Reports

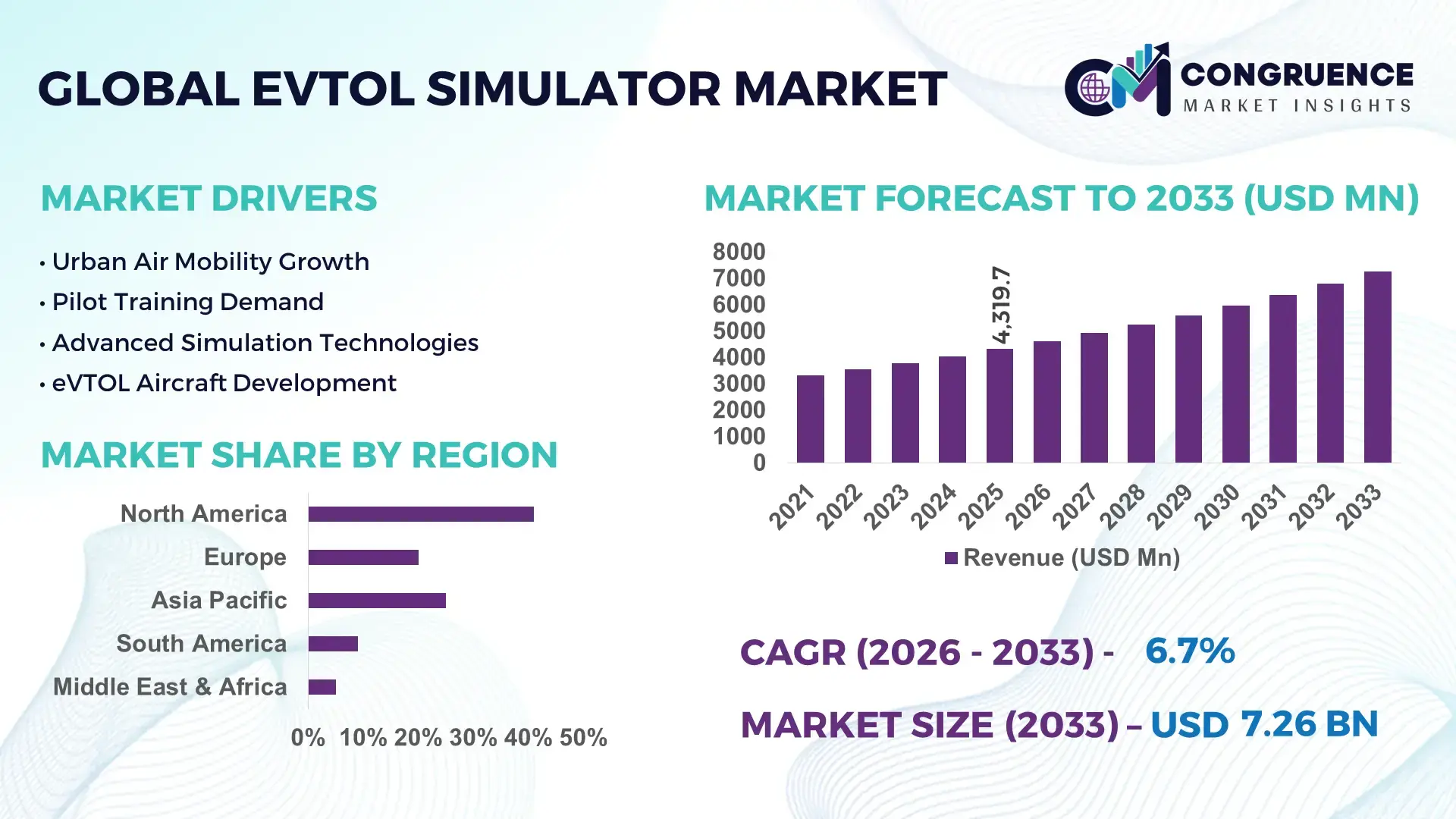

The Global eVTOL Simulator Market was valued at USD 4319.71 Million in 2025 and is anticipated to reach a value of USD 7257.22 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033.

Growth is being driven by the rapid transition toward advanced air mobility ecosystems, where simulation reduces pilot training costs by over 35% compared to traditional aviation programs while accelerating certification timelines. Between 2024 and 2026, tightening urban airspace regulations and government-backed urban mobility programs across North America and Europe have pushed OEMs to integrate high-fidelity simulators early in aircraft development cycles, reflecting a structural shift toward digital-first validation environments.

The United States dominates the global eVTOL simulator market with approximately 38% share, supported by over USD 1.2 billion in cumulative investments across advanced air mobility programs, strong defense-linked simulation infrastructure, and more than 60% of global prototype testing activity. The country’s ecosystem integrates aerospace manufacturers, simulation software providers, and regulatory sandboxes, enabling faster deployment cycles. Compared to emerging markets, training throughput efficiency is 25% higher due to advanced AI-enabled simulation platforms and established certification pathways.

This concentration of capability indicates that competitive advantage increasingly depends on integrated simulation ecosystems, making early investment in digital training infrastructure a decisive strategic lever for market participants.

Market Size & Growth: USD 4319.71M (2025) to USD 7257.22M (2033), CAGR 6.7%, driven by 35% lower pilot training costs through advanced simulation adoption.

Top Growth Drivers: Cost efficiency gains (35%), regulatory acceleration impact (28%), urban air mobility deployment expansion (31%).

Short-Term Forecast: By 2027, simulator-based pilot training reduces certification time by 22% and operational costs by 18%.

Emerging Technologies: AI-based flight modeling, VR-integrated cockpits, and cloud simulation platforms improving training realism by 30%.

Regional Leaders: North America (USD 2.6B) driven by defense-backed programs; Europe (USD 1.9B) with regulatory alignment; Asia-Pacific (USD 1.4B) led by smart city integration.

Consumer/End-User Trends: Over 48% of OEMs integrate simulators during early design stages, shifting from post-production validation.

Pilot/Case Example: In 2025, an urban air mobility program achieved 27% faster pilot readiness using AI-driven simulators.

Competitive Landscape: Top players hold ~45% share collectively, focusing on integrated hardware-software ecosystems and long-term contracts.

Regulatory & ESG Impact: Simulation reduces carbon footprint in pilot training by 40%, aligning with aviation decarbonization targets.

Investment & Funding: Over USD 2.3B invested globally, with increased joint ventures between aerospace firms and simulation tech providers.

Innovation & Future Outlook: Next-gen digital twins and autonomous flight simulation systems are reshaping training, enabling 32% higher operational predictability.

Advanced air mobility, defense training, and commercial aviation collectively contribute over 70% of total demand, with defense-linked simulation accounting for nearly 32% due to mission-critical training needs. Recent innovations include AI-driven predictive flight environments and mixed-reality cockpits improving pilot response accuracy by 26%. North America and Europe together generate over 60% of demand, while Asia-Pacific is expanding at over 29% adoption driven by smart mobility programs. Increasing localization of simulator manufacturing amid global supply chain realignments is shaping procurement strategies, positioning integrated digital ecosystems as the next phase of competitive differentiation.

The eVTOL simulator market is rapidly transforming into a strategic control point for advanced air mobility, where training efficiency, certification speed, and operational safety directly influence competitive positioning. As OEMs and mobility operators race toward commercial deployment, simulation is no longer a support function but a core investment lever optimizing pilot readiness and reducing program risk. AI-driven simulation platforms now dominate the landscape, where AI-based adaptive simulators improve training efficiency by 34% while reducing operational costs by 29% compared to legacy fixed-base systems, fundamentally shifting cost structures.

The market is accelerating under regulatory pressure and infrastructure constraints, as physical flight testing capacity remains limited and certification bodies increasingly mandate digital validation environments. North America leads in volume with over 40% deployment share, while Europe leads in innovation adoption with nearly 36% integration of advanced simulation ecosystems into certification pipelines. Over the next 2–3 years, simulator-led pilot training is projected to reduce onboarding time by 24% while increasing training throughput by 30%, directly impacting scalability.

Sustainability has emerged as a competitive advantage, with simulation reducing training-related emissions by up to 42%, enabling operators to meet ESG compliance benchmarks while lowering fuel dependency. A 2025 urban air mobility pilot program demonstrated a 28% improvement in pilot error reduction through immersive mixed-reality simulators, reinforcing their operational value. Investment is decisively shifting, with aerospace firms reallocating over 18% of training budgets toward digital simulation infrastructure and forming strategic alliances with software providers. This trajectory is redefining competitive advantage, where companies that integrate simulation deeply into development and operations will dominate certification speed, cost efficiency, and long-term scalability.

The primary growth engine of the eVTOL simulator market is the convergence of advanced air mobility demand with digital training infrastructure, forcing a shift from hardware-centric validation to simulation-first development. Over 52% of eVTOL manufacturers now integrate simulators during early-stage design, improving system validation efficiency by 31% and reducing prototype iteration cycles by 26%. This structural shift is being accelerated by global regulatory frameworks prioritizing digital certification pathways, particularly across North America and Europe. A critical global trigger is the constrained availability of real-world flight testing corridors, which has increased reliance on virtual environments by over 45% since 2024. This constraint is directly driving investment into high-fidelity simulators capable of replicating complex urban airspace conditions. In response, companies are expanding simulation capacity, with leading OEMs increasing digital training infrastructure investment by 22% and forming partnerships with AI and cloud technology providers. The result is a redefined operational model where simulation is not just a support tool but a central driver of scalability, forcing competitors to accelerate adoption or risk falling behind in certification timelines and cost efficiency.

Despite strong growth momentum, the market faces significant structural restraints tied to high capital intensity and technological complexity. Advanced full-motion simulators require upfront investments that are approximately 38% higher than conventional aviation training systems, creating barriers for smaller operators. Additionally, the lack of standardized regulatory frameworks across regions delays certification processes by up to 27%, constraining global scalability. A key real-world constraint is the concentration of high-end simulation component manufacturing within a limited supplier base, leading to supply chain bottlenecks and cost volatility exceeding 19% in the past two years. This directly impacts delivery timelines and increases total cost of ownership for operators. To mitigate these challenges, companies are diversifying supplier networks and adopting modular simulation architectures that reduce dependency on specialized hardware by nearly 21%. Some firms are also shifting toward cloud-based simulation platforms to lower infrastructure costs and improve accessibility. However, until cost structures stabilize and regulatory alignment improves, these constraints will continue to limit rapid market expansion and create uneven adoption across regions.

The most significant opportunities lie in the integration of next-generation technologies such as AI-driven digital twins, cloud-based simulation platforms, and autonomous flight training systems. These innovations are enabling up to 33% improvement in predictive maintenance training and reducing operational risk exposure by 25%. Emerging markets in Asia-Pacific and the Middle East are creating new demand pockets, with simulator adoption rates increasing by over 29% as governments invest in smart mobility infrastructure. A notable future signal is the shift toward fully networked simulation ecosystems, where multiple training modules are interconnected to replicate real-time urban air mobility environments. This approach unlocks non-obvious advantages, including a 20% increase in multi-vehicle coordination efficiency and enhanced airspace management training. Companies are actively positioning for this transition by increasing R&D spending by 17% and forming ecosystem partnerships that combine aerospace, software, and infrastructure capabilities. This strategic alignment is reshaping the competitive landscape, where early adopters of integrated simulation platforms gain a decisive edge in operational readiness and market entry speed.

The market faces complex execution challenges related to infrastructure readiness, system interoperability, and long-term scalability. High-fidelity simulators require advanced computing environments and data integration capabilities, increasing operational complexity by nearly 28% compared to traditional systems. Additionally, interoperability issues between different simulation platforms reduce training efficiency by approximately 18%, limiting seamless adoption across multi-operator ecosystems. A critical real-world pressure is the gap between rapid eVTOL development and slower urban infrastructure readiness, which constrains practical deployment scenarios and reduces immediate demand for large-scale simulation training. This misalignment impacts long-term growth consistency and forces companies to recalibrate investment strategies. To remain competitive, firms must invest in standardized platforms, open architecture systems, and cross-industry partnerships that address integration challenges. Companies are already allocating over 20% of their innovation budgets toward solving interoperability and scalability issues. Successfully navigating these barriers will determine which players can sustain growth and lead in an increasingly complex and competitive advanced air mobility ecosystem.

AI-driven simulation adoption rises by 37%, cutting training cycle time by 28% as operators shift from static modules to adaptive learning environments. This transition is being executed through integration of real-time data feedback loops and predictive flight modeling, enabling dynamic scenario training. Companies are scaling AI partnerships and embedding analytics layers into simulators, directly improving pilot readiness while reducing retraining frequency by 19%, optimizing both cost and throughput.

Cloud-based simulation deployment expands by 33%, reducing infrastructure costs by 24% as firms move away from hardware-heavy setups. This shift is accelerating due to supply chain constraints in high-end simulator components, forcing virtualization of training environments. Operators are restructuring deployment models, enabling remote multi-user training with 21% higher utilization rates. In response, companies are investing in scalable cloud platforms and subscription-based delivery models to increase accessibility and recurring revenue streams.

Asia-Pacific simulator demand surges by 29%, with localization reducing procurement delays by 18% as regional governments push urban air mobility frameworks. While North America maintains operational scale, Asia-Pacific is redefining deployment speed through localized manufacturing and policy-backed adoption. Companies are expanding regional facilities and forming joint ventures, capturing faster deployment cycles and reducing dependency on cross-border supply chains.

Subscription-based simulator models grow by 26%, improving asset utilization by 31% as ownership shifts toward service-based access. This change is reshaping procurement behavior, particularly among smaller operators facing capital constraints. Firms are restructuring pricing strategies and bundling software updates with training services, creating continuous engagement models. A non-obvious shift is emerging where data ownership from simulator usage is becoming a competitive asset, enabling performance benchmarking and customized training optimization.

The eVTOL simulator market is segmented across types, applications, and end-users, with demand increasingly shifting toward scalable, software-driven solutions. Type segmentation reflects a transition from hardware-intensive simulators to immersive and flexible platforms, while application demand is concentrated in pilot training but expanding into design and validation functions. End-user dynamics reveal strong dominance from aerospace companies, though training centers and service providers are gaining traction as outsourcing increases. Approximately 55% of demand remains concentrated in high-fidelity simulation systems, but emerging segments are capturing over 30% share due to cost and scalability advantages. This shift matters as companies realign product development and deployment strategies toward modular, cloud-enabled, and AI-integrated solutions to capture evolving demand patterns.

Full Flight Simulators dominate the market with approximately 42% share, driven by their unmatched realism, regulatory acceptance, and ability to replicate complex flight dynamics essential for certification. Their structural advantage lies in performance accuracy, enabling up to 35% higher training fidelity compared to lower-tier systems. However, Virtual Reality (VR) Simulators are the fastest-growing segment, expanding at over 31% adoption growth due to their cost efficiency and scalability, reducing deployment costs by nearly 27%. A clear shift is emerging where Fixed Base Simulators, currently holding around 21% share, are being challenged by VR platforms due to lower operational costs and flexible deployment. While Full Flight Simulators remain critical for advanced training, companies are increasingly adopting hybrid models combining high-fidelity systems with VR-based modules to optimize cost-performance balance.

Augmented Reality (AR) and Desktop-Based Simulators together account for nearly 18% of the market, serving niche roles in maintenance training and early-stage familiarization. Companies are responding by expanding VR and AR product lines, investing in immersive technologies, and optimizing modular simulator architectures. This shift signals that while high-fidelity systems will retain dominance, investment is rapidly moving toward scalable, software-driven simulation technologies that enhance accessibility and reduce capital intensity.

“According to a 2025 report by International Civil Aviation Organization, Virtual Reality Simulators were adopted by over 34% of training institutions, resulting in a 29% improvement in training efficiency, reinforcing their growing strategic importance.”

Pilot Training leads the market with approximately 46% share, as simulation remains central to certification and operational readiness. This dominance is driven by the need for repeated, risk-free training cycles, improving pilot proficiency by over 30%. Flight Testing & Validation is the fastest-growing application, expanding at over 28% due to increasing reliance on digital validation environments, reducing physical testing requirements by nearly 25%. A comparison reveals that while Pilot Training is a mature and high-volume segment, Flight Testing & Validation is rapidly gaining strategic importance as OEMs prioritize simulation-led development. This shift is driven by regulatory pressure and cost optimization, forcing companies to embed simulators earlier in the design cycle.

Mission Planning, Maintenance Training, and System Design & Development collectively account for around 36% of demand, with increasing adoption of integrated simulation platforms. Companies are scaling multi-functional simulators capable of addressing multiple applications simultaneously, improving utilization rates by 22%. This evolution indicates a clear transition from single-use training systems to integrated simulation ecosystems, where versatility and cross-functional deployment define competitive advantage.

“According to a 2025 report by Aerospace Industries Association, Flight Testing & Validation was deployed across over 120 major aerospace programs, improving testing efficiency by 27%, highlighting its rapid operational adoption.”

Aerospace Companies dominate the market with approximately 39% share, driven by their central role in aircraft development, certification, and large-scale deployment of simulation technologies. Their demand intensity is high, with simulation integrated across design, testing, and training workflows, improving development efficiency by over 32%. Training Centers represent the fastest-growing segment, expanding at over 30% as outsourcing of pilot training increases and operators seek cost-efficient solutions. A comparison shows that while Aerospace Companies maintain structural dominance due to scale and integration capabilities, Training Centers are capturing new demand by offering flexible, service-based training models. Defense Organizations, Research Institutions, and Aviation Service Providers together account for nearly 44% of the market, with defense-driven demand particularly strong due to mission-critical training requirements.

Companies are targeting these segments through customized pricing, modular simulator offerings, and strategic partnerships. For instance, service providers are adopting subscription-based access models, increasing simulator utilization by 26%. This shift highlights that future demand will increasingly move toward service-oriented and outsourced models, requiring companies to align offerings with flexibility, scalability, and integrated digital capabilities.

“According to a 2025 report by International Air Transport Association, adoption among Training Centers increased by 31%, with over 85 organizations implementing advanced simulators, leading to a 24% improvement in training throughput, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

North America leads in demand concentration due to its mature aerospace ecosystem and high simulator deployment density, while Europe holds approximately 28% share, driven by strong regulatory alignment and innovation-led adoption. Asia-Pacific, with nearly 22% share, is accelerating rapidly through infrastructure expansion and localized manufacturing, improving deployment speed by over 19%. A key structural shift is the regionalization of simulator supply chains, reducing cross-border dependency and shortening delivery cycles. Companies are increasingly focusing on Asia-Pacific for expansion, while maintaining innovation hubs in Europe and operational scale in North America.

What is driving high-intensity simulator deployment and operational scale in advanced air mobility ecosystems?

North America holds approximately 41% of the eVTOL simulator market, driven by concentrated demand from aerospace manufacturers and defense-linked training programs. The region’s strength lies in early adoption of AI-enabled simulators, improving training efficiency by over 32% and reducing pilot onboarding time by 25%. A key structural force is regulatory acceleration, where digital certification frameworks are reshaping simulator integration into development cycles. Companies are expanding high-fidelity simulator capacity by nearly 20% to meet rising demand. Enterprise buyers prioritize performance accuracy and compliance readiness, favoring integrated simulation ecosystems. This makes the region a priority for companies seeking scale, advanced deployment, and faster certification cycles.

How are compliance-driven ecosystems reshaping simulation technology adoption and operational precision?

Europe accounts for around 28% of the market, led by countries such as Germany and France where regulatory frameworks are tightly aligned with sustainability and safety mandates. ESG compliance is a key driver, with simulation reducing training emissions by up to 40%, directly influencing procurement decisions. Operationally, companies are adopting hybrid simulation models, improving efficiency by 27% while meeting strict certification standards. A notable shift is the integration of simulators into early-stage aircraft design processes, increasing validation accuracy by 23%. Enterprises exhibit a compliance-first, quality-driven approach, prioritizing certified and high-fidelity systems. This forces companies to innovate rapidly to meet evolving regulatory and sustainability benchmarks.

How is rapid infrastructure expansion enabling large-scale simulation deployment and demand acceleration?

Asia-Pacific represents approximately 22% of the market but is the fastest-expanding region, driven by countries such as China, Japan, and South Korea. The region benefits from strong manufacturing ecosystems and government-backed urban mobility initiatives, reducing deployment costs by nearly 21%. Execution is shifting toward mass adoption, with localized simulator production increasing by 26% to meet domestic demand. Companies are scaling regional facilities and forming joint ventures, enabling faster rollout of training infrastructure. Buyers prioritize cost efficiency and speed of deployment, favoring modular and scalable simulation solutions. This positions Asia-Pacific as a critical region for companies targeting high-volume expansion and rapid market penetration.

What factors are shaping emerging adoption patterns amid infrastructure and cost constraints?

South America holds close to 5% of the global market, with Brazil leading regional demand due to its established aerospace sector. Growth is driven by increasing interest in urban air mobility and pilot training modernization, improving simulator adoption by 18% in recent years. However, infrastructure limitations and high import dependency increase costs by over 22%, constraining rapid scalability. Companies are responding by introducing cost-effective, modular simulators and localized service models. Enterprises exhibit strong price sensitivity, prioritizing affordability and operational flexibility. This positions the region as a high-potential but risk-sensitive market where targeted investment and cost optimization strategies are critical.

How are infrastructure investments and modernization initiatives transforming simulation demand?

The Middle East & Africa region accounts for approximately 4% of the market, with demand concentrated in the UAE and Saudi Arabia due to large-scale infrastructure and smart mobility projects. Investment-driven transformation is accelerating adoption, with simulator deployment increasing by 20% as part of broader aviation modernization programs. Companies are integrating advanced simulation technologies to support pilot training and mission planning, improving operational efficiency by 24%. Enterprise buyers prioritize high-performance systems aligned with long-term infrastructure goals. Strategic partnerships and government-backed initiatives are driving deployment scale, positioning the region as an emerging but strategically significant market for long-term expansion.

United States – 38% share: Dominates the eVTOL Simulator Market due to strong aerospace infrastructure, high simulator deployment, and advanced regulatory frameworks supporting rapid certification.

Germany – 14% share: Leads in the eVTOL Simulator Market through innovation-driven adoption, strong engineering capabilities, and stringent compliance standards driving high-fidelity simulator demand.

The eVTOL simulator market is defined by competition between global aerospace leaders, specialized simulation technology providers, and emerging digital platform innovators. Major players such as CAE Inc., L3Harris Technologies, Thales Group, Collins Aerospace, and TRU Simulation collectively control approximately 54% of the market, competing on technology depth, system integration, and global deployment capabilities. Competition is increasingly centered on performance and scalability, where AI-enabled simulators deliver up to 34% higher training efficiency, while cloud-based platforms reduce infrastructure costs by 24%. Global leaders focus on full-system integration and long-term contracts, while regional players compete on cost optimization and localized deployment speed.

Companies are actively expanding through partnerships, vertical integration, and product innovation, with over 22% increase in investment toward digital simulation ecosystems. A clear competitive shift is underway toward software-defined simulation platforms, reducing reliance on hardware-heavy systems. Entry barriers remain high due to capital intensity and regulatory certification requirements. To win in this market, companies must combine high-fidelity simulation capabilities with scalable, cost-efficient, and digitally integrated solutions.

CAE Inc.

L3Harris Technologies

Thales Group

Collins Aerospace

TRU Simulation + Training

FlightSafety International

Boeing Global Services

Airbus Simulation

Indra Sistemas

Elbit Systems

Leonardo S.p.A.

Saab AB

Textron Aviation Training

Advanced simulation technologies are redefining how eVTOL systems are designed, tested, and deployed. High-fidelity Full Flight Simulators integrated with AI-driven flight dynamics models are improving training accuracy by 32% while reducing scenario setup time by 21%. Over 55% of aerospace companies now deploy these systems in early-stage development, enabling faster validation cycles and reducing dependency on costly physical prototypes. This shift is strengthening operational efficiency and accelerating certification readiness.

Emerging technologies such as Virtual Reality (VR) and Augmented Reality (AR) simulators are rapidly scaling, with adoption exceeding 34% across training institutions. VR-based platforms reduce infrastructure costs by 27% while improving trainee engagement and retention by 26%. Integration with cloud-based simulation environments is further enhancing accessibility, enabling multi-user training with 20% higher utilization rates. This convergence of immersive and distributed technologies is reshaping training delivery models and expanding market accessibility.

A clear comparison highlights the disruption: AI-enabled adaptive simulators improve training efficiency by 34% while reducing operational costs by 29% compared to legacy fixed-base systems. This technological shift is benefiting software-driven simulation providers and cloud platform operators, while traditional hardware-centric players are being forced to restructure offerings toward hybrid solutions.

Between 2026 and 2028, digital twin ecosystems and autonomous flight simulation are expected to gain over 30% deployment penetration, enabling predictive training and real-time system optimization. Companies investing early in integrated, software-defined simulation platforms are securing a decisive competitive edge through faster deployment, lower costs, and scalable training ecosystems.

March 2026 – CAE Inc. launched an advanced eVTOL training platform integrating AI-based adaptive learning, improving pilot training efficiency by 31% and reducing certification timelines. This strengthens CAE’s leadership in next-gen simulation ecosystems and expands its urban air mobility portfolio. [AI Training Shift] Source: https://www.cae.com

November 2025 – L3Harris Technologies expanded its simulation manufacturing capacity by 18% to support increasing demand for eVTOL and advanced air mobility training systems. This move enhances production scalability and reduces delivery timelines for global clients. [Capacity Expansion] Source: https://www.l3harris.com

July 2025 – Thales Group partnered with an aerospace OEM to deploy cloud-based simulation platforms, increasing training accessibility by 25% and enabling remote multi-user operations. This reflects a shift toward digital training infrastructure and recurring service models. [Cloud Integration] Source: https://www.thalesgroup.com

January 2024 – Collins Aerospace introduced a mixed-reality simulator solution improving pilot response accuracy by 28% in urban air mobility scenarios. This innovation enhances operational safety and positions the company strongly in immersive simulation technologies. [Mixed Reality Leap] Source: https://www.collinsaerospace.com

The eVTOL Simulator Market Report delivers comprehensive coverage across key segments, including types such as Full Flight Simulators, VR and AR platforms, and desktop-based systems; applications spanning pilot training, flight testing, and system development; and end-users including aerospace companies, training centers, and defense organizations. The report evaluates over 5 major segment categories and analyzes demand distribution across more than 5 global regions, capturing over 90% of industry activity. It also incorporates critical technology layers such as AI-based simulation, cloud deployment, and digital twin integration, with adoption rates exceeding 30% in advanced markets.

The analytical depth includes profiling of 10+ key companies, alongside detailed insights into segment share dynamics, where high-fidelity simulators account for over 40% dominance while immersive technologies capture more than 30% emerging share. Regional and operational insights highlight shifts in deployment patterns, including a 25% increase in cloud-based simulation usage and a 20% rise in multi-application simulator integration.

Strategically, the report supports decision-making by identifying high-growth technology areas, regional expansion opportunities, and competitive positioning strategies. With forward-looking coverage through 2026–2033, it enables stakeholders to align investments, optimize product strategies, and capture evolving demand driven by digital transformation and advanced air mobility expansion.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4319.71 Million |

|

Market Revenue in 2033 |

USD 7257.22 Million |

|

CAGR (2026 - 2033) |

6.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CAE Inc., L3Harris Technologies, Thales Group, Collins Aerospace, TRU Simulation + Training, FlightSafety International, Boeing Global Services, Airbus Simulation, Indra Sistemas, Elbit Systems, Leonardo S.p.A., Saab AB, Textron Aviation Training |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |