking, foam density control, and flame-retardant formulations further strengthen China's technical edge in the global Expanded Polyethylene Market.

Market Size & Growth: Market valued at USD 303.0 Million in 2024, projected to reach USD 417.9 Million by 2032, growing at 4.10% CAGR, driven by rising demand for lightweight protective packaging across high-growth manufacturing sectors.

Top Growth Drivers: 38% rise in protective packaging adoption; 42% improvement in foam processing efficiency; 33% increase in demand for shock-absorption materials.

Short-Term Forecast: By 2028, automation-led production systems expected to deliver 18% reduction in processing cost and 22% improvement in foam density consistency.

Emerging Technologies: Advancements in energy-efficient extruders, precision cross-linking technologies, and smart foam molding systems enhancing consistency and durability.

Regional Leaders: Asia Pacific projected to reach USD 228 Million by 2032, Europe USD 94 Million, North America USD 68 Million, each witnessing distinct adoption trends in packaging, automotive, and construction.

Consumer/End-User Trends: Electronics packaging accounts for fast-rising adoption, with nearly 46% of consumers preferring impact-resistant foam solutions for high-value goods.

Pilot or Case Example: A 2027 industrial packaging pilot in Japan achieved 21% reduction in transit damage using advanced high-density EPE formulations.

Competitive Landscape: Market led by a key manufacturer with approximately 12% share, followed by major competitors including Sealed Air, Armacell, Recticel, JSP Corporation, and Plymouth Foam.

Regulatory & ESG Impact: Increasing emphasis on recyclable polymer usage and mandates driving 25% improvement in eco-compliant foam materials by 2030.

Investment & Funding Patterns: Recent investments exceeding USD 420 Million in capacity expansion, energy-efficient extrusion lines, and upgraded foam molding facilities.

Innovation & Future Outlook: Next-generation EPE composites, ultra-light foams, and hybrid polymer blends expected to accelerate adoption in automotive, healthcare, and logistics.

The Expanded Polyethylene Market is supported by strong demand from industrial packaging, automotive cushioning, construction insulation, and logistics sectors, with innovations in high-density foams and eco-compliant materials driving new application opportunities. Advancements in extrusion, cross-linking efficiency, and recyclability, combined with favorable regulatory shifts and rising demand in Asia and Europe, contribute to a strengthened outlook for the industry.

The strategic relevance of the Expanded Polyethylene Market lies in its expanding role across packaging, automotive, construction, logistics, and consumer goods supply chains. As industries prioritize lightweight, recyclable, and shock-absorbent materials, EPE serves as a critical performance enabler. Next-generation cross-linked foams and energy-efficient extrusion technologies are improving durability and impact resistance. For example, new thermal-stabilized EPE grades deliver up to 27% improvement in compressive strength compared with older non-stabilized formulations, expanding suitability for high-load and high-temperature applications.

Regional variations continue to influence strategic pathways. Asia Pacific dominates in volume, supported by large-scale polymer processing infrastructure, while Europe leads in adoption, with over 56% of enterprises deploying sustainable EPE packaging solutions to meet circular economy goals. By 2028, AI-enabled extrusion control systems are expected to improve production efficiency by 19%, reducing material wastage and optimizing foam density. Such technologies enhance long-term competitiveness, particularly in high-value applications such as medical packaging, automotive parts protection, and precision electronics.

Regulatory and ESG requirements are also reshaping pathways. Manufacturers are committing to 35% recycling efficiency improvement by 2030 in line with global sustainability directives. Many countries are enforcing stricter polymer recovery targets, encouraging investment in advanced recycling, foam reprocessing, and low-emission manufacturing lines. Micro-innovations further illustrate the market’s trajectory: in 2027, a South Korean EPE manufacturer achieved 24% reduction in energy consumption using a smart-extrusion initiative powered by predictive analytics.

Overall, the Expanded Polyethylene Market is positioned as a pivotal contributor to resilient packaging, sustainable product engineering, and advanced logistics solutions. With technology-driven upgrades, ESG compliance, and cross-sector adoption accelerating, the market is expected to become a cornerstone of high-performance material systems aligned with global sustainability and efficiency priorities.

The Expanded Polyethylene Market demonstrates consistent forward momentum driven by rising industrial, commercial, and consumer-sector applications. Technological upgrades in foam extrusion, density optimization, and cross-linking methods continue to influence market behavior. Growing demand for impact-resistant protective packaging, especially for electronics, automotive supplies, and e-commerce logistics, strengthens market fundamentals. Regulatory moves toward recyclable materials and improved polymer recovery rates are further shaping industry choices. Meanwhile, expansion of high-speed manufacturing lines, together with increased investments in automated quality-control systems, is helping improve reliability, reduce material losses, and support scalability. These dynamics position the market for steady, innovation-led development.

Rising global demand for high-performance protective packaging is a key driver supporting growth in the Expanded Polyethylene Market. The expansion of e-commerce, which saw package volumes increase by over 20% annually in several regions, is creating a heightened need for durable, shock-absorbing materials. EPE provides excellent cushioning, insulation, and reusability—attributes essential for the safe transit of electronics, medical devices, and industrial goods. Manufacturers are increasingly shifting toward lightweight foams that reduce shipping weight by up to 15%, contributing to logistics cost optimization. Adoption of high-density EPE in automotive and appliance packaging has also risen by more than 30% in the past five years, owing to improved resistance to vibration and impact. Industries integrating automated packaging lines benefit from EPE’s adaptability, enabling faster packing speeds and reduced damage rates. Collectively, these factors ensure that advanced packaging remains a fundamental growth catalyst.

Fluctuating costs of key raw materials—particularly polyethylene resins—pose a substantial restraint to the Expanded Polyethylene Market. Price volatility of ethylene feedstock, influenced by fluctuating crude oil prices and supply-chain imbalances, can lead to cost variations of 10–18% in polymer procurement. This impacts manufacturers operating with tight production margins and high energy usage. Additionally, transportation and energy expenses have increased significantly in multiple regions, with electricity costs rising up to 22% in certain manufacturing clusters. EPE production is energy-intensive, and spikes in power tariffs directly affect foam extrusion and molding economics. Regulatory restrictions on plastic waste further add compliance costs, requiring investment in recycling, waste-collection, and eco-certification systems. These combined pressures limit pricing flexibility and affect profitability, particularly for small and mid-scale producers unable to absorb rapid cost fluctuations.

Technological advancements are opening substantial opportunities for next-generation EPE products with improved durability, thermal stability, and environmental compatibility. High-precision extrusion technologies now enable density uniformity improvements of 12–16%, supporting applications in automotive insulation, HVAC systems, and consumer appliances. The shift toward circular materials presents another opportunity, with recycling-ready EPE grades gaining traction as industries target 30–40% reduction in polymer waste by 2030. Growth in green construction is also spurring demand for lightweight thermal-insulation foams, where usage of EPE has increased by nearly 25% across Asia and the Middle East. Emerging hybrid foams blending EPE with EVA or cross-linked PE are broadening performance capabilities for sports goods, healthcare packaging, and specialty consumer products. These innovation-driven pathways position the market for sustained value creation.

The Expanded Polyethylene Market faces challenges in navigating evolving regulatory frameworks that emphasize recyclability, emissions control, and sustainable materials. Governments across Europe, North America, and parts of Asia are implementing stricter requirements on polymer waste collection, with recycling targets increasing by 20–35% in recent mandates. Compliance with such policies necessitates investment in updated processing technologies, waste-recovery lines, and eco-certification procedures. Additionally, the technical limitation of achieving consistent foam density and cell structure at high production speeds remains a challenge for many manufacturers. High-density EPE grades may exhibit 8–10% variation in mechanical performance when produced on outdated equipment, affecting suitability for premium applications. Workforce skill shortages in operating advanced extrusion systems and maintaining precision controls also pose operational hurdles. These challenges collectively require strategic manufacturing upgrades and robust quality-control systems.

Technological Advancements in High-Density EPE: Manufacturers are increasingly adopting next-generation extrusion systems that deliver up to 18% improvement in foam density accuracy and 14% reduction in cell-size variation. This supports applications in automotive interiors and industrial cushioning. Automated inspection systems have improved defect detection rates by over 30%, enhancing product consistency across large-scale production environments.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Expanded Polyethylene Market. Research indicates that 55% of new modular projects experienced measurable cost efficiency. Automated cutting and prefabrication technologies reduce labor requirements and shorten project timelines by 12–18%. Demand for precision-engineered EPE components continues to rise in Europe and North America due to stringent energy-efficiency requirements.

Shift Toward Recyclable and Eco-Compliant Foams: Growing environmental regulations are driving a shift toward recyclable EPE formulations, with adoption increasing by more than 28% globally. New foam grades enable up to 40% material recovery, supporting circular-economy targets. Manufacturers integrating low-emission extrusion lines report 15% energy savings, strengthening the viability of sustainable polymer production.

Expansion in Logistics and E-Commerce Applications: The surge in global e-commerce, expanding at 17–22% annually in several markets, is driving higher demand for protective EPE packaging. Damage reduction rates improved by up to 25% when using advanced high-density EPE cushioning. Logistics and electronics manufacturers increasingly prefer EPE for its lightweight structure, reducing shipping loads by 8–12%, and improving transport efficiency.

The Expanded Polyethylene Market is structured across three core segmentation pillars—types, applications, and end-user categories—each reflecting distinct performance dynamics and adoption patterns. Type-wise distribution demonstrates clear differentiation in density, flexibility, and energy-absorption capabilities, with certain variants preferred across protective packaging, construction, and automotive cushioning. Application segmentation reveals strong penetration in electronics packaging, industrial transport systems, and building insulation, supported by rising demand for impact-resistant, lightweight materials. End-user insights show significant adoption by manufacturing, e-commerce, automotive, and consumer-goods sectors, each leveraging expanded polyethylene for product protection, thermal regulation, and operational efficiency. The interplay among these segments illustrates how shifting safety standards, e-commerce expansion, and materials innovation shape overall demand. Together, these segmentation dimensions define the industry’s structural landscape and offer a comprehensive view into adoption behavior, performance requirements, and evolving usage priorities across global markets.

The type segment of the Expanded Polyethylene Market comprises high-density EPE, low-density EPE, cross-linked EPE, and specialty engineered variants tailored for industrial performance needs. Among these, high-density EPE currently accounts for approximately 46% of adoption, driven by its superior mechanical strength, enhanced impact resistance, and suitability for electronics, appliances, and automotive packaging. Low-density EPE follows with about 28% share, offering excellent flexibility and a lightweight profile that supports widespread use in consumer packaging and cushioning applications. Cross-linked EPE, while holding a smaller share, remains the fastest-growing type, supported by increasing demand for premium insulation, vibration damping, and precision-formed components. Growth is further reinforced by technological improvements in cross-linking uniformity, enabling performance advantages over conventional foams. The remaining specialty formulations—including anti-static, laminated, and flame-retardant EPE—contribute a combined 26% share, serving niche sectors such as electronics cleanrooms, medical packaging, and high-heat industrial settings where enhanced functional attributes are required.

The application landscape of the Expanded Polyethylene Market spans protective packaging, construction, automotive components, sports and leisure equipment, and industrial insulation. Protective packaging leads the market with nearly 48% share, driven by rapid expansion in electronics shipments, e-commerce logistics, and consumer-goods transportation. In comparison, construction applications account for around 24%, primarily due to the material’s strong thermal-insulation and moisture-resistance attributes, while automotive applications represent approximately 18%, supported by rising use in vibration damping and interior cushioning components. However, industrial insulation is emerging as the fastest-growing application, propelled by increased demand for lightweight thermal barriers and energy-efficient systems, projected to exceed 28% adoption by 2032, surpassing several conventional use cases. Other applications—including sports goods, medical packaging, and specialty cushioning—represent a combined 10% share. Growing consumer trends also influence adoption: in 2024, more than 38% of global enterprises reported integrating advanced cushioning materials for product-damage reduction, reflecting heightened quality-control priorities; additionally, over 60% of consumers in high-income markets reported higher satisfaction with products shipped using premium protective foams, demonstrating the direct link between material choice and customer experience.

End-user adoption of Expanded Polyethylene reflects strong penetration across manufacturing, e-commerce, automotive, construction, healthcare, and consumer-goods sectors. Manufacturing and industrial users lead with approximately 41% share, leveraging EPE for machinery protection, component packaging, and material-handling applications. In contrast, e-commerce and retail account for about 29%, supported by rapid online-order growth and the need for reliable, lightweight cushioning during last-mile delivery. Automotive end-users hold nearly 17%, with rising integration of vibration-damping components and lightweight interior padding. However, the construction sector is the fastest-growing, supported by increasing adoption of thermal-insulation materials, flexible sealing systems, and sound-absorption foams, with growth expected to exceed 30% adoption by 2032, driven by modern building-efficiency standards. Other end-users—including healthcare, sports equipment manufacturers, and consumer-goods brands—represent a combined 13% share, each drawing on EPE’s durability, water resistance, and customizability. Industry behavior further validates this growth: in 2024, over 42% of mid-scale manufacturing firms reported increased use of advanced polymer foams in production workflows, reflecting the broadening utility of engineered materials. Similarly, consumer-goods companies noted a 25% rise in demand for high-quality protective packaging, emphasizing shifting expectations around product safety and brand reliability.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

Asia-Pacific maintained its dominant position due to its large manufacturing base, high-volume packaging consumption, and continued investments across electronics, automotive, and industrial insulation applications. With China contributing nearly 24% of global demand and India adding another 9%, the region’s combined influence surpasses all others. Europe followed with a 27% share, while North America accounted for 22% of total consumption. South America and the Middle East & Africa together represented around 10%, demonstrating emerging opportunities. The fast-growing Middle East & Africa region is increasingly driven by construction, logistics, and polymer processing expansion, supported by government-backed industrial diversification programs and capacity additions. Rising demand for lightweight foams across infrastructure and consumer packaging also boosts the region’s growth outlook.

North America accounted for approximately 22% of the global Expanded Polyethylene market in volume terms in 2024, supported by advanced manufacturing activities and strong adoption across automotive, electronics, and industrial packaging sectors. The region benefits from early integration of automation, digital tracking, and protective packaging innovations, particularly in the U.S. retail and e-commerce landscape. Industries such as healthcare, food processing, and consumer electronics remain major contributors to demand. The regulatory environment—especially U.S. recyclable material standards and extended producer responsibility (EPR) frameworks—continues to influence product development trends. Local players such as Pregis LLC are expanding their high-density EPE foam offerings tailored for impact-resistant shipping applications. Consumer behavior trends reflect higher enterprise adoption in healthcare and finance, where precision packaging and advanced insulation materials are preferred due to stringent quality and safety norms.

Europe represented approximately 27% of the Expanded Polyethylene market in 2024, driven by strong demand from Germany, France, the UK, and Italy. The region is heavily shaped by circular economy regulations, plastics tax frameworks, and EU Green Deal initiatives that promote sustainable and recyclable material usage. Key industries—including automotive, machinery, logistics, and high-value electronics—continue adopting modified EPE grades to meet durability and lightweighting needs. European players are also integrating bio-based polyethylene feedstocks and advanced extrusion technologies to reduce carbon intensity. Companies such as Sealed Air Europe are focusing on specialized EPE solutions for temperature-sensitive pharmaceutical shipments. Consumer behavior patterns are influenced by strict sustainability expectations, leading to greater emphasis on traceability, compliance, and environmentally responsible packaging design.

Asia-Pacific remained the largest regional market with 41% of global consumption in 2024, backed by high-volume production and extensive downstream industries. China, India, Japan, and South Korea are top contributors due to their robust electronics manufacturing clusters, automotive components industry, and expanding logistics networks. The region’s rapid infrastructure development and growing demand for protective packaging in fast-moving consumer goods (FMCG) reinforce consumption patterns. Innovations such as high-strength cross-linked EPE foams and robotic-assisted manufacturing lines are increasingly adopted in industrial zones across China and Southeast Asia. Companies such as Zhejiang Huali continue to expand EPE capacity for export markets. Consumer behavior is significantly shaped by e-commerce penetration—particularly in India and Southeast Asia—driving higher usage of lightweight protective packaging and flexible foam materials.

South America held an estimated 6% of global EPE demand in 2024, led primarily by Brazil and Argentina. The region’s industrial packaging, automotive aftermarket, and agricultural sectors remain key demand drivers. With modernized manufacturing infrastructure and rising investments in food processing and electronics assembly, the need for reliable cushioning and insulation materials continues to grow. Regional governments have introduced incentives for packaging modernization and local polymer processing capacity, promoting increased adoption of polyethylene-based foams. Local players such as Termotécnica (Brazil) have expanded their portfolio of molded and extruded foam solutions for perishables and industrial logistics. Consumer behavior trends show higher demand for cost-effective, durable protective packaging supported by growing media, electronics, and language localization industries across the region.

The Middle East & Africa region accounted for roughly 4% of global EPE demand in 2024 but is expected to be the fastest-growing region through 2032 due to strong industrialization and packaging modernization efforts. High consumption arises from oil & gas insulation, construction materials, and protective packaging for heavy machinery. Countries such as the UAE, Saudi Arabia, and South Africa remain major growth centers due to rapid infrastructure expansion and adoption of lightweight polymeric materials across logistics and manufacturing. Governments continue supporting industrial diversification programs that stimulate plastics processing and downstream polymer industries. Local manufacturers like Interplast (UAE) are increasingly expanding foam extrusion capacity to cater to regional demand. Consumer behavior reflects growing preference for durable, moisture-resistant packaging in retail, construction, and industrial supply chains.

China – 24% Market Share: Strong dominance due to massive manufacturing output, extensive packaging demand, and high-volume production capacity.

United States – 14% Market Share: Leadership driven by advanced packaging technologies, strong industrial demand, and rapid adoption of high-performance EPE solutions.

The global Expanded Polyethylene (EPE) market shows a semi-consolidated competitive structure, with an estimated 25–35 active global competitors, including multinational manufacturers and numerous regional producers. The top five companies collectively hold about 55–60% of the global share, demonstrating moderate concentration while still allowing room for smaller, agile players. Large manufacturers continue to enhance their market position by investing in capacity expansions, sustainable EPE grades, and advanced engineered foam solutions tailored for automotive, insulation, electronics, and e-commerce packaging.

Competitive strategies increasingly revolve around product differentiation, including enhanced cross-linked formulations, anti-static EPE variants, and customized density grades. Some leading producers are also expanding facilities to support production using recycled polyolefin feedstock, aligning with rising demand for circular-economy–oriented materials. Additionally, automation in converting, cutting, and molding processes is becoming a crucial differentiator, as it enables precision, lower waste, and faster delivery cycles.

Regional manufacturers — especially in Asia-Pacific — remain competitive due to cost-efficient production, localized supply chains, and the ability to serve high-volume domestic demand. These players compete on price, speed, and customization flexibility, maintaining a diverse supplier ecosystem globally. Overall, the EPE market reflects a balance between technology-driven global leaders and cost-focused regional firms, making strategic supplier selection an important consideration for buyers.

Pregis LLC

Kaneka Corporation

Sonoco Products Company

Furukawa Electric Co., Ltd.

Wisconsin Foam Products, Inc.

Technological innovation is reshaping the Expanded Polyethylene market, shifting it from a conventional packaging substrate to a high-performance engineered material used across industrial applications. Advancements in cross-linking technology have enabled EPE foams with improved tensile strength, thermal resistance, uniform density, and long-term durability. These enhanced foams are increasingly used in automotive interiors, HVAC insulation, sports equipment, and premium consumer electronics packaging.

Another major trend is the development of recycling-ready and sustainable EPE formulations. Modern extrusion systems are being upgraded to process recycled polyethylene feedstock while maintaining mechanical stability and cell structure. This transition supports global sustainability initiatives and helps manufacturers reduce material costs. Alongside sustainability, additive-enhanced foams—including anti-static, flame-retardant, UV-resistant, and cushioning-modified EPE—are gaining adoption in sectors that demand specialized performance characteristics.

Manufacturing automation is also advancing rapidly. Digital process controls, AI-based quality monitoring, and precision cutting systems enable consistent foam output with minimal variability and reduced wastage. Automated molding and CNC-cutting machines now allow producers to deliver custom-shaped components for industries requiring precise dimensions and repeatability.

The integration of Industry 4.0 technologies, including real-time monitoring of density, temperature, and cell expansion behavior, ensures tighter production tolerances and higher product quality. These innovations are expanding the application scope of EPE and strengthening the competitive positioning of technologically capable manufacturers.

In Feb 2024, Pregis announced a new range of PE foam products formulated with certified-circular polyethylene resins developed in collaboration with advanced-recycling partners, enabling protective foam packaging with higher recycled content and supporting corporate plastics-circularity targets. Source: www.pregis.com

In June 24, 2024, Sonoco announced a definitive agreement to acquire Eviosys (European metal packaging manufacturer) in a transaction intended to expand Sonoco’s packaging portfolio and generate projected operational synergies upon closing. Source: www.sonoco.com

In Feb 2024, Armacell published preliminary 2023 results and outlined continued investment in engineered foam capabilities and production footprint upgrades—highlighting net sales growth and planned production/R&D investments to support advanced insulation and engineered-foam offerings. Source: www.armacell.com

In H1 2024 disclosure, released Aug 2024, Zotefoams’ H1 2024 interim update reported accelerated strategic spending (noting ReZorce development and capacity additions including a second low-pressure vessel in the USA) to scale sustainable packaging solutions and high-performance polyolefin foams. Source: www.zotefoams.com

This Expanded Polyethylene Market Report provides a comprehensive evaluation covering product types, applications, technologies, regional markets, and end-user industries. The analysis spans multiple foam classifications, including low-density, medium-density, high-density, cross-linked, and non–cross-linked EPE variants. It also covers various product formats such as sheets, rolls, blocks, and molded components, as well as density-specific solutions tailored for packaging, insulation, automotive parts, sports equipment, and industrial cushioning.

The report evaluates regional demand across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, mapping volume consumption trends, industrial activity, regulatory influences, supply chain capabilities, and structural growth drivers in each region. End-user categories include packaging and logistics, automotive manufacturing, industrial machinery, electronics, building and construction, and consumer goods.

Technological insights highlight extrusion optimization, advanced foam cross-linking, additive integration, and automation trends, including CNC shaping, automated molding, and digital quality control. Sustainability-oriented innovations—such as recyclable formulations and closed-loop production systems—are also included to reflect evolving market priorities.

Additionally, the report outlines the competitive landscape, strategic developments, and key manufacturing hubs, while also noting emerging niche segments such as specialized flame-retardant EPE, acoustical insulation foams, and precision-cut foam solutions used in premium electronics and automotive applications. This breadth makes the report a valuable strategic resource for manufacturers, investors, procurement leaders, policymakers, and industry stakeholders seeking detailed insights into the global EPE market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 303.0 Million |

| Market Revenue (2032) | USD 417.9 Million |

| CAGR (2025–2032) | 4.10% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Sealed Air Corporation, Armacell International S.A., Zotefoams plc, Pregis LLC, Kaneka Corporation, Sonoco Products Company, Furukawa Electric Co., Ltd., Wisconsin Foam Products, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |